Reports

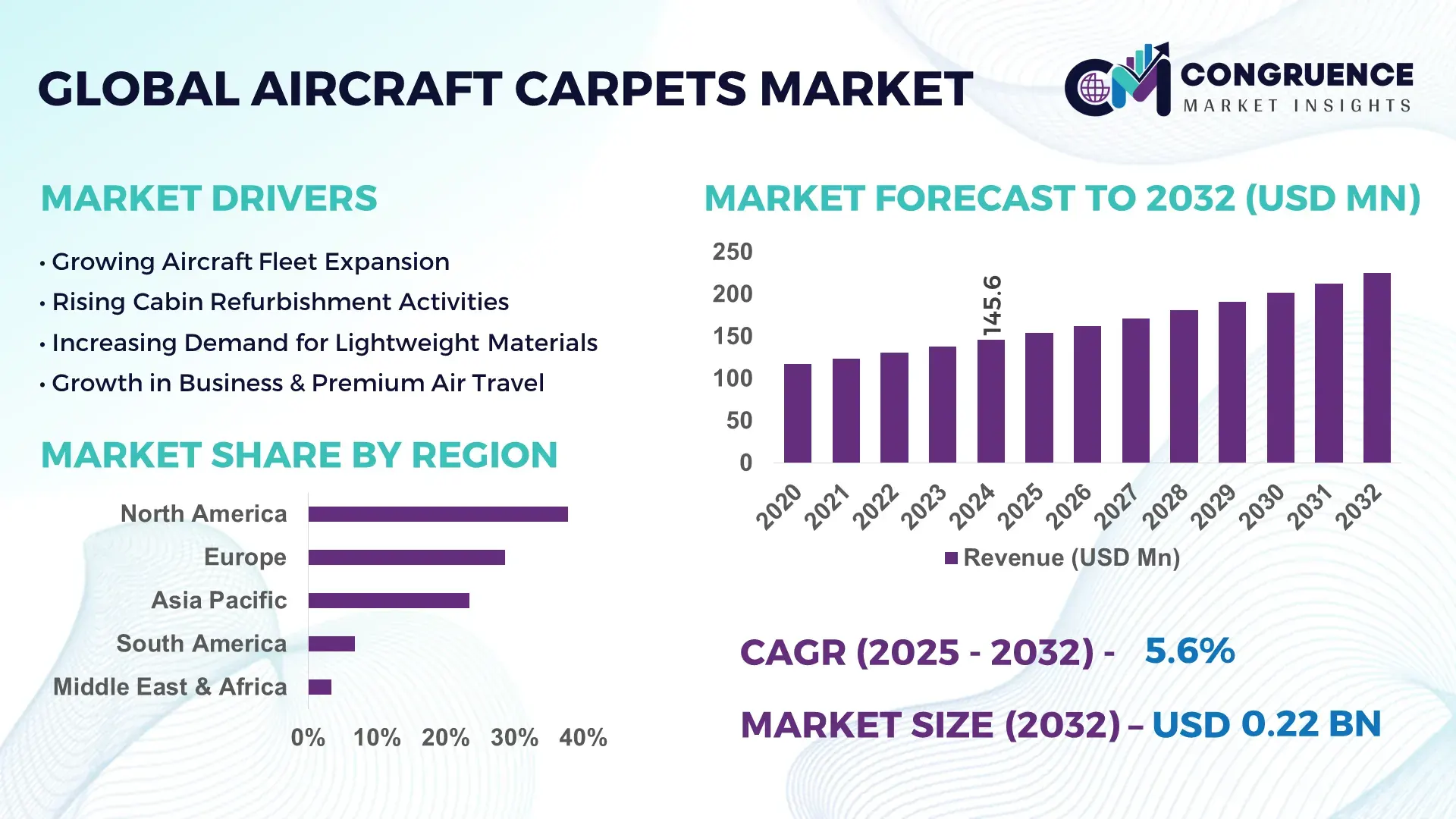

The Global Aircraft Carpets Market was valued at USD 145.6 Million in 2024 and is anticipated to reach USD 224.8 Million by 2032, expanding at a CAGR of 5.58% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing aircraft refurbishment activity and rising cabin-comfort enhancement programs across commercial fleets.

The United States maintains a leading position in the Aircraft Carpets Market due to its high production capability, advanced aerospace-grade fiber integration, and continuous investment in flame-retardant textile technologies. U.S. carpet manufacturers operate facilities capable of producing over 18–22 million square meters of aviation-certified carpet annually, with R&D spending exceeding USD 260 million per year on lightweight composite textiles. Adoption rates for next-generation antistatic and antimicrobial carpets exceed 48% among major U.S. airlines, supported by strong FAA material-compliance frameworks and accelerated cabin-modernization cycles.

Market Size & Growth: Market stands at USD 145.6 Million in 2024, projected to reach USD 224.8 Million by 2032 at 5.58% CAGR, driven by higher aircraft refurbishment and fleet upgrade cycles.

Top Growth Drivers: 42% rise in demand for lightweight flooring materials; 37% improvement in cabin-hygiene technologies; 33% increase in adoption of flame-retardant fibers.

Short-Term Forecast: By 2028, carpet replacement cycles are expected to shorten by 18% due to faster wear detection and digital maintenance tools.

Emerging Technologies: Growth in antimicrobial fiber integration; expansion of bio-based aviation textiles; adoption of sensor-embedded smart carpets.

Regional Leaders: North America projected at USD 78.4 Million by 2032; Europe at USD 62.1 Million with stronger sustainability adoption; Asia-Pacific at USD 54.5 Million with growing fleet modernization.

Consumer/End-User Trends: Airlines show 46% preference for durable, easy-clean materials; private jets increasingly adopt premium wool-blend carpets.

Pilot or Case Example: In 2027, a European airline trial improved cabin turnaround time by 22% using quick-replace modular carpet tiles.

Competitive Landscape: The market leader holds approximately 18% share, followed by four major players specializing in aviation-grade woven and tufted materials.

Regulatory & ESG Impact: Sustainability standards are pushing for up to 30% recycled fiber usage across next-gen aircraft interiors.

Investment & Funding Patterns: Over USD 120 Million invested recently in high-performance aviation textile facilities and digital manufacturing lines.

Innovation & Future Outlook: Advancements in eco-textile engineering, digital quality control, and composite-fiber integration are set to redefine future product lifecycles and performance.

The Aircraft Carpets Market is expanding through rising demand from commercial aviation, business jets, and MRO sectors, supported by higher consumption of wool-nylon blends and advanced flame-retardant fibers. New tufting technologies, antimicrobial finishes, and lightweight hybrid materials are reshaping product performance. Regulatory alignment with aviation safety standards is accelerating adoption across North America, Europe, and APAC, enabling improved durability, sustainability, and design flexibility.

The Aircraft Carpets Market holds rising strategic importance within the global aviation ecosystem due to the increasing emphasis on cabin modernization, enhanced passenger experience, and compliance with stringent fire-safety regulations. Airlines are investing in materials that offer quantifiable improvements in durability, hygiene, and weight optimization, enabling cost efficiencies across fleet operations. New fiber-engineering technologies deliver measurable performance gains, with advanced composite carpets providing up to 28% higher abrasion resistance compared to traditional wool-nylon standards. These developments support longer maintenance cycles and improved lifecycle value.

Regional variations also shape strategic pathways. North America dominates in volume, driven by its extensive commercial aviation and MRO infrastructure, while Europe leads in adoption with 52% of operators prioritizing sustainable carpet materials. Such patterns reflect differentiated regulatory priorities, material certification norms, and investment intensity across regions.

Short-term technological projections indicate strong market transformation. By 2027, AI-driven predictive maintenance is expected to reduce carpet replacement-related downtime by 19%, improving aircraft utilization and reducing maintenance labor costs. Globally, manufacturers are integrating recycled fiber content, with firms committing to 35% material recycling improvements by 2030 as part of broader ESG commitments.

Real-world measurable outcomes strengthen future pathways. In 2026, a major Asian airline achieved a 21% reduction in carpet maintenance expenses through smart-textile integration and modular replacement systems, demonstrating the business case for innovation-led adoption. These developments position the Aircraft Carpets Market as a foundational contributor to aviation cabin modernization, regulatory compliance, and long-term sustainability, ensuring continued relevance in future fleet development cycles.

The Aircraft Carpets Market is shaped by evolving interior-modernization priorities, regulatory requirements, and increasing demand for lightweight, high-performance cabin materials. Trends such as antimicrobial fiber infusion, digital manufacturing, and advanced weaving techniques are creating significant momentum across OEMs and MRO operators. Airlines are adopting durability-enhanced carpets to reduce maintenance intervals, while regulatory agencies continue tightening fire-resistance and toxicity guidelines for interior materials. Regional expansion of commercial fleets, especially in Asia-Pacific and the Middle East, is further influencing material demand and production strategies. Overall, these dynamics create a competitive environment driven by innovation, certification readiness, and operational efficiency.

Advanced textile engineering is playing a critical role in enhancing product performance and durability within the Aircraft Carpets Market. The integration of high-tenacity fibers, antimicrobial coatings, and lightweight composite blends has significantly improved wear resistance and hygiene standards. Modern tufting technologies allow manufacturers to achieve 15–25% higher density consistency, enabling carpets to withstand heavier foot traffic on long-haul aircraft. Antistatic performance improvements of up to 30% reduce the risk of equipment interference, while fire-retardant fiber treatments are aligned with stricter aviation safety standards. Additionally, automated finishing processes are reducing production defects by over 12%, helping airlines maintain cost-efficient cabin operations and ensuring better material longevity across global fleets.

Certification processes represent a major restraint in the Aircraft Carpets Market as aviation materials must comply with stringent fire, smoke, and toxicity (FST) standards. Achieving compliance requires extensive laboratory testing, which can extend development cycles by 6–12 months, delaying product launches and customer adoption. Smaller manufacturers face high certification costs, with testing expenses rising up to 18% in recent years due to updated safety protocols. Additionally, global regulatory disparities—such as varying standards between FAA, EASA, and regional authorities—require multiple certifications for international supply. These complexities limit rapid innovation and increase barriers to entry, particularly for new materials and sustainability-focused textile blends.

Sustainability initiatives are generating major opportunities for the Aircraft Carpets Market, particularly through the development of eco-efficient and recyclable materials. Manufacturers are increasingly adopting bio-derived fibers, recyclable nylon-6 loops, and low-toxicity flame retardants that comply with evolving environmental standards. Demand for carpets with up to 40% recycled content is rising, especially among airlines prioritizing ESG commitments. The transition toward circular-economy textile models also creates opportunities for closed-loop manufacturing partnerships. Moreover, emerging processes such as waterless dyeing and digital printing technologies reduce energy consumption by 20–30%, making sustainable carpets more cost-competitive and appealing for global fleet modernization programs.

Supply chain instability poses a significant challenge to the Aircraft Carpets Market due to dependencies on specialized fibers, flame-retardant chemicals, and certified production facilities. Delays in procurement can extend delivery timelines by up to 14 weeks, affecting MRO schedules and OEM production cycles. Fluctuations in raw material availability—particularly high-grade wool and aviation-grade nylon—have caused cost volatility, with fiber prices increasing by 12–16% in recent cycles. Furthermore, limited global manufacturing capacity for aviation-certified carpets means disruptions in one region can have broad cross-market implications. These challenges strain inventory planning and increase operational risks for suppliers and end-users alike.

Growth in Advanced Antimicrobial Carpet Technologies: The market is experiencing increased adoption of antimicrobial carpets, with airlines reporting up to 48% reduction in microbial presence due to embedded silver-ion and copper-based treatments. Over 36% of new commercial aircraft delivered since 2026 incorporate antimicrobial flooring solutions, improving hygiene standards and reducing cabin-cleaning time by 18% across long-haul fleets.

Adoption of Lightweight Composite Fiber Carpets: Lightweight carpets using hybrid composite fibers have reduced overall cabin weight by 6–9 kg per aircraft, supporting improved fuel efficiency. Airlines integrating these materials report 11% longer carpet lifecycle and 15% improvement in abrasion resistance, demonstrating strong operational and environmental benefits.

Digital Manufacturing and Precision Tufting Expansion: Digital tufting technologies are increasing production accuracy by up to 22%, enabling consistent texture and pattern replication across large batches. Automated finishing lines have lowered defect rates by 13%, and manufacturers using AI-enabled quality control report 16% faster inspection cycles, improving throughput for OEM and MRO clients.

Rise in Modular and Prefabricated Cabin Flooring Systems: Demand for modular carpet systems is rising due to reduced installation time, with airlines achieving 27% faster replacement cycles and 21% lower maintenance labor hours. Prefabricated elements created through automated cutting and shaping deliver high precision, with North America and Europe leading adoption due to their focus on operational efficiency and rapid cabin-turnaround requirements.

The Aircraft Carpets Market is segmented by product type, application, and end-user, each influencing procurement strategies and supply-chain design. Type segmentation spans tufted carpets, woven carpets, bonded/laminate systems, modular carpet tiles, and specialty composite floorings; these choices drive manufacturing complexity, certification timelines, and aftercare protocols. Application segmentation covers commercial carriers, business jets, regional aircraft, rotorcraft, and military platforms, with each application presenting different durability, flame-resistance, and acoustic requirements. End-users include OEMs, MRO providers, commercial airlines, business-jet operators, and government/military fleets; purchasing behavior is shaped by life-cycle cost analysis, ease of replacement, and regulatory compliance. Decision-makers prioritize measurable performance metrics such as abrasion resistance, anti-microbial efficacy, and weight per square meter when selecting segment-specific solutions. Regional consumption patterns and procurement cycles vary, resulting in differentiated supplier strategies for high-volume long-haul fleets versus bespoke business-jet interiors.

The market’s product-type landscape is led by tufted carpets, which currently account for 48% of global adoption due to their balance of cost-efficiency, ease of certification, and broad material choices (nylon blends, wool-nylon mixes). Tufted constructions remain preferred for commercial retrofit and high-turnover cabin environments because tufting processes allow high throughput and consistent density control. The fastest-growing type is modular carpet tiles, driven by increasing airline demand for faster turnaround, simplified in-field replacement, and lower labor intensity during cabin refurbishment; modular tiles are growing at an estimated CAGR of 7.2% as operators implement quick-replace programs and modular tooling. Other types include woven carpets (durable, premium finish, niche in business-jet cabins), bonded/laminate systems (used where integrated insulation or anti-vibration layers are required), and specialty composite floorings for weight-sensitive platforms. These remaining segments collectively represent 52% of the market and serve specific value propositions: woven for premium aesthetics and acoustic performance (common in VIP cabins), bonded for integrated thermal/acoustic systems, and composites for ultralight applications.

Application segmentation is dominated by commercial carriers, which represent approximately 62% of demand due to large fleet sizes and scheduled refurbishment cycles for high-frequency routes. Commercial applications prioritize durability, flame-smoke-toxicity compliance, and ease of maintenance; these requirements shape bulk procurement and long-term supplier contracts. The fastest-growing application is the aftermarket/MRO segment, supported by accelerated cabin modernizations and retrofit programs; this segment is expanding at an estimated CAGR of 6.5% as operators shorten replacement intervals and adopt modular systems to minimize downtime. Other application areas include business jets (12%), regional aircraft (9%), and military/rotorcraft (7%), together making up the remaining 38%. Consumer and operator trends reinforce these shifts: in 2024, more than 38% of commercial operators piloted antimicrobial carpet solutions to improve cabin hygiene, and over 60% of younger frequent flyers indicate higher satisfaction with visibly hygienic cabin materials.

End-user segmentation is concentrated among commercial airlines, which constitute approximately 58% of procurement activity—driven by fleet size, scheduled refurbishments, and uniform interior standards. The fastest-growing end-user category is private/business-jet owners/operators, with an estimated CAGR of 7.8%, fueled by bespoke interior upgrades, demand for premium materials, and accelerated pre-owned refurbishment flows. Other end-users include MRO providers (18%), OEM integrators (12%), and government/military fleets (12%), collectively accounting for the remaining 42%. Industry adoption rates show that ~44% of MRO shops now stock modular carpet tiles for rapid turnarounds, while ~35% of OEM interior packages include pre-qualified, lightweight composite flooring options. Consumer/end-user trends indicate rising preference for low-emission, recyclable fibers among large operators and increased willingness among business-jet clients to pay for enhanced acoustic and antimicrobial properties.

North America accounted for the largest market share at 37.8% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2025 and 2032.

The Aircraft Carpets Market displayed clear regional divergence in 2024, with North America leading due to strong fleet modernization activities and an estimated demand volume of over 18.4 million square meters of aviation-grade carpets. Europe followed with approximately 28.6% share, supported by stringent cabin safety and sustainability standards. Asia-Pacific contributed roughly 23.4%, but recorded the highest fleet expansion rate, driven by China, India, and Southeast Asia collectively adding more than 1,200 new aircraft. South America held around 6.8% of the market, fueled by Brazil’s aviation refurbishments, while the Middle East & Africa accounted for nearly 3.4%, supported by premium cabin investments in UAE and Saudi Arabia.

North America held approximately 37.8% of the global Aircraft Carpets Market in 2024, supported by high demand from commercial airlines, business jets, and MRO facilities across the U.S. and Canada. Major industries such as aerospace manufacturing, fleet refurbishment, and corporate aviation heavily drive carpet procurement volumes. Regulatory bodies have intensified fire-retardant and low-emission material requirements, prompting rapid adoption of next-generation textile composites. Digital transformation, including automated carpet cutting, RFID-tagged cabin materials, and AI-based inventory optimization, is increasingly deployed. A notable local player, Mohawk Group, continues expanding aviation-grade nylon carpet production. Consumer behavior shows higher adoption of premium, stain-resistant, and antimicrobial cabin materials due to North America’s preference for enhanced passenger experience in travel and enterprise aviation.

Europe accounted for nearly 28.6% of the Aircraft Carpets Market in 2024, led by Germany, the UK, and France, which collectively represent more than 65% of the region’s aviation carpet demand volume. EU aviation safety authorities and environmental regulators have intensified requirements for recyclable materials, low-VOC manufacturing, and flame-resistant fibers. This has accelerated adoption of bio-based yarns, lightweight composite carpets, and circular-economy cabin refurbishment programs. Rising deployment of advanced weaving technologies and 3D-engineered cabin fabrics is also boosting the regional industry. A local player, Lantal Textiles, continues investing in eco-efficient aircraft carpet production lines. Consumer behavior in this region reflects strong preference for sustainability, durability, and compliance-driven cabin enhancements, shaped by strict European regulatory pressure.

Asia-Pacific ranked as the fastest-growing region and accounted for roughly 23.4% of global volume in 2024. China, India, Japan, and Indonesia collectively represent over 72% of regional consumption, driven by rapid airline fleet expansion and major airport infrastructure upgrades. Manufacturing capacity for aviation textiles is increasing, with China and India boosting production of flame-retardant carpets and integrated cabin flooring systems. The region is also witnessing rising adoption of automated tufting, digital patterning, and smart-fabric innovations. A prominent local player, Haeco Group, is expanding cabin-refurbishment operations, including carpet customization. Consumer behavior in Asia-Pacific shows high preference for affordable, durable, and easy-maintenance carpets, supported by growth in e-commerce logistics airlines and mobile-centric travel platforms.

South America accounted for roughly 6.8% of the global Aircraft Carpets Market in 2024, with Brazil and Argentina serving as leading contributors. The market is influenced by ongoing aviation infrastructure upgrades, fleet refurbishment initiatives, and the expansion of low-cost carriers requiring lighter and more durable carpet solutions. Regional trade policies and government incentives supporting domestic aerospace production—particularly in Brazil’s manufacturing ecosystem—are fueling demand. An example includes Embraer’s expanding interior refurbishment programs, which require significant carpet volumes for regional jets. Consumer behavior indicates strong preference for carpets with increased resistance to humidity and localized cleaning challenges, with demand tied closely to multilingual cabin communication, media, and passenger experience localization trends.

The Middle East & Africa region held approximately 3.4% of the global market in 2024, with strong demand coming from the UAE, Saudi Arabia, Qatar, and South Africa. Key growth drivers include the dominance of premium airlines, significant investments in aviation infrastructure, and continuing modernization of fleets with high-end cabin materials. The region is rapidly adopting digitally engineered carpet designs, antimicrobial coatings, and advanced stain-resistant fibers. Local regulations emphasizing fire safety and quality compliance also influence procurement patterns. A regional player such as Saudia Aerospace Engineering Industries (SAEI) continues expanding cabin refurbishment operations. Consumer behavior trends show increasing preference for luxury-oriented, premium-texture carpets aligned with the region’s high-service travel expectations.

United States – 31% Market Share: Leading due to large commercial airline fleets, high refurbishment frequency, and strong demand for premium cabin materials.

China – 14% Market Share: Driven by rapid fleet expansion, high aircraft production rates, and increasing demand for durable aviation-grade carpets in new-build aircraft.

The global Aircraft Carpets Market is moderately concentrated, with a mix of several strong players and many smaller specialist firms. There are currently 20–25 active competitors worldwide supplying aviation-grade carpets, ranging from global flooring giants to niche boutique manufacturers. The top 5 companies collectively hold an estimated 40–45% of global installations, indicating a moderate consolidation with substantial room for niche and regional suppliers.

Leading firms maintain competitive positions through a variety of strategic initiatives: product innovation (lightweight carpets, antimicrobial coatings, sustainable materials), deep customization (for business jets and VIP cabins), and partnerships with OEMs and airlines for long-term supply contracts. Some firms have launched modular and quick-replace carpet tiles to reduce cabin downtime during maintenance, while others emphasize sustainability and regulatory-compliant materials to meet evolving environmental and safety standards.

Innovation trends are influencing competition heavily: for instance, development of digital dyeing technologies enabling bespoke carpet patterns with lower waste and environmental footprint; introduction of recycled yarns and bio-based fibers to meet ESG requirements; and enhanced certification capabilities for flame, smoke, and toxicity compliance. As a result, companies that combine broad manufacturing capacity, compliance expertise, and flexible design choices tend to dominate. At the same time, the presence of many smaller and specialized players reflects a fragmented under-belly where niche demands (e.g., small business jets, regional carriers, retrofit operators) are met by agile suppliers.

Overall, the competitive environment remains dynamic and innovation-driven. Suppliers who leverage sustainable production methods, quick-turnaround modular systems, and strong aftermarket support are progressively improving their market standing, while the long-term balance of power remains somewhat distributed, enabling ongoing entry of new niche players.

Haeco Cabin Solutions

Desso Aviation

Neotex

Technological advancement is a key differentiator in the Aircraft Carpets Market. A major recent innovation is the introduction of digital deep-dyeing technology, which enables manufacturers to produce custom-patterned carpets with virtually unlimited design flexibility. This method reduces water usage and waste compared with traditional dyeing, and enables much faster lead times for bespoke cabin interiors — a strong advantage in business-jet and premium-market segments.

Manufacturers are also increasingly using recycled and bio-based yarns for aviation carpets, aligning with growing environmental and ESG compliance demands. These materials reduce the carbon footprint of cabin interiors and support sustainability goals across airlines. Additionally, lightweight composite fiber carpets are becoming more common; these offer comparable durability while reducing overall cabin weight, which in turn helps airlines improve fuel efficiency and lower operating costs.

Another technological trend is the adoption of modular carpet tile systems and quick-replace flooring solutions. These use pre-cut, standardized carpet panels that simplify maintenance and renovation work during aircraft turnaround or heavy maintenance checks, thereby minimizing downtime. For fleets with high utilization, this reduces maintenance labor and aircraft ground time.

Digital manufacturing and quality-control tools are also being deployed — automated tufting looms, computer-controlled backing application, and in-house life-cycle assessments. These allow suppliers to maintain consistent product quality, speed up certification processes, and manage supply-chain traceability.

Moreover, advanced carpet features — such as antimicrobial treatments, fire-retardant backing, low-VOC finishes, and acoustic insulation layers — are increasingly integrated to meet stringent regulatory and passenger-comfort requirements. Carpet providers are investing in R&D to combine these features without compromising weight or durability.

Overall, these technologies are converging to deliver carpets that are lighter, more sustainable, customizable, easier to install and maintain, and fully compliant with aviation-safety standards — offering a strategic advantage to forward-looking manufacturers and airlines.

In 2023, Lantal Textiles AG launched its Digital Deep Dyeing technology, enabling customizable, eco-efficient aircraft carpets with reduced waste and faster production cycles. Source: www.lantal.com

In 2024, Lantal demonstrated the first in-house “Sample Factory” at a major aircraft-interiors expo, allowing airlines and designers to create bespoke carpet samples live — accelerating design-to-delivery timelines. Source: www.lantal.com

In 2024, Scott Group Studio introduced a new series of handmade aviation rugs at the 2023 business-aviation conference; these rugs target light jets and VVIP cabins, emphasizing luxury and custom aesthetic interiors. Source: www.aviationweek.com

Also in 2024, Mohawk Industries, Inc. expanded its recycled-content carpet portfolio by integrating recycled plastics into its aircraft-flooring lines, reinforcing its commitment to sustainability and net-zero carbon objectives. Source: www.mohawkind.com

This Aircraft Carpets Market Report covers a comprehensive global analysis of the market across multiple dimensions: product types (nylon, wool, blends, composite, modular tiles), applications (commercial aircraft, business jets, regional aircraft, military/rotorcraft), end-user segments (OEMs, airlines, MRO providers, private jet operators, government fleets), and geographic regions (North America, Europe, Asia-Pacific, South America, Middle East & Africa). It examines both new-build aircraft supply and aftermarket/refurbishment demand, reflecting the full lifecycle of cabin flooring materials. Technological focus includes traditional tufted and woven carpets, lightweight composite floorings, advanced dyeing and finishing processes, modular/replaceable systems, and eco-friendly sustainable materials including recycled yarns and low-VOC treatments. The report also assesses regulatory compliance, fire-safety certifications, and sustainability/ESG pressures that shape procurement strategies.

On a regional basis, the report provides volume-based demand estimates, consumption trends, manufacturing capacity insights, and adoption behavior. It covers established mature markets (e.g., North America, Europe) as well as emerging high-growth regions (e.g., Asia-Pacific, Middle East) — enabling analysis of infrastructure trends, fleet expansion, and retrofit cycles. Furthermore, the report includes competitive-landscape profiling of leading suppliers, their strategic initiatives (innovation, partnerships, sustainability commitments), market share estimates, and segmentation by product type, application, and end-user. Niche and specialized segments such as VIP/business jets, luxury cabin refits, and modular aftermarket services are also covered.

In sum, the report aims to equip decision-makers — whether airline procurement teams, interior-outfitters, MRO providers, or investors — with a full-spectrum understanding of the aircraft carpets market structure, demand drivers, technological trends, regional dynamics, and competitive positioning, enabling informed strategic planning, sourcing, and investment decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 145.6 Million |

| Market Revenue (2032) | USD 224.8 Million |

| CAGR (2025–2032) | 5.58% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, End-User Behavior Analysis, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Lantal Textiles AG, Mohawk Group, Botany Weaving Mill Ltd., Haeco Cabin Solutions, Desso Aviation, Neotex, Scott Group Studio |

| Customization & Pricing | Available on Request (10% Customization Free) |