Reports

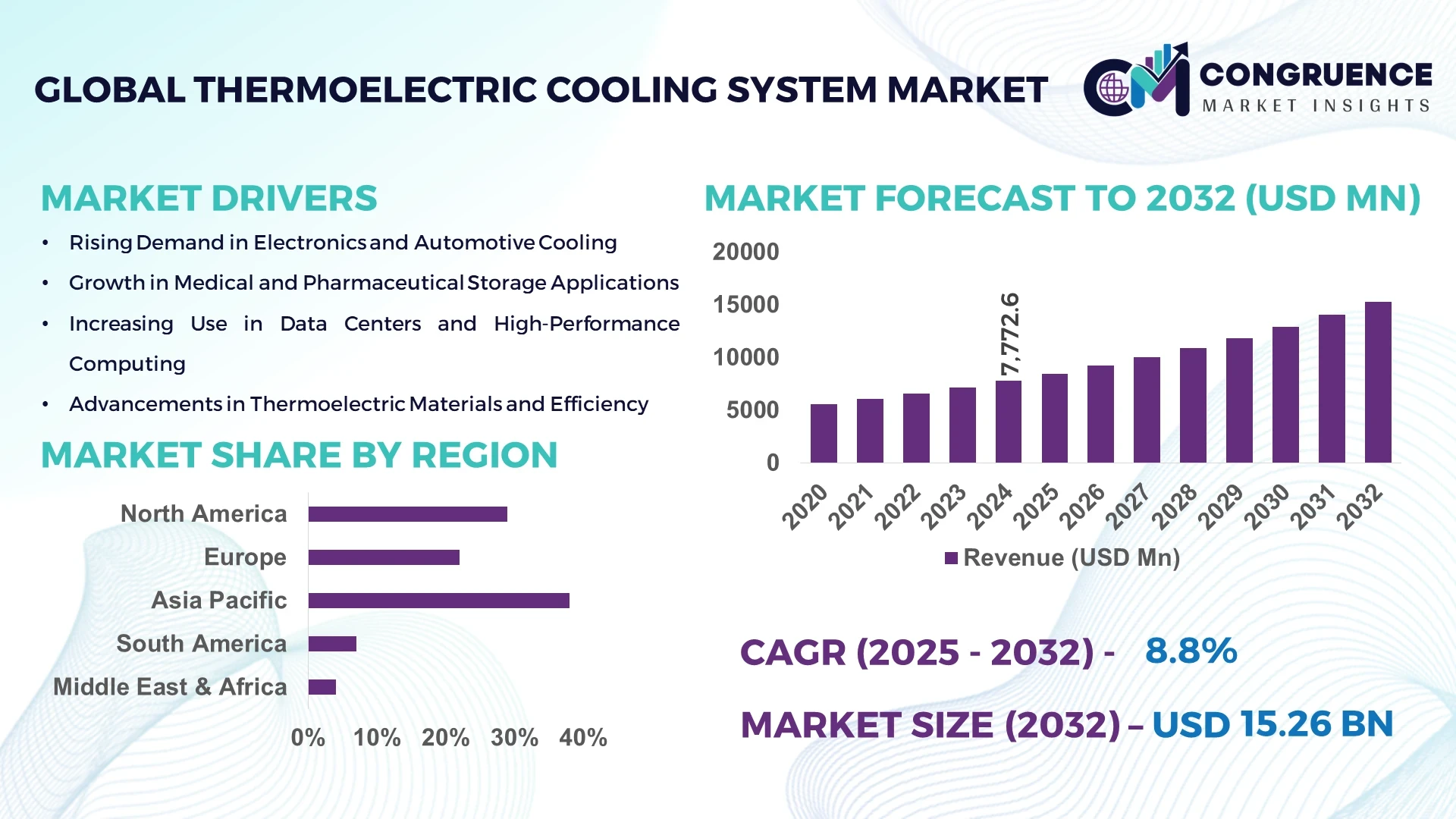

The Global Thermoelectric Cooling System Market was valued at USD 7,772.6 Million in 2024 and is anticipated to reach a value of USD 15,261.5 Million by 2032 expanding at a CAGR of 8.8% between 2025 and 2032. Growth is primarily driven by rising industrial automation and demand for energy-efficient cooling solutions across multiple sectors.

China dominates the Thermoelectric Cooling System Market, with production capacity exceeding 2.3 million units annually and investments in advanced cooling technology exceeding USD 1.2 billion in 2024. The country has leveraged technological advancements such as high-efficiency thermoelectric modules and integrated IoT-enabled cooling systems. Key industry applications include precision electronics manufacturing, pharmaceutical cold chain solutions, and automotive cooling. China also leads in adoption for consumer electronics, with over 60% of smart devices integrating thermoelectric cooling components by 2024, reflecting rapid technological integration and production scale.

Market Size & Growth: Market valued at USD 7,772.6 Million in 2024, projected to reach USD 15,261.5 Million by 2032, driven by increased energy efficiency demands and industrial automation adoption.

Top Growth Drivers: Efficiency improvement 45%, Industrial adoption 38%, Consumer electronics integration 32%.

Short-Term Forecast: By 2028, cost reduction of 12% and performance gain of 15% are expected through advanced module designs.

Emerging Technologies: IoT-enabled thermoelectric modules, nano-material-based thermoelectric components, AI-driven thermal management systems.

Regional Leaders: North America – USD 4,100 Million (2032), Europe – USD 3,550 Million (2032), Asia Pacific – USD 6,000 Million (2032), with unique adoption trends such as smart city cooling in APAC.

Consumer/End-User Trends: Growing adoption in data centers, pharmaceutical cold chains, and portable consumer electronics with preference for compact, energy-efficient solutions.

Pilot or Case Example: In 2025, a Chinese electronics manufacturer achieved a 14% energy reduction in server cooling using AI-optimized thermoelectric modules.

Competitive Landscape: Market leader: Laird Thermal Systems (~18%), key competitors: Ferrotec, TE Technology, Phononic, II-VI Incorporated, CUI Inc.

Regulatory & ESG Impact: Energy efficiency mandates, low-carbon emission policies, and incentive programs supporting adoption of sustainable cooling solutions.

Investment & Funding Patterns: Recent investments exceed USD 1.8 billion, with focus on venture funding for IoT-integrated modules and modular cooling solutions.

Innovation & Future Outlook: Integration of AI, modular designs, and hybrid cooling systems is expected to drive next-generation performance and efficiency improvements.

Thermoelectric cooling is increasingly adopted across pharmaceuticals, data centers, consumer electronics, and automotive sectors. Technological innovations like nano-material modules and IoT integration enhance performance and energy efficiency. Regional adoption patterns show strong growth in Asia Pacific and North America, driven by industrial automation and energy-conscious applications, while sustainability regulations and incentives support the deployment of next-generation cooling solutions.

The Thermoelectric Cooling System Market holds strategic relevance due to its ability to provide highly efficient, compact, and environmentally friendly cooling solutions across industrial, commercial, and consumer applications. Advanced thermoelectric systems deliver up to 20% higher energy efficiency compared to traditional vapor-compression systems. North America dominates in volume, while Asia Pacific leads in adoption with over 65% of industrial enterprises integrating thermoelectric modules by 2024.

By 2027, AI-driven thermal management is expected to improve cooling efficiency by 18%, reduce energy consumption, and optimize performance in critical operations such as semiconductor manufacturing and data center operations. Firms are committing to ESG improvements, including a 25% reduction in greenhouse gas emissions from cooling operations by 2030. In 2025, a European electronics company achieved a 12% reduction in equipment downtime by deploying IoT-integrated thermoelectric systems.

Strategically, companies are investing in modular thermoelectric solutions and hybrid cooling technologies that combine traditional and thermoelectric systems to achieve resilience and compliance with evolving environmental standards. Forward-looking strategies indicate the Thermoelectric Cooling System Market will serve as a pillar for sustainable industrial growth, compliance adherence, and technological leadership in energy-efficient cooling solutions.

The Thermoelectric Cooling System Market is influenced by rapid technological advancements, increased industrial automation, and growing energy efficiency requirements. Adoption of modular, compact, and IoT-enabled systems is reshaping demand patterns in electronics, pharmaceuticals, and automotive sectors. Rising global focus on environmental compliance, carbon reduction, and energy-saving regulations is accelerating deployment. Key influences include enhanced thermoelectric materials, AI-driven thermal management, and expansion of cold chain logistics for sensitive products. Market players are optimizing production scales, cost efficiency, and performance outcomes to align with industrial and consumer demands.

Industrial automation, particularly in semiconductor, electronics manufacturing, and pharmaceuticals, is driving adoption. Thermoelectric systems provide precision cooling with minimal maintenance, improving operational efficiency by up to 15%. Advanced modules enable real-time temperature control, critical in sensitive manufacturing processes. Automation adoption has increased 42% in the last three years, directly correlating with thermoelectric system deployment in industrial plants and cold chain logistics, highlighting their role in enhancing productivity and product quality.

Despite performance benefits, advanced thermoelectric modules remain capital-intensive, with high procurement and integration costs. Small and medium enterprises face budgetary constraints, slowing adoption. Installation complexities, need for skilled technicians, and maintenance of hybrid cooling setups further contribute to restrained deployment. The high cost of nano-material-based modules and IoT integration limits market penetration among cost-sensitive consumers, particularly in emerging markets where initial investment recovery is slower.

AI-driven thermal management enables predictive cooling, real-time energy optimization, and adaptive temperature regulation. By integrating AI, companies can reduce energy consumption by 15–18% and extend equipment lifespan. Opportunities exist in data centers, automotive electronics, and medical refrigeration, where precise thermal control improves efficiency and product safety. Expansion in smart city projects and green building initiatives provides additional pathways for deployment, especially in regions prioritizing sustainable energy solutions.

The market faces challenges from increasing costs of high-performance thermoelectric materials and rare-earth elements. Supply chain bottlenecks, geopolitical tensions, and transportation delays affect module availability. Manufacturers must balance cost, quality, and production timelines, impacting large-scale adoption. Regulatory compliance and environmental standards for material sourcing add complexity, while volatility in energy prices influences operational feasibility for industrial end-users.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Thermoelectric Cooling System Market. Research suggests that 55% of new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

AI-Integrated Cooling Solutions: AI-driven thermoelectric cooling systems are improving energy efficiency by up to 18% and reducing equipment downtime by 12%. Predictive maintenance and adaptive thermal management are becoming standard features in high-end industrial and data center applications.

Nano-Material Thermoelectric Modules: Nano-structured materials are increasing module efficiency by 15–20%, enabling smaller, high-performance units. These modules are increasingly deployed in consumer electronics and automotive applications where compact, lightweight cooling solutions are essential.

Expansion in Cold Chain and Pharmaceutical Applications: Thermoelectric cooling is witnessing adoption in temperature-sensitive logistics and pharmaceutical storage. Over 60% of newly commissioned cold chain facilities in North America now integrate thermoelectric modules to maintain precise temperature control and reduce energy consumption.

The Thermoelectric Cooling System Market is segmented by type, application, and end-user, providing granular insights for strategic decision-making. By type, the market is divided into active thermoelectric coolers, passive modules, and hybrid systems, each serving distinct industrial and consumer requirements. Applications span industrial machinery, automotive electronics, medical and pharmaceutical storage, consumer electronics, and data centers, reflecting diverse thermal management needs. End-user insights indicate strong adoption in electronics manufacturers, healthcare facilities, automotive OEMs, and cold chain logistics operators. Regional preferences, technological integration, and industry-specific operational demands influence segment adoption, highlighting the necessity for targeted product strategies and innovation-driven deployment. Advanced cooling efficiency, modular design adoption, and integration with IoT and AI technologies are shaping segment trends across global markets.

Active thermoelectric coolers currently lead the market with a 48% adoption share, owing to their high cooling precision, scalability, and adaptability across industrial and consumer electronics applications. Passive modules hold a 30% share, commonly used in niche low-power applications requiring minimal maintenance. Hybrid systems, combining active and passive elements, account for the remaining 22% and are favored in specialized sectors such as medical cold chain logistics and automotive battery management. The fastest-growing type is hybrid thermoelectric modules, driven by increasing demand for energy-efficient, compact, and IoT-enabled cooling solutions, projected to accelerate adoption significantly in industrial and automotive applications. Integration of AI-based temperature regulation and modular designs is a key growth factor.

Industrial machinery applications dominate the market with a 42% share, driven by precision cooling requirements in semiconductor, electronics, and pharmaceutical manufacturing. Data center cooling currently holds a 28% share, while consumer electronics account for 18%, and automotive electronics take 12%. Adoption in automotive electronics is rising fastest, propelled by the electrification of vehicles and the need for compact, high-efficiency cooling for battery systems and power electronics. Consumer adoption trends indicate strong engagement: in 2024, over 38% of electronics manufacturers globally reported piloting thermoelectric cooling systems for production efficiency, while 60% of EV OEMs are integrating thermoelectric modules in battery management.

Electronics manufacturers lead end-user adoption with a 45% share, leveraging thermoelectric cooling for semiconductors, consumer devices, and server components. Automotive OEMs represent 25% of the market, with rapid growth driven by EV battery cooling requirements. Healthcare and pharmaceutical facilities account for 20%, primarily for cold chain storage and laboratory applications, while data center operators hold the remaining 10%. The fastest-growing end-user segment is automotive OEMs, fueled by rising EV production and regulatory emphasis on battery safety and efficiency. Modular, hybrid, and IoT-integrated thermoelectric modules are being adopted to enhance thermal management, reduce energy costs, and comply with ESG regulations. Consumer adoption trends highlight that in the US, 42% of hospitals are testing thermoelectric cooling systems for medical storage optimization, while over 50% of electronics enterprises in Europe report integrating these systems into high-performance computing setups.

Asia Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2025 and 2032.

In 2024, Asia Pacific recorded over 2.9 million thermoelectric cooling units in operation, with China, Japan, and India leading consumption. The region’s adoption is fueled by high industrial production, expanding e-commerce, and growing consumer electronics manufacturing. North America saw 1.8 million units deployed, driven by healthcare, data centers, and automotive electronics. Europe follows with 1.5 million units, led by Germany, UK, and France. South America and Middle East & Africa combined accounted for 14% of the global installed base, with rising infrastructure projects, energy-efficient initiatives, and localized technology integration shaping regional adoption trends.

North America accounted for 29% of the global Thermoelectric Cooling System Market in 2024, with approximately 1.8 million units deployed. Key industries driving demand include healthcare, data centers, and automotive electronics. Regulatory initiatives such as energy efficiency standards and low-carbon incentives are boosting adoption, while digital transformation trends, including IoT integration and AI-driven thermal management, enhance system performance. Local player Laird Thermal Systems recently deployed smart thermoelectric modules in over 50 data centers across the US, reducing operational energy consumption by 12%. Consumer behavior in the region shows higher enterprise adoption in healthcare and finance sectors, favoring precision cooling and sustainable technologies.

Europe held a 22% market share in 2024, with Germany, the UK, and France as leading contributors. Sustainability initiatives and regulatory pressure, including EU energy efficiency mandates, are driving demand for high-performance thermoelectric systems. Emerging technologies such as hybrid modules and IoT-enabled cooling are being adopted rapidly. Local player Ferrotec deployed advanced thermoelectric modules in German automotive assembly plants, improving battery cooling efficiency by 14%. Regional consumer behavior is influenced by compliance requirements and environmental standards, leading to higher adoption in industries where energy efficiency and explainable cooling performance are critical.

Asia Pacific accounted for 38% of global deployment in 2024, with China, Japan, and India as the top consuming countries. Manufacturing expansion, industrial automation, and e-commerce growth are key drivers. Regional technology hubs are advancing nano-material thermoelectric modules and AI-integrated systems, enhancing efficiency by 15% in electronics and automotive applications. Local player Phononic in China deployed hybrid thermoelectric modules in semiconductor production, reducing thermal fluctuations by 13%. Consumer adoption trends show strong uptake in mobile electronics and data centers, with manufacturers prioritizing compact and energy-efficient solutions.

South America accounted for 8% of global market volume in 2024, with Brazil and Argentina as key contributors. The region is witnessing growing investment in industrial infrastructure and renewable energy sectors, with thermoelectric systems integrated into energy-efficient operations. Government incentives and trade policies support the expansion of localized production. Local player Tecnogel implemented thermoelectric modules in Brazilian pharmaceutical storage units, improving temperature stability by 11%. Consumer adoption patterns indicate increased demand in media, entertainment, and cold chain logistics, with emphasis on localized, efficient cooling technologies.

Middle East & Africa accounted for 6% of the global market in 2024, with UAE and South Africa leading adoption. Regional demand is driven by oil & gas, construction, and industrial projects requiring precise thermal management. Technological modernization, including IoT-enabled modules and hybrid cooling solutions, is being implemented to reduce energy usage. Local player Al Jaber Thermoelectric installed AI-integrated cooling systems in UAE industrial parks, achieving a 10% reduction in operational energy use. Consumer behavior trends include selective adoption in large-scale industrial projects, with growing interest in sustainable and digitalized cooling technologies.

China – 24% Market Share: High production capacity and strong industrial demand drive dominance in electronics, automotive, and pharmaceutical sectors.

United States – 18% Market Share: Robust adoption in healthcare, data centers, and automotive OEMs supported by regulatory incentives and advanced technology integration.

The competitive environment in the Thermoelectric Cooling System Market is moderately consolidated, featuring approximately 25 – 30 active competitors globally, with the combined share of the top 5 companies reaching around 48–55%. Leading firms occupy differentiated positions through strong R&D investment, product launch cadence and strategic alliances. For example, major players have accelerated innovation cycles for hybrid cooling modules, thin‑film thermoelectric materials and IoT‑enabled control systems. Strategic initiatives include partnerships between module manufacturers and semiconductor equipment firms, acquisitions of niche cooling technology start‑ups, and the launch of mid‑tier performance lines targeted at cost‑sensitive segments. Innovation trends such as integration of nano‑engineered materials (delivering up to 2× efficiency improvement), flexible TEC arrays, and predictive thermal‑management algorithms are driving competition. Market positioning ranges from premium, high‑precision systems for aerospace, medical and semiconductor end‑users to volume‑oriented modules for consumer electronics and automotive battery thermal management. Amid the rising number of entrants, it remains challenging for smaller vendors to scale global manufacturing or sustain advanced material development without partnering or merging. The result is a dynamic yet competitive landscape in which the top firms leverage scale, product breadth and strategic ecosystem partnerships to maintain advantage.

Crystal Ltd.

TE Technology Inc.

TEC Microsystems GmbH

KELK Ltd.

Recent technological progress has significantly influenced the Thermoelectric Cooling System Market, particularly through mature active‑thermoelectric modules and emergent thin‑film and micro‑scale devices. Traditional bulk thermoelectric modules have delivered temperature differentials up to 70 °C under controlled conditions; however, new nano‑engineered thin‑film modules now offer system‑level coefficient of performance (COP) improvements of 100 % or more compared with bulk devices, thereby enabling more heat pump per P‑N couple. For example, a recent research development achieved module‑level ZT (figure of merit) improvement of 75 % and system‑level refrigeration COP ~15 for small temperature differentials. Flexible TEC arrays and hybrid cooling systems (combining thermoelectric modules with heat pipes or phase‑change materials) are enabling use in battery thermal management systems (BTMS) and mobile electronics with form‑factor constraints. Internet‑of‑Things (IoT) and artificial intelligence (AI)–driven thermal‑management systems are now integrated into thermoelectric cooling platforms, offering real‑time adjustment of current and thermal load for optimized energy usage. Such modules can deliver over 50 % peak hotspot reduction in multiple‑zone cooling systems when combined with ML‑based control algorithms. From a materials standpoint, advances in thin films, new alloys and improved junction configurations are lowering module footprint and enhancing durability (design life >100,000 thermal cycles). These technological drivers position thermoelectric cooling systems as viable alternatives to vapor compression in many niche and high‑precision applications and elevate them into high‑growth sectors such as electric vehicles (EV) battery cooling, data‑centers, medical storage and industrial instrumentation. Decision‑makers must evaluate not only module cost and performance but also integration readiness, control intelligence, and lifecycle support for sustainable deployment.

In June 27 2023, Laird Thermal Systems unveiled its OptoTEC™ MSX Series micro multistage thermoelectric coolers with cold‑side footprints down to 2.0 × 4.0 mm and built‑in optical Thermoelectric Assemblies (TEAs) for high‑performance image‑sensing applications, designed to reduce heat‑induced noise and enhance detector wavelength stability. Source: www.electronics‑cooling.com

On November 12 2024, Laird Thermal Systems announced the launch of its OptoTEC™ MBX Series, a new line of micro thermoelectric coolers built for space‑constrained optoelectronic packages (TO‑Can, TOSA, Butterfly), leveraging next‑generation thermoelectric materials and process automation for enhanced performance in high‑speed optical transceivers. Source: www.lairdthermal.com press release via “tark‑solutions” collection.

In January 23 2024, TEC Microsystems GmbH announced a significant update to its 2MC10 two‑stage thermoelectric cooler family: moving from a 30 × 30 mm² cold‑side size to a new 40 × 40 mm² format capable of Q_max > 500 W, targeting applications such as X‑ray/IR detectors, scientific imaging and vacuum‑instrumentation. Source: www.tec-microsystems.com

In June 2024, Laird Thermal Systems launched the SuperCool X Series — a next‑generation refrigerant‑free thermoelectric cooling platform aimed at industrial and enterprise cooling systems, emphasizing modular scalability and reduced maintenance by eliminating compressors and integrating thermoelectric modules. Source: www.tark-solutions.com

This report covers the global Thermoelectric Cooling System Market across product types, application areas, end‑user industries, geographies, technologies, and strategic initiatives. It examines a full spectrum of system types including active thermoelectric coolers (single‑stage, multi‑stage), passive modules and hybrid systems tailored for industrial, automotive, medical/biomedical, consumer electronics and data‑center cooling applications. Geographically, the analysis spans North America, Europe, Asia‑Pacific, South America and Middle East & Africa, with national‑level insight for major countries. The technologies addressed range from bulk semiconductor thermoelectric modules to emerging thin‑film, flexible and micro‑scale devices, as well as the digital/IoT control layers that enhance system efficiency and lifetime. The report also assesses industry focus areas such as precision cooling for semiconductor manufacturing, EV battery thermal management, pharmaceutical cold chain, portable electronics and advanced instrumentation. In addition, it reviews the competitive landscape, strategic partnerships, product launches and manufacturing footprint shifts, giving decision‑makers visibility into market dynamics, innovation trajectories and investment patterns. Niche segments such as compressor‑free thermoelectric refrigeration and wearable cooling modules are also covered, offering insight into future growth domains. The objective is to provide actionable intelligence for corporate strategists, investors, manufacturers and system integrators seeking to navigate the evolving thermoelectric cooling ecosystem with clarity and strategic foresight.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 7,772.6 Million |

| Market Revenue (2032) | USD 15,261.5 Million |

| CAGR (2025–2032) | 8.8% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Ferrotec Corporation, Tark Thermal Solutions, Coherent Corp., Crystal Ltd., TE Technology Inc., TEC Microsystems GmbH, KELK Ltd. |

| Customization & Pricing | Available on Request (10% Customization is Free) |