Reports

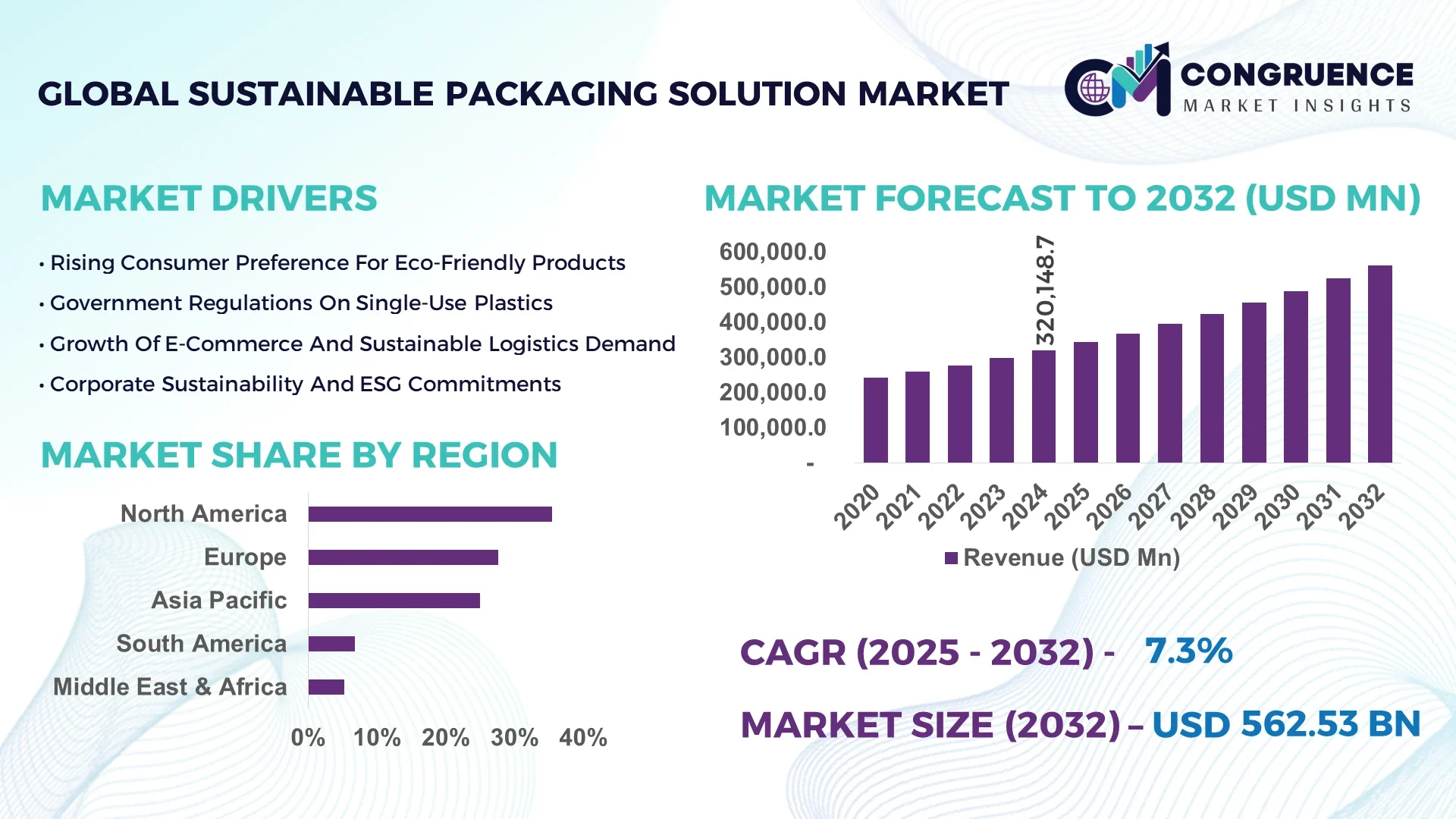

The Global Sustainable Packaging Solution Market was valued at USD 320,148.7 Million in 2024 and is anticipated to reach a value of USD 562,535.0 Million by 2032 expanding at a CAGR of 7.3% between 2025 and 2032. The rising demand for eco-friendly materials and strong regulatory mandates are accelerating adoption across industries.

The United States plays a dominant role in the global sustainable packaging landscape, with packaging manufacturers producing over 40 million metric tons of recyclable materials annually. In 2024, investment in bio-based polymers exceeded USD 2.8 billion, particularly for food and beverage and e-commerce applications. Technological advancements in biodegradable films and high-barrier compostable coatings have scaled production efficiency by nearly 25%. Consumer adoption is also robust, with 64% of U.S. households consistently choosing recyclable or compostable packaging products.

Market Size & Growth: USD 320.1 billion in 2024, projected to reach USD 562.5 billion by 2032, expanding at 7.3% CAGR, driven by strict environmental compliance.

Top Growth Drivers: 68% adoption in e-commerce, 54% efficiency improvements in supply chains, 47% consumer preference shift toward recyclable materials.

Short-Term Forecast: By 2028, operational costs for manufacturers expected to drop by 19% through use of lightweight packaging.

Emerging Technologies: Compostable biopolymers, plant-based nanocoatings, and smart labeling integration.

Regional Leaders: North America forecasted at USD 162.3 billion by 2032 (led by food & beverage), Europe at USD 144.6 billion (regulatory-driven adoption), Asia-Pacific at USD 170.2 billion (manufacturing scale advantages).

Consumer/End-User Trends: Over 72% of millennials prioritize brands with eco-friendly packaging; FMCG and retail sectors lead adoption.

Pilot or Case Example: In 2024, a pilot in Germany achieved 28% reduction in plastic waste via large-scale compostable food packaging rollout.

Competitive Landscape: A leading multinational holds ~12% market share; key competitors include Amcor, DS Smith, Mondi, Smurfit Kappa, and WestRock.

Regulatory & ESG Impact: New single-use bans and carbon neutrality mandates push firms to achieve 40% recycling targets by 2030.

Investment & Funding Patterns: More than USD 6.5 billion invested in 2023–2024 in biopolymer plants and recycling innovations.

Innovation & Future Outlook: Blockchain-enabled traceability and AI-driven material optimization are shaping next-generation sustainable packaging systems.

The sustainable packaging solution market is being shaped by fast-growing adoption in e-commerce, FMCG, and healthcare, where recyclable and biodegradable materials account for nearly 60% of packaging volumes. Innovations such as compostable coatings, lightweight corrugated boxes, and plant-based polymers are transforming consumer choices, while EU green directives and North American recycling targets continue to fuel growth across industries.

Sustainable packaging solutions are no longer a branding choice but a strategic requirement across global industries. By integrating recyclable polymers, biodegradable films, and smart traceability systems, companies are achieving measurable efficiency and compliance. For instance, compostable bioplastics deliver up to 32% carbon footprint reduction compared to conventional petroleum-based plastics, directly addressing climate commitments. Regionally, Asia-Pacific dominates in production volume due to its high manufacturing scale, while Europe leads in adoption with 78% of enterprises integrating sustainable packaging across FMCG and retail. By 2027, AI-enabled material optimization is expected to cut packaging waste in logistics by 21%, creating new efficiency benchmarks.

Compliance frameworks reinforce market direction: firms in North America and Europe are committing to 40% plastic recycling improvements by 2030 under ESG mandates. A micro-scenario demonstrates progress— in 2024, a Scandinavian beverage company achieved a 25% reduction in raw plastic usage by adopting 100% recycled PET bottles. The strategic pathway of this market lies in integrating automation, bio-material innovation, and regulatory compliance, positioning the Sustainable Packaging Solution Market as a foundation for resilient supply chains, ESG compliance, and sustainable growth worldwide.

The sustainable packaging solution market is evolving under the dual influence of environmental regulations and consumer expectations for eco-friendly products. Advances in biodegradable plastics, lightweight corrugated packaging, and smart traceability tools are reshaping supply chains. Government restrictions on single-use plastics in more than 90 countries are compelling industries to adopt alternatives. Consumer demand is equally pivotal, with 62% of global shoppers preferring recyclable packaging in 2024. Additionally, automation and nanotechnology are improving cost-effectiveness and scalability.

E-commerce is a key growth driver, as over 68% of global online retailers adopted recyclable or biodegradable packaging in 2024. With parcel volumes surpassing 150 billion shipments globally, lightweight corrugated boxes and compostable mailers are being deployed at scale. The transition reduces shipping costs by up to 14% while improving consumer perception. FMCG companies and logistics providers are increasingly investing in high-barrier paper packaging to ensure durability while maintaining sustainability standards, creating long-term growth opportunities.

Despite advancements, sustainable packaging often incurs costs 20–30% higher than traditional alternatives due to expensive bio-resins and limited recycling infrastructure. SMEs face challenges adopting advanced compostable films or multilayer biodegradable packaging because of cost inefficiencies in scaling. Additionally, certain biodegradable plastics lack durability for heavy-duty applications, restricting their use in industrial and pharmaceutical packaging. This limits universal adoption, particularly in emerging economies where affordability remains critical.

Emerging biopolymer technologies such as PHA (polyhydroxyalkanoates) and PLA (polylactic acid) are unlocking new opportunities in food & beverage and healthcare packaging. These materials provide barrier protection equivalent to petroleum plastics while being compostable. By 2028, bio-based plastics are projected to represent 22% of global sustainable packaging volume. Coupled with nanocoatings and AI-driven design optimization, these innovations present a strong opportunity for industries aiming to balance sustainability with functionality.

Recycling rates remain uneven globally, with Europe achieving 48% packaging recycling while Asia and Africa remain below 20%. This inconsistency challenges uniform adoption of sustainable packaging. Developing economies lack material recovery facilities, causing compostable or recyclable packaging to end up in landfills. Additionally, fragmented regulations across regions complicate supply chain consistency for multinational corporations. These challenges underline the urgent need for harmonized recycling frameworks and global infrastructure investment.

• Expansion of Biodegradable Plastics Adoption: In 2024, global biodegradable plastic production exceeded 2.1 million tons, marking a 19% rise year-on-year. Food and beverage applications accounted for nearly 45% of consumption, with Europe leading adoption. This trend reflects a shift toward plant-based polymers and compostable materials that reduce carbon footprints.

• Growth in Lightweight Corrugated Packaging: More than 32% of global FMCG packaging in 2024 transitioned to lightweight corrugated boxes, reducing logistics costs by 17%. The ability to maintain durability while lowering material usage is accelerating adoption in both e-commerce and retail supply chains.

• Integration of Smart Packaging Technologies: Smart labels and QR-code tracking systems expanded to 26% of all sustainable packaging deployments in 2024. These innovations enhance consumer transparency, support recycling, and reduce counterfeit risks in pharmaceuticals and luxury goods.

• Rise in Circular Economy Partnerships: By 2024, over 180 large corporations joined recycling and reuse consortiums, resulting in 29% growth in post-consumer recycled material usage. Collaborative efforts are fostering material innovation and increasing cross-industry recycling efficiencies.

The sustainable packaging solution market is segmented by type, application, and end-user industries. Biodegradable plastics, recycled paper, and lightweight corrugated boards dominate the product mix. Applications span food & beverage, e-commerce, pharmaceuticals, personal care, and industrial packaging, each demonstrating distinct adoption behaviors. End-users such as FMCG and retail sectors lead the market, driven by consumer sustainability preferences. In 2024, FMCG accounted for more than 40% of demand, while healthcare and e-commerce are rapidly growing segments.

Biodegradable plastics represent the leading segment, accounting for 38% of adoption in 2024, supported by their expanding role in food packaging and healthcare applications. Recycled paper and corrugated board contribute around 30%, driven by e-commerce parcel shipments. Compostable films are the fastest-growing type, projected to grow at 9.5% annually due to expanding use in FMCG flexible packaging. Other types, including biopolymer blends and molded fiber packaging, collectively hold 32% share, serving niche industrial and consumer applications.

According to a 2025 U.S. Department of Agriculture report, biopolymer-based compostable films were introduced into large-scale fruit packaging, improving shelf life by 15% while reducing plastic dependency.

Food & beverage packaging leads the market with 42% share in 2024, driven by strict hygiene and sustainability mandates. E-commerce follows with 28%, supported by global shipping volumes. Healthcare applications are the fastest-growing, forecasted to expand at 10% annually, reflecting rising adoption of sterile biodegradable packaging. Industrial and personal care applications collectively contribute 30%. In 2024, over 38% of enterprises reported piloting sustainable packaging in logistics operations, while 57% of global consumers preferred eco-packaging in personal care products.

According to a 2024 European Commission report, compostable packaging in the dairy sector reduced plastic waste by 22%, benefiting over 12 million households.

The FMCG sector remains the dominant end-user, accounting for 41% of demand in 2024, supported by retail and consumer product manufacturers. E-commerce is the fastest-growing, projected at 11% annual growth, as online shopping surges across Asia-Pacific and North America. Healthcare, industrial, and luxury goods collectively contribute 34%. In 2024, 63% of Gen Z consumers indicated stronger trust in brands offering eco-friendly packaging, while 46% of global SMEs began integrating recyclable solutions in supply chains.

According to a 2025 Gartner report, sustainable packaging adoption among SMEs in retail rose by 22%, enabling 500+ firms to cut logistics waste significantly.

North America accounted for the largest market share at 35.4% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2025 and 2032.

North America recorded consumption volumes exceeding 82 million metric tons of sustainable packaging materials, driven by high adoption in food and beverage, healthcare, and retail industries. Europe followed with 27.6% share in 2024, supported by regulatory frameworks mandating eco-friendly packaging standards. Asia-Pacific, with demand exceeding 70 million metric tons in 2024, is projected to cross 125 million metric tons by 2032, led by China, India, and Japan. Latin America and Middle East & Africa contributed 6.8% and 5.2% respectively, where adoption is accelerating in agriculture, FMCG, and e-commerce logistics. Regional consumption trends are influenced by shifting consumer preferences, policy-driven sustainability targets, and localized production hubs enhancing supply efficiency.

How Are Innovative Material Substitutes Transforming Packaging Practices in This Region?

The region held nearly 35.4% of global market share in 2024, supported by rapid adoption in food & beverage, pharmaceuticals, and retail distribution. Regulatory initiatives such as single-use plastic bans in several U.S. states accelerated demand for compostable and biodegradable materials. Technological advancements include smart labeling and digital traceability for packaging optimization. Local players like Sealed Air Corporation are investing in bio-based foam packaging to reduce petroleum reliance. Consumer behavior reflects a shift toward premium eco-brands, with over 62% of enterprises in healthcare and finance sectors integrating sustainable packaging into supply chains to meet ESG commitments.

Why Are Circular Economy Policies Driving Adoption in This Region?

Europe accounted for 27.6% of market share in 2024, with Germany, the UK, and France leading adoption across FMCG, automotive, and healthcare sectors. Strict directives under the European Green Deal and EU Packaging Waste Directive accelerated transitions to recyclable, reusable, and compostable packaging solutions. Advanced innovations in fiber-based packaging and bio-polymers are driving industry compliance. Local players like Smurfit Kappa are investing in next-generation corrugated packaging tailored to e-commerce supply chains. Consumer demand leans toward transparency and eco-labels, with 58% of households preferring certified recyclable products, creating higher adoption momentum across retail and logistics.

What Role Does E-Commerce Expansion Play in Accelerating Packaging Innovation?

Asia-Pacific ranked second by volume in 2024, consuming over 70 million metric tons of sustainable packaging products, led by China, India, and Japan. The region is a global manufacturing hub, driving large-scale deployment of bio-plastics, plant-fiber materials, and compostable packaging for consumer goods and electronics. E-commerce expansion, which accounts for more than 48% of packaging demand in China and 36% in India, is pushing adoption of lightweight, recyclable solutions. Local players such as Japan’s Mitsubishi Chemical are pioneering plant-based polymer alternatives. Consumer preferences are evolving toward mobile-enabled traceability and eco-brands, with 64% of Gen Z buyers showing loyalty to sustainable-packaged products.

How Are Trade Policies and Local Industries Shaping Market Demand?

South America contributed 6.8% of global share in 2024, with Brazil and Argentina driving consumption in food processing, agriculture exports, and beverage sectors. Government trade policies incentivizing bio-packaging for export products are accelerating regional growth. Infrastructure projects in logistics and energy also support higher packaging demand. Local players such as Klabin in Brazil are focusing on renewable paper-based packaging solutions. Consumer preferences are influenced by affordability and sustainability balance, with nearly 45% of urban buyers in Brazil opting for reusable packaging formats, particularly in beverages and personal care products.

How Is Diversification Beyond Oil Creating New Packaging Opportunities?

The region contributed 5.2% of market share in 2024, with UAE, Saudi Arabia, and South Africa leading adoption. Demand is growing in construction, retail, and food distribution sectors as governments diversify away from oil dependence. Regulatory measures in GCC countries encourage biodegradable packaging for food imports, while African nations are adopting extended producer responsibility (EPR) frameworks. Local innovators, such as South Africa’s Mpact Limited, are expanding recycled packaging production. Consumer adoption reflects growing eco-consciousness, with over 41% of urban households preferring recyclable or refillable packaging, particularly in e-commerce and FMCG channels.

United States – 21.4% Market Share

High production capacity, strong FMCG and healthcare demand, and advanced R&D investment in biodegradable and compostable materials.

China – 18.6% Market Share

Large-scale manufacturing base, rapid e-commerce expansion, and government-backed initiatives supporting bio-based packaging innovation.

The Sustainable Packaging Solution market is moderately consolidated, with more than 450 active competitors globally. The top 5 companies collectively account for approximately 38% of the overall market, leveraging strong supply networks, product innovation, and mergers to maintain leadership. Competitive positioning is shaped by bio-based materials, digital printing technologies, and automation-driven packaging efficiency. Strategic collaborations between manufacturers and e-commerce giants are accelerating large-scale deployments. Companies are focusing on closed-loop recycling systems, with nearly 29% of market players investing in reusable packaging solutions. The rise of ESG-driven procurement policies is compelling businesses to adopt sustainable product lines, and local players are increasingly expanding capacity to meet regional regulatory mandates. Innovation in biodegradable polymers, plant-based composites, and water-soluble films is defining differentiation strategies, while competitive intensity remains high due to simultaneous demand from FMCG, retail, and healthcare end-users.

Amcor plc

Mondi Group

Klabin S.A.

DS Smith plc

Tetra Pak International S.A.

Uflex Ltd.

Mpact Limited

The Sustainable Packaging Solution market is witnessing rapid integration of advanced materials and digital innovations. Bio-based plastics made from corn starch, sugarcane, and cellulose derivatives are replacing conventional petroleum-based packaging at scale, with global production exceeding 2.8 million tons in 2024. Recyclable multi-layer films are enabling cost-efficient packaging with barrier properties suitable for food and pharmaceutical applications. Advanced nanotechnology coatings are being introduced to enhance shelf life and reduce food waste by 20–25% in pilot projects. Digital printing technologies are reshaping customization, with nearly 36% of packaging converters adopting cloud-based workflows and automation to minimize material wastage.

Emerging technologies such as water-soluble polymers and compostable films are gaining traction in personal care and single-use food service packaging. Blockchain-based traceability is increasingly applied in Europe and North America, providing real-time supply chain visibility for 15–20% of premium packaging brands. Smart packaging innovations, such as QR-enabled authentication and freshness indicators, are projected to expand consumer engagement while supporting regulatory compliance. Robotics and AI-driven automation are improving efficiency in sorting and recycling streams, with early deployments reporting productivity improvements of 28%. These technological shifts are positioning the market for significant long-term transformation, creating scalable solutions for industries pursuing net-zero commitments.

• In March 2023, Amcor introduced its AmFiber™ Performance Paper packaging in Europe, offering recyclability in standard paper streams while maintaining durability for frozen and chilled food applications. The new line is designed to replace multi-material plastic packaging. Source: www.amcor.com

• In October 2023, Smurfit Kappa launched its “Better Planet Packaging” innovation center in the UK, showcasing advanced fiber-based packaging solutions aimed at reducing single-use plastic. The center enables collaborative testing with retailers and manufacturers. Source: www.smurfitkappa.com

• In January 2024, Mondi unveiled a recyclable monomaterial pouch for dry food products, made from polyethylene with barrier properties that maintain product safety and freshness. The innovation replaces multi-material laminate structures. Source: www.mondigroup.com

• In June 2024, Uflex developed India’s first recyclable, mono-material PET-based packaging solution for snack products, designed to align with government EPR compliance frameworks. This innovation reduced packaging waste by nearly 30%. Source: www.uflexltd.com

The Sustainable Packaging Solution Market Report covers a wide spectrum of product types, including biodegradable plastics, paper-based packaging, plant-fiber materials, water-soluble films, and recyclable multilayer composites. Applications analyzed extend across FMCG, food and beverage, healthcare, e-commerce, personal care, automotive, and industrial distribution sectors. End-user insights highlight adoption patterns across small enterprises, multinational corporations, and public institutions.

Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with sub-regional coverage of leading countries including the United States, China, Germany, Brazil, and South Africa. The study evaluates regulatory impacts, technological advances, and sustainability targets shaping demand across regions.

The report also highlights technological innovations such as blockchain-enabled traceability, nanocoatings, robotics, and bio-based polymers. It includes a detailed review of competitive strategies, supply chain transformations, and ESG-driven procurement practices. Additionally, the report emphasizes niche growth areas like reusable packaging systems, plant-derived biopolymers, and smart packaging with interactive digital features. The scope positions the Sustainable Packaging Solution market as a pivotal domain for industries targeting compliance, cost efficiency, and sustainability-driven growth in global operations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 320,148.7 Million |

|

Market Revenue in 2032 |

USD 562,534.9 Million |

|

CAGR (2025 - 2032) |

7.3% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User Industry

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sealed Air Corporation, Smurfit Kappa Group, Mitsubishi Chemical Holdings Corporation, Amcor plc, Mondi Group, Klabin S.A., DS Smith plc, Tetra Pak International S.A., Uflex Ltd., Mpact Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |