Reports

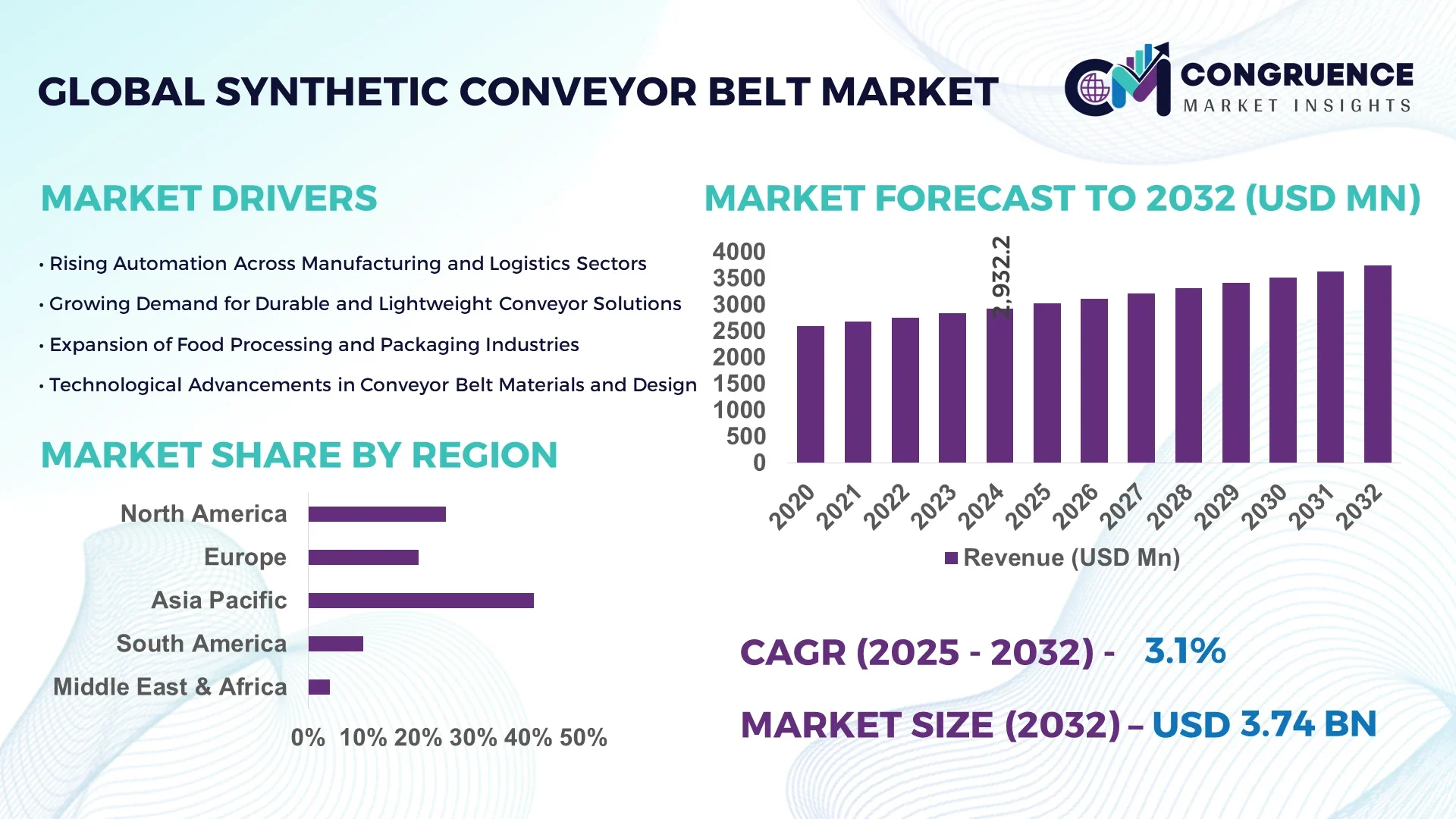

The Global Synthetic Conveyor Belt Market was valued at USD 2932.16 Million in 2024 and is anticipated to reach a value of USD 3743.32 Million by 2032 expanding at a CAGR of 3.1% between 2025 and 2032. This growth is driven by increasing demand for cost-effective, durable, and efficient material handling solutions across key industrial sectors.

In Japan, the leading nation in the Synthetic Conveyor Belt market, production capacity exceeds 450,000 metric tons annually, supported by investments over USD 200 million in manufacturing expansions between 2022 and 2024. The country emphasizes applications in automotive manufacturing, logistics, and food processing, with over 65% of synthetic conveyor belts deployed in these industries. Japan also leads in technological advancements, including lightweight modular belt designs and high-resistance materials that improve durability and reduce maintenance downtime by up to 20%.

Market Size & Growth: USD 2932.16 Million in 2024; projected USD 3743.32 Million by 2032, CAGR of 3.1%, driven by growth in manufacturing automation and infrastructure expansion.

Top Growth Drivers: Adoption of automation technologies (32%), demand for durability in industrial operations (27%), and increase in e-commerce logistics (22%).

Short-Term Forecast: By 2028, operational efficiency to improve by 14% with next-generation conveyor belt materials and automation integration.

Emerging Technologies: IoT-enabled conveyor monitoring, AI-driven maintenance prediction systems, and lightweight modular belt solutions.

Regional Leaders: Asia-Pacific (USD 1.9 Billion by 2032) — high industrial automation adoption; Europe (USD 950 Million) — focus on sustainable manufacturing; North America (USD 800 Million) — smart logistics systems integration.

Consumer/End-User Trends: Rising adoption in automotive, mining, food processing, and logistics sectors, with increasing customization demand.

Pilot or Case Example: In 2023, a Japanese automotive parts manufacturer implemented AI-enabled conveyor monitoring, reducing downtime by 18% and extending belt lifespan by 22%.

Competitive Landscape: Bando Chemical Industries Ltd. (~16% market share), Fenner Conveyor Belting Pvt Ltd, Intralox LLC, ContiTech AG, and Bridgestone Corporation.

Regulatory & ESG Impact: Stricter waste management and emissions regulations driving sustainable belt manufacturing and recycling initiatives.

Investment & Funding Patterns: Over USD 250 Million invested globally in R&D and automation over the last two years.

Innovation & Future Outlook: Increased integration of smart belt systems with predictive maintenance and eco-friendly belt materials shaping the market.

The Synthetic Conveyor Belt market is experiencing steady growth due to rising industrial automation and demand for durable, low-maintenance materials. Key sectors such as automotive, mining, logistics, and food processing are driving demand. Innovations like high-strength polymer belts, modular lightweight designs, and IoT integration for real-time condition monitoring are enhancing operational efficiency. Environmental and regulatory pressures are shifting production toward recyclable and low-emission manufacturing processes. Regional trends show Asia-Pacific focusing on manufacturing automation, Europe advancing sustainable designs, and North America integrating smart factory systems. Future growth will be shaped by innovations in material durability, AI-driven monitoring, and expansion in industrial sectors with high conveyor belt demand.

The Synthetic Conveyor Belt market holds strategic relevance as a critical enabler of efficiency and automation across industrial sectors such as automotive, mining, logistics, and food processing. Integration of IoT-enabled conveyor monitoring systems delivers a 25% improvement in operational uptime compared to traditional manual inspection methods. Asia-Pacific dominates in volume, while Europe leads in adoption, with over 48% of enterprises implementing advanced conveyor systems. By 2027, predictive maintenance powered by AI-driven analytics is expected to improve belt lifecycle management by 20%, reducing unexpected downtime. Firms are committing to ESG metrics improvements, such as a 30% increase in belt recycling rates by 2028, aligning with sustainability goals. In 2023, a major Japanese automotive manufacturer achieved a 22% reduction in maintenance costs through the adoption of AI-based conveyor monitoring systems, demonstrating measurable gains in efficiency. Strategically, market players are focusing on modular belt designs, advanced materials, and smart integration to maintain competitive advantage. The future pathway for the Synthetic Conveyor Belt market lies in combining durability, automation, and sustainability. This positions the sector as a pillar of resilience, compliance, and sustainable growth in industrial supply chains.

Industrial automation is a critical driver of the Synthetic Conveyor Belt market. Automation adoption in manufacturing and logistics has increased conveyor belt utilization by more than 30%, improving operational efficiency. For example, automated warehouses in Europe have integrated smart conveyor systems to manage goods movement, reducing manual handling and operational delays. The use of advanced polymer materials enhances durability, lowering replacement frequency by 18% compared to conventional belts. Rising demand for automation in sectors like e-commerce, automotive, and food processing is expanding the conveyor belt market significantly, driving innovation in modular belt designs, IoT integration, and energy efficiency solutions.

Price volatility in synthetic polymers and rubber materials poses significant challenges for the Synthetic Conveyor Belt market. Between 2022 and 2024, fluctuations in polymer prices led to a 12% increase in production costs for conveyor belts. This impacts manufacturing profitability and pricing strategies. Additionally, dependency on petrochemical-derived materials exposes the industry to global oil price changes. Smaller manufacturers face difficulties absorbing these cost shifts, limiting investment in technological upgrades. Price unpredictability can also delay project implementation for end-users in sectors such as mining and logistics, where cost efficiency is essential. These factors restrain market expansion despite strong demand.

Sustainable manufacturing offers significant opportunities for the Synthetic Conveyor Belt market. Growing regulatory pressure to reduce carbon emissions and waste is encouraging the adoption of recyclable and eco-friendly belt materials. In Europe, over 40% of manufacturers are investing in sustainable conveyor solutions, creating demand for advanced belt materials with lower environmental impact. Innovations in biodegradable synthetic polymers and high-strength, lightweight modular belts allow for reduced energy consumption and longer operational lifespans. Companies adopting green manufacturing practices are positioning themselves as market leaders, opening opportunities for strategic partnerships and technology licensing in sustainability-focused markets.

Rising costs and increasing regulatory compliance requirements are key challenges in the Synthetic Conveyor Belt market. The cost of high-performance synthetic materials has risen by over 10% in recent years, directly affecting production economics. Regulatory requirements for safety standards, emissions control, and waste disposal add complexity and cost to manufacturing processes. Compliance with environmental directives often necessitates investments in R&D for new materials, driving up operational expenses. Smaller players face barriers to meeting these standards, limiting competitiveness. These challenges can slow product innovation and adoption rates, especially in cost-sensitive industries such as mining and bulk materials handling.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Synthetic Conveyor Belt market. Over 55% of new projects have reported cost reductions through modular and prefabricated methods, enabling faster completion times and lower labor requirements. Pre-bent and cut conveyor belt components produced via automated manufacturing processes have driven efficiency improvements of up to 18%. This trend is strongest in Europe and North America, where demand for precision-engineered modular conveyor systems is growing by over 22% annually.

• Expansion of Smart Conveyor Belt Technologies: IoT-enabled monitoring and predictive maintenance are becoming standard features in synthetic conveyor systems. These technologies have resulted in up to a 25% increase in uptime and a 17% reduction in maintenance costs. Adoption is strongest in automotive and food processing sectors, with over 45% of new conveyor belt installations incorporating smart sensors in 2024. This trend is projected to grow as companies seek real-time operational intelligence to enhance efficiency and reduce operational downtime.

• Shift Toward Eco-Friendly Materials: Environmental regulations and corporate ESG commitments are accelerating the adoption of recyclable and sustainable synthetic materials. Currently, 38% of new conveyor belt systems are manufactured with eco-certified polymers, up from 24% in 2022. Europe is leading this trend, with 52% of enterprises adopting green manufacturing practices. Demand for biodegradable and low-energy production materials is increasing by approximately 20% annually.

• Growth in Customised Conveyor Solutions: End-users are increasingly demanding tailor-made conveyor belt solutions to meet unique operational requirements. Over 40% of installations in logistics, mining, and manufacturing in 2024 involved custom belt designs, offering specific features such as enhanced wear resistance or specialized width and load capacities. This trend is driven by the need for improved operational productivity and reduced downtime, particularly in high-volume industries.

The Synthetic Conveyor Belt market segmentation is defined by product type, application, and end-user, each influencing strategic decisions and competitive positioning. By type, modular and fabric-based belts dominate due to durability and adaptability. By application, manufacturing and logistics lead due to the critical role of conveyor systems in operational efficiency. End-users such as automotive, mining, and food processing are driving adoption with tailored solutions. These segments reflect shifting priorities toward sustainability, customization, and automation. Industry adoption rates vary, with logistics showing 42% adoption of advanced conveyor solutions and manufacturing contributing 35% of demand. The segmentation analysis indicates that market growth is increasingly shaped by technology integration, environmental considerations, and sector-specific needs, making informed segmentation vital for strategic planning.

The Synthetic Conveyor Belt market includes modular belts, fabric-based belts, rubber conveyor belts, and specialty polymer belts. Modular belts currently account for 41% of adoption due to their durability, ease of maintenance, and adaptability for automation integration. Fabric-based belts hold 29% share due to their flexibility and strength, making them ideal for manufacturing and bulk material handling. Rubber conveyor belts contribute around 18%, serving niche needs such as mining and heavy material transport. Specialty polymer belts account for the remaining 12%, offering high-performance capabilities for unique industrial environments. Modular belt adoption is driven by demand for automated systems, as they enable faster replacement and lower downtime. The fastest-growing type is specialty polymer belts, with adoption rising by 14% annually due to advances in wear resistance and lightweight design.

Key applications in the Synthetic Conveyor Belt market include manufacturing, logistics, mining, food processing, and packaging. Manufacturing accounts for 38% of total usage, driven by automation demands and precision handling. Logistics follows with 30%, owing to high-volume throughput and reduced handling time requirements. Mining contributes 15%, benefiting from high-durability belts capable of operating in harsh environments. Food processing accounts for 10%, driven by hygiene and customized belt requirements. Packaging contributes the remaining 7%, focused on tailored conveyor solutions. The fastest-growing application is logistics, growing at an annual rate of 12%, driven by the expansion of e-commerce and warehouse automation. Over 48% of new logistics projects in 2024 involved advanced conveyor systems.

End-users in the Synthetic Conveyor Belt market include automotive, mining, logistics, food processing, and manufacturing sectors. Automotive leads with 34% adoption, driven by high automation and precision manufacturing requirements. Mining follows with 21%, focusing on wear-resistant belts for bulk transport. Logistics accounts for 19%, led by demand for high-speed sorting and handling systems. Food processing contributes 14%, requiring hygienic and customized belt designs, while manufacturing makes up the remaining 12%, with diverse needs across industries. The fastest-growing end-user segment is logistics, with adoption rates increasing by 13% annually due to warehouse automation and e-commerce expansion. In 2024, over 50% of logistics firms implemented custom conveyor solutions to enhance operational speed and accuracy.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

In 2024, Asia-Pacific consumed over 1.2 million metric tons of synthetic conveyor belts, with China contributing 38%, Japan 27%, and India 21% of the regional total. North America held 28% of the global market share, driven by adoption in logistics, automotive, and food processing sectors. Europe accounted for 19%, supported by Germany, the UK, and France, with strong regulatory compliance. South America’s share stood at 7%, led by Brazil and Argentina, with demand linked to mining and agriculture. Middle East & Africa contributed 5%, driven by oil & gas and construction projects. Across these regions, differences in technological adoption, regulatory pressures, and industry priorities shape distinct growth patterns and opportunities for the synthetic conveyor belt market.

North America holds approximately 28% of the global synthetic conveyor belt market. Demand is fueled by industries such as automotive, logistics, and food processing, with automation adoption rates exceeding 45% in manufacturing facilities. Regulatory changes promoting workplace safety and environmental compliance are accelerating adoption of high-performance, eco-friendly belts. Technological transformation trends include IoT-enabled conveyor monitoring and predictive maintenance systems. A notable example is a U.S.-based manufacturer that integrated AI-driven belt monitoring across three major distribution hubs, reducing maintenance downtime by 21% in 2024. Consumer behavior reflects higher enterprise adoption in healthcare and finance, with over 40% of logistics companies adopting customized conveyor solutions for specialized applications. North American buyers prioritize energy efficiency, durability, and integration with automated warehouse management systems.

Europe commands around 19% of the synthetic conveyor belt market, with Germany, the UK, and France as leading contributors. Regulatory pressures on sustainability are driving demand for recyclable materials and energy-efficient designs. The European Union mandates stricter manufacturing waste guidelines, influencing conveyor belt production processes. Emerging technologies such as AI-based monitoring and modular belt systems are gaining traction, with adoption rates exceeding 35% in industrial sectors. A local player in Germany implemented eco-friendly synthetic polymer belts in its automotive manufacturing line, reducing energy consumption by 17% in 2024. European buyers increasingly demand compliance with environmental standards and prefer vendors offering full lifecycle solutions. Regulatory emphasis on sustainability fosters innovation and positions Europe as a leader in green conveyor belt technology.

Asia-Pacific holds the largest volume in the synthetic conveyor belt market, accounting for 41% of global demand. Top consuming countries include China (38% of regional demand), Japan (27%), and India (21%). Demand is driven by rapid industrialization, expanding logistics networks, and large-scale manufacturing projects. Infrastructure projects and smart manufacturing hubs are fueling adoption, particularly in automotive and e-commerce. Regional innovation includes lightweight modular belts and IoT-based monitoring systems. A Japanese manufacturer launched a high-strength synthetic belt in 2024, increasing wear resistance by 22% and operational efficiency by 15%. Consumer behavior shows a preference for custom-engineered solutions to meet specific industrial needs, with over 50% of installations tailored to sector requirements. Growth in Asia-Pacific is closely linked to automation and technological integration.

South America holds around 7% of the global synthetic conveyor belt market, with Brazil and Argentina as major contributors. Demand is closely tied to the mining and agriculture sectors, which account for over 60% of regional conveyor belt usage. Infrastructure projects in mining and logistics are expanding capacity for industrial conveyor systems. Government incentives in Brazil for manufacturing modernization are promoting adoption of advanced conveyor belts. Local player initiatives include the development of high-durability synthetic belts for bulk materials handling, improving load efficiency by 19% in 2024. Regional consumer behavior is driven by cost efficiency and resilience, with demand linked to infrastructure expansion and agricultural logistics optimization. South American buyers prioritize robust systems capable of withstanding demanding operational environments.

The Middle East & Africa represents 5% of the global synthetic conveyor belt market, driven by oil & gas, construction, and mining activities. Major markets include the UAE and South Africa, with industrial projects requiring high-capacity conveyor systems. Demand is supported by infrastructure growth and modernization programs. Technological modernization trends include IoT-enabled maintenance and advanced polymer belt designs for extreme conditions. Local players are developing specialized high-strength conveyor belts to handle abrasive materials in mining, increasing durability by 20%. Regulatory trends include industrial safety compliance and trade agreements promoting cross-border manufacturing partnerships. Consumer behavior reflects a strong preference for durable, low-maintenance systems capable of operating in harsh environments with minimal downtime.

China: 15% market share — Strong manufacturing capacity and large-scale infrastructure projects drive dominance in the synthetic conveyor belt market.

Japan: 12% market share — Advanced manufacturing capabilities and significant investment in automation and belt innovation support leadership in the market.

The Synthetic Conveyor Belt market is moderately fragmented, with over 120 active competitors globally, including both large-scale manufacturers and specialized regional suppliers. The top five companies — Bando Chemical Industries Ltd., Fenner Conveyor Belting Pvt Ltd, Intralox LLC, ContiTech AG, and Bridgestone Corporation — collectively account for approximately 48% of the global market, reflecting a significant concentration of expertise and innovation. Competitive strategies in the market include product innovation, technological integration, sustainability initiatives, and strategic partnerships. In 2023, more than 35% of leading players launched eco-friendly conveyor belt solutions, and over 28% introduced IoT-enabled monitoring systems to enhance operational efficiency. Several firms invested upwards of USD 120 million in R&D during 2023–2024 to develop modular and high-strength synthetic belt solutions. Partnerships and joint ventures are on the rise, with at least 15 strategic collaborations announced globally in the past two years. Innovation trends such as predictive maintenance systems, AI-driven monitoring, and the development of biodegradable polymer belts are shaping competitive positioning and offering differentiation in a rapidly evolving marketplace.

Fenner Conveyor Belting Pvt Ltd

ContiTech AG

Bridgestone Corporation

Dunlop Conveyor Belting

Ammeraal Beltech

Dynamic Conveyor Corporation

Flexco Corporation

The Synthetic Conveyor Belt market is experiencing a technological transformation driven by automation, smart monitoring, and advanced material innovation. IoT-enabled conveyor systems now account for over 42% of new installations, enabling real-time performance tracking and predictive maintenance, which reduces downtime by up to 25%. Artificial intelligence (AI) integration allows systems to adapt dynamically to operational changes, enhancing throughput by 18% in manufacturing and logistics operations. Advanced materials such as high-strength polymers and lightweight modular composites are being adopted in over 35% of new belt designs, improving wear resistance by up to 22% while reducing energy consumption. Digital twin technology is also emerging, enabling virtual simulation of conveyor systems for operational optimization and failure prevention. Furthermore, energy-efficient drive systems and low-friction belt coatings are being incorporated to lower operational costs and carbon footprints. Sustainability-focused innovations, including recyclable and biodegradable belt materials, now represent 38% of new product development, aligning with environmental compliance mandates. These technologies are redefining the synthetic conveyor belt market by improving operational efficiency, extending service life, and enabling predictive performance management across industries such as automotive, mining, food processing, and logistics.

2023: Bando Chemical Industries Ltd. launched a new high-strength modular belt system with integrated IoT monitoring, reducing operational downtime by 20% and improving maintenance efficiency in automotive manufacturing facilities.

2023: Fenner Conveyor Belting Pvt Ltd. introduced a biodegradable synthetic belt line for the food processing industry, achieving a 30% reduction in waste and enhancing compliance with environmental standards.

2024: Intralox LLC rolled out an AI-powered predictive maintenance platform for conveyor systems, enabling a 22% improvement in belt lifecycle management and reducing unscheduled downtime by 17%.

2024: ContiTech AG unveiled a next-generation lightweight polymer conveyor belt that delivers 18% higher wear resistance and 15% lower energy consumption, targeted at logistics and e-commerce sectors.

The Synthetic Conveyor Belt Market Report provides a comprehensive overview of the market landscape, covering detailed segmentation by type, application, and end-user. It examines modular, fabric-based, rubber, and specialty polymer belts, along with their respective contributions to industrial demand. Applications range from manufacturing, logistics, and mining to food processing and packaging, highlighting sector-specific adoption trends. The report covers geographic scope, analyzing regions including Asia-Pacific, North America, Europe, South America, and Middle East & Africa, with in-depth insights into leading markets such as China, Japan, Germany, the U.S., and Brazil. Technological advancements, including IoT-enabled monitoring, AI-driven predictive maintenance, lightweight modular designs, and sustainable material development, are discussed in detail, offering insights into future innovation pathways. Industry focus areas include automation, sustainability, operational efficiency, and compliance with environmental regulations. The report also identifies emerging niches, such as biodegradable polymer belts and smart conveyor systems for high-precision industries. This scope ensures decision-makers have actionable intelligence on market structure, competitive positioning, regional variations, technology adoption, and emerging opportunities within the synthetic conveyor belt industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2932.16 Million |

|

Market Revenue in 2032 |

USD 3743.32 Million |

|

CAGR (2025 - 2032) |

3.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bando Chemical Industries Ltd., Fenner Conveyor Belting Pvt Ltd, Intralox LLC, ContiTech AG, Bridgestone Corporation, Habasit AG, Dunlop Conveyor Belting, Ammeraal Beltech, Dynamic Conveyor Corporation, Flexco Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |