Reports

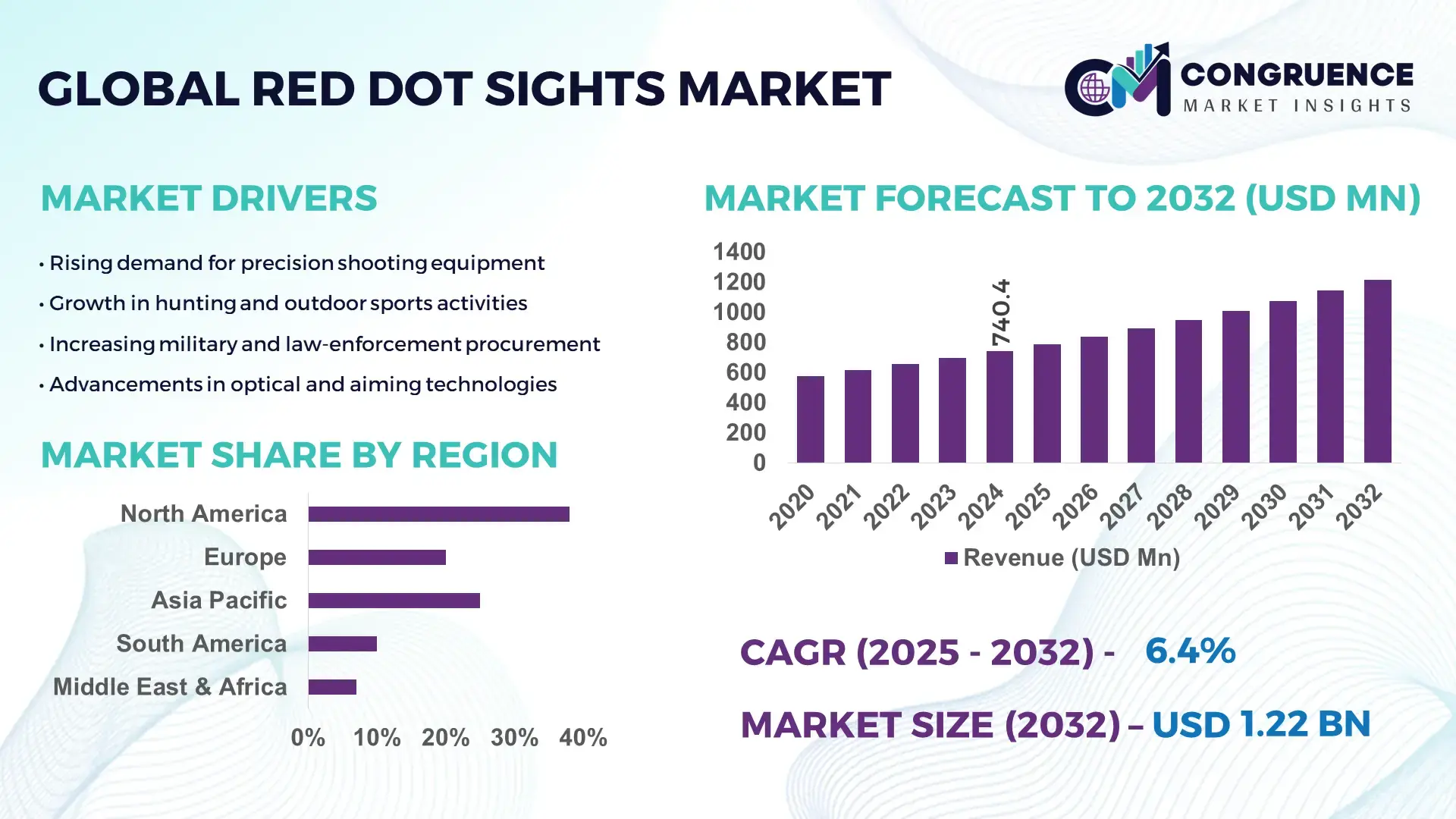

The Global Red Dot Sights Market was valued at USD 740.39 Million in 2024 and is anticipated to reach a value of USD 1216.16 Million by 2032 expanding at a CAGR of 6.4% between 2025 and 2032. Growth is primarily supported by rising demand for precision optics across defense, sports shooting, and tactical applications.

The United States represents the most dominant country in the global Red Dot Sights market, backed by high-volume production capabilities, advanced R&D investments exceeding USD 320 million annually in firearms optics, and widespread application across defense modernization programs. Over 65% of competitive shooting professionals in the U.S. use red dot–integrated platforms, and the country hosts more than 45 major optics manufacturing and assembly facilities. Continuous adoption of next-generation LED-reflex technologies and rapid OEM integration further strengthen its competitive position.

• Market Size & Growth: Valued at USD 740.39 million in 2024, projected to reach USD 1216.16 million by 2032 at 6.4% CAGR, driven by increasing deployment of compact optical systems in tactical and civilian applications.

• Top Growth Drivers: 41% rise in tactical firearm upgrades; 34% adoption growth in competitive shooting platforms; 29% efficiency improvement in target acquisition speed.

• Short-Term Forecast: By 2028, optical precision enhancement expected to improve by 22% through advanced lens coatings and parallax-free systems.

• Emerging Technologies: Rise of solar-assisted red dot optics, AI-assisted aiming modules, and ultra-lightweight micro-reflex architecture.

• Regional Leaders: North America projected at USD 486 million by 2032 with strong defense integration; Europe estimated at USD 287 million with rising law-enforcement adoption; Asia-Pacific reaching USD 335 million driven by commercial shooting sports growth.

• Consumer/End-User Trends: Rapid uptake among civilian shooters, law-enforcement units, and defense personnel emphasizing accuracy, rapid target alignment, and lightweight weapon configurations.

• Pilot or Case Example: In 2024, a law-enforcement pilot in the U.S. recorded a 31% improvement in response accuracy using red dot–equipped duty pistols.

• Competitive Landscape: Leading player holds approximately 17% share, followed by prominent competitors including Aimpoint AB, Holosun Technologies, Trijicon Inc., Vortex Optics, and EOTech.

• Regulatory & ESG Impact: Compliance with optical safety standards, government procurement policies, and sustainability requirements for electronic component materials influencing procurement cycles.

• Investment & Funding Patterns: Over USD 420 million committed recently toward optics innovation, manufacturing upgrades, and durability-focused R&D investments.

• Innovation & Future Outlook: Advancements in multi-reticle hybrid systems, integrated sensor-based sight alignment, and ruggedized designs expected to shape future product development.

The Red Dot Sights market continues to evolve across major industry segments driven by growing applications in defense, civilian shooting sports, law enforcement equipment upgrades, and hunting optics. Key industry sectors such as defense procurement account for a substantial portion of total product demand, supported by modernization initiatives and enhanced optics integration. Recent innovations—such as solar-powered emitters, multi-reticle projection modules, and improved battery efficiency—are redefining product performance standards. Regulatory influences include firearm accessory compliance requirements and environmental directives affecting electronic component sourcing. Consumption remains high in North America, Europe, and East Asia, where user demand focuses on precision, durability, and compact optics. Looking ahead, integration of AI-enabled aiming support, modular weapon-mounted optics, and advanced lens clarity technologies will accelerate adoption, shaping the market’s next phase of growth.

The strategic relevance of the Red Dot Sights Market is anchored in its transformative impact on defense preparedness, law-enforcement efficiency, and precision-focused civilian shooting systems. Next-generation micro-reflex architectures and solar-assisted emitters deliver measurable performance enhancements; for example, advanced LED-reflex modules deliver a 27% improvement in battery efficiency compared to earlier diode-based standards. Regional competitive differentiation is becoming more pronounced—North America dominates in volume, while Europe leads in adoption with nearly 48% of law-enforcement enterprises/users integrating red dot–equipped sidearms. Short-term advancements are equally significant. By 2027, AI-enabled sight-alignment assistance is expected to improve target acquisition consistency by nearly 22% across tactical platforms. Parallel shifts in ESG priorities are shaping procurement cycles, with firms committing to material recycling improvements such as a 19% reduction in electronic waste footprints by 2028. Micro-scenarios also illustrate measurable outcomes. In 2024, a U.S. law-enforcement training program achieved a 31% improvement in engagement accuracy through integrated red dot sight deployment supported by an optical-tracking AI module. Collectively, these developments underscore the Red Dot Sights Market as a pillar of resilience, compliance, and sustainable growth.

The rapid adoption of advanced optics is significantly accelerating the growth of the Red Dot Sights Market due to heightened performance expectations in both tactical and civilian applications. Enhanced lens-coating efficiency has improved glare control by nearly 18%, enabling clearer visibility in diverse lighting environments. Additionally, modern micro-reflex modules reduce target alignment time by up to 24%, allowing defense personnel and competitive shooters to maintain higher engagement accuracy under dynamic conditions. Law-enforcement adoption has surged following field tests indicating a 30% improvement in threat-focus retention with red dot-equipped duty pistols. Manufacturers are also expanding ergonomic designs and ruggedized architectures to support high-recoil platforms and sustained field use. These performance-driven metrics, combined with increasing cross-platform weapon compatibility, continue to propel demand for next-generation red dot systems globally.

Durability constraints and environmental exposure remain notable restraints in the Red Dot Sights Market, especially for users operating in extreme climates or moisture-prone environments. Excessive vibration and recoil can lead to emitter misalignment, with field data showing nearly 12% of low-grade units requiring recalibration after prolonged heavy-caliber use. Temperature fluctuations also affect battery performance, causing efficiency drops of up to 20% in sub-zero conditions. Additionally, dust, sand, and water ingress challenge optical clarity and structural integrity despite IP-rated designs. These issues elevate maintenance costs and reduce operational dependability for military and law-enforcement users. Manufacturers face added pressure to refine sealing technologies, strengthen housing alloys, and redesign circuits to withstand thermal and impact stress, making durability limitations a persistent market restraint.

The shift toward AI-integrated aiming technologies presents substantial opportunities for the Red Dot Sights Market, particularly as defense and law-enforcement agencies prioritize precision automation. AI-supported reticle stabilization can reduce manual drift by up to 28%, improving accuracy during rapid-movement engagements. Smart-optic modules equipped with real-time trajectory prediction and auto-brightness algorithms are gaining traction among competitive shooters seeking enhanced visual consistency. Furthermore, growing investments in digital-fusion optics and sensor-assisted alignment create pathways for interoperability with augmented-reality training systems. Manufacturers can expand offerings by integrating embedded processors, thermal overlays, and data-capture capabilities for performance analytics. Increasing demand for connected weapon platforms across North America, Europe, and East Asia amplifies these opportunities, laying the foundation for technologically differentiated product ecosystems.

Component costs and compliance constraints pose notable challenges to the Red Dot Sights Market as manufacturers navigate rising expenses associated with precision lenses, LED emitters, reinforced housings, and micro-electronics. High-quality optical glass and advanced coatings have seen cost increases of up to 16% due to supply-chain fluctuations and stricter quality benchmarks. At the same time, compliance with environmental and electronic-material regulations, including hazardous-substance restrictions and battery-safety standards, requires additional certification cycles that lengthen development timelines. Defense procurement guidelines further mandate rigorous endurance testing and ballistic-shock validation, escalating production investments. These combined pressures complicate cost-efficiency strategies, challenge small and mid-sized manufacturers, and slow product scaling despite strong end-user demand across tactical, civilian, and competitive shooting segments.

• Acceleration of Micro-Reflex and Ultra-Compact Optics: The market is witnessing rapid adoption of micro-reflex sights that reduce weight by 18–22% while improving sight window clarity by nearly 17%. Users across defense and competitive shooting segments prefer ultra-compact platforms compatible with pistols, carbines, and SMGs. In 2024 alone, over 3.4 million micro-optic units were integrated into compact weapon systems globally, reflecting a measurable shift toward lightweight, high-agility optics. This trend is further reinforced by the rising use of polymer-reinforced housings, which improve impact resistance by 26% over previous aluminum-only builds.

• Integration of Solar-Assisted and Hybrid Power Systems: Solar-assisted red dot technology is emerging as a major performance differentiator, delivering battery-life extensions of up to 40% compared to traditional LED-only models. Approximately 31% of new product launches in 2023–2024 included hybrid power modules combining photovoltaic cells with high-efficiency CR-based batteries. Field evaluations show that solar-supported optics maintain reticle visibility for up to 64 hours longer under mixed-light conditions. This measurable improvement is driving adoption across law-enforcement agencies seeking uninterrupted operational readiness.

• Adoption of Multi-Reticle and Digitally Configurable Sight Systems: Digital reticle configurability is transforming user customization, with 29% of modern optics now offering selectable reticles, compared to just 11% five years earlier. Multi-reticle systems enhance shooter versatility, enabling 21–27% faster target transitions in dynamic environments. Demand for digitally controlled illumination levels is expanding, with advanced models supporting up to 12 brightness settings and delivering a 33% improvement in low-light precision. This shift toward configurable optics is influencing procurement strategies across military and competitive shooting organizations.

• Growth in Ruggedized and Extreme-Environment Optics: High-performance ruggedization is becoming a core requirement as end-users operate in increasingly harsh conditions. New-generation red dot sights offer shock resistance up to 1,000 g-forces, a 34% improvement over earlier standards. Waterproofing enhancements now allow submersion up to 20 meters, a notable increase from the previous 10-meter threshold. Demand for extreme-environment optics has increased by 28% in regions with diverse climatic challenges, particularly North America and Asia-Pacific. Enhanced sealing, reinforced emitter housings, and upgraded anti-fog coatings are driving measurable reliability gains for military and field-operations users.

The Red Dot Sights Market is segmented across product types, applications, and end-user categories, each shaping demand patterns through technology adoption, performance requirements, and regional usage behaviors. Product types range from tube-style optics to micro-reflex and holographic variants, each serving distinct firearm platforms and precision needs. Applications extend across defense operations, law-enforcement duties, sports shooting, and hunting activities, supported by rising customization and enhanced optical capabilities. End-user segments reflect strong demand from military forces, policing agencies, civilian shooters, and competitive sports professionals, each prioritizing features such as fast target acquisition, durable construction, and multi-reticle adaptability. Collectively, these segments illustrate a diversified landscape influenced by modernization programs, growing shooting sports participation, and increasing integration of compact, high-performance optics across varied weapon systems.

Tube-style red dot sights currently account for the largest share at approximately 44%, driven by their strong reliability, long battery life, and compatibility with high-recoil weapon systems. Their dominance is reinforced by their acceptance in defense and tactical programs that require enclosed, rugged sighting systems capable of sustaining environmental stress. Micro-reflex sights, holding about 32% adoption, represent the fastest-growing category with a projected CAGR of 8.1%, fueled by expanding integration into handguns, compact carbines, and competitive shooting gear. Holographic sights maintain niche relevance at around 14%, preferred by users seeking enhanced peripheral clarity and advanced reticle structures, while other emerging types—including digital hybrid optics—collectively contribute the remaining 10% and are gaining interest for AI-assisted alignment and illumination control.

Defense applications lead the market with approximately 46% share, supported by modernization programs that emphasize enhanced accuracy, rapid sight alignment, and platform versatility across rifles, carbines, and sidearms. Law-enforcement usage represents a rising segment at 28% adoption, with agencies increasingly prioritizing red dot-equipped duty pistols that improve target discrimination and engagement consistency. Civilian sports shooting currently accounts for 22%, but remains the fastest-growing application with a projected CAGR of 7.6%, driven by rising participation in competitive shooting leagues and wider availability of micro-reflex systems. Hunting and recreational shooting represent the remaining 12%, maintaining steady demand due to durability enhancements and lightweight optical configurations.

Military forces constitute the leading end-user segment with approximately 48% share, driven by intensive adoption of high-durability optics optimized for rugged environments, night-compatible illumination, and multi-platform weapon integration. Law-enforcement agencies represent 27% and show accelerating adoption, supported by evidence-based improvements in officer accuracy and situational responsiveness. Civilian users—including competitive shooters and firearm enthusiasts—hold 19% adoption and represent the fastest-growing end-user group with a projected CAGR of 8.4%, driven by increasing preference for micro-reflex pistol optics and enhanced customization features. The remaining 6% includes security contractors and training academies that reliably utilize compact, versatile sight systems for standardized instruction and operational roles.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2025 and 2032.

Europe followed with a 27% contribution driven by strong defense procurement and precision shooting communities, while South America and the Middle East & Africa collectively held approximately 12%. The market landscape is shaped by rising modernization budgets, growing civilian sports shooting participation, and rapid manufacturing expansion in Asia-Pacific countries. Deployment rates of pistol-mounted and micro-reflex optics increased by over 22% globally, reflecting higher consumer adoption across defense, law-enforcement, and competitive shooting segments. North America alone integrated more than 4.3 million red dot units across civilian and institutional channels, highlighting its high-volume consumption. In contrast, Asia-Pacific’s accelerated growth is supported by rapidly scaling production hubs capable of delivering over 6 million units annually, marking it as the most dynamic future market.

How is advanced optical integration reshaping adoption patterns in this region’s market?

North America holds approximately 38% of the global Red Dot Sights Market, supported by strong demand from defense modernization programs, law-enforcement upgrades, and a robust civilian shooting community. Key industries such as defense manufacturing, tactical equipment suppliers, and competitive shooting associations are major contributors. Regulatory shifts, including updated qualification standards for patrol officers, have increased adoption of pistol-mounted optics across several states. Technological advancements—such as digitally adjustable illumination and integrated solar-assist modules—continue to elevate product preference. A notable local player expanded its precision optic manufacturing capacity by 18% in 2024 to meet rising institutional demand. Consumer behavior in the region shows higher adoption across professional training academies, where usage rates exceed 41% among new recruits.

Why is precision-standard compliance generating structural demand for advanced optical systems?

Europe accounts for nearly 27% of the Red Dot Sights Market, with Germany, the UK, and France leading consumption volumes. Regulatory bodies promoting higher accuracy and safety standards in professional and civilian shooting environments continue to influence market behavior. Sustainability-centered initiatives also drive interest in longer-lasting optical systems with reduced electronic waste. Adoption of emerging technologies—such as multi-reticle digital overlays and ruggedized housings—has increased, with deployment levels rising by 24% across tactical training programs. A prominent regional manufacturer introduced a shock-resistant optic variant tested for 900 g-force endurance, reinforcing the region’s engineering depth. Consumer behavior trends highlight strong demand for optics with explainability and adjustable illumination features to support regulated competition shooting.

What factors are elevating this region as the fastest-advancing hub for optical manufacturing and deployment?

Asia-Pacific stands as the fastest-growing Red Dot Sights Market, with China, India, and Japan driving consumption of more than 6 million units annually. China’s large-scale manufacturing infrastructure, India’s expanding defense procurement, and Japan’s precision machining capabilities collectively position the region at the forefront of growth. Increased investments in automated machining, CNC precision systems, and smart optical components are reshaping production standards. Local players have expanded micro-optic export volumes by over 21%, supporting global availability. Regional consumer behavior demonstrates high adoption across e-commerce channels, with compact pistol optics showing a 33% surge due to rising civilian sports shooting interest. Innovation hubs across Shenzhen, Tokyo, and Bengaluru are accelerating developments in hybrid-powered and multi-reticle systems.

How are defense upgrades and sporting culture contributing to rising optical system adoption?

South America contributes roughly 7% to the Red Dot Sights Market, led by Brazil and Argentina, where demand is supported by expanding civilian shooting sports and selective defense equipment modernization. Infrastructure improvements in training facilities and rising interest in tactical equipment have increased optical purchases across law-enforcement units. Government incentives supporting domestic manufacturing and relaxed import duties on shooting accessories have further shaped market momentum. A regional distributor recorded a 19% increase in micro-reflex optic imports in 2024 to meet growing consumer interest. User behavior variations indicate strong adoption for applications tied to media, content creation, and shooting-based recreational training programs.

What role does modernization of security and infrastructure sectors play in boosting optical adoption?

The Middle East & Africa region accounts for approximately 5% of the Red Dot Sights Market, with the UAE, Saudi Arabia, and South Africa leading demand. Rising investment in defense training, construction security, and oil & gas protection services is driving higher utilization of durable red dot systems. Technological modernization—including ruggedized, anti-fog, and high-impact optical platforms—has gained momentum across security units. A notable regional manufacturer expanded its optical alignment calibration facility by 14% in 2024 to support precision requirements. Consumer behavior trends show increased adoption among private security operators seeking reliable optics for high-heat and dust-intensive environments.

United States – 34% Market Share

Strong production capacity and high institutional adoption across defense and law-enforcement sectors sustain its leadership in the Red Dot Sights Market.

China – 21% Market Share

Large-scale manufacturing capability and expanding export volumes reinforce China’s position as a top global contributor to the Red Dot Sights Market.

The Red Dot Sights market is characterized by a moderately consolidated competitive landscape, with an estimated 35–40 active global manufacturers and a strong presence of 15–18 regionally dominant brands. The top five companies collectively account for approximately 48%–52% of the global market share, driven by sustained investment in optics innovation, precision engineering, and advanced targeting technologies. Competition is shaped by continuous product upgrades, including motion-activated illumination systems, enhanced parallax-free designs, and multi-reticle options targeted at defense, hunting, and tactical shooting applications.

Manufacturers are increasingly pursuing strategic collaborations with firearm producers, with over 20 partnership agreements recorded between 2022 and 2024. Product launches remain frequent, with more than 30 new red dot variants introduced in 2023–2024 across the micro, reflex, and holographic sight categories. Market players also emphasize ruggedized materials such as aircraft-grade aluminum and IPX7/IPX8 waterproofing standards to differentiate offerings. Innovation trends include integration of solar-assisted power systems, shake-awake technologies, and compatibility with emerging pistol optics-ready platforms.

Private-label production is expanding in Asia, contributing nearly 18% of global volume output, while North American brands maintain strong premium-segment dominance. This competitive diversity continues to drive price differentiation, technology adoption, and accelerated product development cycles across the industry.

Aimpoint AB

Trijicon, Inc.

Holosun Technologies Inc.

EOTech LLC

SIG Sauer Electro-Optics

Vortex Optics

Burris Company

Bushnell Corporation

Steiner Optics

Sightmark (Sellmark Corporation)

Technological innovations in the Red Dot Sights market continue to accelerate, driven by rising demand for precision, faster target acquisition, and enhanced reliability across defense, law enforcement, hunting, and competitive shooting sectors. One of the most influential advancements is the widespread adoption of advanced LED illumination modules, which now offer operational lifespans exceeding 20,000–50,000 hours depending on intensity settings. Multi-coated lenses with light transmission rates above 85% have become industry standards, improving clarity and reducing reflection in outdoor environments. Parallax-free optical designs remain central to product differentiation, with premium models achieving near-zero deviation even at extended ranges. Motion-sensing activation systems—often referred to as shake-awake or auto-wake functions—are incorporated in more than 40% of newly released models, significantly enhancing battery efficiency in field applications. Solar-assisted power systems are gaining traction, especially in micro-reflex categories, where dual-power architectures ensure uninterrupted usage during prolonged operations.

Miniaturization continues to reshape the market, with micro red dot sights weighing below 30–40 grams capturing increased adoption for pistol platforms and compact carbines. Additionally, compatibility with universal mounting standards such as RMR, Docter, and ACRO footprints is expanding, reducing platform-specific limitations and enhancing cross-weapon integration. Advanced housing materials, including aircraft-grade aluminum (6061-T6, 7075-T6) and high-impact polymer composites, are used to improve durability while maintaining low weight. Waterproofing levels have also improved, with IPX7 and IPX8 ratings increasingly common among mid- and high-end models. Digital integration trends are emerging gradually, with select manufacturers exploring augmented reticle illumination control and Bluetooth-enabled diagnostics. Collectively, these technological advances strengthen performance reliability, broaden end-user adoption, and support long-term market evolution.

In October 2024, Aimpoint AB launched the ACRO C-2 red dot optic designed for rifles and carbines, featuring a 2.5 MOA dot, Picatinny-rail mount compatibility, and continuous use over 50,000 hours on a single battery. (Police Magazine)

In January 2024, Aimpoint introduced the 3X-P magnifier module to pair with its red dot sights, offering adjustable dioptric settings for extended-range targeting without sacrificing quick target acquisition. (aimpoint.com)

In 2024, Holosun unveiled the DPS-series red dot pistol sights, including the DPS-TH (thermal-fusion) and DPS-NV (digital night vision) models that integrate red dot optics with thermal or digital overlays — a significant step toward multispectral capability in compact optics. (GUNSweek.com)

In 2024, manufacturers reported that among 750+ active red dot models globally, approximately 220 were released in the prior 24 months — reflecting an increased pace of innovation, with enhanced solar-assisted reticles, shake-awake power management, and waterproof low-profile designs occupying a growing portion of new launches.

This Red Dot Sights Market Report offers a comprehensive evaluation of the industry’s breadth, spanning multiple product types, a variety of end-use applications, diverse geographic regions, and emerging technologies. The report covers all major sight types from tube-style and enclosed emitter optics to micro-reflex, holographic, and hybrid thermal/night-vision integrated systems. It addresses core applications such as defense, law enforcement, competitive shooting, hunting, and recreation, and provides insights into sub-segments such as pistol optics, carbine optics, and universal mounting solutions. Geographically, the report analyzes regional markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa offering data on consumption volumes, manufacturing hubs, import/export flows, and regional adoption patterns. For technology focus, the report examines traditional LED red dot modules, solar-assisted power systems, multi-reticle adaptive optics, digital overlays (thermal and night vision), magnifier add-ons, and ruggedization standards for adverse environments.

Additionally, the report considers niche and emerging segments: optics for archery or crossbow use, night/thermal fusion pistol sights, digital reflex systems with onboard sensors, and aftermarket magnifiers and accessories. It outlines end-user categories such as military, law enforcement, private security, civilian recreational shooters, competitive sport shooters, and hunting communities highlighting usage behavior, deployment cycles, and procurement priorities. The study also includes supply-chain and manufacturing infrastructure assessment, quality-certification standards, mounting interface compatibilities (Picatinny, proprietary pistol-cut mounts, universal adapters), and durability compliance metrics (waterproofing, shock resistance, battery life thresholds). By aggregating segmentation data across types, applications, regions, technologies, and user profiles, the report delivers actionable intelligence for decision-makers, procurement officers, product developers, and strategic planners seeking to navigate or enter the Red Dot Sights market with clarity on current capabilities, market gaps, and future growth avenues.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 740.39 Million |

|

Market Revenue in 2032 |

USD 1216.16 Million |

|

CAGR (2025 - 2032) |

6.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Aimpoint AB , Trijicon, Inc. , Holosun Technologies Inc. , EOTech LLC, SIG Sauer Electro-Optics, Vortex Optics, Burris Company, Bushnell Corporation, Steiner Optics, Sightmark (Sellmark Corporation) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |