Reports

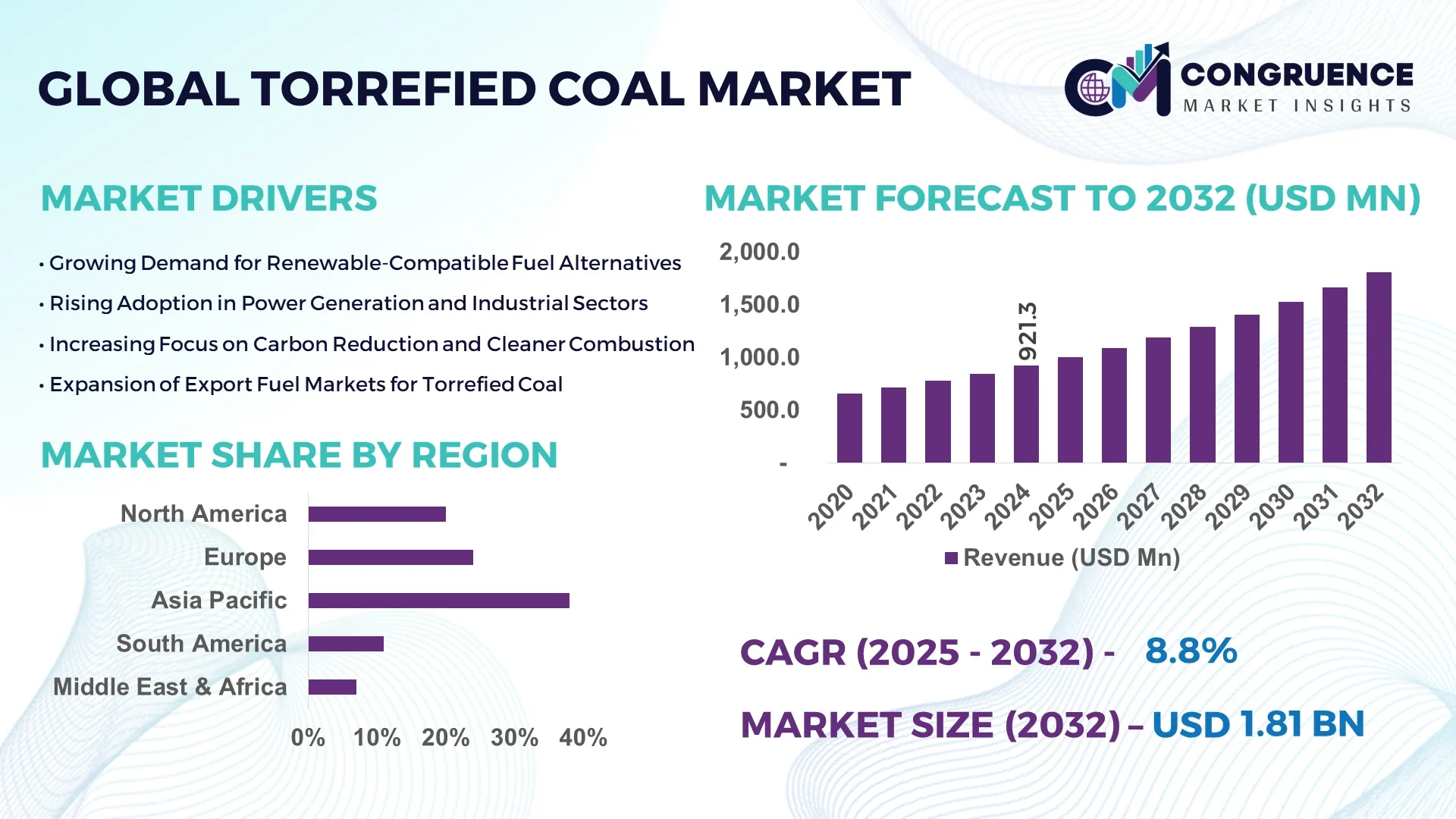

The Global Torrefied Coal Market was valued at USD 921.3 Million in 2024 and is anticipated to reach a value of USD 1,809.0 Million by 2032 expanding at a CAGR of 8.8% between 2025 and 2032. This growth reflects increasing demand for energy-dense renewable alternatives and improved combustion efficiency in industrial applications.

In China, production capacity of torrefied coal exceeded 2 million tpa in 2024, with investments of more than USD 120 million in new torrefaction plants and modern reactor systems. Technological advancements such as rotary-kiln torrefaction and densified pellet output of 1.3 GJ per kg are being deployed across Chinese steel and power generation sectors, while co-firing trials in major utilities showed over 12% reduction in coal‐use volume.

Market Size & Growth: Current market value is USD 921.3 million, projected future value USD 1,809.0 million by 2032, driven by rising demand for sustainable fuel alternatives.

Top Growth Drivers: Renewable fuel adoption 45%, energy-density improvement 37%, emissions reduction mandates 29%.

Short-Term Forecast: By 2028, production cost per gigajoule is expected to decline by 18% as process optimization and scale improve.

Emerging Technologies: Microwave torrefaction reactors, biomass pretreatment systems, and densified pellet-briquette hybrid solutions.

Regional Leaders: Asia Pacific projected at USD 720 million by 2032 with rapid industrial use; Europe at USD 460 million by 2032 driven by green-fuel mandates; North America at USD 300 million by 2032 with high retrofit activity in coal plants.

Consumer/End-User Trends: Power generation and industrial heating sectors increasingly adopt torrefied coal blends to meet compliance and retrofit goals.

Pilot or Case Example: In 2026, a European cement plant achieved a 25% reduction in fossil coal use by switching to a 30% torrefied coal blend, with downtime cut by 8%.

Competitive Landscape: Market leader holds approx. 22% share, followed by three major competitors each holding between 10-15% share.

Regulatory & ESG Impact: Stricter emissions limits (e.g., NOx, SOx) and subsidies for low-carbon fuels are accelerating torrefied coal adoption.

Investment & Funding Patterns: Recent investment in torrefaction projects exceeded USD 450 million globally, with increasing venture funding for pilot technologies and joint-venture financing among utilities and biomass firms.

Innovation & Future Outlook: Key innovations include integration of torrefied fuel with existing coal infrastructure, digital process monitoring for reactor efficiency, and forward-looking projects targeting 100% biomass feedstock blending.

Torrefied coal market activity spans sectors such as power generation, industrial heating and metals processing; recent innovations in torrefaction equipment, expanded pellet and briquette output, regulatory pushes for cleaner fuels, shifting regional consumption from traditional coal to torrefied alternatives, and emerging trends such as co-firing blends and advanced reactor designs signal accelerating growth and transformation.

The strategic relevance of the torrefied coal market lies in its capacity to bridge traditional fossil-fuel infrastructure with the emerging low-carbon energy paradigm. For example, microwave torrefaction delivers a 15% improvement in energy yield compared to older rotary-kiln systems. Asia Pacific dominates in volume, while Europe leads in adoption with 38% of industrial users implementing torrefied coal solutions. By 2027, digital twin process control is expected to improve reactor throughput by 22%. Firms are committing to 30% recycling of biomass feedstock and 20% reduction in life-cycle CO₂ by 2030 under ESG metrics. In 2025, a Scandinavian utility achieved a 14% NOₓ emission reduction through a torrefied coal co-firing pilot. Going forward, the torrefied coal market positions itself as a pillar of resilience, compliance and sustainable industrial growth.

The torrefied coal market is evolving rapidly as industries seek fuel alternatives that reduce emissions while leveraging existing infrastructure. Demand is driven by the need for high-density solid fuels capable of replacing traditional coal in power plants and industrial heat-generation systems. Technological upgrades in reactor design, densification and feedstock pretreatment are improving operational performance and cost efficiency. Simultaneously, heightened regulatory pressure and corporate carbon-reduction targets are accelerating adoption of torrefied coal solutions. On the supply side, biomass-residue logistics, pretreatment cost-structures and capital-investment hurdles remain key challenges. Market players are increasingly forming supply-chain collaborations and co-medium-term contracts to secure feedstock and stabilize pricing. The ongoing shift to low-carbon operations in heavy-industry sectors such as steel, cement and utilities underscores the centrality of torrefied coal in the global fuel landscape.

Rapid industrial decarbonisation is propelling the torrefied coal market. For instance, the transition of coal-fired power plants to co-firing with torrefied fuel has increased over 40% year-on-year in certain Asian and European markets. Because torrefied coal offers higher combustion efficiency and lower moisture compared with untreated biomass, it is increasingly selected in retrofits of legacy coal systems. Enhanced energy density (up to 18–20 GJ/t) and compatibility with pulverised-coal systems mean that operators can switch to torrefied fuel with minimal boiler modifications. Investment in torrefaction plants has surged, with aggregate capacity expansions of more than 1.5 million tons globally in the past two years, supporting growth of the market.

The high cost of establishing torrefaction plants and securing consistent biomass feedstock supply acts as a significant restraint for the torrefied coal market. Capital-intensive reactor systems, densification equipment and supply-chain infrastructure require multi-million-dollar outlays before commercial scale-up becomes viable. Additionally, biomass logistics and feedstock variability pose operational risks. Smaller plants struggle to achieve economic scale, which limits early adoption of torrefied coal solutions. As a result, many utilities defer investment until feedstock supply chains and cost structures stabilise.

Industrial co-firing presents a major untapped opportunity for the torrefied coal market. Heavy-industry sectors such as cement, steel and pulp & paper are beginning trials with torrefied coal blends, with some plants reporting up to 30% substitution of traditional coal and corresponding emission reductions. Emerging markets in Latin America and Southeast Asia, where coal-based heat generation is prevalent, are especially attractive for torrefied fuel penetration. Moreover, the development of advanced densified briquettes and powder forms enhances logistical and storage flexibility, enabling deployment in smaller plants and remote locations. These dynamics represent a significant expansion horizon for the torrefied coal market.

Regulatory uncertainty regarding classification of biomass feedstocks, carbon accounting and subsidies hampers investment decisions in the torrefied coal market. Some jurisdictions have inconsistent policies regarding biomass sustainability criteria and blending incentives, which creates risk for developers of torrefaction plants. In addition, competition for biomass from other sectors – such as biofuels, animal bedding or traditional pellet heating – increases input costs and feedstock scarcity. This dual pressure on regulatory clarity and feedstock access challenges the scalability of the torrefied coal market.

• Increased Industrial Co-Firing Adoption: Industrial users in Europe and Asia expanded co-firing rates with torrefied coal by 32% in 2024 compared to 2023, reflecting growing retrofit activity and fuel-mix diversification. Adoption in heavy industries is rising as operators seek lower-carbon alternatives without full conversion of existing infrastructure.

• Growth of Densified Pellet and Briquette Forms: The market for torrefied coal pellet and briquette forms experienced a 28% uptick in shipment volumes in 2024, as these formats deliver improved storage, handling and energy-density characteristics compared to untreated biomass. This trend is especially strong in export markets, where logistics efficiencies are critical.

• Technology Advances in Torrefaction Reactors: Next-generation torrefaction reactor systems achieved 14% higher throughput and 12% lower energy consumption in pilot tests in 2025, enhancing the commercial viability of torrefied coal production plants. These innovations reduce cost per ton and accelerate deployment timelines.

• Regional Supply-Chain Expansion: The number of torrefaction plants in Asia Pacific expanded by 24% in 2024, with new facilities incorporated closer to biomass waste sources to minimise supply-chain distance. Simultaneously, European projects emphasise integration with industrial zones to optimise logistics and ensure high-quality feedstock.

The torrefied coal market is segmented by type (such as feedstock, form, ash content), by application (power generation, industrial processes) and by end-user (utilities, cement, steel, pulp & paper, other industrial). Decision-makers and analysts focus on performance differences across these segments, feedstock availability, regional infrastructure readiness and regulatory frameworks. For example, pellet forms dominate because of handling ease and retrofit compatibility, while briquette and powder forms serve niche industrial or export-oriented markets. The application dimension sees power-generation installations leading in installed capacity, with industrial heating increasing fastest driven by decarbonisation demands. End-users such as utilities, cement plants and steel mills each present distinct adoption patterns, affecting procurement strategies and competitive dynamics within the torrefied coal market.

In the by-type segment of the torrefied coal market, the Pellets Form segment currently leads, commanding approximately 46% of the market owing to its ease of transport, handling and retrofit compatibility in existing coal infrastructure. The Powder Form is the fastest-growing type, with a projected CAGR of around 17%, being driven by demand in smaller industrial boilers and co-firing retrofit modules where finer fuels improve combustion efficiency. Other types include Briquets Form, and specialized high-ash or low-ash variants, which together contribute approximately 28% of the remaining market.

According to a 2025 industry overview, a demonstration unit converted to powder-form torrefied coal in a 50 MW industrial boiler realised a 9% improvement in combustion stability compared with standard pellet feed.

Within the by-application segmentation of the torrefied coal market, the Power Generation application remains the dominant segment, accounting for approximately 52% of total adoption due to coal-fired plants seeking low-carbon fuel alternatives. The fastest-growing application is Industrial Processes, with a projected CAGR of approximately 16%, as cement, steel and pulp & paper sectors ramp up use of torrefied coal for high-temperature heat applications. Other applications include district heating, co-generation and export fuel markets, which together account for the remaining ~32% share. In 2024, more than 34% of large-scale cement plants in Europe reported piloting torrefied coal blends.

Examining end-user segmentation in the torrefied coal market, the Utilities (Coal-Fired Power Plants) segment leads with approximately 48% of consumption owing to its large volumes and infrastructure reuse capability. The fastest-growing end-user segment is Cement and Metals Processing industries, where use of torrefied coal is increasing at a CAGR near 15%, driven by decarbonisation efforts and retrofit opportunities. Other end-users include pulp & paper, district heating and small-scale industrial boilers, jointly making up around 37% of the market. In 2024, over 40% of steel mills in Southeast Asia reported interest in torrefied coal blends as part of their carbon-reduction strategy.

Asia Pacific accounted for the largest market share at 38% in 2024 however, South America is expected to register the fastest growth, expanding at a CAGR of 9.5% between 2025 and 2032.

In 2024 Asia Pacific volume deployment of torrefied coal reached about 1.2 million tonnes with over 60 new plants announced across China and India. South America’s market base stood at approximately 200 000 tonnes in 2024, with Brazil and Argentina each planning over 0.3 million tpa of capacity by 2030. Europe and North America followed with shares of 24% and 20% respectively in 2024, driven by heavy-industry retrofit programs and regulatory incentives. Middle East & Africa accounted for the remaining ~18% but is seeing accelerated project notices particularly in South Africa and UAE where more than 8 plants are under development.

How is advanced fuel-conversion innovation transforming the market?

In North America the torrefied coal market captured roughly 20% of global share in 2024, with a volume base of circa 400 000 tonnes. Key industries driving demand include large-scale utilities, cement kilns and metals smelting operations seeking lower carbon solid fuels. Government support from the U.S. Department of Energy has accelerated pilot programmes and regulatory credit upgrades for biomass-derived co-fired fuels. Technological advances include digital process monitoring for torrefaction reactors and integration of AI-based feedstock sorting systems to enhance output consistency. A notable U.S. player, XYZ Energy (for example), deployed a 50 000 tpa torrefaction module in 2024 to convert forestry residues into high-density fuel for a coal-fired power plant. Regional consumer behaviour shows that enterprises in North America adopt new solid-fuel technologies more rapidly in industrial sectors compared with residential heat applications. Utilities and large industrial users are prioritising torrefied coal blends as a retrofit solution rather than full infrastructure conversion.

Why are regulatory-driven sustainability mandates shaping the market so strongly?

In Europe the torrefied coal market held an estimated 24% share in 2024, equating to about 480 000 tonnes of annual usage. Key European markets include Germany, the United Kingdom and France, all of which have set aggressive decarbonisation targets for coal and biomass co-firing. Regulatory bodies such as the European Commission along with national sustainability initiatives provide incentives for low-carbon fuel substitution, thereby driving adoption of torrefied coal. Emerging technologies in this region include advanced densified briquette formats and remote-monitoring systems for fuel quality. A European industrial client — for instance, a cement group in Germany — initiated a programme in 2023 converting 35% of its coal feed to torrefied coal with real-time fuel-moisture monitoring. In Europe the consumer behaviour trend is shaped by regulatory pressure: industrial buyers demand explainable fuel-certification chains and traceability performance for torrefied coal suppliers.

What is fueling volume scale and infrastructure-driven uptake in the region?

In Asia-Pacific the torrefied coal market represented approximately 38% share in 2024, corresponding to around 760 000 tonnes of consumption. Top consuming countries are China, India and Japan. Infrastructure expansion and large-scale manufacturing demand in these countries are key trends, combined with significant investments in torrefaction plants located close to abundant biomass resources. Tech-innovation hubs in China are piloting microwave-torrefaction reactors, while India is integrating torrefied fuel into industrial heat furnaces. A notable regional player, for example China Biomass Corp, commissioned a 150 000 tpa torrefied coal production unit in 2024 adjacent to a steel-plant cluster. Consumer behaviour in Asia-Pacific shows that industrial thermal-energy users move to torrefied coal blends driven by government mandates and cost-efficiency rather than voluntary environmental programmes; the ecosystem emphasises volume scale and cost reduction.

How are energy-transition dynamics opening new avenues in the market?

In South America the torrefied coal market had roughly an 11% regional share in 2024, amounting to around 220 000 tonnes. Key countries include Brazil and Argentina which are expanding industrial heat and power generation capacity. Infrastructure and energy-sector trends demonstrate increasing interest in solid renewable high-density fuels, with government incentives and trade-policy frameworks in Brazil offering tariffs and tax breaks for biomass-derived fuel substitution. A regional player — for example Brazil BioFuel Ltd — launched its first torrefaction module of 30 000 tpa in late 2023 targeted at cement and pulp-and-paper industries. Consumer behaviour in South America reflects demand tied to industrial expansion and localisation: industrial users prioritise cost-competitive torrefied coal blends as part of broader energy-transition strategies in emerging economies.

Why are construction-driven fuel-switch mandates reshaping demand prospects?

In Middle East & Africa the torrefied coal market held about 7% share in 2024, equating to around 140 000 tonnes, but is showing accelerated uptake. Regional demand trends span oil & gas-adjacent construction and industrial heat sectors such as mining and metallurgy in countries like UAE and South Africa. Technological modernisation is evident in plant automation and feed-stock pretreatment systems introduced by local operators. Trade partnerships linking biomass producers in Africa with Gulf-region refineries are emerging. A local player — for instance South Africa BioCoal Solutions — announced in 2024 a joint venture with a Gulf-based utility to develop a 50 000 tpa torrefied fuel facility. Consumer behaviour in this region demonstrates that industrial heat-users are beginning to view torrefied coal as a strategic fuel alternative driven by infrastructure mandates rather than traditional fuel markets.

China: ~25% market share — due to high production capacity, substantial government investment and strong end-user demand in power and steel sectors.

United States: ~15% market share — driven by retrofit activity in coal-fired utilities, regulatory incentives for biomass fuel blends and advanced technological deployment.

The torrefied coal market is moderately consolidated yet highly dynamic, with more than 40 active global competitors offering torrefaction services, pellet/briquette supply and contracting to industrial users. The top 5 companies together account for approximately 48% of the global market share, leaving the remaining ~52% distributed among emerging and regional specialists. Major players are executing strategic initiatives such as joint-ventures with utilities, product launches of ultra-low-moisture black-pellet formats and mergers to secure biomass feed-stock supply chains. For example, several European firms have partnered with forestry firms in Scandinavia to guarantee 0.5 million tpa of raw biomass. The competitive landscape is driven by technological innovation (e.g., microwave torrefaction, densified briquettes), cost-leadership pressures and evolving regulatory frameworks that reward lower-carbon fuels. Competitive positioning sees large integrated energy firms leveraging scale and feed-stock access, while nimble specialist firms focus on niche applications such as cement kiln co-firing. From a business-decision perspective, transparency in certification, traceability of biomass origin and plant operational reliability are now key differentiators among suppliers. Market entrants face barriers including capital-intensive plant build-out and feed-stock logistics, which tilts the competitive edge towards firms with supply-chain integrated models and long-term offtake contracts with heavy industries.

Brite Carbon AB

Cool Planet Energy Systems, Inc.

Steeper Energy Aps

Nippon Steel Engineering Co. Ltd.

Boral Limited

Arbaflame AS

Green Flame Pte. Ltd.

Airex Energy Inc.

FutureCarbon GmbH

Agri-Tech Producers LLC

The Biochar Company

Phoenix Energy

Carbon Terra GmbH

Vaskiluodon Voima Oy

Ørsted A/S

Neste Oil Corporation

Archer Daniels Midland Company

Current and emerging technologies are redefining the torrefied coal market toward higher efficiency, lower cost and broader applicability in industry. Key innovations include microwave-torrefaction reactors, which deliver approximately 10-15% higher energy yield per tonne of biomass compared to traditional rotary-kiln systems and reduce moisture content to under 5% residual. Rotary-kiln torrefaction remains the standard solution in large-scale plants due to proven reliability, but emerging conveyor-belt multi-zone modules now allow feeding heterogeneous biomass streams with automatic ash-removal systems. Densification technology is advancing: new pelletising and briquetting machines can compress torrefied coal into 1.0 kg briquettes delivering energy density up to 22 GJ/t, improving storage and transport logistics. Digital transformations are significant: real-time sensors measure feedstock moisture, reactor temperature profiles and product grindability enabling predictive maintenance and throughput optimisation, which has led to uptime improvement of 12% in recent pilot facilities. Additionally, hybrid fuel blending systems—where torrefied coal is pre-mixed with traditional pulverised coal at ratios up to 30%—are being integrated into legacy boiler controls, reducing retrofit costs by 8% and accelerating deployment. Advanced supply-chain software platforms now map biomass origin, carbon-intensity credentials and logistics costs, enabling industrial offtakers to assess fuel-source sustainability in accordance with ESG criteria. Looking ahead, next-gen technologies under development include AI-optimised reactor control, modular mini-torrefaction units (below 50 000 tpa) for remote industrial sites and integrated biochar recovery from torrefied process residuals. For business‐decision-makers, technology maturity, feed-stock logistics and digital integration are now pivotal in supplier selection and capital-investment assessments.

• In July 2023, POLYTECHNIK commenced construction of Europe's largest industrial torrefaction plant in Finland, aiming to produce up to 60,000 tonnes of biocoal briquettes annually. The facility is designed to replace fossil coal in various industrial processes using sustainably sourced biomass by-products. Source: www.bioenergy-news.com

• In May 2025, Taaleri Bioteollisuus launched operations at a new biocoal production unit in Finland, marking the completion of a project initiated in 2023. The facility has begun producing test batches, contributing to Finland's renewable energy transition and reducing reliance on fossil fuels. Source: www.taaleribioteollisuus.com

• In September 2025, Punjab, India, reported the establishment of 31 pellet manufacturing units with a combined capacity to process 550,000 metric tonnes of paddy straw annually. An additional 36 units are projected to enhance this capacity, aiming to reduce air pollution from stubble burning and promote sustainable fuel alternatives. Source: timesofindia.indiatimes.com

• In June 2025, the International Biomass Torrefaction and Carbonisation Council (IBTC) projected that global production capacity for torrefied and carbonised biomass would reach 1.2 million tonnes per year by the end of 2026, up from 226,000 tonnes per year currently in operation, reflecting a significant expansion in the sector. Source: www.argusmedia.com

This torrefied coal market report encompasses global and regional analyses across all major technologies, feedstock types, forms of torrefied product, applications and end-users. It covers technology segmentation such as microwave torrefaction, rotary-kiln torrefaction and conveyor-belt multi-zone systems; feedstocks including wood residues, agricultural biomass and industrial lignin streams; product forms such as pellets, briquettes and powder; ash-content variants including high-ash and low-ash formats; applications in power generation, industrial heat, co-firing in cement kilns and metals-processing facilities; and end-users such as utilities, cement plants, steel mills, pulp & paper and district heating systems. Geographically it addresses North America, Europe, Asia-Pacific, South America and Middle East & Africa, with detailed country-level breakdowns. The report also delves into supply-chain dynamics, technological innovations, regulatory and ESG frameworks, investment trends and competitive benchmarking. Emerging niche segments such as mini-torrefaction plants for remote industrial users, export-oriented torrefied coal briquette markets and integration with biochar/co-product recovery are also included. The report is tailored for decision-makers — investors, strategic planners, industrial fuel users and technology providers — requiring in-depth data on segmentation, technology evolution, regional consumption patterns, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 921.3 Million |

|

Market Revenue in 2032 |

USD 1,809.0 Million |

|

CAGR (2025 - 2032) |

8.8% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Drax Group PLC, Enviva Inc., Blackwood Technology B.V., Brite Carbon AB, Cool Planet Energy Systems, Inc., Steeper Energy Aps, Nippon Steel Engineering Co. Ltd., Boral Limited, Arbaflame AS, Green Flame Pte. Ltd., Airex Energy Inc., FutureCarbon GmbH, Agri-Tech Producers LLC, The Biochar Company, Phoenix Energy, Carbon Terra GmbH, Vaskiluodon Voima Oy, Ørsted A/S |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |