Reports

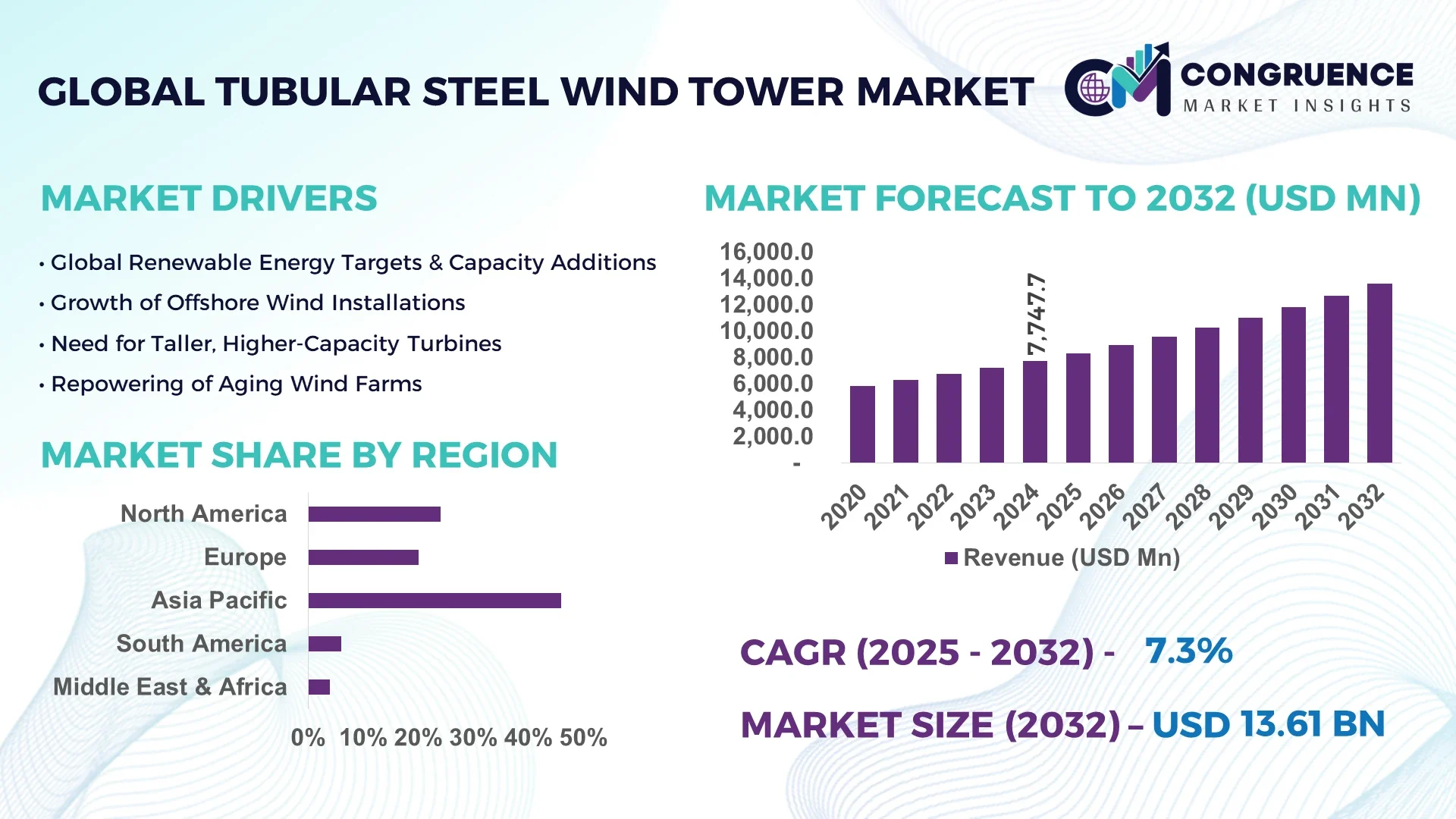

The Global Tubular Steel Wind Tower Market was valued at USD 7,747.7 Million in 2024 and is anticipated to reach a value of USD 13,613.53 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032.

China leads the market with expansive production infrastructure, pioneering investment in ultra-tall tubular steel towers, and deployment across offshore and onshore wind applications. Its production capacity includes factories capable of manufacturing towers exceeding 150 meters, coupled with substantial state-backed funding and continuous advancements in automated welding, corrosion-resistant coatings, and modular fabrication techniques.

Across key sectors—onshore utility projects, offshore wind farms, distributed rural installations, and industrial power systems—the market is shaped by robust demand. Recent innovations include advanced tube-forming robotics, lightweight high-strength steel grades, and modular tower sections for rapid deployment in remote regions. A favorable mix of regulatory support encouraging renewable infrastructure investment, carbon emission targets, and sustainability mandates is boosting demand. Economically, falling steel costs, improved project financing, and economies of scale are enabling broader adoption. Regionally, Asia-Pacific consumption continues to climb rapidly, while emerging markets in Latin America and Africa are beginning to invest in medium-height towers. Trends point toward taller towers, digital manufacturing, integration with turbine design, and enhanced environmental performance through recyclable materials and lower-carbon production processes.

The Tubular Steel Wind Tower Market is undergoing a transformative shift as AI integrates into manufacturing, design, operations, and maintenance. AI-driven automation and smart manufacturing systems are improving production throughput and consistency across tower fabrication, with automated welding, quality inspection, and real-time defect detection reducing manual labor and errors. In design, AI-enhanced optimization tools, including generative design and surrogate modeling, are enabling structurally efficient towers with reduced material use and faster design cycles by simulating hundreds of design iterations virtually. During operations, AI-powered monitoring systems—leveraging sensor data and predictive analytics—enhance preventive maintenance for towers, enabling early detection of stress, fatigue, or corrosion, which improves reliability and reduces downtime.

AI-based digital twins and real-time simulation platforms are enabling virtual testing under variable wind loads, environmental factors, and dynamic stressors, guiding adaptive maintenance strategies and informing future tower enhancements. These technologies raise structural resilience and extend asset lifespan. Overall, AI elevates production efficiency, design precision, and operational performance—positioning the Tubular Steel Wind Tower Market as more agile, cost-effective, and intelligent in meeting global renewable energy infrastructure demands.

“In 2025, GE Vernova deployed AI-powered robotic crawlers and computer-vision algorithms to inspect the interior of wind turbine blades, automatically detecting microscopic deviations and issuing digital quality certificates—streamlining inspection cycles to under 30 minutes per blade while ensuring consistent manufacturing standards.”

The Tubular Steel Wind Tower Market is shaped by a combination of technological advancements, policy frameworks, global renewable energy targets, and evolving industry supply chains. Increasing investments in wind energy infrastructure, driven by decarbonization goals, have amplified demand for taller, more efficient towers that enhance energy capture. Industry trends point towards the adoption of advanced steel alloys, automated manufacturing, and modular construction methods to reduce costs and installation times. Government incentives, carbon-neutral energy mandates, and grid expansion initiatives in emerging economies are creating favorable conditions for market growth. Additionally, offshore wind projects are pushing the design and production of extra-large tubular steel towers, influencing innovation across the sector.

Technological innovations are significantly influencing the Tubular Steel Wind Tower Market, particularly the development of high-strength, low-alloy steels and precision manufacturing techniques. These advancements allow the production of taller towers exceeding 150 meters, which improve wind turbine efficiency by accessing stronger and more consistent wind speeds. Automated welding, robotic fabrication, and advanced corrosion-resistant coatings are reducing manufacturing defects and extending product lifecycles. For example, the adoption of seamless steel tube rolling and modular assembly has cut production timelines by over 20% in certain facilities. These process improvements lower operational costs for developers and increase deployment feasibility in both onshore and offshore environments, reinforcing the market’s competitive edge.

A primary restraint for the Tubular Steel Wind Tower Market is the significant upfront investment required for production facilities, installation equipment, and specialized logistics. The manufacturing of large-scale towers demands heavy infrastructure, precision engineering, and compliance with stringent safety standards, which increases capital expenditure. Additionally, steel price volatility—driven by fluctuations in raw material costs and global trade dynamics—creates uncertainty for project developers and manufacturers. For example, sudden spikes in steel prices can elevate tower production costs by 10–15%, impacting profitability and delaying project timelines. These cost pressures often discourage smaller developers from entering the market and can slow expansion in regions with limited financial incentives.

The Tubular Steel Wind Tower Market has a significant growth opportunity in offshore wind development, particularly in emerging economies such as Vietnam, Brazil, and South Africa. Governments in these regions are introducing long-term renewable energy targets and providing incentives for offshore wind farm investments. Tubular steel towers are ideally suited for the harsh marine environment due to their structural integrity, corrosion resistance, and capacity to support large turbines. Advancements in transport and assembly technology, such as floating crane systems, are making offshore installations more feasible. Projections indicate that global offshore capacity could triple by 2030, creating sustained demand for extra-tall, heavy-duty tubular steel towers.

One of the major challenges in the Tubular Steel Wind Tower Market is the logistical complexity of transporting large tower sections from manufacturing facilities to installation sites. Towers exceeding 100 meters in height require specialized transport vehicles, reinforced roads, and in some cases, partial dismantling of infrastructure en route. These challenges are amplified in remote or mountainous regions, where infrastructure limitations increase costs and extend delivery timelines. Offshore projects face additional hurdles with port availability, vessel compatibility, and weather-dependent installation windows. Such logistical constraints not only raise project costs but also limit the feasibility of large-scale deployments in certain geographic areas, impacting market scalability.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is transforming the Tubular Steel Wind Tower market by streamlining manufacturing and installation processes. Pre-bent, cut, and welded tower sections are now produced in specialized facilities using automated machinery, enabling precise tolerances and minimizing on-site assembly work. This approach can reduce installation time by up to 30% and significantly lower labor requirements. In Europe and North America, where wind project timelines are tightly regulated, these innovations are accelerating project delivery and optimizing resource use.

Shift Toward Extra-Tall Towers for Enhanced Energy Capture: Demand for tubular steel towers exceeding 140 meters is increasing, driven by the need to harness stronger, more consistent wind speeds at higher altitudes. Taller towers can boost turbine capacity factors by 10–15%, particularly in low to medium wind regions. Manufacturers are adopting advanced welding techniques, reinforced flange designs, and lightweight high-strength steels to produce these structures without compromising stability. This trend is especially prominent in onshore projects across Asia-Pacific and North America, where land-based wind resources are being maximized.

Integration of Digital Twin Technology in Tower Lifecycle Management: Digital twin platforms are being deployed to simulate, monitor, and optimize the performance of tubular steel towers throughout their lifecycle. By collecting real-time data from embedded sensors, these systems can predict maintenance needs, track structural fatigue, and reduce unexpected downtime. Early adoption in offshore wind projects has demonstrated maintenance cost reductions of up to 25%, enhancing overall project returns. This technology is also enabling data-driven design improvements for future tower generations.

Increased Use of Recyclable and Low-Carbon Steel Materials: Sustainability initiatives are driving the use of low-carbon and fully recyclable steels in tubular steel wind tower production. Advances in electric arc furnace technology and green hydrogen-based steelmaking are lowering the carbon footprint of tower manufacturing. In certain projects, more than 80% of the tower’s steel content is sourced from recycled material. This shift supports environmental compliance and strengthens the market’s alignment with global decarbonization goals, particularly in regions with stringent emissions regulations.

The Tubular Steel Wind Tower market is segmented by type, application, and end-user, each contributing uniquely to the industry’s growth trajectory. Type segmentation ranges from onshore to offshore-specific designs, each optimized for distinct environmental and operational conditions. Application-wise, these towers are deployed in utility-scale wind farms, distributed generation systems, and hybrid renewable installations. End-user segmentation encompasses utility companies, independent power producers, and industrial energy users, each with unique procurement patterns and operational priorities. Onshore towers currently lead due to widespread land-based projects, while offshore installations are seeing rapid adoption driven by deeper water and higher capacity developments. Industrial sectors increasingly seek localized renewable generation, creating niche demand for medium-height modular towers. These segmentation dynamics reflect a diverse and evolving market, shaped by regional infrastructure capabilities, environmental regulations, and technological adoption rates.

Onshore tubular steel towers represent the leading type in the market, largely due to the extensive global deployment of land-based wind farms. Their relatively lower logistical and installation complexities make them the preferred choice for most large-scale projects. Offshore tubular steel towers, although representing a smaller share, are the fastest-growing segment. This surge is fueled by rising investments in offshore wind energy, particularly in Europe, China, and the U.S., where deep-water projects require taller, more robust designs to withstand harsh marine environments. Hybrid and modular designs are also gaining traction, offering flexibility for projects in regions with infrastructure constraints. Medium-height towers serve niche applications in rural and industrial settings where space limitations or wind profile characteristics dictate specific design requirements. Extra-tall towers above 140 meters are increasingly being adopted for low-wind regions to optimize capacity factors, highlighting the market’s focus on efficiency and yield maximization.

Utility-scale wind farms dominate the application segment, accounting for the majority of installed tubular steel towers worldwide. These large projects benefit from economies of scale and contribute substantially to national renewable energy targets. The fastest-growing application segment is offshore wind farms, supported by technological advancements that allow construction in deeper waters and the deployment of high-capacity turbines. Distributed generation systems are also emerging as a key application, particularly in regions where localized energy solutions reduce dependence on centralized grids. Hybrid renewable projects, integrating wind with solar or storage solutions, are leveraging tubular steel towers for their durability and adaptability. Small and community-based wind projects, while holding a smaller market share, maintain relevance in rural electrification initiatives, where modular tower systems provide cost-effective solutions. This application diversity underscores the market’s capacity to serve both large-scale and specialized renewable energy initiatives.

Utility companies remain the leading end-user segment in the Tubular Steel Wind Tower market, leveraging their resources and infrastructure to develop large-scale wind energy projects. Their dominance is reinforced by government partnerships, long-term power purchase agreements, and the ability to manage complex installations. Independent power producers (IPPs) are the fastest-growing end-user category, driven by flexible investment models and the ability to rapidly deploy both onshore and offshore projects. Industrial end-users are increasingly adopting wind energy solutions to reduce operational carbon footprints and secure stable energy costs, often investing in dedicated on-site towers. Community energy cooperatives and local municipalities, while representing a smaller portion of the market, are expanding their footprint in decentralized energy generation. These end-user dynamics are shaped by evolving energy policies, financing mechanisms, and the push for sustainability across industrial and residential sectors.

Asia-Pacific accounted for the largest market share at 46% in 2024 however, South America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2025 and 2032.

The Asia-Pacific region benefits from large-scale manufacturing hubs, abundant steel production capacity, and extensive onshore and offshore wind development projects. China, India, and Japan are spearheading turbine installation programs that demand increasingly taller and more efficient tubular steel towers. Government-led renewable energy targets, favorable project financing schemes, and advanced production technologies—such as automated welding and modular assembly—are accelerating regional adoption. South America’s rapid growth is supported by significant investments in offshore exploration and hybrid renewable projects, particularly in Brazil and Chile, combined with expanding grid infrastructure to support large-scale wind integration. These market conditions are shaping a dynamic competitive environment where localized production capabilities and technology transfer play key roles.

Advancements in Automated Fabrication and Offshore Expansion

Holding a market share of approximately 24% in 2024, this region is witnessing strong demand driven by utility-scale wind projects in coastal and inland states. The sector is supported by renewable portfolio standards and federal tax incentives promoting clean energy development. Major manufacturing centers in the Midwest are adopting robotic welding, precision steel cutting, and advanced coating technologies to enhance durability and reduce operational costs. Offshore wind expansion in the Atlantic and Pacific is prompting investments in ultra-tall towers capable of supporting high-capacity turbines. Regulatory updates, such as streamlined permitting for renewable projects, are further accelerating adoption across both onshore and offshore segments.

Innovative Steel Alloys and Offshore Leadership

With a market share of 20% in 2024, this region remains a global leader in offshore wind deployment, particularly in Germany, the UK, and France. European Union directives promoting carbon neutrality by 2050 are pushing adoption of tubular steel towers in both offshore and onshore projects. Manufacturers are implementing advanced alloy compositions to reduce weight while maintaining structural strength, enabling taller tower designs. Digital fabrication processes and sustainability-focused initiatives—such as integrating recycled steel into production—are increasingly common. The region’s offshore sector is setting benchmarks in turbine size and installation efficiency, driving demand for robust, corrosion-resistant tower designs.

Large-Scale Production Hubs and Emerging Innovation Centers

Representing the highest market volume globally in 2024, this region’s demand is concentrated in China, India, and Japan, with significant contributions from South Korea and Australia. Large-scale steel production capacity and vertically integrated manufacturing ecosystems are enabling mass production of tubular steel towers. In China, advanced robotic welding lines and modular construction methods are cutting fabrication times significantly. India’s expanding onshore wind sector and Japan’s push for offshore projects are driving technological advancements in tower design and assembly. Regional innovation hubs are experimenting with hybrid steel-composite structures to increase height and reduce maintenance requirements, enhancing long-term operational efficiency.

Offshore Potential and Infrastructure Modernization

In 2024, this region holds around 6% of the global market share, led by Brazil and Argentina. Government-backed renewable energy auctions and tax exemptions for clean energy projects are boosting investment in wind power infrastructure. Offshore wind opportunities, particularly along Brazil’s coastline, are gaining momentum as port facilities upgrade to handle large tower sections. The industrial sector is expanding local manufacturing capabilities to reduce import reliance, while trade policies are facilitating equipment sourcing. Tower designs are being adapted to withstand tropical climate conditions and high coastal humidity, ensuring reliability and performance in challenging environments.

Diversification of Energy Portfolios through Wind Investments

Holding approximately 4% of the global share in 2024, the region’s demand is concentrated in the UAE, Saudi Arabia, South Africa, and Morocco. Energy diversification initiatives are driving investments in wind power alongside solar and hydrogen projects. Modernization of manufacturing facilities is introducing CNC-controlled fabrication lines and advanced corrosion-resistant coatings suited for desert and coastal environments. Local content regulations in several countries are encouraging domestic tower production, reducing dependency on imports. Strategic trade partnerships with Europe and Asia are further strengthening supply chains for wind infrastructure components.

China – 38%

Strong production capacity, extensive onshore and offshore projects, and advanced manufacturing technologies in tubular steel tower fabrication.

United States – 16%

High demand from large-scale utility wind farms, supported by robust renewable energy policies and growing offshore wind initiatives.

The Tubular Steel Wind Tower market features a moderately consolidated competitive landscape, with over 40 active manufacturers and engineering firms operating globally. The market is characterized by the presence of vertically integrated players capable of managing design, fabrication, and installation, alongside specialized companies focusing on high-strength steel production or offshore tower assembly. Leading companies are strengthening their market positioning through strategic joint ventures, regional manufacturing expansions, and the adoption of advanced robotic fabrication lines. Partnerships between steel producers and renewable energy developers are becoming more common, aimed at ensuring steady material supply and reducing production lead times. Recent competitive trends include the introduction of modular tower systems for faster deployment, investments in low-carbon steel manufacturing to align with sustainability mandates, and the integration of digital twin technology for lifecycle management. Offshore project growth, particularly in Europe, Asia-Pacific, and North America, is driving competition for high-capacity tower designs exceeding 150 meters in height, positioning innovation as a critical differentiator in the industry.

Vestas Wind Systems A/S

Siemens Gamesa Renewable Energy S.A.

CS Wind Corporation

Valmont Industries Inc.

Broadwind Energy Inc.

Windar Renovables

Speco Ltd.

Ambau GmbH

Shanghai Taisheng Wind Power Equipment Co., Ltd.

KGW Schweriner Maschinen- und Anlagenbau GmbH

The Tubular Steel Wind Tower market is currently benefiting from breakthroughs in manufacturing precision and material innovation. Higher-grade steels such as S500, costing 20–25% more than traditional S355, deliver up to 30% weight savings due to increased strength, enabling lighter tower sections and reducing transport complexities. Spiral-welded, site-formed towers built using rolled sheet steel eliminate limitations imposed by traditional transportation—you can erect near any turbine hub height with on-site fabrication, requiring up to 80% less labor. Hybrid tower designs are gaining traction, combining concrete foundations with tubular steel upper sections. This hybrid configuration offers enhanced height and stability while retaining corrosion resistance and structural dependability. These assemblies are especially suited to high-load and deep-sea offshore environments where robustness and long-term performance are vital.

Robotic-assisted bending technologies now accommodate precise tube diameters, wall thicknesses, and bending angles, reducing production errors and ensuring consistent tower performance. Companies offering multi-roll bending systems produce steel sections within extremely tight tolerances, supporting the growing demand for modular, multi-piece tubular assemblies. Digital twin platforms and AI-driven structural optimization are reshaping tower lifecycle management. These technologies simulate the performance of towers under complex load profiles, enabling predictive maintenance and guiding material and design improvements. In offshore wind projects, this translates to enhanced structural resilience and reduced unscheduled maintenance. Together, these technological advancements are enabling more efficient, sustainable, and higher-performing tower infrastructure, critical for meeting energy capture and durability demands in wind power deployment.

• In 2023, modular tower systems captured roughly 25% of new installations, reducing transportation costs by nearly 20% and cutting assembly times by approximately 30%, particularly useful in remote and offshore deployments.

• In late 2023, hybrid steel-concrete tower designs gained wider adoption, increasing their representation in new builds by nearly 15%, improving structural stability while lowering raw material usage by approximately 10%.

• In mid-2024, over 40% of new offshore tubular steel towers featured enhanced anti-corrosion coatings, improving service life by nearly 20% and aligning long-term performance with marine durability standards.

• In early 2024, offshore installations accounted for nearly 30% of wind energy projects, with tubular steel towers used in about 60% of these projects, emphasizing their suitability for extreme environments and growing offshore demand.

This report examines the Tubular Steel Wind Tower market across multiple dimensions, including product typologies, regional footprints, application sectors, and technological platforms. The content spans types such as tubular steel, hybrid assemblies, and prefabricated modular towers, each assessed by design, fabrication approach, and performance attributes. Applications are analyzed across onshore, offshore, distributed, and hybrid integration systems, highlighting the adaptability of tower solutions across differing energy infrastructures.

Geographically, the report covers major regions—North America, Europe, Asia-Pacific, South America, Middle East & Africa—detailing manufacturing capacities, consumption volumes, and evolving infrastructure capabilities. Emerging micro-segments, such as lightweight spiral-welded towers and concreting hybrid bottom sections, offer forward-looking insight. Technology facets—including high-strength material usage, robotic bending systems, digital twin integration, and corrosion-resistant treatments—are explored in depth to showcase how innovation is reshaping cost efficiency, operational longevity, and strategic deployment.

Furthermore, the report addresses industry focus areas such as vertical integration models, fabrication and logistics optimizations, and lifecycle management frameworks. Designed for business executives and analysts, its structured layout enables swift navigation through product categories, regional dynamics, use-case scenarios, and future-ready technologies—providing a comprehensive strategic guide without overlap from preceding sections.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 7747.7 Million |

|

Market Revenue in 2032 |

USD 13613.53 Million |

|

CAGR (2025 - 2032) |

7.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Vestas Wind Systems A/S, Siemens Gamesa Renewable Energy S.A., CS Wind Corporation, Valmont Industries Inc., Broadwind Energy Inc., Windar Renovables, Speco Ltd., Ambau GmbH, Shanghai Taisheng Wind Power Equipment Co., Ltd., KGW Schweriner Maschinen- und Anlagenbau GmbH |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |