Reports

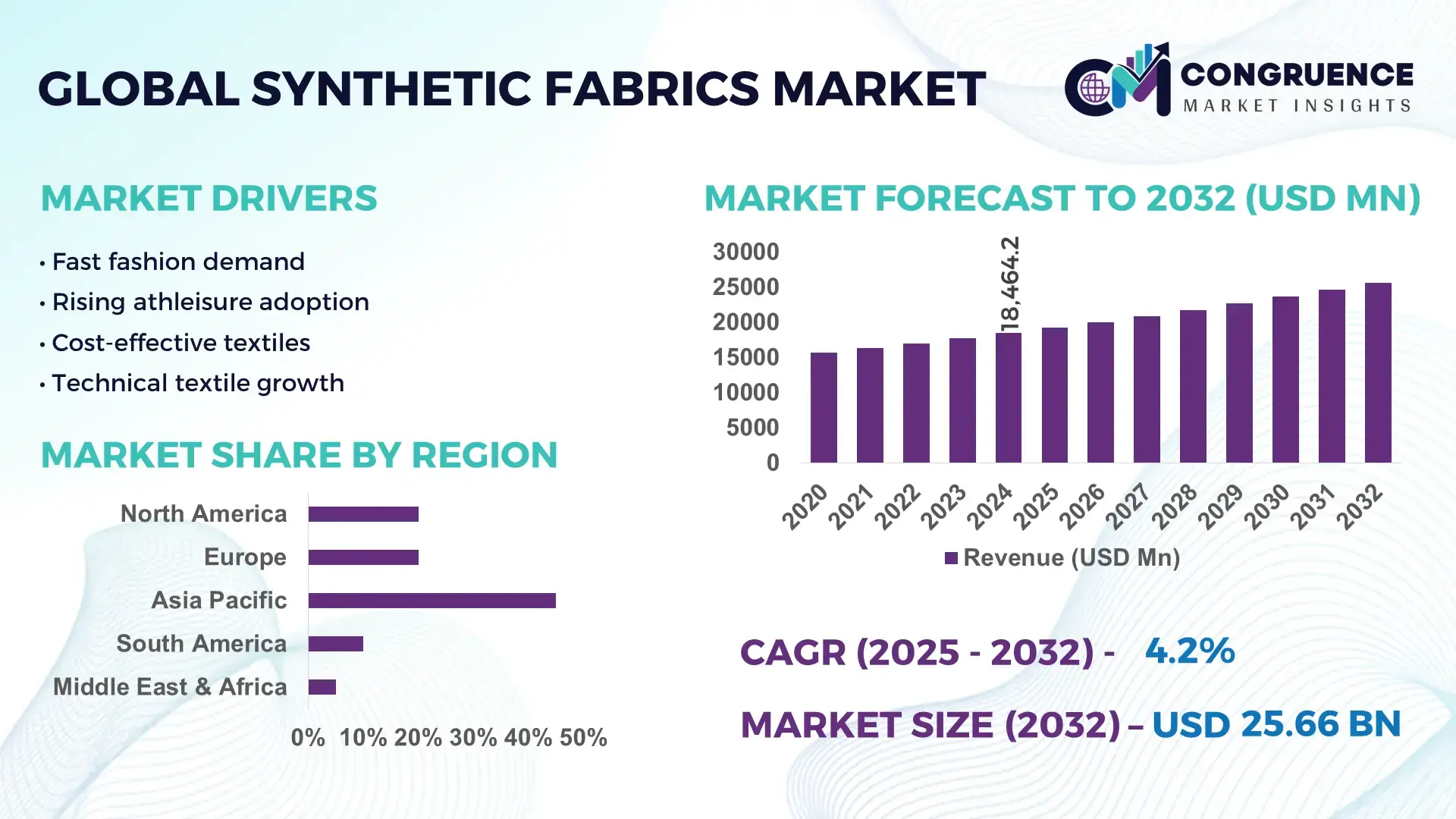

The Global Synthetic Fabrics Market was valued at USD 18464.24 Million in 2024 and is anticipated to reach a value of USD 25660.97 Million by 2032 expanding at a CAGR of 4.2% between 2025 and 2032. This growth is driven by increasing demand across apparel, automotive, home textiles, and industrial applications due to synthetic fabrics’ durability and cost advantages.

China is the foremost country in the synthetic fabrics landscape, with production output exceeding tens of millions of metric tons annually and vast integrated facilities covering polymerization to finished textiles. Its investment in advanced manufacturing technologies and R&D propels enhancements in high-performance polyester and nylon fabrics, with over 60% of its textile mills oriented toward synthetic fabric production. China’s export-oriented infrastructure supports large-scale shipment volumes to global markets, and it continues to invest heavily in sustainable textile technologies and automation to support future demand.

Market Size & Growth: 2024 market valued at USD 18,464.24 M, forecast to reach USD 25,660.97 M by 2032 at a 4.2% CAGR, supported by broadening use in diversified end-use industries.

Top Growth Drivers: Apparel sector adoption increase ~46%, automotive material substitution ~15%, and industrial textile demand growth ~12%.

Short-Term Forecast: By 2028, synthetic fabric cost efficiencies and production yield improvements expected to enhance output performance by ~18%.

Emerging Technologies: Growth in moisture-wicking polymer blends and antimicrobial treatments; adoption of automated weaving technologies.

Regional Leaders: Asia-Pacific ~USD 10,800 M by 2032 with expanding textile hubs; North America ~USD 5,400 M driven by technical textiles; Europe ~USD 4,200 M with sustainability-focused fabrication.

Consumer/End-User Trends: Rising preference for performance and activewear fabrics; growth in home textile applications due to e‑commerce penetration.

Pilot or Case Example: 2025 pilot of automated polyester dyeing technology reduced energy consumption by ~22%.

Competitive Landscape: Market leader ~25% share with China‑based conglomerates, followed by key players Far Eastern New Century, Toray Industries, Reliance Industries, and Hyosung.

Regulatory & ESG Impact: Stricter environmental mandates promoting recycled content and cleaner dyeing technologies shaping manufacturing norms.

Investment & Funding Patterns: Recent infusion of over USD 1.2 B in textile tech facilities and circular economy initiatives across APAC.

Innovation & Future Outlook: Continued focus on sustainable polymers, bio‑based synthetic fibers, and integration of AI‑enabled process controls enhancing competitive positioning.

The Synthetic Fabrics Market is heavily influenced by key industry sectors such as apparel, automotive interiors, and home furnishing textiles, which collectively contribute significant usage volumes. Recent technological innovations include advanced moisture management and antimicrobial finishes that improve product performance in activewear and healthcare textiles. Regulatory and environmental drivers are promoting increased adoption of recycled and low‑impact synthetic materials, while divergent regional consumption patterns reflect stronger growth in Asia and expanding demand for high‑performance fabrics in developed economies. Emerging trends point toward greater automation and digital integration in production, and a future outlook centered on sustainability and advanced material functionality for technical applications.

The Synthetic Fabrics Market holds strategic relevance as a backbone for diversified industrial and consumer applications, where enhanced material performance directly influences cost structures and product competitiveness. High‑performance polyester blends have demonstrated a 28% improvement in tensile strength compared to older standard nylon fabrics, driving adoption in technical apparel and automotive textiles. Asia‑Pacific dominates in volume, while North America leads in adoption with over 65% of advanced material users integrating smart synthetic fabrics into performance and protective wear. By 2027, AI‑enabled quality inspection is expected to improve defect detection rates by up to 42%, reducing waste and enhancing throughput in large manufacturing hubs.

Strategic pathways leverage digital weaving and dyeing technologies that compress production cycles while maintaining high precision. Firms are committing to ESG metrics such as 50% recycled content integration by 2030 and 30% reduction in water use by 2028, aligning with regulatory and sustainability mandates. In a 2025 pilot, a major textile manufacturer in India achieved a 33% reduction in energy consumption through automated, sensor‑driven finishing lines, illustrating measurable operational gains.

Looking forward, the Synthetic Fabrics Market will underpin resilience in global supply chains, enable compliance with stricter environmental standards, and serve as a catalyst for sustainable growth through innovation and technology adoption across regions and end‑use sectors.

The rising demand for performance apparel is a major growth driver for the Synthetic Fabrics Market, as consumers and professional users increasingly seek materials with enhanced breathability, elasticity, and durability. Athletic and outdoor wear manufacturers are integrating high‑tenacity polyester and engineered spandex blends to offer moisture‑wicking, UV protection, and abrasion resistance. Industry data indicates that more than 70% of activewear producers have shifted toward advanced synthetic fabrics to meet evolving consumer expectations for functionality and comfort. This demand surge is further amplified by expansion in e‑commerce channels, which facilitates rapid product diversification and regional penetration. Corporate and institutional buyers also prefer synthetic fabrics for uniforms and protective clothing due to easier maintenance and longer service life. These trends translate into larger order volumes and ongoing investment in next‑generation textile technologies, strengthening the overall Synthetic Fabrics Market momentum.

Environmental regulations and waste management challenges are significant restraints for the Synthetic Fabrics Market, as governments and industry bodies implement stricter controls on emissions, effluents, and polymer waste. Synthetic polymers such as polyester and nylon contribute to microplastic pollution during washing and disposal, prompting regulators to enforce limitations on untreated effluents and require extended producer responsibility. Compliance with these mandates often requires capital‑intensive upgrades to wastewater treatment, recycling infrastructure, and chemical management systems, increasing operational complexity for manufacturers. Additionally, consumer advocacy for eco‑friendly alternatives exerts pressure on brands to reduce non‑recyclable content and transition to circular solutions, which can slow production cycles. These constraints, coupled with the cost and time needed to adapt supply chains and processes, act as formidable barriers affecting investment decisions and near‑term market expansion efforts.

The rising availability and acceptance of recycled and bio‑based polymers present significant opportunities for the Synthetic Fabrics Market, offering pathways to align with sustainability goals and differentiate product portfolios. Innovations in chemically recycled polyester and plant‑derived nylon alternatives are enabling manufacturers to reduce dependence on virgin petrochemicals while delivering performance comparable to traditional synthetics. Early commercial deployments show up to 40% reduction in carbon footprint for fabrics produced from certified recycled sources, attracting environmentally conscious brands and consumers. These developments are spawning new partnerships between resin producers, textile mills, and apparel brands to scale sustainable fiber streams. Moreover, labels emphasizing eco‑credentials have seen stronger engagement in retail channels, indicating potential for premium positioning. Geographic markets with strong green policy frameworks, such as Europe and North America, are accelerating adoption, creating opportunities for first‑mover advantages, strategic alliances, and diversified revenue streams within the broader Synthetic Fabrics ecosystem.

High volatility in raw material prices and energy costs poses a significant challenge to the Synthetic Fabrics Market, affecting profitability and pricing stability across the value chain. Feedstock polymers such as PET and nylon precursors are closely tied to global crude oil and natural gas markets, where fluctuations can rapidly shift production costs. For example, sudden spikes in polymer resin prices translate into higher input costs for textile converters and end‑product manufacturers, compressing margins and complicating long‑term contracts. Energy‑intensive processes such as extrusion, dyeing, and finishing also contribute to cost pressures, especially in regions with elevated power tariffs. These financial burdens can delay capacity expansions, limit investment in modernization, and prompt manufacturers to seek alternative materials or offshored production sites. Additionally, unpredictable input costs undermine budgeting accuracy and risk management, making it harder for businesses to plan strategic growth initiatives and maintain competitive pricing across global markets.

Growth in Smart and Functional Fabrics: The adoption of smart textiles with moisture-wicking, antimicrobial, and UV-protective properties has increased by 38% in the past two years. Over 60% of sportswear and activewear manufacturers have integrated performance-enhancing synthetic fabrics into their product lines, driving technological upgrades in production facilities globally.

Expansion of Recycled and Sustainable Materials: Use of recycled polyester and bio-based synthetic fibers has grown by 45% in 2024 compared to 2022, with more than 50% of European and North American textile producers committing to sustainable production initiatives. This shift reduces environmental impact while meeting regulatory and consumer demand for eco-friendly fabrics.

Automation and Digital Weaving Adoption: Automated looms and AI-assisted weaving technologies are being implemented in 42% of production units in Asia-Pacific, resulting in up to 30% improvement in production accuracy and a 25% reduction in material wastage. These technologies enable faster turnaround and precise quality control for high-volume orders.

Regional Customization and Rapid Deployment: Manufacturers in North America and Europe are increasingly adopting region-specific synthetic fabric solutions, with 55% of new product launches tailored for local climate and consumer preferences. This trend is complemented by digital sampling and rapid prototyping, reducing design-to-market timelines by approximately 20%, improving responsiveness to market shifts and consumer demand.

The Synthetic Fabrics Market is segmented across types, applications, and end-user industries, reflecting diverse use cases and technological requirements. By type, key fibers include polyester, nylon, acrylic, spandex, and related polymers, with each offering distinct performance attributes ranging from strength and elasticity to lightweight and moisture management. Across applications, synthetic fabrics serve apparel, home textiles, industrial textiles, and specialist uses such as protective clothing, illustrating adaptability to both consumer and technical demands. End-user segmentation spans fashion and clothing brands, automotive and transportation sectors, healthcare and medical textiles, sports and leisure equipment, and other industrial industries. Adoption patterns vary, with apparel and activewear driving volume usage due to durability and easy-care features, while automotive and industrial textiles prioritize high‑strength and functional properties. Regional consumption trends show Asia‑Pacific’s large manufacturing base influencing overall demand, while developed markets emphasize performance and sustainability metrics. This segmentation provides stakeholders clear visibility into targeted growth areas, material preferences, and sector‑specific requirements, enabling strategic planning and resource allocation across the value chain.

Polyester remains the leading type in the Synthetic Fabrics segment, accounting for roughly 55% share of global usage due to its versatility, resilience, and broad adoption across apparel, home textiles, and nonwoven applications. Polyester’s combination of wrinkle resistance, easy care, and adaptability to recycled feedstocks cements its leadership position. Nylon follows with approximately 25% market presence, valued for its superior strength and elasticity in technical, industrial, and performance‑oriented fabrics. The fastest‑growing type is polypropylene, expanding rapidly as demand rises for lightweight, moisture‑resistant, and chemically resilient textiles in medical nonwovens and filtration applications, driven by increased industrial and hygiene uses. Other types such as acrylic and spandex collectively contribute around 20% of the remaining segmentation, with spandex notable for stretchability in activewear and specialty garments.

Apparel is the dominant application for Synthetic Fabrics, representing approximately 60% share of total usage due to the broad demand for durable, easy‑care, and performance garments ranging from casual wear to activewear. Apparel’s reliance on synthetic materials stems from the need for wrinkle resistance, moisture wicking, and cost‑effective mass production in fast fashion and sportswear segments. The fastest‑growing application is protective and industrial textiles, driven by safety standards and functional requirements in sectors such as construction, automotive interiors, and filtration, where performance characteristics are paramount. Other applications include home textiles and specialty industrial uses, which together account for around 40% of overall application share, with home furnishings leveraging synthetic fabrics for durability and ease of maintenance.

Within end users, fashion and clothing manufacturers capture the largest segment with roughly 60% share, due to the extensive use of synthetic fabrics in mass market and performance apparel. This leadership reflects consumer preferences for easy‑care, lightweight, and affordable textiles. The fastest‑growing end-user segment is the automotive and transportation industry, where synthetic textiles are increasingly specified for seating, interior trims, and composite components, responding to lightweighting and durability goals tied to efficiency improvements. Other end users include healthcare providers and sports and leisure equipment manufacturers, which together constitute about 40% combined share, with rising adoption of high‑performance synthetic materials in surgical textiles, geotextiles, and technical sports gear.

Asia-Pacific accounted for the largest market share at 45% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

In 2024, Asia-Pacific’s synthetic fabrics consumption exceeded 8.2 million metric tons, driven by China’s 4.5 million metric tons and India’s 2.1 million metric tons. The region benefits from large-scale textile manufacturing hubs, high adoption in apparel and automotive sectors, and significant investment in automated spinning and weaving facilities. Europe follows with 20% share, led by Germany and France, while North America holds approximately 18% of global demand. Rising consumer preference for performance fabrics and sustainable materials is reshaping production requirements, with digital weaving adoption increasing by 42% across the top manufacturing hubs. Regional infrastructure improvements, such as high-capacity logistics networks and smart manufacturing plants, are facilitating efficient distribution and product diversification across local and export markets.

How is demand from industrial and consumer sectors shaping synthetic fabrics usage?

North America accounts for roughly 18% of the global Synthetic Fabrics Market, with demand largely driven by the automotive, healthcare, and performance apparel industries. Regulatory support, including environmental compliance incentives, is encouraging adoption of recycled and bio-based synthetic materials. Technological transformation through automated weaving, digital inspection, and AI-assisted production has improved fabric precision by 25% while reducing material waste. A key player, DuPont, is implementing advanced polymer blends for automotive interiors, improving durability and lightweighting by over 15%. Consumer behavior varies, with higher enterprise adoption in healthcare and finance sectors, emphasizing antimicrobial and high-performance textile solutions for uniforms, protective gear, and facility applications.

What role do sustainability regulations and technology adoption play in synthetic fabrics growth?

Europe holds approximately 20% of the global Synthetic Fabrics Market, with Germany, UK, and France leading production and consumption. Strong regulatory frameworks focused on sustainability have accelerated adoption of recycled and eco-friendly fabrics, with 60% of manufacturers incorporating green practices. Emerging technologies such as automated finishing and AI-driven quality control have enhanced production efficiency and reduced fabric defects by 18%. A local player, Lenzing AG, is producing sustainable synthetic blends for apparel and home textiles, boosting market penetration. Consumer behavior emphasizes compliance and environmentally responsible products, leading to higher preference for explainable and traceable synthetic fabrics across both commercial and retail channels.

How is infrastructure and digital innovation driving synthetic fabrics adoption?

Asia-Pacific represents the largest market volume at 45%, with top consuming countries including China, India, and Japan. Advanced textile infrastructure, including automated weaving and integrated finishing units, supports high output, with China alone producing over 4.5 million metric tons annually. Technological innovation hubs in India and Japan focus on smart fabrics and functional polymer blends, enhancing activewear and industrial textile applications. Local players like Toray Industries are expanding production of high-performance polyester and nylon fabrics to meet growing demand. Consumer behavior is strongly influenced by e-commerce and mobile purchasing, with over 60% of apparel purchases in urban centers utilizing online platforms, driving faster market turnover.

What factors are driving synthetic fabrics demand across key South American countries?

South America holds around 8% of the global Synthetic Fabrics Market, with Brazil and Argentina as leading markets. Demand is fueled by growing automotive and construction sectors, where synthetic materials are preferred for durability and cost efficiency. Government incentives, including import duty reductions on machinery and raw materials, support manufacturing growth. Local player Santista Textil is expanding synthetic polyester production to supply both domestic and export markets. Consumer behavior is influenced by media-driven trends and language-specific branding, resulting in high preference for regionally tailored apparel and home textiles, particularly in urban areas.

How are industrial applications and modernization influencing synthetic fabrics adoption?

The Middle East & Africa region contributes approximately 9% of global Synthetic Fabrics demand, led by the UAE and South Africa. Growth is primarily driven by oil & gas, construction, and infrastructure projects requiring durable industrial textiles. Technological modernization, including automated weaving and digital quality monitoring, is being adopted to improve efficiency and reduce production defects by 20%. Government initiatives supporting industrial investment and trade partnerships are increasing local manufacturing capacity. A regional player, Alok Industries, is introducing lightweight polyester fabrics for industrial and automotive applications. Consumer trends show growing preference for functional apparel and protective clothing in both commercial and retail sectors.

China: 28% market share; high production capacity and extensive manufacturing infrastructure drive global leadership in synthetic fabrics.

India: 12% market share; strong end-user demand and expanding textile manufacturing hubs position India as a key contributor to regional and global markets.

The competitive environment in the Synthetic Fabrics market is marked by a blend of large multinational producers and numerous specialized regional manufacturers, resulting in a moderately consolidated yet fragmented market for commodity synthetic fabrics and an oligopolistic structure for technical and high‑performance segments. There are over 150 active competitors globally, but production capacity and innovation leadership are concentrated among the top tier. The combined share of the top 5 companies in the global supply chain—spanning polyester, nylon, and advanced synthetic blends—accounts for an estimated 55% to 60% of overall market capacity, underscoring a significant role for major leaders in setting industry dynamics.

Key strategic initiatives shaping competition include technology partnerships, expanded production facilities, and strategic product launches in sustainable and performance fabrics. For example, global producers are increasing capacity for recycled polyester and bio‑based fibers, integrating digital quality control systems that improve defect detection by more than 30% in regional mills. Mergers and acquisitions are also influencing competitive positioning, with larger players acquiring specialty fiber firms to broaden portfolios and enter niche applications such as automotive composites and protective textiles.

Innovation trends, such as smart synthetic blends and moisture‑responsive textiles, are creating new differentiation avenues; roughly 40% of recent product introductions integrate enhanced functional properties. Market positioning strategies increasingly emphasize ESG performance, with several manufacturers committing to high recycled content and lower energy intensities in production. Overall, competition is driven by a balance of scale, innovation leadership, and responsiveness to evolving consumer expectations for sustainability and performance attributes.

Sinopec Group

Teijin Limited

Lenzing AG

Mitsubishi Chemical Holdings Corporation

Toyobo Co., Ltd.

E. I. du Pont de Nemours and Company

Hyosung Corporation

BASF SE

Bombay Dyeing

Eclat Textile Co. Ltd.

Nilit Ltd.

The Synthetic Fabrics Market is undergoing significant transformation driven by both current and emerging technologies that enhance efficiency, quality, and functional performance. Advanced polymerization methods now enable the production of high-tenacity polyester and nylon fibers with tensile strength improvements of up to 28% compared to traditional methods, supporting applications in technical textiles, automotive interiors, and performance apparel. Digital weaving technologies and automated looms are increasingly adopted, with approximately 42% of large-scale mills globally implementing AI-assisted weaving systems, resulting in 25% reduction in material waste and a 20% improvement in production precision.

Emerging technologies such as smart fabrics, moisture-wicking composites, and antimicrobial polymer coatings are expanding functional applications in healthcare, sports, and industrial sectors. For example, over 60% of activewear manufacturers have incorporated synthetic fabrics with integrated UV protection, moisture management, and odor control features, reflecting a shift toward multifunctional textiles. Additive manufacturing, including 3D knitting and printing of synthetic fibers, is being piloted in Europe and North America, enabling rapid prototyping and customization for small-batch, high-performance applications.

Sustainability-focused innovations are also reshaping the market, with recycled polyester and bio-based polymers accounting for roughly 45% of new production lines in leading textile hubs. Digital quality control and sensor-based monitoring allow real-time detection of defects and improved process efficiency. Companies are increasingly integrating IoT-enabled machines to optimize energy consumption, with pilot programs showing up to 22% reduction in electricity use during finishing operations. These technology advancements collectively reinforce the market’s competitiveness, operational resilience, and capacity to meet evolving consumer and regulatory demands.

• In March 2024, Toray Industries launched its ULTRASUEDE® Bio series, incorporating plant‑based synthetic fibers blended with organic cotton for luxury automotive interiors and premium fashion applications, achieving a 40% reduced carbon footprint compared to conventional alternatives.

• In January 2024, Reliance Industries announced a strategic partnership with H&M Group to develop closed‑loop recycling systems for polyester‑cotton blends, establishing a dedicated line capable of processing 50,000 tons annually of post‑consumer textile waste into new blended fibers.

• In July 2024, Indorama Ventures completed the acquisition of a recycled polyester production facility in France for €180 million, enhancing sustainable blended fiber output for the European automotive and fashion industries.

• In 2024, PUMA scaled up its RE:FIBRE textile‑to‑textile recycling technology, producing official replica football jerseys using materials made from old garments and factory waste instead of recycled plastic bottles for major competitions including Euro and Copa América. (temp.matexil.org)

The scope of the Synthetic Fabrics Market Report encompasses a comprehensive analysis of material types, application domains, geographic regions, technological drivers, and industrial use cases shaping the global landscape. On the product spectrum, the report examines key synthetic fibers such as polyester, nylon, polypropylene, acrylic, and specialty blends, highlighting performance characteristics relevant to durability, elasticity, moisture management, and functional enhancements. It also covers emerging materials including recycled and bio‑based polymers that are transforming sustainability practices within textile supply chains.

Application segmentation includes mainstream apparel, technical and protective wear, automotive interiors, home textiles, industrial and nonwoven fabrics, and specialist sectors such as healthcare and filtration media. Geographic coverage spans major markets across Asia‑Pacific, North America, Europe, South America, and Middle East & Africa, offering insights into consumption volumes, manufacturing capacities, regulatory environments, and regional demand variations influenced by consumer behavior and industry trends.

Technological insights within the report address digital weaving, AI‑assisted quality control, automated production systems, and breakthroughs in smart and multifunctional fabrics. It also assesses innovation adoption in sustainable recycling methods and circular economy frameworks. By combining segmentation depth with regional analysis and technology mapping, the scope equips decision‑makers with a strategic understanding of current market structures, competitive landscapes, and future growth vectors across the synthetic fabrics ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 18464.24 Million |

|

Market Revenue in 2032 |

USD 25660.97 Million |

|

CAGR (2025 - 2032) |

4.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Reliance Industries Limited, Toray Industries, Inc., Indorama Ventures Public Company Limited, Sinopec Group, Teijin Limited, Lenzing AG, Mitsubishi Chemical Holdings Corporation, Toyobo Co., Ltd., E. I. du Pont de Nemours and Company, Hyosung Corporation, BASF SE, Bombay Dyeing, Eclat Textile Co. Ltd., Nilit Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |