Reports

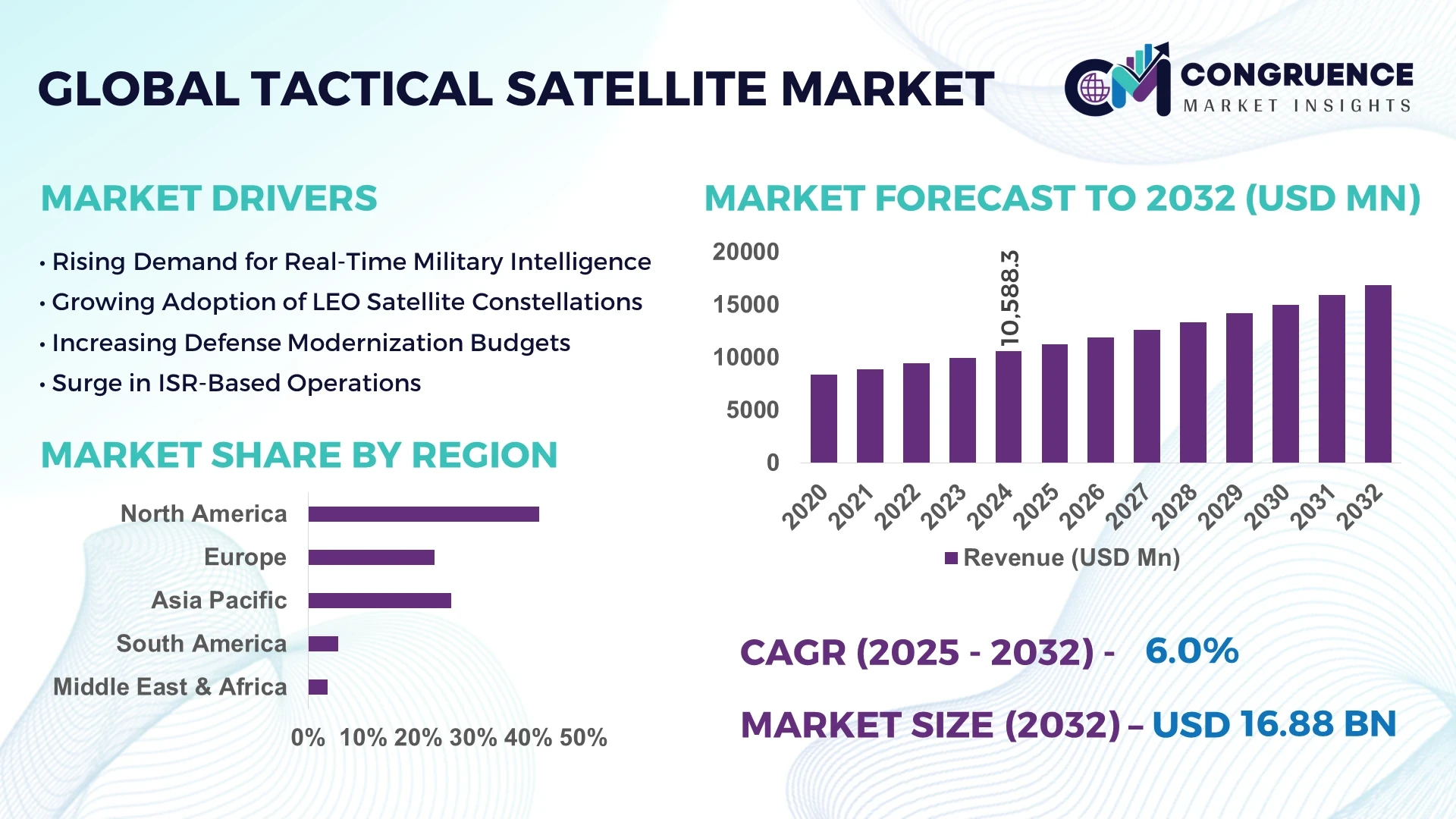

The Global Tactical Satellite Market was valued at USD 10,588.34 Million in 2024 and is anticipated to reach a value of USD 16,876.2 Million by 2032, expanding at a CAGR of 6.%% between 2025 and 2032.

The United States leads the tactical satellite market, with significant investments in advanced defense technologies and satellite systems.The U.S. Department of Defense continues to prioritize the development and deployment of tactical satellites to enhance national security and global military operations.

The tactical satellite market is experiencing robust growth, driven by advancements in miniaturization, propulsion systems, and AI-driven analytics.These innovations have significantly enhanced the capabilities of tactical satellites, enabling more accurate and timely data collection.Governments and private entities are investing heavily in research and development, further accelerating technological progress and broadening the scope of applications.The increasing geopolitical tensions and the need for advanced defense and surveillance mechanisms are also propelling the market forward.As nations strive to safeguard their borders and enhance their military prowess, the demand for tactical satellites that offer superior reconnaissance, communication, and navigation capabilities is on the rise.These satellites provide critical real-time data, improving situational awareness and decision-making processes during military operations.

Artificial Intelligence (AI) is revolutionizing the tactical satellite market by enhancing data processing capabilities, enabling autonomous operations, and improving decision-making processes.AI algorithms are being integrated into satellite systems to analyze vast amounts of data in real-time, reducing the reliance on ground-based processing and enabling faster response times.This integration allows for more efficient use of satellite resources, improved accuracy in data interpretation, and the ability to adapt to changing mission requirements dynamically. The implementation of AI in satellite systems has led to significant advancements in various areas.For instance, AI-driven image analysis has improved the speed and accuracy of object identification, which is crucial for surveillance and reconnaissance missions.Machine learning models are being used to predict satellite component failures, allowing for proactive maintenance and reducing downtime.Additionally, AI is facilitating the development of autonomous satellite operations, where satellites can make decisions without human intervention, increasing operational efficiency and reducing the need for constant ground control.

Furthermore, AI is playing a pivotal role in enhancing satellite communication systems.By utilizing AI algorithms, satellites can optimize signal processing, manage bandwidth more effectively, and improve overall communication reliability.This is particularly important in military applications, where secure and efficient communication is critical.AI also enables the development of adaptive beamforming techniques, allowing satellites to dynamically adjust their signal patterns to maintain optimal communication links. The integration of AI into tactical satellite systems is not only improving current capabilities but also paving the way for future innovations.As AI technology continues to advance, we can expect to see even more sophisticated satellite systems capable of performing complex tasks autonomously, further enhancing the strategic value of tactical satellites in defense and security operations.

“In October 2024, defense technology company Anduril announced a partnership with LA-based startup Apex to utilize their satellite hardware for deploying AI-powered systems aimed at space situational awareness and missile tracking. This collaboration includes plans to launch Anduril's own mission to space in 2025, supported by a $25.3 million contract with the US Space Force to enhance its Space Surveillance Network using AI-driven Lattice software.”

Government defense budgets are increasingly being allocated toward space-based tactical infrastructure, particularly satellites with quick-launch and high-agility features. Countries like the U.S., China, and India have significantly expanded their focus on space as a warfare domain. For instance, the U.S. Space Development Agency has ramped up procurement of low Earth orbit tactical satellites that provide persistent tracking and communication coverage. Military satellite launches globally increased by over 20% in 2023 alone. Tactical satellites, with their capability to rapidly deploy in mission-critical environments, are becoming a core component of national defense strategies. The push toward agile, small satellite constellations is further intensifying this trend.

One of the main restraints in the tactical satellite market is the relatively short operational life of these systems. Tactical satellites typically operate in low Earth orbit (LEO), where atmospheric drag, radiation, and collision risk with space debris significantly reduce their longevity. On average, tactical satellites function efficiently for 3 to 5 years, requiring frequent replacement and launch cycles. This increases the overall expenditure and places pressure on defense budgets, particularly in countries with constrained financial resources. Additionally, re-launch logistics and potential delays in resupply missions can compromise mission continuity, especially during prolonged conflict scenarios.

The market is witnessing unprecedented opportunities driven by the miniaturization of satellite components and the development of next-generation propulsion systems. Innovations in compact propulsion, lightweight materials, and modular hardware are enabling the design of micro and nano tactical satellites with enhanced capabilities. These satellites are not only cost-effective to build and launch but also offer scalability for forming large constellations. For example, advancements in electric propulsion are enabling more efficient maneuvering and extended mission life for compact satellites. This opens doors for commercial defense contractors and space startups to enter the tactical satellite ecosystem, offering new competitive dynamics and fueling growth.

The growing deployment of tactical satellites also exposes them to a rising number of cybersecurity threats and anti-satellite (ASAT) weapon systems. Tactical satellites, often responsible for highly sensitive surveillance and communication functions, are high-value targets for adversaries. Cyberattacks can compromise command protocols, interfere with data transmission, or even cause satellite deactivation. Moreover, the global proliferation of ASAT technologies has escalated the threat to low-orbit tactical assets. In recent years, multiple nations have tested and demonstrated ASAT capabilities, increasing the operational risk to tactical satellites. Ensuring secure communication, hardened systems, and space situational awareness are becoming critical challenges that operators must address.

• Proliferation of Small Satellite Constellations: The tactical satellite market is witnessing a rapid shift toward the deployment of small satellite constellations, particularly in low Earth orbit. Defense agencies and private sector players are increasingly adopting swarms of interconnected tactical satellites to achieve persistent surveillance and improved data redundancy. In 2024 alone, over 150 small tactical satellites were launched for defense-specific applications globally. These constellations enhance responsiveness, reduce latency in communication, and offer better scalability compared to traditional large satellites, making them a preferred choice for modern military strategies.

• Integration of Advanced Imaging and Sensing Technologies: The integration of high-resolution optical, infrared, and synthetic aperture radar (SAR) payloads in tactical satellites has become a dominant trend. These advanced sensors enable 24/7 surveillance capabilities, irrespective of weather conditions or terrain. In 2024, over 40% of newly deployed tactical satellites were equipped with SAR sensors, indicating growing demand for all-weather operational efficiency. Enhanced image analytics also support precision targeting and threat assessment in real time, boosting mission success rates in complex operational environments.

• Shift Toward Rapid Launch Capabilities: There is an accelerating demand for launch-on-demand satellite deployment, especially for tactical scenarios requiring immediate intelligence gathering or secure communication. Countries are investing heavily in responsive launch platforms such as air-launched rockets and mobile ground-based systems. For example, over 20 tactical satellites were launched within 48 hours of demand notification in 2024 under military readiness protocols, showcasing the strategic focus on deployment speed.

• Growth in Public-Private Military Collaborations: Collaborative programs between defense ministries and private aerospace firms are reshaping innovation cycles in the tactical satellite space. Several military space agencies signed contracts in 2024 with private players to co-develop tactical payloads and cost-efficient satellite buses. These partnerships are expediting R&D and helping bring cutting-edge technologies, such as AI-driven satellite control and autonomous operation, to operational readiness. The dual-use capability of such systems further enhances their applicability in disaster relief, environmental monitoring, and secure national communication networks.

The global tactical satellite market is comprehensively segmented by type, application, and end-user, each demonstrating distinct growth trends and deployment priorities. This segmentation helps identify performance-driven satellite technologies, mission-critical operational uses, and specific end-user categories contributing to revenue concentration and accelerated market expansion. The increased focus on agile, multi-role platforms, low Earth orbit deployment, and real-time communication capabilities has led to robust development across various satellite types and functionalities. Key segments such as small satellites and reconnaissance missions are dominating, with governments, defense organizations, and aerospace innovators increasingly investing in advanced satellite architecture tailored to real-time battlefield intelligence, navigation, and secured communication.

The tactical satellite market is segmented into small satellites, micro-satellites, mini-satellites, and nano-satellites. Among these, small satellites (typically 500–1,000 kg) emerged as the leading segment in 2024, accounting for over 38% of global deployments. Their dominance is attributed to their balance between payload capacity and affordability, making them ideal for a wide range of defense operations. Nano-satellites, weighing less than 10 kg, represent the fastest-growing segment and are projected to expand rapidly due to their cost-efficiency and rapid deployment capability. In 2024, over 300 nano-satellites were launched for tactical and reconnaissance missions, a 27% increase compared to the previous year. Mini-satellites and micro-satellites also play crucial roles in signal interception, border surveillance, and encrypted communication, offering a layered advantage in multi-satellite configurations. This segmentation reflects an overarching industry pivot toward flexible, low-cost, and quick-to-launch tactical solutions for dynamic mission requirements.

Key application segments of the tactical satellite market include surveillance and reconnaissance, navigation and positioning, communication, intelligence gathering, and meteorological monitoring. Surveillance and reconnaissance dominated the application landscape in 2024, accounting for nearly 42% of the overall market share, due to increasing military demand for 24/7 monitoring across conflict-prone zones. The communication segment is witnessing the fastest growth, driven by a surge in secure data transfer needs in modern hybrid warfare environments. Secure tactical communication satellites enable encrypted channels for real-time coordination between military assets on land, sea, and air. Navigation and positioning applications are also rising, particularly for autonomous drones and missile systems that require high-precision geolocation data. Meanwhile, meteorological satellites are being integrated for weather prediction in battlefield planning. The continuous need for multi-dimensional battlefield intelligence is driving convergence across these applications, making satellites an indispensable asset in military modernization strategies.

The tactical satellite market is segmented by end-users into defense forces, homeland security, intelligence agencies, aerospace contractors, and emergency response teams. Defense forces remain the dominant end-user, holding over 50% of the market share in 2024, primarily due to their expansive operational mandates ranging from surveillance to cyberwarfare support. Defense departments are also the principal buyers of advanced small and nano-satellite fleets used for theater-specific deployment. Intelligence agencies are the fastest-growing segment, with significant investment in real-time geospatial data, enemy movement tracking, and encrypted signal interception. In 2024, several national intelligence agencies allocated increased funding to expand satellite surveillance networks for border security and threat detection. Homeland security and emergency response units are also leveraging tactical satellites for disaster relief coordination and strategic infrastructure protection. Aerospace contractors, serving as key developers and integrators, are increasingly involved in design, R&D, and satellite-as-a-service models. This dynamic segmentation emphasizes the broadening utility and strategic relevance of tactical satellites across global security ecosystems.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

North America dominates due to heavy defense spending and advanced satellite technology development, with a strong presence of key aerospace contractors and government agencies. Europe holds a significant share owing to its focus on modernization of tactical satellite fleets, while Asia-Pacific’s growth is driven by increasing military investments and emerging space programs in countries like India and China. Middle East & Africa and South America have smaller but rapidly evolving tactical satellite markets due to geopolitical factors and growing defense modernization efforts.

“Advancements and Strategic Deployments in the Tactical Satellite Sector”

North America continues to lead the tactical satellite market with over 42% market share in 2024, backed by significant government and defense contracts. The U.S. Department of Defense alone accounted for launching over 60 tactical satellites in the past two years, focusing on enhanced communication and surveillance. The region emphasizes rapid deployment capabilities with ongoing development of mobile launch systems. Canada is also increasing investments in satellite communication networks for Arctic surveillance. North America’s advanced technological infrastructure enables integration of AI and autonomous systems in tactical satellites. Collaborations between private aerospace firms and defense agencies fuel innovation in small satellite constellations for real-time battlefield intelligence.

“Innovations and Defense Collaborations Driving the Tactical Satellite Market”

Europe holds approximately 25% of the global tactical satellite market, with key contributions from countries like France, Germany, and the UK. The region’s emphasis on joint defense programs through organizations like the European Space Agency is fostering multi-national tactical satellite projects. In 2024, Europe deployed more than 40 tactical satellites focused on secure communication and intelligence gathering. Investments in modular satellite platforms and all-weather synthetic aperture radar payloads are prevalent. European nations prioritize interoperability across NATO partners, accelerating the adoption of shared satellite networks for surveillance. Additionally, private aerospace firms in Europe are focusing on cost-effective tactical satellites to meet growing regional defense needs.

“Rapid Expansion and Technological Adoption in Tactical Satellites”

Asia-Pacific is emerging as the fastest-growing tactical satellite market, driven by expanding defense budgets in China, India, Japan, and South Korea. The region accounted for nearly 18% of the global market share in 2024. China launched more than 50 tactical satellites in 2024 alone, primarily focused on reconnaissance and communication. India’s space agency increased investments in tactical satellite constellations to enhance border security and maritime surveillance. Regional powers are integrating AI-based payloads for autonomous threat detection. The Asia-Pacific also sees rising interest in small and nano-satellites due to cost-effectiveness and rapid deployment capabilities, supporting diverse applications including disaster management and strategic communication.

“Emerging Applications and Market Growth in Tactical Satellites”

South America’s tactical satellite market is smaller, representing about 5% of the global share, but it is showing steady growth due to increasing defense modernization efforts in Brazil and Argentina. Brazil launched three tactical satellites in 2024, mainly for communication and environmental monitoring to support military operations. The region focuses on improving cross-border surveillance capabilities amidst geopolitical tensions. Investments in affordable nano and micro-satellites are rising as nations seek cost-effective solutions for tactical needs. Collaborative regional projects aiming to enhance interoperability among defense forces are underway, promoting shared satellite communication infrastructure. Growing demand for real-time data and intelligence is fostering new tactical satellite applications.

“Defense Modernization and Communication Enhancements in Tactical Satellites”

The Middle East & Africa region holds about 10% of the tactical satellite market share, driven by increasing investments in defense and security infrastructure by countries such as Saudi Arabia, UAE, and South Africa. The region is expanding its tactical satellite capabilities to enhance border security and surveillance in politically volatile zones. In 2024, over 15 tactical satellites were deployed for encrypted communication and real-time intelligence gathering. There is a growing focus on partnerships with global aerospace firms to develop resilient satellite networks. African countries are increasingly adopting tactical satellites for disaster management and resource monitoring, adding dual-use benefits alongside military applications. The region’s strategic location makes satellite-based communication and reconnaissance critical for national security.

United States (38%): Leading in 2024 due to the highest defense expenditure and advanced technological infrastructure supporting tactical satellite deployment and innovation.

China (22%): In 2024, rapidly growing tactical satellite fleet driven by expanding military space programs and strategic focus on border and maritime surveillance.

The Tactical Satellite market is highly competitive with several leading aerospace and defense companies actively investing in research and development to enhance satellite communication capabilities. In 2024, key players focused on innovations such as miniaturized satellite platforms, advanced encryption technologies, and AI-powered payloads to meet evolving defense requirements. The demand for resilient, secure, and rapid-deployment tactical satellite systems has intensified competition, pushing companies to form strategic partnerships and joint ventures. Several firms are expanding their manufacturing capacities to address increasing government contracts, particularly in North America and Asia-Pacific. The market also witnesses significant investment in satellite constellation projects to improve global coverage and real-time intelligence sharing. Additionally, advancements in propulsion and power systems are contributing to longer mission durations and reduced operational costs, further intensifying competitive pressures among market leaders.

Lockheed Martin Corporation

Boeing Company

Airbus SE

Thales Group

Northrop Grumman Corporation

Raytheon Technologies Corporation

L3Harris Technologies, Inc.

General Dynamics Corporation

Mitsubishi Electric Corporation

BAE Systems plc

The Tactical Satellite market is experiencing significant technological advancements driven by the need for enhanced communication security, agility, and real-time data transmission in defense operations. Modern tactical satellites increasingly incorporate high-throughput payloads that enable rapid data transfer and improved bandwidth efficiency, which is critical for battlefield communications and intelligence gathering. Additionally, the integration of software-defined radios (SDRs) allows satellites to dynamically adjust frequency bands and protocols, providing flexibility to counteract electronic warfare threats. Advanced encryption techniques and anti-jamming technologies are now standard features to secure tactical communication links from interception or disruption. The deployment of smaller, more cost-effective microsatellites and nanosatellites is also reshaping the market by enabling rapid constellation deployments for continuous global coverage. Furthermore, improvements in onboard AI and machine learning algorithms support autonomous satellite operations, anomaly detection, and optimized resource management, reducing the need for constant ground control intervention. Power-efficient solar panels and enhanced propulsion systems contribute to longer mission life and maneuverability, ensuring operational resilience in contested environments. These technological trends collectively support the evolving tactical needs of modern armed forces and intelligence agencies worldwide.

In February 2024, Lockheed Martin successfully launched a next-generation tactical communications satellite equipped with advanced anti-jamming technology, enhancing secure data transmission capabilities for U.S. military forces globally.

In August 2023, Airbus deployed a new compact tactical satellite designed for rapid deployment and real-time battlefield communication support, significantly reducing the setup time from weeks to days.

In November 2023, Northrop Grumman announced the integration of AI-powered payload management systems into its tactical satellite lineup, improving autonomous operational capabilities and reducing ground control workload.

In May 2024, Thales Group unveiled its latest encrypted satellite communication system that supports dynamic frequency hopping, significantly boosting resistance against electronic warfare and cyber threats in tactical scenarios.

The scope of the Tactical Satellite Market report encompasses a comprehensive analysis of market segments based on type, application, and end-user industries. It covers various satellite technologies, including geostationary, low Earth orbit (LEO), and medium Earth orbit (MEO) tactical satellites, detailing their capabilities and deployment trends. The report highlights key applications such as secure military communications, intelligence, surveillance, reconnaissance (ISR), and emergency response operations. It also explores growing demand from defense agencies, government bodies, and private security organizations globally. Geographically, the report analyzes regional market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, emphasizing factors driving market growth and adoption in each region. It includes insights into technological advancements like AI integration, anti-jamming features, and miniaturization of satellite payloads, which are shaping the market landscape. Furthermore, the report evaluates competitive strategies adopted by leading players, including product launches, partnerships, and capacity expansions. Key challenges such as high development costs, regulatory complexities, and geopolitical tensions impacting satellite deployment are also discussed. Overall, this report serves as a vital resource for stakeholders seeking to understand tactical satellite market trends, investment opportunities, and future growth prospects through detailed data analysis and market intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 10588.34 Million |

|

Market Revenue in 2032 |

USD 16876.2 Million |

|

CAGR (2025 - 2032) |

6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lockheed Martin Corporation, Boeing Company, Airbus SE, Thales Group, Northrop Grumman Corporation, Raytheon Technologies Corporation, L3Harris Technologies, Inc., General Dynamics Corporation, Mitsubishi Electric Corporation, BAE Systems plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |