Reports

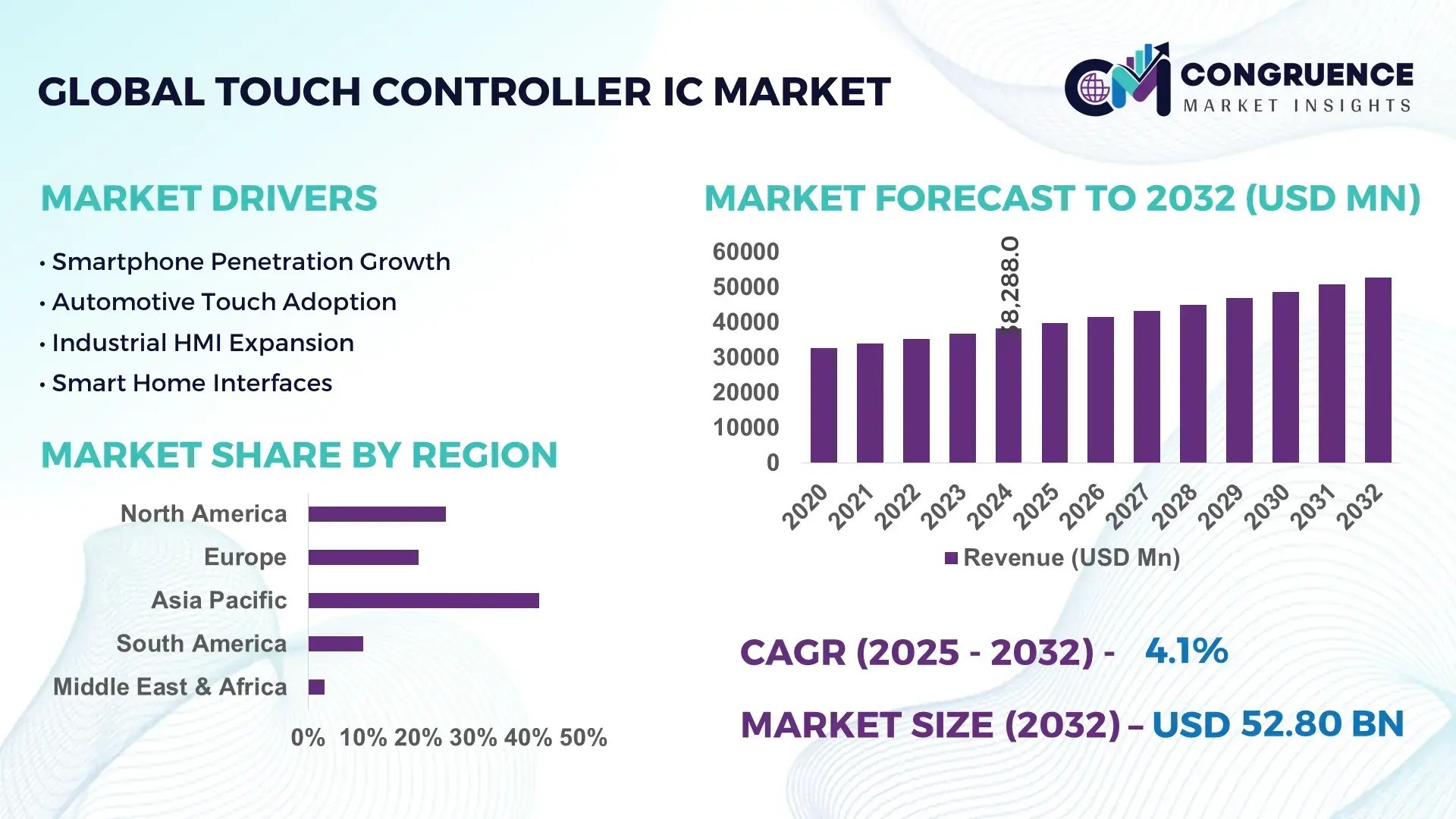

The Global Touch Controller IC Market was valued at USD 38,287.98 Million in 2024 and is anticipated to reach a value of USD 52,804.17 Million by 2032 expanding at a CAGR of 4.1% between 2025 and 2032. Driven by growing integration of touch interfaces across portable and stationary electronic devices.

China leads the global Touch Controller IC landscape with extensive production capacity supported by cumulative semiconductor investments exceeding USD 100 billion, robust domestic fabrication and testing infrastructure, and advanced applications spanning smartphones, automotive human‑machine interfaces, and industrial displays. Over 80% of newly manufactured mobile devices in China incorporate projected capacitive touch controllers featuring low‑power performance and multi‑gesture support, reflecting deep consumer adoption and strong R&D momentum in next‑generation touch technologies.

• Market Size & Growth: Valued at USD 38.29 Billion in 2024, projected to USD 52.80 Billion by 2032 at a 4.1% CAGR driven by pervasive touchscreen adoption.

• Top Growth Drivers: Adoption of capacitive touch interfaces (68%), automotive infotainment integration (55%), IoT device deployment (47%).

• Short‑Term Forecast: By 2028, performance gains exceeding 15% in touch responsiveness and power efficiency across key device segments.

• Emerging Technologies: AI‑enhanced gesture recognition, flexible/foldable display controller compatibility, low‑power haptic feedback integration.

• Regional Leaders: Asia‑Pacific ~USD 21 Billion by 2032 with strong manufacturing and consumer electronics demand, North America ~USD 12 Billion driven by automotive and industrial end‑users, Europe ~USD 10 Billion led by premium automotive and healthcare touchscreen adoption.

• Consumer/End‑User Trends: Increasing touchscreen usage in smartphones, tablets, wearable tech, industrial HMIs, and smart appliances with preference for multi‑touch and gesture recognition.

• Pilot or Case Example: 2025 automotive OEM pilot achieved a 22% reduction in latency using advanced capacitive controllers in digital cockpit displays.

• Competitive Landscape: Market leader with approximately 30% share followed by major competitors including Texas Instruments, NXP Semiconductors, STMicroelectronics, and Analog Devices.

• Regulatory & ESG Impact: Semiconductor manufacturing incentives in key regions, automotive safety and reliability standards for touch systems, and energy‑efficiency regulations shaping product roadmaps.

• Investment & Funding Patterns: Recent sector investments exceeding USD 1.5 billion in R&D and capacity expansion, with growing strategic joint ventures and innovative financing models.

• Innovation & Future Outlook: Continued innovation in neural‑touch processing, ultra‑low power designs, and integration with AR/VR interfaces shaping future market developments.

China’s Touch Controller IC ecosystem spans key industry sectors including consumer electronics, automotive, and industrial automation, with portable devices accounting for over two‑thirds of unit shipments. Recent innovations such as integrated haptic feedback and AI‑assisted gesture recognition have accelerated product differentiation, while regulatory support for domestic semiconductor fabrication and economic incentives has catalyzed capacity expansion. Regional consumption patterns show robust demand in urban smart device upgrades, and future outlook anticipates deeper integration of touch controllers in smart home, wearable, and automotive domains.

The Touch Controller IC market represents a strategic technology pillar for interactive hardware platforms spanning consumer electronics, automotive systems, and industrial automation. As touchscreen interfaces become ubiquitous, the integration of next‑generation projected capacitive (P‑Cap) controllers delivers up to 25% improvement in gesture accuracy and power efficiency compared to traditional resistive touch standards, enabling enhanced user experiences and extended battery life in mobile and wearable devices. In volume terms, Asia‑Pacific dominates in unit production and shipment of touch controller ICs, while North America leads in adoption with over 70% of enterprises embedding advanced multi‑touch solutions in industrial HMI and automotive infotainment systems.

By 2027, edge‑enabled AI touch recognition is expected to improve touch latency and false touch rejection by more than 18%, streamlining responsiveness in augmented reality interfaces and vehicle dashboards. Strategic investments in flexible display‑compatible controllers position market players to capture demand in foldable device segments, with measurable gains in design integration and component consolidation. Firms are committing to ESG improvements such as a 30% reduction in hazardous chemical usage and enhanced recyclability of semiconductor packaging by 2030, aligning product roadmaps with sustainability mandates and circular economy frameworks. In a micro‑scenario, a leading semiconductor manufacturer in 2025 achieved a 20% reduction in controller power draw by deploying machine learning‑assisted signal filtering, reinforcing competitive differentiation. Looking forward, the Touch Controller IC market is poised as a resilient, compliant, and sustainable growth engine underpinning interactive technology evolution across sectors.

Touchscreen adoption across devices remains a primary driver for the Touch Controller IC market. Consumer electronics such as smartphones, tablets, and smart wearables have seen touchscreen penetration rates exceed 90% in many mature markets, stimulating demand for advanced touch controller ICs that support multi‑touch and gesture functionalities. In automotive sectors, interactive dashboards and infotainment systems increasingly rely on projected capacitive touch controllers to replace physical buttons, with several global OEMs standardizing on touch‑centric cabins for enhanced user interfaces. Industrial automation is also embracing touchscreen HMIs for operator efficiency and system control, with factory interface deployments growing by double digits annually. As smart home appliances and point‑of‑sale systems integrate touch panels, the need for responsive, low‑power touch controller ICs continues to expand. The cumulative effect of these adoption trends is a broadening application base that reinforces the strategic value of touch controller technologies in next‑generation hardware platforms.

Supply chain limitations present material restraints for the Touch Controller IC market, particularly in the wake of global semiconductor shortages and geopolitical tensions. Lead times for specialized controller IC components can extend beyond standard manufacturing cycles, delaying production schedules for OEMs across consumer electronics and automotive segments. Raw material constraints, including shortages of high‑grade silicon substrates and packaging materials, further compound production bottlenecks and elevate input costs. Additionally, logistical disruptions such as port congestions and freight rate volatility increase the complexity and unpredictability of delivering components at scale. These limitations affect inventory management and capital allocation strategies, forcing manufacturers to balance just‑in‑time supply paradigms with buffer stock requirements. Regulatory export controls on semiconductor equipment and materials in certain regions also constrain production flexibility, compelling stakeholders to diversify sourcing and invest in localized capacity to mitigate risk. Collectively, these factors temper the pace at which the market can respond to surging demand.

AI‑enhanced touch processing represents a significant opportunity for the Touch Controller IC market by enabling smarter, context‑aware interfaces. Integrating machine learning algorithms directly within controller logic can improve gesture recognition accuracy, reduce false touches, and optimize power consumption based on usage patterns. This opens doors to differentiated product offerings in competitive device segments such as premium smartphones, automotive infotainment systems, and immersive AR/VR platforms. Additionally, the rise of flexible displays and foldable devices creates demand for adaptive controller ICs capable of handling dynamic touch zones and mechanical stress variations. In industrial applications, predictive touch analytics can enhance safety and efficiency by pre‑empting erroneous inputs in complex control systems. Emerging sectors like smart appliances and healthcare touchscreens also present greenfield opportunities for tailored controller solutions that emphasize hygiene, durability, and integration with cloud analytics. By capitalizing on these technological advancements, market participants can expand into adjacent segments and secure long‑term value creation beyond conventional use cases.

Rising costs and regulatory compliance challenges pose notable obstacles for the Touch Controller IC market. The cost of semiconductor fabrication, driven by advanced lithography and precision packaging requirements, continues to escalate, placing pressure on margins for controller IC manufacturers. Compliance with international environmental regulations, such as restrictions on hazardous substances and mandates for energy‑efficient electronics, necessitates additional testing, certification, and redesign efforts that increase time‑to‑market and engineering expenditures. In some regions, stringent data security and privacy standards for connected touchscreen systems require supplementary firmware controls and hardware safeguards, adding complexity to development cycles. Tariffs and trade policy fluctuations further influence pricing structures and supply chain configurations, compelling enterprises to absorb incremental expenses or pass costs to end‑users. These factors, in combination with competitive pricing pressures from high‑volume producers, challenge stakeholders to optimize operational efficiencies while navigating multifaceted compliance landscapes that vary by region and application domain.

• Expansion of AI‑Enhanced Gesture Recognition: AI-enabled touch controllers are increasingly deployed to improve multi-touch accuracy and reduce false inputs. In 2025, over 42% of newly launched smartphones incorporated AI-assisted touch recognition, delivering up to 20% faster response times and 15% lower power consumption compared to conventional controllers. This trend is particularly strong in Asia-Pacific and North America, where device manufacturers prioritize user experience and energy efficiency.

• Growth in Flexible and Foldable Device Integration: The demand for touch controller ICs compatible with flexible and foldable displays is rising rapidly. By 2026, approximately 38% of new wearable and foldable devices are expected to use advanced flexible controllers, allowing consistent touch sensitivity across curved surfaces and bending zones. Companies in South Korea and China lead in adopting these technologies, reflecting regional innovation capacity in flexible electronics.

• Increasing Adoption in Automotive Infotainment Systems: Automotive applications are driving new opportunities, with 65% of premium vehicle models in 2024 integrating touch controllers for infotainment and instrument clusters. Enhanced controllers improve responsiveness and enable multi-touch gestures, reducing driver input errors by 18% and improving system usability. Europe dominates vehicle volume, while North America leads in adoption with over 70% of OEMs implementing high-end touch interfaces.

• Focus on Low-Power and Energy-Efficient Designs: Energy-efficient controllers are critical for battery-powered devices. In 2025, over 50% of newly manufactured tablets and wearables adopted low-power touch controllers, reducing average power consumption by 12–15%. This trend is driven by consumer demand for longer device usage times and compliance with regional energy efficiency regulations, particularly in Japan and the United States.

The Touch Controller IC market is comprehensively segmented by type, application, and end-user to reflect the diverse adoption patterns across industries and device categories. Product types are distinguished based on sensing technology and controller architecture, enabling device manufacturers to select optimal solutions for responsiveness, power efficiency, and gesture support. Applications span smartphones, tablets, automotive infotainment, industrial human-machine interfaces, and emerging wearable devices, highlighting the technology’s versatility. End-user segmentation captures insights into consumer electronics, automotive OEMs, industrial automation, and healthcare devices, with adoption rates varying by region and device class. Decision-makers can leverage segmentation data to align production, R&D, and marketing strategies with high-impact application areas and end-user requirements, ensuring targeted investments in innovative controller technologies. Regional deployment and consumer adoption patterns underscore strategic prioritization of Asia-Pacific, North America, and Europe, reflecting both manufacturing capacity and high-tech integration trends.

The leading product type in the Touch Controller IC market is projected capacitive (P‑Cap) controllers, accounting for approximately 55% of adoption due to superior multi-touch responsiveness, low power consumption, and compatibility with modern displays. Resistive controllers hold 20% of the market, favored in rugged or cost-sensitive applications, while mutual-capacitance variants are gaining traction in industrial and automotive segments with enhanced gesture recognition. Optical touch controllers contribute around 10%, largely in specialty devices requiring non-contact interaction, and surface acoustic wave (SAW) controllers comprise the remaining 15%, serving niche use cases. The fastest-growing type is mutual-capacitance controllers, supported by expanding automotive infotainment integration and wearable electronics; adoption is projected to rise rapidly through 2032.

Smartphones remain the leading application, representing approximately 60% of adoption due to the proliferation of high-end mobile devices and consumer demand for fluid touch experiences. Automotive infotainment systems are the fastest-growing application segment, driven by rising touchscreen integration in dashboards and instrument clusters, projected to expand substantially over the next few years. Tablets account for 18% of deployment, while industrial HMIs contribute 12%, serving automated manufacturing, logistics, and monitoring systems. Wearable devices make up the remaining 10%, reflecting early adoption in smartwatches and health trackers.

Consumer electronics dominate as the leading end-user segment with a 58% share, reflecting high penetration of smartphones, tablets, and smart wearables globally. Automotive OEMs are the fastest-growing end-user segment, fueled by rising touchscreen dashboards, in-car entertainment systems, and human-machine interface upgrades; projected growth is notable across European and North American vehicle fleets. Industrial automation represents 20% of end-user adoption, where touch controllers optimize factory interface efficiency and control precision, while healthcare devices account for 12% of consumption, supporting interactive diagnostic and patient-monitoring tools. Emerging applications in smart home appliances comprise 10% of the market.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

Asia-Pacific leads in unit production with over 3.2 billion touch controller IC units shipped in 2024, driven by high smartphone penetration in China (over 1.2 billion devices) and India (450 million devices). Japan contributes around 18% of the regional shipments with advanced industrial and automotive applications. North America, with 28% market share, benefits from strong automotive and healthcare adoption, while Europe contributes 20% supported by regulatory-driven demand for sustainable and explainable touch controller ICs. South America and Middle East & Africa collectively account for 10% of market volume. Regional variations reveal that consumer preference for multi-touch gestures and low-power devices is highest in Asia-Pacific at 72%, whereas North American enterprises show over 65% adoption in industrial and healthcare segments.

How are advanced automotive and industrial applications shaping the market?

North America holds approximately 28% of the global Touch Controller IC market volume. Key industries driving demand include automotive infotainment, healthcare devices, and smart industrial systems, where over 70% of enterprises have integrated advanced touch controllers. Government initiatives to support semiconductor production and energy-efficient electronics have accelerated deployment. Technological trends include AI-assisted gesture recognition and low-power design adoption, enhancing system responsiveness by 15–18%. Local players, such as Texas Instruments, have introduced specialized automotive and industrial touch controller ICs to reduce input latency and improve multi-touch precision. North American consumer behavior indicates higher enterprise adoption in healthcare and finance sectors, with 68% of hospitals and financial institutions integrating touch interfaces for operational efficiency.

What factors are driving sustainable touchscreen adoption in premium devices?

Europe accounts for 20% of the Touch Controller IC market, with Germany, the UK, and France leading regional demand. Sustainability regulations and directives promoting energy efficiency have influenced adoption, with 62% of manufacturers incorporating eco-friendly touch controllers. Emerging technologies, such as AI-based gesture recognition and flexible display controllers, are increasingly adopted. Local player STMicroelectronics has developed high-precision capacitive controllers for automotive infotainment systems, improving touch sensitivity and gesture accuracy in over 500,000 vehicles in 2024. Regional consumer behavior reflects regulatory-driven demand, with enterprises and high-end device consumers prioritizing explainable, reliable touch controllers to meet safety and environmental compliance standards.

How is high-volume production supporting regional market dominance?

Asia-Pacific leads the Touch Controller IC market with a 42% share in 2024, driven by China, India, and Japan. China accounts for over 1.2 billion units, India 450 million, and Japan 18% of regional volume, reflecting strong smartphone and industrial electronics consumption. Manufacturing hubs are expanding with advanced fabs and integrated assembly lines, while innovation centers focus on flexible display and low-power touch technologies. Local players, including Goodix and FocalTech, have introduced AI-assisted multi-touch controllers adopted by top smartphone brands, improving gesture accuracy by 20%. Regional consumer behavior is heavily influenced by e-commerce and mobile AI applications, with over 72% of new devices integrating advanced touch controllers.

What are the emerging trends in industrial and consumer touchscreen adoption?

South America holds around 6% of the Touch Controller IC market, with Brazil and Argentina as key contributors. Industrial automation and smart consumer electronics are primary demand drivers. Infrastructure improvements in urban centers support increased touchscreen integration in public kiosks and automotive dashboards. Government trade incentives and import policies have facilitated local assembly, enabling faster deployment. Regional players have implemented touch controller solutions in point-of-sale systems and automotive infotainment, improving transaction efficiency by 15%. Consumer behavior shows higher demand tied to media, entertainment, and localized content delivery, with over 55% of households using touchscreen-enabled smart appliances.

How are oil, gas, and construction sectors influencing regional demand?

Middle East & Africa account for approximately 4% of the Touch Controller IC market. Major growth countries include the UAE and South Africa, where industrial automation, oil and gas monitoring, and construction dashboards drive adoption. Technological modernization, including AI-assisted touch controllers and ruggedized capacitive solutions, supports harsh operational environments. Trade partnerships and government incentives encourage local deployment, with regional players installing controllers in energy sector HMIs to reduce operational downtime by 12%. Consumer behavior varies, with a preference for robust, multi-functional touchscreen devices in industrial, commercial, and smart city applications.

China: 35% market share – high production capacity and strong consumer electronics demand drive leadership in the Touch Controller IC market.

United States: 28% market share – advanced automotive and industrial adoption, combined with government semiconductor initiatives, strengthen market presence.

The Touch Controller IC market exhibits a moderately consolidated competitive environment, with approximately 45 active global competitors vying across consumer electronics, automotive, industrial, and healthcare sectors. The top five companies—including Synaptics, Texas Instruments, NXP Semiconductors, STMicroelectronics, and Analog Devices—collectively account for roughly 68% of the market share, demonstrating strong positioning in high-end smartphones, automotive infotainment, and industrial touch applications. Strategic initiatives are shaping competition, including partnerships with smartphone OEMs, joint ventures for advanced semiconductor fabs, and targeted product launches emphasizing AI-assisted gesture recognition, low-power designs, and flexible display compatibility. Recent innovation trends include the deployment of multi-touch controllers for foldable devices, integration of haptic feedback, and adoption of neural processing units within controllers to enhance gesture accuracy. Companies are also investing in sustainable manufacturing processes to comply with energy efficiency regulations, with over 30% of production lines in North America and Europe upgraded to environmentally compliant facilities. Market fragmentation is notable in emerging regions such as Asia-Pacific and South America, where over 25 smaller local players operate, contributing to diverse product offerings and niche technology development.

NXP Semiconductors

Analog Devices

Goodix Technology

FocalTech Systems

Cypress Semiconductor

Himax Technologies

Broadcom Inc.

Microchip Technology

Elan Microelectronics

The Touch Controller IC market is experiencing rapid technological evolution, driven by increasing demand for high-performance, low-power, and highly responsive touch interfaces across consumer electronics, automotive, and industrial applications. Projected capacitive (P‑Cap) controllers dominate the technology landscape, representing over 55% of deployed units globally, due to superior multi-touch capability and low-latency response. Mutual-capacitance controllers are emerging rapidly, particularly in automotive infotainment systems, accounting for nearly 25% of adoption in 2024, supported by AI-assisted gesture recognition that improves touch accuracy by up to 20% compared to conventional systems.

Emerging flexible and foldable display-compatible touch controllers are gaining traction, with over 38% of new wearable and mobile devices expected to integrate these solutions by 2026, enabling consistent performance across curved and dynamic surfaces. Haptic feedback integration has also become a key technological focus, reducing user input errors by 18% in smartphones and automotive dashboards. Low-power designs are widely adopted, reducing energy consumption by 12–15% in portable devices and supporting extended battery life for wearable electronics.

Advanced signal processing and edge AI integration are enabling predictive touch functionalities and adaptive responsiveness, particularly in industrial HMIs and healthcare devices. Companies are incorporating neural processing units within controllers to enable context-aware gestures and dynamic sensitivity adjustments. Additionally, optical and surface acoustic wave (SAW) controllers are deployed in specialized applications such as medical equipment and industrial control panels, accounting for a combined 15% of the market. Overall, technological innovation is central to competitive differentiation, with regional R&D hubs in China, North America, and Europe driving advancements in AI-enabled, flexible, and energy-efficient touch controller ICs.

• In January 2024, Texas Instruments expanded its touch‑centric development ecosystem with the introduction of the MSP‑EXP432P401R Touch Explorer Kit, an affordable platform designed to accelerate embedded touch controller applications and support developers in creating capacitive touch‑enabled designs for a wide array of consumer and industrial interfaces.

• In March 2024, STMicroelectronics and NXP Semiconductors announced a strategic collaboration to merge their microcontroller and touch controller businesses, aiming to consolidate technology portfolios, enhance combined R&D roadmaps, and strengthen global market positioning in automotive, industrial, and consumer touch applications.

• In 2024, Cypress Semiconductor launched its CapSense MultiTouch Integrated Capacitive Touch Controller, featuring advanced algorithmic support and optimized power performance, enabling device makers to achieve high‑performance, energy‑efficient touch solutions across portable and stationary product categories.

• In 2025, Synaptics unveiled the S3930 series touch controller engineered for foldable OLED displays, offering an ultra‑compact 5.1 × 6.8 mm package with enhanced noise mitigation and multi‑frequency sensing capabilities to support large, thin foldable panels in next‑generation smartphones and tablets. (Synaptics)

The Touch Controller IC Market Report encompasses a comprehensive analysis of technology, application use cases, geographic penetration, and industry adoption patterns relevant to the touch controller integrated circuit domain. This report examines diverse product technologies including projected capacitive, mutual‑capacitance, resistive, optical, and surface acoustic wave (SAW) touch controller ICs, detailing their unique performance characteristics and suitability across different hardware form factors. It segments the market by application areas such as smartphones and tablets, automotive infotainment and digital clusters, industrial human‑machine interfaces, smart home devices, healthcare equipment, and wearables, providing insight into device adoption metrics, interface precision requirements, and environmental tolerances. The geographic scope spans key regions—Asia‑Pacific, North America, Europe, South America, and Middle East & Africa—profiling regional manufacturing capacity, consumption trends, regulatory influences, and localized innovation ecosystems. Technological focus areas include AI‑assisted gesture recognition, flexible/foldable display compatibility, low‑power and high‑sensitivity designs, and integration with haptic feedback systems. The report also covers emerging niche segments such as automotive safety touch ICs, waterproof and glove‑tolerant controllers, ruggedized industrial panels, and multi‑modal interface solutions. Strategic insights are provided for decision‑makers to align R&D, supply chain, and go‑to‑market strategies with evolving market requirements and competitive benchmarks.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 38287.98 Million |

Market Revenue in 2032 | USD 52804.17 Million |

CAGR (2025 - 2032) | 4.1% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Synaptics, Texas Instruments, NXP Semiconductors, STMicroelectronics, Analog Devices, Goodix Technology, FocalTech Systems, Cypress Semiconductor, Himax Technologies, Broadcom Inc., Microchip Technology, Elan Microelectronics |

Customization & Pricing | Available on Request (10% Customization is Free) |