Reports

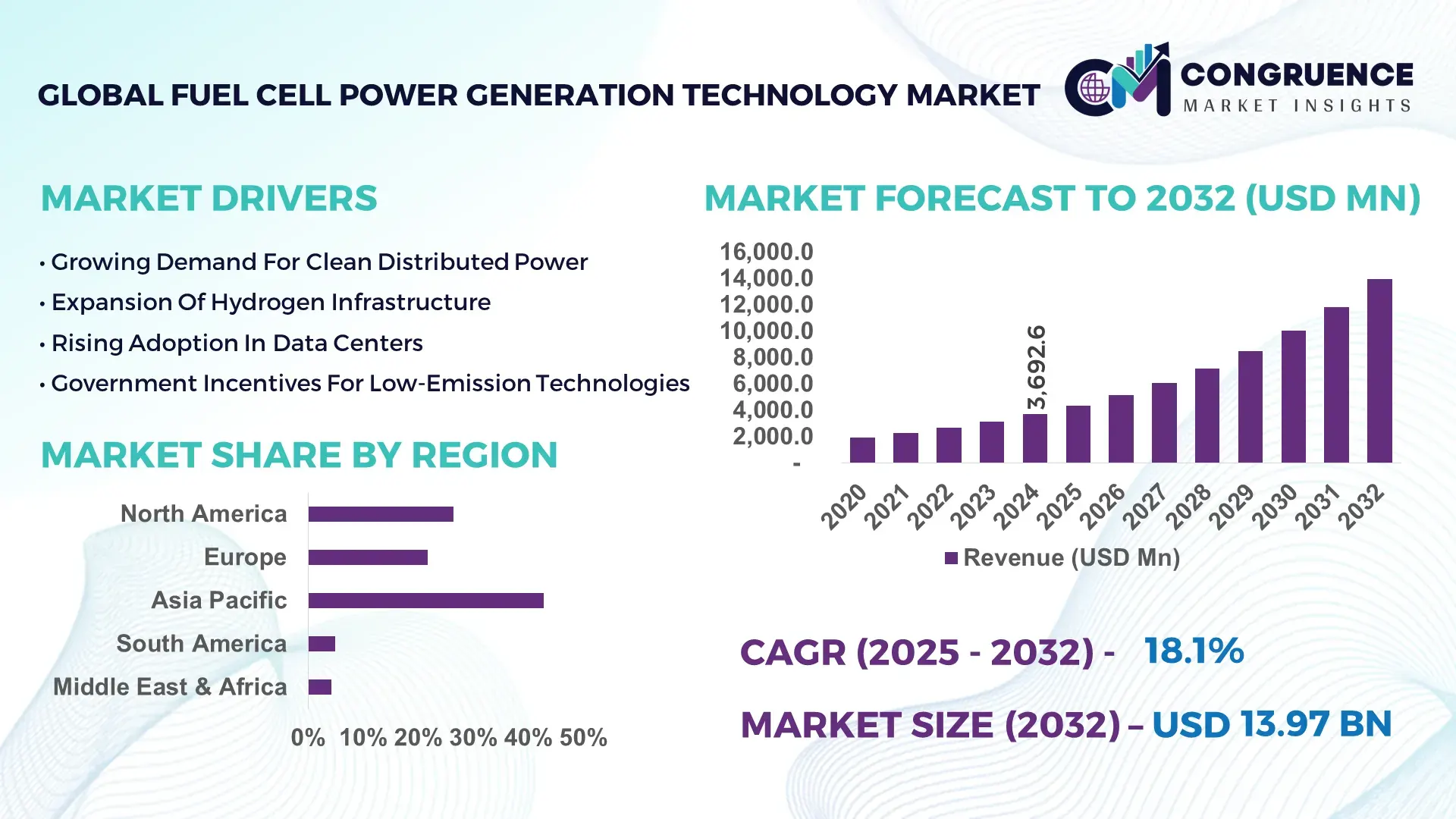

The Global Fuel Cell Power Generation Technology Market was valued at USD 3,692.6 Million in 2024 and is anticipated to reach a value of USD 13,974.3 Million by 2032, expanding at a CAGR of 18.1% between 2025 and 2032, according to an analysis by Congruence Market Insights — reflecting growing global demand for clean, reliable power alternatives driven by decarbonization efforts.

Asia-Pacific—particularly countries such as Japan, South Korea and China—leads global fuel cell power generation production capacity, with over 300 MW of installed industrial-scale fuel cell capacity reported in South Korea alone by 2024. Governments in the region are investing heavily in stationary fuel cell power systems for industrial, commercial and residential use, backing both PEM and SOFC technologies. Utility-scale deployments and household micro-CHP installations have surged, as the region ramps up hydrogen infrastructure and integrates fuel cell systems into both power grids and distributed energy frameworks.

Market Size & Growth: Market value in 2024 at USD 3,692.6 M, projected to reach USD 13,974.3 M by 2032, with an expected CAGR of 18.1% — driven by rising demand for low-carbon, decentralized energy solutions.

Top Growth Drivers: Clean energy transition policies (≈ 48%) driving green power adoption; growing hydrogen infrastructure deployment (≈ 35%); increasing industrial and commercial backup power demand (≈ 27%).

Short-Term Forecast: By 2028, fuel cell system cost per kilowatt-hour expected to reduce by ~22%, while efficiency for combined heat and power (CHP) configurations improves by ~15%.

Emerging Technologies: Next-gen Solid Oxide Fuel Cells (SOFC), advanced Proton Exchange Membrane Fuel Cells (PEMFC), and modular micro-grid integrated fuel cell units.

Regional Leaders: Asia-Pacific at ~USD 6,500 M by 2032 (rapid industrial & residential adoption); North America at ~USD 3,200 M (strong data-center backup and commercial use); Europe at ~USD 2,400 M (industrial SOFC and CHP integration).

Consumer/End-User Trends: Increased uptake in industrial plants, data centers, telecom base stations — demand patterns show preference for reliable, continuous, clean power supply.

Pilot or Case Example: In 2025, a 1.2 MW SOFC-based pilot in South Korea delivered a 28% reduction in downtime compared with conventional diesel backup systems, improving operational reliability significantly.

Competitive Landscape: Market leader holds roughly 25–30% share, followed by 3–4 major competitors controlling approximately 45–50% combined capacity and technology licensing.

Regulatory & ESG Impact: Stringent emission regulations and favorable subsidies in key markets are driving adoption; ESG commitments push companies toward up to 40% reduction in CO₂ emissions by using fuel cell power by 2030.

Investment & Funding Patterns: In 2024–2025, over USD 700 M was invested globally in fuel cell generation projects, with increasing venture funding in green hydrogen infrastructure and public–private financing models for distributed power systems.

Innovation & Future Outlook: Integration of fuel cells with renewable energy (solar, wind) and energy storage systems; deployment of modular hydrogen-based microgrids; scalable fuel cell arrays shaping resilient, decentralized power networks.

Recent developments in stationary power generation systems, combined with expanding hydrogen infrastructure and cost-efficiency improvements, have positioned fuel cell technology as a viable alternative to conventional grid-based power — particularly in regions facing reliability, sustainability, and emissions challenges.

The Fuel Cell Power Generation Technology market is benefiting from cross-sector adoption, including industrial, commercial and residential segments, alongside supportive environmental policies and growing investments in hydrogen infrastructure. Advancements in SOFC and PEMFC technologies, increasing integration with renewables, and rising demand for decentralized clean power across urban and rural regions indicate strong future momentum and shifting consumption patterns toward low-emission energy solutions.

The Fuel Cell Power Generation Technology market plays a strategically critical role in the global transition to clean, reliable energy infrastructure — offering resilience, decentralization, and reduced carbon emissions. Adoption of next-generation Solid Oxide Fuel Cells delivers up to 25% efficiency improvement compared to older combustion-based generators. Asia-Pacific dominates in volume with over 60% of new deployments, while North America leads in enterprise-level adoption with nearly 35% of industrial users employing fuel cell backup systems. By 2027, modular hydrogen-fuel cell microgrids are expected to improve uptime for remote industrial sites by 30%. Many firms are committing to a 40% reduction in CO₂ emissions by 2030 through clean power integration. In 2025, a South Korean industrial facility deployed a 2 MW SOFC array and achieved a 22% reduction in operational energy costs compared to conventional grid power. Fuel Cell Power Generation Technology stands out as a pillar of resilience, compliance, and sustainable growth for energy-intensive industries worldwide — offering a pathway toward long-term energy security and reduced environmental impact.

The Fuel Cell Power Generation Technology market is being shaped by increasing global emphasis on decarbonization, energy security, and grid-independent power generation. Fuel cell systems are gaining traction as reliable alternatives to conventional generators and as complements to renewable energy setups. Key industry players, governments and utilities are investing heavily in hydrogen infrastructure, stack manufacturing capacity, and deployment of both stationary and utility-scale fuel cell power plants. As fossil-fuel reliance declines, demand for distributed and backup power solutions — especially in industrial, commercial, telecom, and residential microgrid applications — is fueling rapid market expansion. Technological improvements in fuel cell efficiency, durability, and integration are also driving convergence between clean energy and energy-intensive industries.

Rising demand for clean, decentralized power is significantly boosting the Fuel Cell Power Generation Technology market. Industrial plants, data centers, and telecom towers increasingly seek reliable backup power that aligns with global decarbonization targets. For example, stationary fuel cell installations in the Asia-Pacific region surged by over 62% in recent years, driven by hydrogen infrastructure expansion and supportive regulatory frameworks. This trend is reinforced by companies preferring fuel cell systems for combined heat and power (CHP), microgrid integration, and off-grid resilience — offering better reliability and lower emissions compared to diesel generators. As electrification of industries and commercial facilities accelerates globally, the need for clean, uninterrupted power supports widespread adoption of fuel cell power systems.

High capital expenditure and dependency on critical materials such as platinum or rare catalysts remain a major barrier. Fuel cell stack manufacturing and hydrogen infrastructure require significant upfront investment, making deployment cost-intensive for many markets. For many industrial and commercial users — especially in developing economies — the initial cost of system installation and maintenance, along with hydrogen supply logistics, limits large-scale adoption. Additionally, fluctuating material costs and limited local manufacturing capacity for fuel cell components hamper scalability. These factors combine to slow down market penetration, particularly in regions with constrained capital budgets or weak hydrogen infrastructure.

Integration of fuel cells with renewable energy sources (like solar and wind) and energy storage systems offers high potential. As countries increase renewable energy capacity, fuel cell systems can complement intermittent power sources by providing stable backup or baseline power, enabling reliable microgrids for remote industrial, commercial, or residential use. Industrial estates, data centers, and remote facilities in regions with unreliable grid supply present large untapped opportunity. The push for zero-emission logistics and clean distributed power further supports fuel cell adoption, especially where grid upgrades are costly or impractical. Emerging green hydrogen projects and supportive financing models also create favorable conditions for rapid deployment.

Limited hydrogen supply infrastructure, storage challenges, and lack of widespread refueling or distribution networks remain major challenges. Without robust hydrogen production, transport, and storage systems — especially in developing regions — fuel cell power generation cannot be effectively scaled. Additionally, regulatory frameworks and safety standards for hydrogen handling remain inconsistent across many geographies, increasing operational risk and compliance costs. For remote or rural deployment scenarios, establishing supply chains for hydrogen or installing local production facilities significantly increases project complexity and delays implementation. These infrastructure and logistical constraints make large-scale adoption of fuel cell power systems more difficult.

• Rising Adoption Of SOFC In Industrial And Utility-Scale Deployments: Solid Oxide Fuel Cells are seeing increasing demand for large-scale power generation. In 2024, over 100 MW of new SOFC capacity was reported in North America alone, indicating strong industrial interest. Utilities and manufacturing plants are choosing SOFC due to its scalability and suitability for continuous high-output operations.

• Growth In Stationary Fuel Cell Systems For Data Centers And Telecom: A growing number of data centers, telecom towers, and critical infrastructure sites are deploying stationary fuel cell systems for reliable backup or primary power. In 2023, more than 40,000 fuel cell units were shipped globally for stationary and portable power use, revealing significant uptake in non-mobility sectors. Commercial operators value fuel cells for clean, uninterrupted power — especially where grid reliability is weak.

• Integration With Renewable Energy And Hydrogen Infrastructure Expansion: Fuel cell power generation systems are increasingly integrated with hydrogen production and storage infrastructure, enabling hybrid clean energy solutions. Industrial plants and utilities are combining on-site green hydrogen production with fuel cell generation to support energy security and emissions commitment. Renewables-driven hydrogen supply chains are scaling, supporting broader deployment of fuel cell systems.

• Modular And Distributed Energy Solutions Gain Traction: Demand for modular and distributed fuel cell power units is rising, especially for remote facilities, microgrids, and decentralized energy projects. These systems allow flexible deployment, scalable capacity, and quick installation — making them attractive to commercial, industrial, and offgrid users seeking resilient power solutions.

Segmentation analysis of the Fuel Cell Power Generation Technology market provides insight into different types, applications, and end-user usage patterns. Product types such as PEMFC and SOFC dominate deployments, with PEMFC widely used due to versatility across stationary, mobile, and backup-power use cases, while SOFC is preferred for industrial and utility-scale power generation due to higher efficiency and capacity. Various applications emerge including distributed generation for microgrids, backup power for data centers and telecom, combined heat and power (CHP) for commercial/residential buildings, and utility-scale grid-connected power plants. End-users span industries such as manufacturing, commercial real estate, telecom, utilities, and remote/off-grid facilities — each segment contributing to the overall market dynamics based on their energy reliability and clean energy requirements. Adoption patterns vary by region: in Asia-Pacific, residential micro-CHP and industrial deployments dominate; in North America, data centers and commercial backup power drive demand; in Europe, utilities and industrial users are leading.

Proton Exchange Membrane Fuel Cells (PEMFC) remain the leading type in the Fuel Cell Power Generation Technology market, accounting for approximately 50% of global installations. Their adaptability for both stationary and mobility applications — along with relatively faster startup times and modular design — makes them preferred for commercial buildings, backup power systems, and small- to medium-scale deployments. Solid Oxide Fuel Cells (SOFC) are the fastest-growing type, driven by demand for larger capacity and higher efficiency in industrial and utility-scale power generation; growth in SOFC installations has been accelerating, especially for capacity ranging from several kW to multi-MW systems. Other types, including Alkaline Fuel Cells and intermediate-temperature fuel cells, occupy the remaining ~10–15% share, serving niche requirements where cost constraints, specific energy densities or unique operating conditions justify their selection.

According to recent industry data, SOFC installations grew by more than 100 MW in 2024 alone, with major industrial clients opting for high-capacity solid oxide systems.

Distributed generation and backup power systems constitute the leading application for fuel cell power generation, representing roughly 45–50% of global deployments, owing to the need for decentralized, reliable, clean energy in grids with intermittent supply or in remote/industrial settings. The fastest-growing application is utility-scale industrial power generation, where SOFC and large-capacity stationary fuel cells are being adopted for continuous base-load supply to manufacturing plants, data centers, and commercial complexes, supported by rising industrial electrification and hydrogen infrastructure. Other applications include combined heat and power (CHP) for commercial and residential buildings, microgrid systems for remote areas, and emergency backup for critical infrastructure — making up around 20–25% combined share. In 2024, more than 38% of commercial facilities globally reported evaluating fuel cell systems for backup or primary power applications.

According to recent market estimates, over 3 GW of fuel cell-based distributed generation capacity was operational globally by 2025.

Industrial and commercial enterprises dominate as end-users, with industrial manufacturing plants, data centers, telecom towers, and utility providers constituting the largest segment, accounting for nearly 55% of total demand for fuel cell power systems. The fastest-growing end-user segment is data centers and telecom infrastructure, where demand surged by over 30% in 2024 due to needs for high-reliability, low-emission backup power. Other end-users — including commercial real estate, hospitals, residential micro-CHP users, and remote/off-grid facilities — comprise the remaining ~45% share, contributing to diversified adoption across sectors.

Recent data shows that in 2024, over 35% of major data centers in North America adopted fuel cell systems for uninterrupted backup power.

Asia-Pacific accounted for the largest market share at 42.8% in 2024; however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 19.4% between 2025 and 2032.

The regionally uneven distribution of hydrogen infrastructure, with Asia-Pacific hosting over 310 MW of installed stationary fuel cell capacity versus Europe’s 185 MW and North America’s 230 MW, reflects differing maturity levels of clean-energy deployment. Japan alone contributed more than 1.2 million residential fuel cell micro-CHP units installed by 2024, while South Korea added more than 100 MW of SOFC capacity in the same period. In comparison, North America registered strong demand from data centers, contributing nearly 28% of regional installations. Europe showed heightened adoption across Germany, the UK and France, collectively accounting for over 55% of the continent’s operational stationary fuel cell systems. Emerging economies in South America demonstrated growth potential through Brazil’s expanding hydrogen roadmaps, while Middle East & Africa’s acceleration is linked to large-scale hydrogen and industrial diversification projects in the UAE and Saudi Arabia.

How Is Advanced Power Reliability Shaping Adoption in This Market?

North America held an estimated 26.4% share of the global market in 2024, supported by high deployment volumes in the U.S. and Canada across data centers, commercial buildings, and telecom infrastructure. Key industries driving demand include IT, financial services, healthcare, and energy-intensive manufacturing facilities seeking uninterrupted, clean backup power. Government policies such as hydrogen tax credits and stationary fuel cell incentives have accelerated adoption. The region is also witnessing advancements in hybrid SOFC-battery systems for mission-critical infrastructure. Local players such as Bloom Energy continue expanding multi-MW SOFC installations for enterprise campuses. Consumer behavior trends show higher enterprise-level adoption in healthcare and financial services, driven by low-tolerance for power outages and sustainability commitments.

Why Is Regulatory Alignment Strengthening Market Uptake in This Region?

Europe captured nearly 21.7% of the global market in 2024, with Germany, the UK, and France representing over 62% of regional consumption. Stringent decarbonization frameworks, including energy-efficiency directives and hydrogen strategies, play a central role in accelerating fuel cell deployment. Germany’s industrial sector, the UK’s commercial estates, and France’s utility-scale clean power programs drive much of the demand. The region has adopted next-generation SOFC and PEMFC systems integrated with hydrogen hubs. Companies such as Elcogen continue advancing solid oxide stack technology. Consumer behavior trends indicate strong demand for explainable and regulation-compliant solutions due to strict sustainability reporting requirements.

What Factors Are Driving Large-Scale Technological Expansion in This Market?

Asia-Pacific dominated in 2024 with the highest global volume, representing 42.8% of fuel cell power installations. China, Japan, and South Korea—collectively contributing over 75% of regional demand—lead adoption due to strong domestic manufacturing, hydrogen infrastructure, and residential micro-CHP deployment. The region has become a hotspot for large SOFC farms, scalable PEMFC units, and industrial power applications. Japan’s ENE-FARM program surpassed 1.2 million household units, while China continues expanding MW-scale hydrogen fuel cell power plants. Companies such as Doosan Fuel Cell are actively scaling industrial SOFC installations. Consumer behavior reflects rapid uptake driven by e-commerce, mobile apps, and technology-centric urbanization.

How Are Emerging Energy Transitions Supporting Growth in This Market?

South America accounted for approximately 4.9% of global market share in 2024, with Brazil and Argentina being the leading contributors. Regional adoption is influenced by expanding renewable-hydrogen programs, industrial sector modernization, and increased interest in decentralized power solutions for remote assets. Infrastructure development around hydrogen corridors and distributed power networks is improving feasibility for stationary fuel cell systems. Local companies are exploring partnerships to introduce compact fuel cell units for commercial facilities. Consumer behavior demonstrates demand tied to media, customer engagement platforms, and language-specific localization needs.

What Is Driving the Rapid Shift Toward Clean Industrial Power in This Market?

Middle East & Africa represented nearly 4.2% of global share in 2024, driven by major contributors such as the UAE, Saudi Arabia, and South Africa. The region is moving toward hydrogen-enabled industrial power for oil & gas, construction, and heavy-industry operations. Technological modernization initiatives, including integration of high-capacity SOFC systems in industrial clusters, are advancing rapidly. Local regulations supporting hydrogen economy development and clean energy diversification have improved adoption rates. Companies across the region are piloting MW-scale SOFC and PEMFC projects for industrial estates. Consumer behavior reveals strong adoption in sectors requiring high-reliability power and low-emission operations.

Japan – 18.5% market share – Dominance driven by large-scale residential micro-CHP installations and strong technology manufacturing capacity.

United States – 16.2% market share – Leadership supported by high demand from data centers, commercial users, and enterprise-grade reliability requirements.

The Fuel Cell Power Generation Technology market is moderately consolidated, with approximately 35–40 active global competitors and the top five players collectively holding around 48% of the global market share. The competitive environment is shaped by continuous product innovation, long-term supply agreements, and investments in hydrogen infrastructure. Leading companies focus on expanding SOFC and PEMFC portfolios, improving system durability, and scaling MW-level installations for industrial customers. Several major players are forming partnerships with utilities and hydrogen producers to strengthen integration across distributed energy networks. Innovation trends include modular system design, high-efficiency ceramic stacks, and hybrid power configurations that combine fuel cells with battery storage. Companies are also prioritizing localization strategies for manufacturing to reduce reliance on imported catalysts and stacks. Competitive differentiation increasingly depends on operational efficiency, lifecycle cost reduction, and digital monitoring platforms that optimize power reliability.

Doosan Fuel Cell

FuelCell Energy

Panasonic Corporation

Mitsubishi Power

Cummins Inc.

Elcogen

SFC Energy

Horizon Fuel Cell Technologies

Nedstack Fuel Cell Technology

Intelligent Energy

SolidPower

Toshiba Energy Systems

Technological progress in the Fuel Cell Power Generation Technology market is driven by advancements in stack materials, system integration, and hydrogen infrastructure readiness. Solid Oxide Fuel Cells continue to gain momentum due to high electrical efficiency and suitability for multi-MW industrial systems. Improvements in ceramic electrolytes, such as enhanced ionic conductivity and thermal durability, have enabled SOFCs to operate more efficiently in large installations. Proton Exchange Membrane Fuel Cells are also evolving through catalyst layer optimization and reduced platinum loading, which enhances durability and decreases cost per kilowatt. Companies are increasingly integrating PEMFC systems into backup infrastructure for data centers and telecom operations. Digital monitoring and predictive maintenance tools are becoming fundamental to fuel cell operations, applying real-time analytics and condition-based optimization to improve performance. Hybrid systems that combine fuel cells with advanced battery storage are emerging as viable solutions for peak-shaving and grid-responsive operations. Hydrogen storage technologies, including high-pressure tank systems and solid-state hydrogen storage materials, are strengthening the scalability of fuel cell plants. Meanwhile, modular fuel cell units allow flexible deployment for industrial parks, commercial complexes, and microgrid installations. As hydrogen production shifts toward electrolysis-based green hydrogen, interoperability between renewable energy assets and fuel cell power systems will expand, supporting wider adoption across industries.

• In April 2024, Ballard Power Systems received a multi-MW order for its latest fuel cell modules to support data center backup power applications. The deployment aims to strengthen clean-energy resilience for hyperscale data operators and includes next-generation PEM stacks for improved operational output. Source: www.ballard.com

• In February 2024, Bloom Energy commissioned a 10 MW SOFC installation for a large U.S. manufacturing facility, marking one of the region’s largest on-site fuel cell deployments. The system enhances power reliability and contributes to operational decarbonization targets. Source: www.bloomenergy.com

• In October 2023, Plug Power expanded its green hydrogen production capacity with the launch of a new electrolyzer facility designed to support fuel cell power projects across industrial and commercial sectors. The facility boosts domestic hydrogen availability for stationary power systems. Source: www.plugpower.com

• In July 2023, FuelCell Energy announced the completion of a major upgrade to its carbonate fuel cell platform, improving electrical efficiency and extending stack life for distributed power applications. The upgrade supports growing demand from commercial campuses and industrial customers. Source: www.fuelcellenergy.com

The Fuel Cell Power Generation Technology Market Report provides an extensive analysis of the global industry ecosystem, covering key segments such as fuel cell types, applications, end-users, and technology developments across major geographies. The scope includes detailed segmentation of PEMFC, SOFC, AFC, PAFC, and emerging intermediate-temperature systems, focusing on their adoption across industrial, commercial, utility, and residential applications. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional energy strategies, hydrogen infrastructure expansion, demand mapping, and installation patterns. The report evaluates distributed generation systems, micro-CHP, utility-scale installations, data center backup power, and hybrid energy frameworks. It also examines supply-chain factors such as stack manufacturing, catalyst sourcing, hydrogen distribution, and supporting infrastructure. The scope includes competitive benchmarking, technology readiness, regulatory frameworks, and ecosystem partnerships influencing adoption. The report also highlights emerging areas such as modular fuel cell arrays, off-grid microgrids, digitalized monitoring solutions, and integration with renewable-energy-based hydrogen production. The analysis is tailored for decision-makers seeking clarity on market opportunities, deployment feasibility, and technology-driven growth potential across industries.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 3,692.6 Million |

|

Market Revenue in 2032 |

USD 13,974.3 Million |

|

CAGR (2025 - 2032) |

18.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bloom Energy, Plug Power, Ballard Power Systems, Doosan Fuel Cell, FuelCell Energy, Panasonic Corporation, Mitsubishi Power, Cummins Inc., Elcogen, SFC Energy, Horizon Fuel Cell Technologies, Nedstack Fuel Cell Technology, Intelligent Energy, SolidPower, Toshiba Energy Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |