Reports

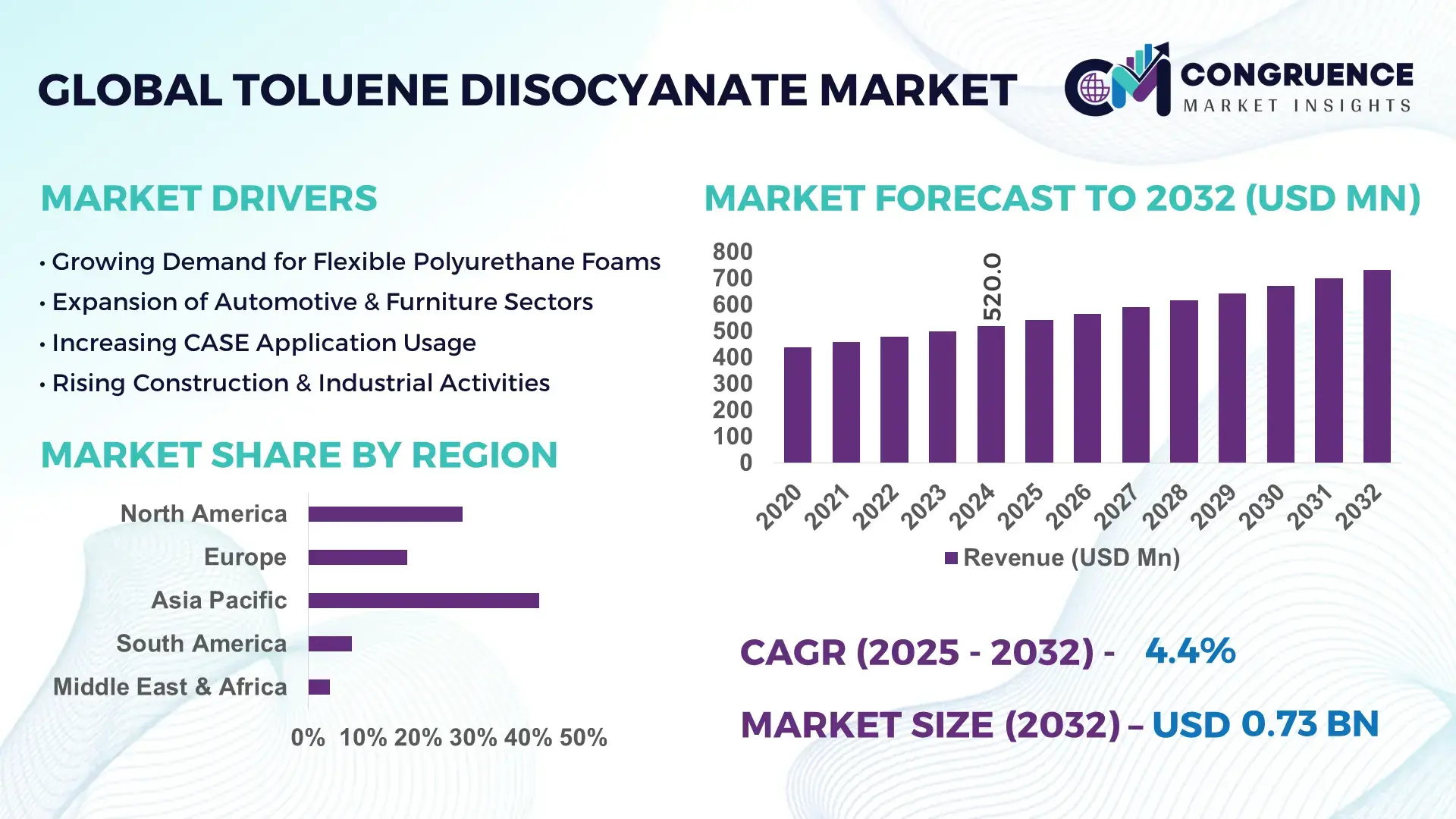

The Global Toluene Diisocyanate Market was valued at USD 520.0 Million in 2024 and is anticipated to reach a value of USD 731.0 Million by 2032, expanding at a CAGR of 4.35% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily driven by increased demand in polyurethane applications across several high-growth industries.

China, the dominant country in the Toluene Diisocyanate market, operates large-scale production complexes with an annual TDI output exceeding 1 million metric tons, backed by major investments from companies such as Wanhua Chemical and BASF. Its strong downstream polyurethane sector leverages TDI for flexible foams, coatings, adhesives, and elastomers, while recent technological advancements such as advanced purification and low‑emission TDI production have boosted efficiency and reduced environmental impact.

Market Size & Growth: Estimated at USD 520.0 Million in 2024, projected to reach USD 731.0 Million by 2032 with a 4.35% CAGR; driven by strong polyurethane demand in construction, automotive, and furniture industries.

Top Growth Drivers: Flexible foam adoption (~60 %), automotive lightweighting (~25 %), construction insulation (~15 %).

Short-Term Forecast: By 2028, efficiency gains in TDI manufacturing are expected to reduce energy consumption by up to 8%.

Emerging Technologies: Catalytic low-emission TDI synthesis; bio-based isocyanate alternatives; closed-loop polyurethane recycling.

Regional Leaders: China & Asia-Pacific – major production hub with integrated TDI and PU capacity; North America – steady adoption, especially in automotive foams; Europe – increasingly adopting green TDI technologies by 2032.

Consumer/End-User Trends: High uptake by automotive (seating), furniture (mattresses), and CASE (coatings, adhesives) segments.

Pilot / Case Example: In 2025, Wanhua Chemical implemented a pilot low-emission TDI process, reducing volatile organic compound (VOC) emissions by 12%.

Competitive Landscape: Leading producer holds ~25% capacity (BASF), followed by Covestro, Wanhua, Dow, and Mitsui.

Regulatory & ESG Impact: Stricter isocyanate exposure limits plus incentives for recycling and green manufacturing are shaping investment.

Investment & Funding Patterns: Over USD 300 million in recent capacity expansion and green‑tech projects by key global players.

Innovation & Future Outlook: Integration of digital process control, bio-based feedstocks, and advanced catalysts is expected to drive the next wave of market evolution.

Toluene Diisocyanate applications are expanding in flexible and rigid polyurethane foams (furniture, construction), CASE (coatings, adhesives, sealants, elastomers), and elastomer products. Green chemistry, stricter emissions regulation, and recycling are reshaping demand, while Asia-Pacific remains a key consumption and production region, and technological innovation continues to fuel future growth.

Toluene Diisocyanate (TDI) remains strategically critical for the global polyurethane ecosystem: as lightweight, resilient foams become foundational to automotive, furniture, and insulation sectors, TDI enables performance gains with cost efficiency. Modern production technologies, such as new low‑emission catalytic processes, deliver up to 15% lower emissions compared to traditional phosgenation, making TDI production more sustainable.

Regionally, Asia-Pacific dominates in production volume, while North America leads in adoption, with over 40% of polyurethane automotive seating producers integrating TDI-based foams. By 2027, advanced process control and digitalized manufacturing are expected to improve TDI yield efficiency by 10%, reducing energy use and operating costs. Moreover, with regulatory pressure mounting, many firms are committing to ESG metrics, for example targeting a 20% reduction in emissions and increasing recycling of polyurethane waste by 2030.

In 2025, Covestro innovated by deploying a closed-loop recovery system in its European TDI plant, resulting in a 10% reduction in raw material waste. Looking ahead, TDI is poised not just as a raw material but as a pillar of resilient, compliant, and sustainable chemical supply chains, serving both traditional industrial demand and emerging green, circular economy applications.

The Toluene Diisocyanate market is shaped by a convergence of high-growth downstream sectors, regulatory pressures, and technological shifts. Strong demand in flexible polyurethane foams, especially for bedding, automotive, and furniture, continues to drive volume. At the same time, stricter regulations around isocyanate exposure and emissions force producers to invest in greener, safer synthesis technologies. Raw material volatility (e.g., toluene, aniline) also introduces cost risk and supply chain complexity. Meanwhile, innovation in bio-based TDI feedstocks and recycling of polyurethane waste is steadily gaining traction, offering a pathway to more sustainable growth. These forces make the TDI market both an essential industrial input and a growing focus for ESG-driven transformation.

Flexible polyurethane foam — used in furniture cushions, automotive seating, and mattresses — remains the largest consumer of TDI. As urbanization accelerates and disposable incomes rise, especially in emerging economies, demand for such foams is surging. Moreover, the automotive industry’s push for lightweight materials amplifies the need for TDI-based PU to improve fuel efficiency. This macro‑trend translates into stable upstream investment in TDI production and long-term contracts between TDI manufacturers and foam fabricators. At the same time, TDI’s favorable reactivity profile and cost‑performance balance make it uniquely suited to deliver high-performance foam at scale.

TDI is classified as a respiratory sensitizer, which requires strict handling protocols and workplace safety measures. These regulations impose compliance costs — such as closed-loop systems and enhanced worker protection — that can raise operational expenses materially. Further, environmental regulations aimed at reducing emissions of isocyanates are tightening in many jurisdictions, necessitating investment in costly abatement technologies. These compliance burdens disproportionately affect smaller producers, limiting their ability to scale and compete, and can slow the rate of capacity expansions in the industry.

Emerging recycling technologies for polyurethane waste — including chemical depolymerization — present a major opportunity. Through these processes, TDI can be recovered and reused, reducing reliance on virgin raw materials. As regulatory bodies increasingly incentivize circularity, more firms are investing in pilot recycling plants. By capturing end-of-life PU, manufacturers can mitigate feedstock risk, cut emissions, and address sustainability targets. This shift also opens new business models, such as closed-loop supply agreements and circular‑material-as-a-service offerings.

TDI producers are heavily exposed to fluctuations in toluene and aniline prices, which together make up a significant portion of production cost. Geopolitical instability and oil price swings can cause raw material costs to vary by 20–30%, affecting margins and planning. These swings lead to price risk, forcing manufacturers to hedge, hold inventories, or pass costs to downstream users, which can reduce demand. Smaller producers or those with less flexible cost structures are particularly vulnerable, limiting their competitiveness and constraining long-term investment.

Rising Modular Construction Demand: The adoption of modular and prefabricated construction methods is reshaping TDI demand. Roughly 55% of modular construction projects report cost savings thanks to factory-made PU elements, boosting the need for high-performance TDI-based foams.

Sustainable TDI Innovations: Manufacturers are increasingly investing in low-emission catalytic production, which has reduced VOC emissions in some plants by 12%–15%, aligning with tighter ESG mandates.

Closed‑Loop Polyurethane Recycling: Pilot recycling units using depolymerization are enabling recovery of TDI precursors, helping firms divert up to 8% of PU waste back into production streams.

Digital Process Optimization: Use of AI-driven process control systems has improved yield efficiency in TDI plants by as much as 10%, reducing waste and energy consumption while improving product consistency.

The Toluene Diisocyanate (TDI) market is structured across multiple layers, offering nuanced insights into types, applications, and end-user segments. By type, the market encompasses pure TDI, modified TDI, and specialty blends, each tailored for specific polyurethane and industrial requirements. Application segmentation includes flexible foams, coatings, adhesives, sealants, elastomers (CASE), and rigid foams, reflecting TDI’s versatility in construction, automotive, furniture, and industrial sectors. End-user insights indicate that automotive, furniture, and construction industries are primary consumers, leveraging TDI-based materials for performance and durability. Rising urbanization, industrial expansion, and technological adoption in manufacturing are shaping both regional and global demand patterns, with Asia-Pacific demonstrating the highest production intensity and North America exhibiting early adoption of advanced TDI-based technologies. Overall, the segmentation provides critical guidance for strategic planning, investment prioritization, and innovation in product development.

The TDI market is categorized into pure TDI, modified TDI, and specialty blends. Among these, pure TDI leads, accounting for approximately 58% of adoption due to its broad utility in flexible polyurethane foam and CASE applications, offering consistent reactivity and reliable performance. Modified TDI is the fastest-growing type, supported by innovations in low-odor and low-emission formulations, capturing attention for use in consumer-facing applications and specialty coatings. Its adoption is rising rapidly, with increasing uptake in Asia-Pacific, Europe, and North America. Specialty blends, including pre-reacted TDI systems and polymer-modified products, collectively contribute 25% of the market, serving niche industrial requirements.

Flexible foams dominate TDI consumption, representing 60% of usage, primarily driven by automotive seating, furniture cushions, and bedding products where high resilience and comfort are critical. CASE applications (coatings, adhesives, sealants, elastomers) are the fastest-growing segment, fueled by automotive lightweighting and industrial demand for high-performance coatings. Rigid foams, used in insulation and construction, alongside other minor applications, account for 25% combined share, serving specialized industrial and construction needs. Consumer trends indicate that in 2024, over 38% of furniture manufacturers globally adopted TDI-based flexible foams, while 42% of automotive seating producers integrated TDI in high-resilience cushioning.

The leading end-user segment is automotive, holding 55% of market adoption, leveraging TDI for lightweight, resilient foams and elastomers in seating, interiors, and insulation. The furniture sector is the fastest-growing end-user, driven by rising urbanization and demand for comfort-enhancing mattresses and cushions, with adoption projected to increase notably in emerging economies. Other end-users, including construction, industrial equipment, and electronics, together contribute 30% of TDI utilization, supporting niche applications. Trends show that in 2024, over 60% of top-tier furniture manufacturers reported implementing advanced TDI foams, and 42% of North American automotive OEMs tested innovative TDI formulations for enhanced seating.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 4.35% between 2025 and 2032.

In 2024, Asia-Pacific’s Toluene Diisocyanate (TDI) consumption exceeded 220,000 metric tons, with China alone producing over 1 million metric tons annually. The region benefits from large-scale manufacturing hubs, robust construction, and automotive sectors. North America, with market share of 28%, is rapidly adopting advanced TDI technologies. Europe holds 18%, while South America and Middle East & Africa collectively contribute 12%, reflecting growing industrialization and regulatory-driven green initiatives. The regional adoption patterns highlight strong industrial integration, infrastructure expansion, and technological investments across global TDI applications.

North America holds a 28% share of the TDI market, driven by automotive, furniture, and construction industries. Advanced digital process control and low-emission TDI production techniques are increasingly deployed across U.S. and Canadian plants. Regulatory changes, such as stricter OSHA standards and VOC limits, encourage manufacturers to adopt sustainable practices. Covestro’s U.S. facility recently implemented a closed-loop recovery system, enhancing process efficiency and reducing waste. Consumer adoption shows higher enterprise uptake in healthcare, construction, and industrial equipment sectors. Firms are also leveraging AI-driven predictive maintenance, reducing downtime by 7–10%, indicating growing integration of digital transformation in regional TDI production and utilization.

Europe represents 18% of the global TDI market, with Germany, the UK, and France as major contributors. Strict REACH regulations and sustainability initiatives push producers toward low-emission TDI processes. Emerging technologies, including catalytic low-VOC synthesis and bio-based TDI blends, are gaining traction. BASF’s German plant has introduced advanced purification techniques reducing environmental impact while improving foam quality. Consumer trends indicate high adoption in automotive manufacturing and building insulation applications, supported by regulatory pressures that demand explainable, safe chemical usage. Companies increasingly invest in energy-efficient facilities and circular manufacturing processes to meet compliance and environmental expectations.

Asia-Pacific is the largest TDI market, accounting for 42% of global consumption, with China, India, and Japan as top consumers. Rapid urbanization, construction expansion, and automotive production are key demand drivers. Technological hubs in China are advancing low-emission TDI production and automation, enhancing efficiency and reducing VOC emissions. Wanhua Chemical operates large integrated TDI-PU plants, producing over 1 million metric tons annually. Consumer behavior varies, with increased adoption in e-commerce-driven furniture and mobile applications influencing demand for high-performance TDI foams. Regional infrastructure investment in smart manufacturing further accelerates TDI uptake.

South America contributes 8% of the global TDI market, with Brazil and Argentina as key countries. Investments in construction, automotive, and industrial equipment sectors are fueling growth. Government incentives for chemical manufacturing and trade policies supporting import-export balance drive market stability. Braskem has initiated pilot TDI projects focusing on process efficiency and emissions reduction. Regional consumer trends emphasize industrial and infrastructure projects, with growing demand for TDI-based flexible foams in commercial and residential construction. Energy sector modernization and localized production facilities further reinforce TDI consumption patterns.

Middle East & Africa holds 4% of global TDI consumption, led by UAE and South Africa. Construction and oil & gas industries are major consumers. Technological modernization, including automated TDI production lines and emission control systems, is increasing operational efficiency. SABIC has invested in plant upgrades to enhance production reliability and environmental compliance. Consumer adoption shows industrial preference for durable, high-resilience PU products in construction and automotive. Trade partnerships and regional regulations are also influencing investment patterns and promoting greener production practices across the region.

China – 42% Market Share: Dominates due to high production capacity exceeding 1 million metric tons and extensive downstream PU applications.

United States – 28% Market Share: Strong end-user demand in automotive, furniture, and construction sectors, supported by advanced low-emission TDI technologies.

The Toluene Diisocyanate (TDI) market is moderately consolidated, with more than 20 active global competitors, though the top 5 companies together account for around 65–70% of capacity. Leading producers such as BASF, Covestro, Wanhua Chemical, Dow, and Mitsui dominate via integrated production and strong downstream partnerships. These firms are executing strategic initiatives: Wanhua is rapidly expanding its TDI capacity with new large-scale plants; Covestro is investing in low-emission and bio‑based TDI lines; BASF is optimizing its production locations and enhancing process sustainability. Innovation is a key differentiator: major players are deploying advanced catalysts, digital twin process optimization, and closed-loop recycling to reduce emissions and improve yield. Additionally, some smaller regional players are gaining traction by offering cost-competitive production in localized markets, contributing to increased regional fragmentation. Competitive pressures are also driving joint R&D collaborations, capacity expansions, and green-tech transitions across the value chain, making the market both dynamic and strategically important.

Wanhua Chemical Group

Mitsui Chemicals, Inc.

Huntsman Corporation

The TDI market is undergoing significant technological transformation driven by environmental regulation, process efficiency, and sustainability goals. One major trend is the adoption of low-emission catalytic processes, which dramatically lower VOC emissions and energy consumption. These new catalyst systems can reduce benzene-related emissions during TDI production by over 90%, helping producers meet stricter environmental standards.

Another important technology shift is the development of bio‑based or biomass-balance TDI, where part of the feedstock is derived from renewable sources. This approach supports circular economy principles and aligns TDI production with sustainable chemistry mandates. Companies are also exploring closed-loop recycling of polyurethane waste to recover isocyanate precursors, thereby reducing reliance on virgin feedstocks and minimizing waste.

Digital transformation is playing a crucial role: digital twin and AI-driven process optimization tools are being used to enhance reaction yields, reduce off-spec production, and improve energy efficiency. These systems allow real-time simulation and optimization of plant operations, leading to material savings and lower operating costs. Moreover, carbon-tracing methodologies (such as atom-mapping models) are emerging to help producers track biogenic vs. fossil carbon in TDI supply chains, which is increasingly important for ESG reporting and regulatory compliance.

Finally, modular and flexible production units are gaining traction, enabling smaller-capacity TDI plants that can be deployed closer to local end‑users. This reduces logistics costs and enhances resilience in the supply chain. For decision-makers, these technology trends collectively signal a shift toward more sustainable, efficient, and digitally-enabled TDI manufacturing, positioning the market for long-term growth under tightening environmental frameworks.

In March 2025, Covestro successfully completed the modernization of its TDI plant in Dormagen, Germany. The upgraded reactor uses reaction heat to generate steam, reducing energy consumption by 80% and cutting CO₂ emissions by 22,000 tonnes annually. Source: www.covestro.com

Also in March 2025, Covestro announced a new global energy‑efficiency target: it aims to reduce energy use per ton of product by 20% by 2030 (vs. 2020), which corresponds to avoiding approximately 550,000 tonnes of CO₂ emissions. Source: www.covestro.com

In May 2023, Wanhua Chemical commissioned a 250,000‑ton/year TDI plant at its Fujian site, achieving 99.98% purity in its TDI output — a benchmark in product quality. Source: www.en.whchem.com

In March 2023, Mitsui Chemicals announced that it would cut capacity at its Omuta TDI plant from 120,000 t/year to ~50,000 t/year by July 2025, as part of its restructuring to focus more on high-value isocyanates and greener production. Source: www.jp.mitsuichemicals.com

The Toluene Diisocyanate (TDI) Market Report offers a comprehensive assessment of global market dynamics, spanning types, applications, end‑users, and geographies. It covers TDI variants such as 80/20 and 65/35 formulations, specialty modified grades, and bio-based production. Applications examined include flexible foams, rigid foams, coatings, adhesives & sealants, and elastomers, reflecting TDI’s versatility across industries like automotive, furniture, construction, electronics, and footwear.

Geographically, the report analyzes major regions—North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa—highlighting supply‑chain structures, local capacity, and consumption trends. It also explores technological innovations, such as low-emission and phosgene-free production, digital process control, and recycling of polyurethane waste. End-use insights focus on key industry players in automotive seating, building insulation, and consumer foam manufacturing. The report further examines strategic developments: capacity expansions, mergers & acquisitions, joint R&D initiatives, and regional investments.

In addition, the report delves into future-facing themes like circular economy models, bio-based TDI feedstocks, and carbon-tracing for ESG compliance. Niche segments—such as high-performance coatings, thermoplastic polyurethane (TPU), and recycled isocyanates—are also discussed to provide a rounded view of potential growth paths. This scope ensures that decision-makers, analysts, and investors have actionable insight into both current market conditions and emerging strategic opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 520.0 Million |

| Market Revenue (2032) | USD 731.0 Million |

| CAGR (2025–2032) | 4.35% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | BASF SE, Covestro AG, Dow Inc., Wanhua Chemical Group, Mitsui Chemicals, Inc., Huntsman Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |