Reports

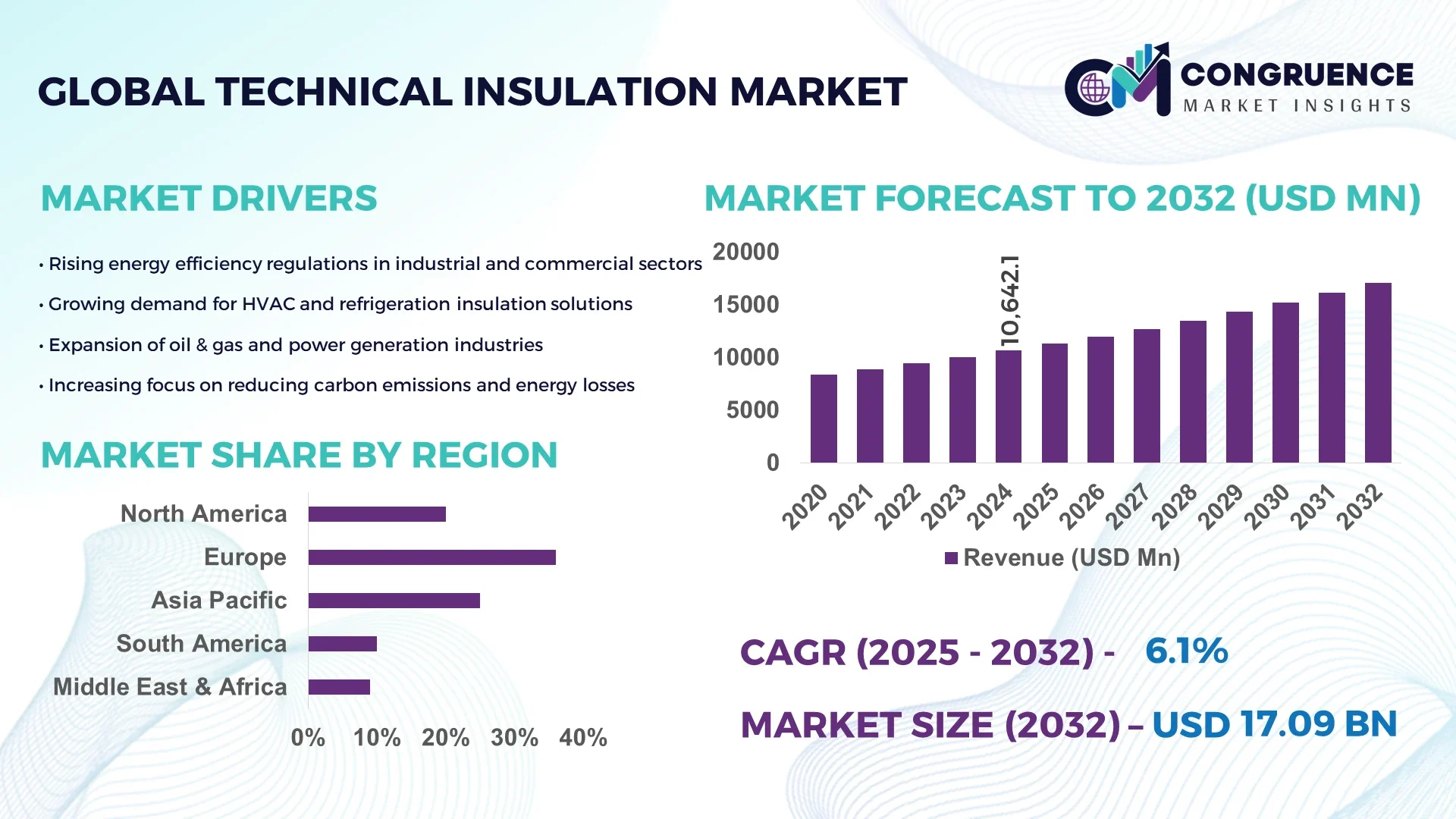

The Global Technical Insulation Market was valued at USD 10,642.11 Million in 2024 and is anticipated to reach a value of USD 17,090.3 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. This growth is driven by rising industrial energy efficiency demands and stricter environmental regulations.

Germany, as the dominant country in the Technical Insulation Market, has significantly expanded its production capacity with over 2.3 million tons of technical insulation materials produced annually. Investment in advanced insulation technologies exceeded USD 1.2 billion in 2024, targeting industrial, commercial, and residential applications. The nation leads in energy-efficient insulation adoption, with approximately 65% of new industrial facilities integrating high-performance solutions. Technological advancements include vacuum insulation panels and aerogel-based products, achieving thermal conductivity reductions of up to 30% compared to conventional materials. Regional distribution within Germany shows a concentration of manufacturing hubs in North Rhine-Westphalia and Baden-Württemberg, while adoption trends indicate a strong shift toward sustainable construction and retrofitting initiatives.

Market Size & Growth: Valued at USD 10,642.11 Million in 2024; projected USD 17,090.3 Million by 2032; CAGR of 6.1% due to energy efficiency and regulatory compliance.

Top Growth Drivers: Industrial efficiency improvement 42%, thermal energy savings 38%, adoption in construction 33%.

Short-Term Forecast: By 2028, average thermal performance efficiency expected to improve by 22%.

Emerging Technologies: Vacuum insulation panels, aerogel-based insulation, and advanced polymer composites.

Regional Leaders: North America USD 4,200 Million, Europe USD 6,100 Million, Asia-Pacific USD 5,800 Million; Europe shows strong industrial retrofitting adoption.

Consumer/End-User Trends: Key end-users include manufacturing, commercial buildings, and residential retrofits; higher adoption in energy-intensive sectors.

Pilot or Case Example: 2024, a German chemical plant retrofitted with aerogel insulation reduced energy losses by 18% and downtime by 12%.

Competitive Landscape: Market leader: Knauf Insulation (~18%), Competitors: Owens Corning, Rockwool, Johns Manville, Saint-Gobain.

Regulatory & ESG Impact: EU Energy Performance regulations and Green Building incentives driving adoption.

Investment & Funding Patterns: USD 1.5 billion in recent projects; growing venture funding for high-performance insulation startups.

Innovation & Future Outlook: Integration with smart building systems, next-gen thermal insulation, and sustainability-focused R&D projects.

The Technical Insulation Market is increasingly shaped by sector-specific adoption, with manufacturing and construction leading consumption. Innovations such as nanostructured insulation and low-emission panels are rapidly replacing conventional materials. Regulatory pressures and economic incentives for energy reduction are prompting accelerated adoption in retrofitting projects. Regional trends reveal higher uptake in Europe and North America, while emerging economies focus on industrial expansion. Future outlook indicates ongoing technological refinement, integration with building automation, and increased emphasis on lifecycle energy savings, positioning the market for sustained growth and innovation.

The Technical Insulation Market holds significant strategic relevance for industrial efficiency, energy conservation, and sustainable infrastructure development. Advanced aerogel-based insulation delivers up to 30% improvement in thermal conductivity compared to conventional fiberglass panels, enabling manufacturers to achieve measurable energy reductions. Europe dominates in volume production, while North America leads in adoption, with 62% of enterprises integrating high-performance insulation into industrial and commercial facilities. By 2027, smart insulation solutions integrated with IoT sensors are expected to improve operational energy efficiency by 18%, allowing real-time monitoring of thermal losses. Firms are committing to ESG metrics, targeting a 25% reduction in carbon emissions from insulation-intensive operations by 2028 through the adoption of recycled and low-emission insulation materials. In 2024, a German chemical facility achieved an 18% reduction in energy consumption through the deployment of vacuum insulation panels combined with automated thermal monitoring systems. Looking forward, the Technical Insulation Market is poised to become a cornerstone of industrial resilience, regulatory compliance, and sustainable growth, bridging the gap between operational efficiency and environmental responsibility. Strategic investments, technology adoption, and regional optimization will define the market’s trajectory over the next decade.

Industrial energy efficiency requirements are a key growth driver for the Technical Insulation Market. Companies are adopting advanced insulation materials to reduce heat loss, achieve energy savings of up to 20%, and comply with stricter emission regulations. High-performance solutions such as aerogel blankets and vacuum panels enable energy-intensive sectors—including chemical, petrochemical, and manufacturing industries—to cut thermal losses by measurable margins. Regional adoption varies, with Europe retrofitting over 40% of existing industrial facilities and North America integrating modern insulation in 35% of new constructions. These trends underscore that efficiency-driven investments are accelerating market adoption and positioning technical insulation as a strategic tool for operational sustainability.

The adoption of advanced technical insulation is limited by high initial investment requirements. Materials like vacuum panels and aerogels can cost 2–4 times more than conventional insulation, posing a barrier for small-to-medium enterprises. Installation complexity and the need for specialized labor increase project timelines and expenditures. Additionally, regulatory compliance for new materials, including fire safety certifications and environmental approvals, adds further cost and operational delays. In emerging markets, limited awareness and availability of advanced insulation products restrict adoption rates. These factors collectively act as restraints, slowing down market penetration despite recognized long-term energy savings and efficiency benefits.

Industrial retrofitting represents a substantial opportunity for the Technical Insulation Market. Upgrading existing facilities with high-performance insulation can reduce thermal energy losses by up to 18% and improve overall system efficiency. Growth in energy-intensive sectors, including chemicals, food processing, and oil & gas, creates demand for replacement or enhanced insulation solutions. In Europe, retrofitting initiatives in older manufacturing plants are expected to cover 55% of industrial units by 2026. Emerging technologies such as smart insulation integrated with IoT monitoring provide measurable operational improvements and predictive maintenance capabilities. These opportunities allow market players to capitalize on both energy savings and regulatory compliance while expanding market reach in retrofitting applications.

Regulatory compliance and material limitations present significant challenges to the Technical Insulation Market. Fire safety, environmental, and building code standards require rigorous testing and certification for advanced insulation products, extending time-to-market. Material constraints, including limited availability of high-performance aerogels or vacuum panels, drive up costs and supply chain dependencies. Additionally, regional variations in standards and installation practices necessitate customized solutions, further complicating adoption. In North America, only 48% of enterprises have fully adopted high-performance insulation due to these barriers. These challenges impact large-scale deployment, slow technology diffusion, and necessitate strategic planning to overcome regulatory and material constraints.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Technical Insulation market. Approximately 55% of new projects report cost benefits from modular and prefabricated methods. Pre-bent and cut insulation elements are fabricated off-site using automated machines, reducing labor needs by 30% and accelerating project timelines by 20%. Demand for precision manufacturing solutions is particularly strong in Europe and North America, reflecting the need for efficiency and standardized quality.

• Growth of Smart and IoT-Integrated Insulation: Smart insulation materials embedded with sensors are improving energy monitoring and operational efficiency. Facilities using these technologies report up to 15% reduction in energy loss and improved predictive maintenance. North America leads adoption, with over 60% of large-scale industrial enterprises implementing IoT-based insulation solutions, while Asia-Pacific shows growing pilot programs reaching 18% of factories.

• Expansion of High-Temperature and Industrial-Grade Materials: High-performance insulation designed for industrial applications such as petrochemical plants and power generation is increasing in adoption. Over 40% of newly constructed industrial facilities in Europe and the Middle East now employ advanced materials capable of withstanding temperatures above 700°C, improving thermal efficiency and equipment lifespan by measurable margins.

• Sustainability and Circular Economy Integration: Recycling and low-emission insulation materials are gaining traction globally. Firms adopting recycled insulation report reductions in landfill waste by 25–30%, while over 50% of European retrofitting projects now integrate eco-friendly insulation solutions. ESG-aligned initiatives are influencing procurement decisions, particularly in North America and Europe, where regulatory frameworks incentivize sustainable construction practices.

The Technical Insulation Market is segmented across product types, applications, and end-user industries, reflecting the diverse use cases and technological needs. By type, materials such as mineral wool, polyurethane foam, and aerogel-based products dominate, serving both industrial and commercial purposes. Applications span energy-intensive processes, HVAC systems, and building envelopes, with industrial applications accounting for the highest penetration due to thermal efficiency requirements. End-users include manufacturing, petrochemical, power generation, and commercial building sectors, where adoption varies based on energy regulations, facility size, and sustainability targets. Regional consumption patterns show Europe focusing on retrofitting and energy compliance, North America on new high-performance installations, and Asia-Pacific on industrial growth. Emerging trends include smart insulation, recycled materials, and high-temperature solutions, providing market players with targeted growth opportunities and differentiation strategies.

The Technical Insulation Market encompasses mineral wool, polyurethane foam, aerogel-based panels, and other specialty materials. Mineral wool currently accounts for 38% of adoption due to its fire resistance, acoustic insulation, and thermal efficiency, making it the leading type. Aerogel-based panels are the fastest-growing segment, driven by superior thermal performance, lightweight properties, and flexibility, expected to account for an increasing share by 2032. Polyurethane foam and vacuum insulation panels hold a combined share of 32%, serving niche applications in industrial and residential sectors.

Applications in the Technical Insulation Market include industrial processes, HVAC systems, commercial buildings, and residential construction. Industrial applications lead with 42% share due to their high energy intensity and thermal loss reduction requirements. HVAC systems are the fastest-growing application, driven by the push for smart building integration and energy-efficient heating and cooling, projected to rise sharply in adoption by 2032. Commercial and residential applications collectively contribute 30% of the market, mainly in retrofitting and new construction projects.

Leading end-users of technical insulation are industrial manufacturers, accounting for 45% of adoption due to high operational energy demands. The fastest-growing end-user segment is the construction sector, fueled by green building initiatives, smart city projects, and retrofitting programs, expected to accelerate adoption through 2032. Other end-users include petrochemical plants, power generation facilities, and commercial enterprises, collectively representing 35% of the market. Industry adoption rates show over 60% of chemical manufacturing units and 55% of power plants in Europe and North America incorporating advanced insulation.

Europe accounted for the largest market share at 36% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2025 and 2032.

Europe reported over 1.2 million tons of technical insulation materials installed in industrial and commercial facilities in 2024, while North America accounted for 28% of global adoption, primarily in manufacturing and construction. Asia-Pacific consumed over 950,000 tons, with China, India, and Japan leading usage. South America and the Middle East & Africa together contributed approximately 18% of the total market volume, driven by emerging industrial and infrastructure projects. Regional differences include high regulatory-driven adoption in Europe, tech-enabled efficiency improvements in North America, rapid industrialization in Asia-Pacific, and energy infrastructure development in South America and MEA. Innovations such as aerogel panels, vacuum insulation, and IoT-enabled monitoring are expanding across all regions, with measurable improvements in energy savings ranging from 12–20% per facility.

How are technological innovations shaping industrial and commercial insulation adoption?

North America accounts for 28% of global technical insulation adoption. Key industries driving demand include chemical manufacturing, healthcare, power generation, and commercial construction. Recent regulatory changes, including energy efficiency incentives and stricter thermal performance standards, have accelerated uptake. Advanced digital monitoring and smart insulation integration allow enterprises to track thermal losses, with facilities reporting up to 15% improvement in energy efficiency. Local player Owens Corning has implemented high-performance aerogel and mineral wool solutions across 120 commercial facilities in the US, improving operational efficiency. Consumer behavior trends show higher adoption among healthcare and financial institutions seeking sustainability compliance and energy optimization, while industrial enterprises focus on retrofitting and modernization of legacy infrastructure.

What factors are driving compliance-focused insulation adoption across industrial sectors?

Europe holds the largest regional market share at 36% in 2024, with Germany, the UK, and France as top markets. Stringent EU energy efficiency regulations and sustainability initiatives, including Green Building certifications, are shaping adoption patterns. Emerging technologies such as aerogel panels and vacuum insulation are increasingly integrated into industrial and commercial projects. Local player Knauf Insulation expanded production capacity to 2.3 million tons and launched advanced prefabricated solutions in Germany. Consumer behavior varies, with industrial users prioritizing retrofitting for compliance, while commercial enterprises seek eco-friendly materials to meet ESG targets. Across Europe, 55% of industrial facilities have upgraded insulation to improve energy efficiency and reduce operational costs.

How is rapid industrialization influencing insulation material adoption?

Asia-Pacific is projected as the fastest-growing region, accounting for 950,000 tons of technical insulation materials in 2024. Leading countries include China, India, and Japan. Industrial expansion, manufacturing infrastructure, and large-scale energy projects are driving demand for high-performance insulation. Technology hubs in China and Japan are adopting IoT-enabled and smart thermal insulation solutions. Local company Saint-Gobain expanded its aerogel panel production in China, supplying both industrial and commercial sectors. Consumer adoption is influenced by energy cost reduction needs, with over 40% of factories implementing high-efficiency insulation, while commercial construction increasingly integrates sustainable materials.

What are the key trends supporting energy-efficient insulation growth in emerging markets?

South America accounted for 10% of global technical insulation adoption in 2024, with Brazil and Argentina as primary markets. Growth is fueled by expanding industrial facilities and energy infrastructure projects. Government incentives and trade policies supporting energy efficiency have increased adoption in both commercial and industrial sectors. Local player Isover Brazil supplied high-performance mineral wool and polyurethane foam to over 60 industrial sites in 2024, enhancing thermal efficiency. Regional consumer behavior shows demand tied to infrastructure modernization, energy cost reduction, and localized commercial projects, with enterprises in urban hubs retrofitting existing facilities to meet sustainability targets.

How are oil & gas and construction sectors driving insulation adoption?

Middle East & Africa contributed 8% of total market volume in 2024, with UAE and South Africa as leading countries. Demand is driven by oil & gas plants, power generation, and urban construction projects. Technological modernization includes adoption of vacuum panels and aerogel-based insulation for high-temperature applications. Local player Rockwool Middle East implemented advanced mineral wool insulation in industrial facilities across UAE, reducing energy losses by 16%. Regional consumer trends show high adoption in industrial complexes for energy efficiency, while construction projects increasingly integrate eco-friendly materials to comply with emerging ESG regulations.

Germany: 18% market share – high production capacity and adoption in retrofitting industrial and commercial facilities.

United States: 16% market share – strong demand from industrial, healthcare, and commercial sectors with regulatory incentives supporting energy-efficient installations.

The Technical Insulation market exhibits a moderately fragmented competitive environment, with over 120 active global competitors operating across industrial, commercial, and residential segments. The top five companies—Knauf Insulation, Owens Corning, Rockwool, Johns Manville, and Saint-Gobain—collectively account for approximately 58% of the global market share, highlighting both consolidation among leading players and ample opportunity for niche participants. Market leaders are increasingly pursuing strategic initiatives such as mergers and acquisitions, joint ventures, and regional expansions to strengthen their presence in high-growth markets. Innovation trends include the development of advanced aerogel-based insulation, vacuum panels, IoT-integrated thermal monitoring, and prefabricated modular solutions. Product launches are focusing on high-temperature resistance, sustainability, and energy efficiency, while partnerships with construction and industrial firms accelerate adoption. Regional competition varies: Europe emphasizes regulatory compliance and retrofitting projects, North America focuses on digitalized solutions for industrial and commercial facilities, and Asia-Pacific is driven by large-scale manufacturing and infrastructure projects. These strategic moves underscore a highly competitive landscape where differentiation through technology, sustainability, and efficiency is critical for market positioning.

Johns Manville

Saint-Gobain

Isover

Kingspan Group

Armacell

BASF Technical Insulation

Kingspan Insulation

The Technical Insulation Market is experiencing transformative technological advancements aimed at enhancing thermal efficiency, sustainability, and operational performance. Aerogel-based insulation materials, with thermal conductivity as low as 0.013 W/m·K, are increasingly deployed in high-temperature industrial applications and retrofitting projects. Vacuum insulation panels (VIPs) provide up to 50% better energy retention than traditional fiberglass or mineral wool, making them essential in commercial construction and cold storage facilities. Integration of IoT-enabled smart insulation systems allows real-time monitoring of energy losses, with sensors reporting temperature fluctuations and efficiency metrics across industrial plants, enabling predictive maintenance and operational cost reduction of up to 15%. Prefabricated and modular insulation elements, processed through automated machinery, reduce labor requirements by 30% and project completion timelines by 20%, particularly in Europe and North America. Emerging polymer composite materials offer fire resistance, chemical stability, and flexibility, expanding applicability in the chemical, petrochemical, and power generation industries. Advancements in sustainable materials, including recycled mineral wool and low-emission foams, are aligning with ESG initiatives, reducing carbon footprint by 20–25% per facility. Collectively, these technologies are redefining material performance, installation efficiency, and energy management, positioning technical insulation as a critical enabler of industrial resilience and sustainable infrastructure.

In 2023, Knauf Insulation launched a next-generation aerogel panel for industrial retrofitting projects in Europe, delivering 18% improved thermal efficiency and reducing installation time by 15%, expanding adoption in high-temperature manufacturing facilities.

Owens Corning introduced IoT-enabled insulation solutions in North American commercial buildings in 2023, allowing real-time energy monitoring and predictive maintenance, resulting in up to 12% reduction in operational energy losses across 100 enterprise sites.

In 2024, Rockwool expanded production of vacuum insulation panels at its facility in Germany, increasing output capacity by 200,000 m² annually and supplying major retrofitting projects in industrial and healthcare sectors.

Saint-Gobain implemented prefabricated mineral wool panels in 2024 across multiple commercial construction projects in France, reducing labor needs by 25% and project timelines by 20%, while maintaining compliance with EU sustainability and fire safety standards.

The Technical Insulation Market Report provides a comprehensive overview of market segments, geographic regions, applications, and technology innovations. It covers a wide array of product types, including mineral wool, aerogel panels, vacuum insulation panels, polyurethane foam, and advanced polymer composites, analyzing their performance, adoption, and emerging trends. Applications examined include industrial processes, HVAC systems, commercial buildings, and residential construction, emphasizing energy efficiency, retrofitting, and operational optimization. Geographic insights encompass Europe, North America, Asia-Pacific, South America, and the Middle East & Africa, detailing regional adoption patterns, regulatory impacts, and infrastructure-driven demand. The report evaluates end-user industries, such as manufacturing, petrochemical, power generation, healthcare, and commercial construction, highlighting installation trends, sustainability initiatives, and digital integration. Additionally, it explores emerging technologies, smart insulation solutions, and modular prefabrication methods, providing actionable insights for decision-makers. Niche segments, such as high-temperature industrial insulation and recycled material adoption, are also examined, presenting opportunities for market differentiation. Overall, the report serves as a strategic resource for understanding the current landscape, technological evolution, and future pathways of the Technical Insulation Market across global regions and sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 10642.11 Million |

|

Market Revenue in 2032 |

USD 17090.3 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Knauf Insulation, Owens Corning, Rockwool, Johns Manville, Saint-Gobain, Isover, Kingspan Group, Armacell, BASF Technical Insulation, Kingspan Insulation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |