Reports

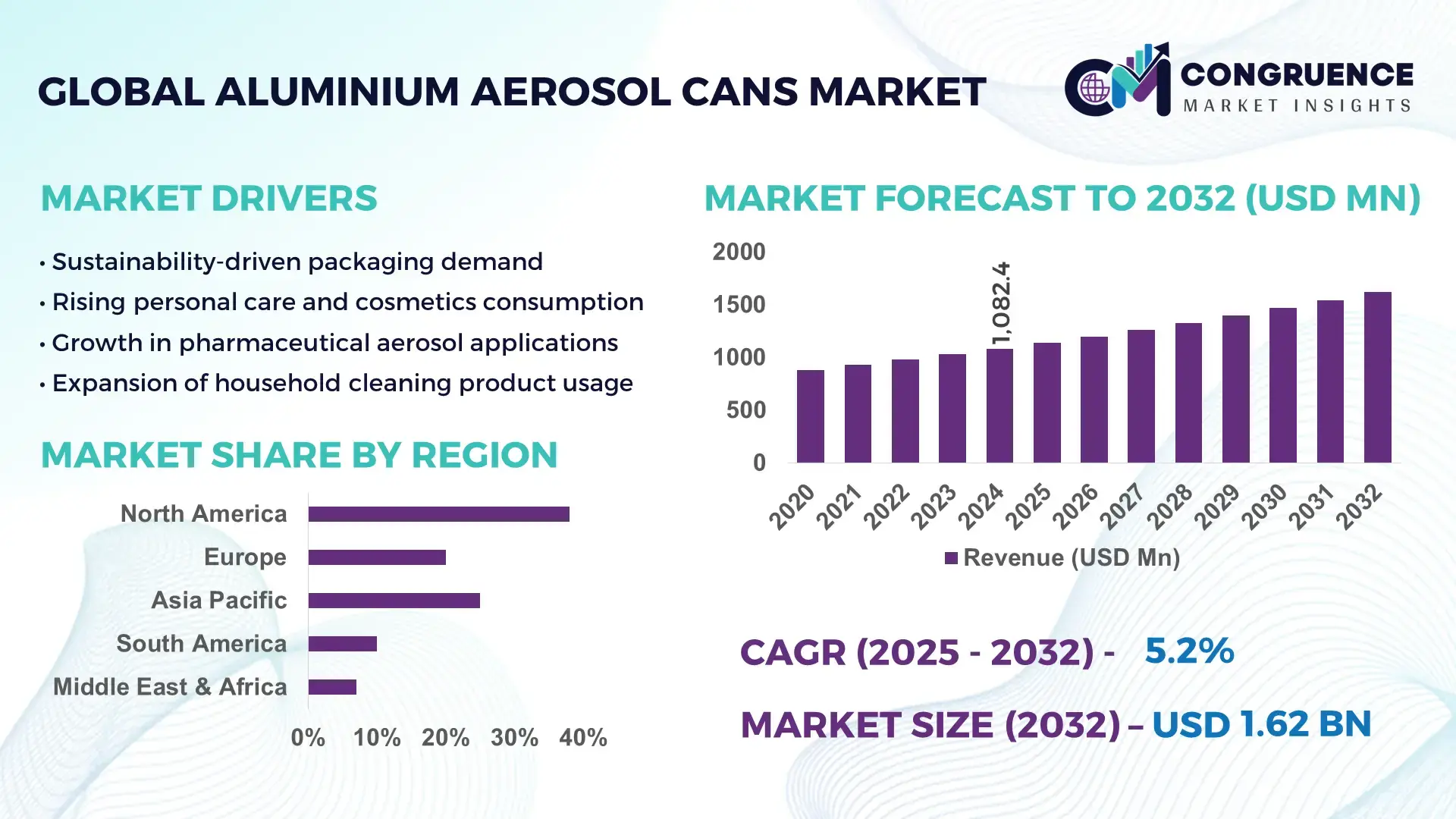

The Global Aluminium Aerosol Cans Market was valued at USD 1082.35 Million in 2024 and is anticipated to reach a value of USD 1623.66 Million by 2032 expanding at a CAGR of 5.2% between 2025 and 2032. Continuous packaging innovation and rising demand from personal care and household segments are accelerating market expansion.

Germany holds a strong position in the Aluminium Aerosol Cans market, supported by one of the world’s largest integrated aluminium packaging manufacturing ecosystems and an annual production capacity exceeding 6.2 billion aluminium aerosol units. Over USD 1.4 billion of cumulative investment has been directed toward automated can-forming systems, multi-layer spray coatings, and post-consumer aluminium recycling technologies in the last five years. The industry maintains high production output for deodorants, haircare, air fresheners, and pharmaceutical sprays, backed by heavy deployment of high-precision shaping and eco-friendly alloy processing lines. More than 68% of consumer aerosol packaging brands in Europe source from German suppliers due to consistent quality standards, lightweighting capabilities, and rapid scaling of smart-filling automation.

• Market Size & Growth: USD 1082.35 Million in 2024 projected to reach USD 1623.66 Million by 2032 at 5.2% CAGR, supported by surging demand for lightweight and recyclable packaging

• Top Growth Drivers: 37% rising adoption in personal care sprays, 29% production efficiency improvement, 22% growth in pharmaceutical aerosol applications

• Short-Term Forecast: By 2028, average unit production cost forecasted to drop by 13% due to advanced automated extrusion and material optimization

• Emerging Technologies: Monobloc shaping, digital printing for mass customization, and water-based internal coating technologies gaining rapid deployment

• Regional Leaders: Europe projected at USD 658 Million by 2032 driven by high personal care consumption; Asia Pacific at USD 521 Million with expanding industrial aerosols; North America at USD 339 Million with strong household spray usage

• Consumer/End-User Trends: High recurring demand from personal care, household care, healthcare aerosols, and automotive lubrication products with strong preference for recyclable lightweight metal packaging

• Pilot or Case Example: In 2024, a pilot production line by a leading manufacturer achieved 19% energy reduction and 14% unit-cycle time improvement via AI-based extrusion monitoring

• Competitive Landscape: Market leader holds roughly 18% share, followed by key competitors including Ball Corporation, Trivium Packaging, CCL Container, LINHARDT Group, and Alucon

• Regulatory & ESG Impact: Global sustainability regulations supporting recycled aluminium utilization and VOC-free coatings are accelerating technology upgrades

• Investment & Funding Patterns: More than USD 820 Million invested recently in R&D, automation, and recycling system upgrades across major global facilities

• Innovation & Future Outlook: Integration of digital printing, eco-alloy formulations, and smart aerosol valve systems expected to drive next-generation product developments through 2032

The Aluminium Aerosol Cans market continues to expand due to rising demand for recyclable and durable packaging formats across personal care, household chemicals, pharmaceuticals, and industrial sprays, each contributing significantly to overall market share allocation. Innovative barrier coating formulations, lightweight alloy processing, and smart-print customization are reshaping product portfolios while regional consumption patterns reflect strong growth in Asia Pacific and Europe. Environmental compliance, low-carbon manufacturing initiatives, and circular recycling policies are playing a key role in procurement strategies and supply chain modernization. The market outlook suggests steady long-term growth driven by sustainable material adoption, aerosol application diversification, and continued investment in automation and high-precision manufacturing technologies.

The Aluminium Aerosol Cans Market holds substantial strategic relevance as industries transition toward high-performance, recyclable, and lightweight packaging formats. Technological upgrades in monobloc shaping, digital mass custom printing, and eco-alloy processing are reshaping production efficiency and product differentiation. Automated extrusion platforms integrated with real-time analytics deliver 27% improvement compared to conventional single-stage forming lines, enhancing speed, safety, and spray precision. Europe dominates in volume, while Asia Pacific leads in adoption with 63% of aerosol manufacturers integrating smart-filling automation. Over the next 2–3 years, digital printing and AI-based defect mapping are expected to reduce production downtime by 18% by 2027. ESG-compliant manufacturing is becoming a procurement prerequisite across personal care, pharmaceuticals, and household sprays, with firms committing to recycling improvements such as 32% post-consumer aluminium recovery and reprocessing by 2030. In 2024, Germany achieved a 21% material efficiency improvement through an AI-enabled coating optimisation initiative. Future pathways include the integration of bio-propellant compatibility, lightweight alloys with reduced carbon intensity, and IoT-enabled packaging traceability, positioning the Aluminium Aerosol Cans Market as a pillar of resilience, compliance, and sustainable growth.

Rising consumption of deodorants, hair styling sprays, air fresheners, and surface cleaners is directly accelerating production requirements for the Aluminium Aerosol Cans Market. Over 71% of new personal care spray launches globally now utilise aluminium containers due to their durability and corrosion resistance. Additionally, premium brands are adopting high-precision digital printing and gradient coating finishes to enhance branding value and retail appeal. Growth in organized retail and e-commerce has also increased product turnover rates for aerosol-based hygiene and grooming items, compelling manufacturers to scale capacity with faster line speeds and higher unit output. Increased adoption of travel-size packs and multipack consumer formats further supports an upward volume trajectory for aluminium packaging solutions across consumer hygiene and household goods categories.

Volatility in raw aluminium cost and supply chain disruptions associated with bauxite mining, energy pricing, and transportation constraints are imposing operational pressure on the Aluminium Aerosol Cans Market. Manufacturers face elevated expenditures associated with alloy procurement, smelting, and cold extrusion processes, making cost optimisation a critical challenge. Geopolitical uncertainties and carbon-linked tariffs further contribute to price instability for primary aluminium feedstocks. Although recycled aluminium presents a cost-efficient alternative, supply volumes remain insufficient to meet rapid global production growth, leading to intermittent shortages. Logistics disruptions are also affecting delivery lead times, causing delays for finished aerosol packaging across personal care and household industries.

Increasing regulatory and consumer emphasis on sustainable packaging is creating major opportunities for the Aluminium Aerosol Cans Market. Advanced alloy formulations using post-consumer aluminium and water-based internal coatings align with circular design mandates and enable high-volume adoption across healthcare, personal care, and industrial sectors. AI-enabled quality monitoring and digital printing for mass customisation present strong prospects for branding differentiation and production optimisation. Growth in bio-propellant-compatible aerosol products and refill-ready application formats is also encouraging further innovation. With more than 44% of personal care brands planning to transition to low-carbon packaging by 2030, manufacturers leveraging smart automation and sustainable alloy technologies are well-positioned for long-term gains.

Escalating requirements around carbon intensity reduction, VOC-free internal coatings, and recyclable-content certifications are presenting cost and compliance challenges for the Aluminium Aerosol Cans Market. Manufacturers must invest significantly in upgrading extrusion lines, supply chain traceability infrastructure, and sustainable coating chemistries to meet mandatory certification criteria. Recycling integration requires extensive logistical coordination and advanced processing infrastructure to ensure consistent alloy quality. Compliance audits and environmental reporting standards add administrative pressure and extend product qualification timelines for personal care, pharmaceutical, and household aerosols. These combined regulatory and sustainability demands continue to elevate capital and operational expenses for market participants.

• Surge in Digital Printing and Mass Customisation Capabilities: Digital printing adoption in the Aluminium Aerosol Cans market has accelerated, with 48% of new production lines integrating high-resolution direct-to-metal printing systems in 2024. Brands are leveraging variable data printing to support up to 30,000 unique design runs per batch, improving product differentiation and promotional agility. Manufacturers report a 22% reduction in labelling and packaging lead times due to the removal of secondary labeling processes. Personal care and cosmetics segments are the fastest adopters, accounting for nearly 62% of digitally printed aerosol formats launched over the past year.

• Rapid Shift Toward High-Recycled-Content Alloy Formulations: Sustainability-focused procurement is driving increased demand for aluminium aerosol cans containing high percentages of recycled content. Manufacturers have increased post-consumer recycled aluminium use by 36% between 2022 and 2024 to comply with low-carbon packaging requirements. Facilities implementing closed-loop alloy recovery have achieved 19% reductions in metal waste per production cycle. Regulatory pressures in Europe and North America are contributing to the highest adoption rates, with 54% of new consumer aerosol product launches marketed as recyclable or low-carbon packaging.

• Adoption of AI- and Automation-Enabled Production Lines: Automation has become a defining trend, with 41% of major global producers deploying AI-enabled extrusion and defect-detection systems to optimise line speed and reduce production variations. Smart filling modules have resulted in measurable gains, with a 17% drop in rejected units and a 14% improvement in material utilisation. Manufacturers integrating automated valve-crimping and pressure monitoring systems report consistently stable output above 900 cans per minute. Asia Pacific currently leads technology uptake, driven by large-scale capacity expansion plans.

• Expansion of Pharmaceutical and Medical Aerosol Applications: The growth of pharmaceutical sprays and medical disinfectant aerosols is significantly influencing market direction. Across 2023–2024, medical and healthcare applications accounted for a 28% increase in order volumes for sterile-grade aluminium aerosol packaging. Demand is rising for barrier-coated interiors and biocompatible dispensing valves, with 33% of market participants ramping investments in medical-grade production lines. Cold-chain compatible aluminium aerosol containers are being adopted by 21% more pharmaceutical manufacturers to support temperature-sensitive spray therapies and sanitisation solutions.

The Aluminium Aerosol Cans Market is segmented across types, applications, and end-user categories, each showing distinct adoption patterns and technological direction. Types include monobloc cans, two-piece aluminium cans, and lightweight multi-layer coated cans, each serving different filling and durability requirements. Applications span personal care, household care, pharmaceuticals, and industrial sprays, reflecting varied performance, compliance, and safety expectations. End-users range from FMCG, healthcare, automotive, and hospitality to institutional customers, with increasing adoption of recyclable and lightweight packaging formats. The market landscape is evolving toward high-precision digital printing, eco-alloy processing, and smart aerosol fitment technologies. Demand concentration remains highest in personal care and household care, while healthcare and industrial sectors are expanding rapidly due to sterilization, lubrication, and disinfection requirements across commercial and medical environments.

Monobloc aluminium aerosol cans represent the leading type in the Aluminium Aerosol Cans Market, accounting for 57% of total consumption due to their seamless structure, high burst resistance, and compatibility with high-pressure aerosol formulations. Their dominance is reinforced by strong use in deodorants, hair sprays, automotive lubricants, and medical disinfectants where leak-proof and corrosion-resistant structures are critical. Two-piece aluminium cans are gaining momentum as the fastest-growing segment, supported by a 6.8% CAGR, driven by increasing adoption among personal care and cosmetics brands seeking reduced material use and enhanced surface printing flexibility. Lightweight multi-layer coated cans, though niche, contribute meaningfully to efficiency-focused applications in pharmaceuticals and household care, representing a combined 18% share across remaining segments for long-shelf-life or chemically aggressive formulas.

Personal care dominates as the leading application in the Aluminium Aerosol Cans Market, covering 51% of usage driven by high-volume global demand for deodorants, hair sprays, body mists, and cosmetic aerosols supported by robust retail penetration and repeat purchase cycles. Household care products hold 23% of consumption, while pharmaceuticals currently represent 14%; however, pharmaceutical aerosol adoption is expanding fastest with a 7.4% CAGR due to the growing need for sterilized packaging for nasal sprays, disinfectants, topical pain relief aerosols, and respiratory treatments. Industrial aerosols and automotive applications—lubricants, anti-corrosion coatings, and precision cleaners—together contribute 12% and offer steady demand for high-pressure aluminium packaging.

FMCG represents the leading end-user segment in the Aluminium Aerosol Cans Market, accounting for 58% of total consumption supported by persistent demand for personal grooming and household hygiene products and the continued dominance of aluminium packaging in aerosol-enabled daily-use items. Healthcare is the fastest-growing end-user, expanding at an 8.1% CAGR due to rising adoption of aluminium aerosol delivery formats in disinfectants, metered sprays, topical treatments, and respiratory therapies. Automotive and industrial sectors collectively account for 22% of demand and are driven by maintenance sprays, cleaning agents, and anti-rust coatings where precision spray dispersal is required. Hospitality and institutional procurement—covering hotels, hospitals, and commercial facilities—represent the remaining 9% and are expanding gradually with increased emphasis on hygiene and sanitation compliance.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2025 and 2032.

Europe followed with a 28% share, driven by eco-focused packaging regulations and advanced can-forming automation deployments. South America held 9% of the market, supported by rising demand for personal care and institutional sanitation products. The Middle East & Africa collectively represented 7%, led by expansion in industrial maintenance sprays and hygiene aerosols. Across all regions, personal care and healthcare applications accounted for 64% of total aluminium aerosol can consumption in 2024.

How are sustainability-driven packaging innovations transforming aluminium-based spray solutions?

The North America Aluminium Aerosol Cans Market represented 24% of global consumption in 2024, driven primarily by strong demand from personal care, household care and medical disinfectant applications. Healthcare and pharmaceutical aerosols have shown the fastest adoption rate, with hospitals and clinics increasing usage by 31% during 2023–2024. Regulations supporting recyclable metal packaging have accelerated the use of high-recycled-content aluminium units, especially in the U.S. where multiple states enforce extended producer responsibility compliance for packaging. Digital printing and AI-based defect inspection systems are shaping production efficiency trends, with line automation adoption rising by 18% among regional producers. A notable player, CCL Container, expanded its Ohio facility by increasing monobloc aerosol can output to over 400 million units annually. Consumer behaviour in North America shows higher acceptance of medical and hygiene aerosols in both enterprise and household environments.

Is the shift toward circular packaging standards accelerating next-generation aerosol formats?

The Europe Aluminium Aerosol Cans Market accounted for 28% of global demand in 2024, with Germany, the UK, and France representing 71% of regional volume. Strong sustainability regulations and emissions-based packaging rules have increased transitions to low-carbon alloys and 100% recyclable can structures. Adoption of digital embossing, UV-curable coatings, and water-borne inks is rising across production lines to reduce environmental footprint. Local manufacturers have integrated smart laser inspection and automated visual tracking to reduce internal coating failure rates by up to 14%. A prominent example is an Italian producer deploying a new carbon-neutral aerosol filling facility with an annual output exceeding 280 million cans. Consumers in Europe demonstrate a strong preference for sustainable aerosol packaging that offers transparency in materials and disposal processes.

Are large-scale capacity expansions meeting rising consumer and industrial aerosol requirements?

The Asia-Pacific Aluminium Aerosol Cans Market is the highest volume contributor, representing 41% of global output in 2024. China, India, and Japan collectively generated 84% of regional demand driven by personal grooming, disinfectant sprays, automotive maintenance fluids, and industrial lubrication aerosols. The region hosts several mega-manufacturing clusters with high-speed extrusion machines and automated valve-crimping lines designed to support production of over 1.2 billion units annually. Technology adoption is also expanding, with 22% of regional facilities integrating digital printing and predictive maintenance systems. A major Japanese manufacturer recently deployed lightweight alloy aerosol can technology to reduce material use per unit by 12% while enhancing durability. Asia-Pacific consumer behaviour reflects high uptake of aerosol hygiene and beauty products purchased through e-commerce channels.

How is rising domestic production capacity reshaping the aerosol packaging ecosystem?

The South America Aluminium Aerosol Cans Market accounted for 9% of global demand in 2024, primarily driven by Brazil and Argentina, which jointly held 72% of regional volume. Expansion of local FMCG and institutional hygiene sectors has sharply increased adoption of aluminium aerosol packaging for deodorants, disinfectant sprays, and cleaning agents. Investments in regional aerosol filling facilities have strengthened supply resilience, with multiple new lines increasing collective capacity by 310 million units annually. A notable Brazilian producer recently invested in energy-efficient curing furnace systems to reduce power consumption by 17% per production cycle. Consumer behaviour in South America reflects higher demand for fragranced personal care aerosols and sanitation sprays across urban retail chains.

Are industrial and infrastructure developments accelerating adoption of advanced aerosol product formats?

The Middle East & Africa Aluminium Aerosol Cans Market represented 7% of global demand in 2024 with strong traction from industrial maintenance sprays, automotive care products, and institutional hygiene aerosols. The UAE and South Africa are the leading growth engines, together accounting for 58% of regional demand. Rapid modernization of industrial plants and automotive service facilities has increased the consumption of lubrication and anti-rust aerosols packaged in high-pressure aluminium units. Ongoing trade partnerships have encouraged import and local-scale production of aluminium aerosol containers to meet rising demand. A South African distributor recently expanded its specialised hospital-grade disinfection aerosol program across 180 healthcare institutions. Regional consumer behaviour indicates growing demand for high-performance maintenance and sanitation products in commercial and industrial sectors.

• China – 26% share — China leads the Aluminium Aerosol Cans Market driven by unmatched production capacity and extensive consumption across personal care, industrial, and automotive aerosol applications.

• Germany – 14% share — Germany maintains a key position in the Aluminium Aerosol Cans Market due to advanced sustainability regulations and strong personal care and household spray manufacturing clusters.

The Aluminium Aerosol Cans market presents a moderately consolidated competitive environment, with nearly 35–40 active global manufacturers and over 120 regional players competing across personal care, household, automotive, and pharmaceutical applications. The top 5 companies collectively account for approximately 52% of the global market share, driven by strong production capacity, advanced shaping and printing capabilities, and long-term contracts with FMCG and cosmetics brands. Competitive intensity continues to rise as companies focus on lightweighting innovations, recycled aluminium integration, and high-speed digital printing lines to enhance design precision and SKU flexibility. More than 60% of leading players have engaged in strategic initiatives since 2022, including product portfolio expansion, capacity enhancement, and regional distribution partnerships. Mergers and acquisitions have increased by nearly 18% over the past two years as companies aim to strengthen supply chain security and reduce raw material procurement costs. Sustainability-driven differentiation is a central competitive lever, with over 70% of manufacturers committing to >80% recycled aluminium utilisation over the next decade, further shaping the market dynamics.

Ball Corporation

CCL Industries

Trivium Packaging

Crown Holdings, Inc.

Alucon Public Company Limited

Nampak Ltd

Shanghai Sunway Aluminium Packaging Co., Ltd.

TUBEX GmbH

Bharat Aerosol Industries Pvt. Ltd.

Aryum Metal Packaging Co.

The Aluminium Aerosol Cans Market is increasingly driven by advanced manufacturing and packaging technologies that enhance production efficiency, product performance, and sustainability. Monobloc can-forming technology remains a foundational process, with over 62% of global production lines utilizing seamless extrusion-drawing to ensure high-pressure resistance and uniform wall thickness. Digital printing and laser-etching systems are being integrated into more than 48% of new production facilities, enabling variable data designs, high-resolution branding, and faster SKU changeovers, reducing lead times by up to 22%. Multi-layer internal coating technology is widely adopted in 34% of manufacturing plants to provide superior chemical resistance, extend shelf life, and maintain product integrity for pharmaceutical and industrial aerosol applications.

Automation and AI-driven quality control are transforming operational efficiency, with defect detection and predictive maintenance modules cutting production downtime by 17% on average and improving material utilization by 14%. Lightweight aluminium alloys with enhanced tensile strength are replacing conventional materials in 29% of new can deployments, reducing material consumption by 12% per unit while maintaining durability. Emerging trends also include water-based internal coatings, bio-propellant compatibility, and smart valve technologies designed for metered and controlled dispensing. Additionally, IoT-enabled production monitoring and end-to-end traceability are being implemented in 26% of plants to support regulatory compliance and ESG objectives. Collectively, these technological advancements are enabling manufacturers to meet rising consumer demand, improve operational resilience, and align with sustainability-driven packaging mandates across the global aluminium aerosol cans market.

In 2024, total worldwide deliveries of aluminium aerosol cans reached 6.75 billion units, marking a 4.2% increase from 2023. Global demand remained robust across personal care, household, pharmaceutical, and food aerosol segments. (International Aluminium Journal)

In 2024 the Trivium Packaging and the Turkish manufacturer Aryum secured top honours at the AEROBAL World Aluminium Aerosol Can Awards: Trivium for an insect‑repellent aluminium can with bag‑on‑valve spray technology and Aryum for a premium non‑gas perfume can featuring 360° embossed shaping with oriented printing. (Packaging Connections)

In the first half of 2024, deliveries from AEROBAL member companies rose 4.4% to over 3.4 billion units, driven particularly by a 7% increase in deodorants and an 8% increase in hairsprays, along with ~12% growth in food aerosol deliveries. (Packaging Europe)

Through 2024, a leading packaging firm implemented a lightweight‑alloy can design using an aluminium formulation containing 25% recycled content produced with renewable energy and reducing internal varnish use by nearly 50%, significantly lowering the carbon footprint of aerosol packaging. (CanTech International)

This Aluminium Aerosol Cans Market Report covers a comprehensive global scope, examining product segmentation by type — including monobloc, two‑piece, and multi‑layer coated cans — and application areas such as personal care, household care, pharmaceuticals, industrial aerosols, and food‑grade spraying solutions. It evaluates regional markets globally, covering North America, Europe, Asia‑Pacific, South America, Middle East & Africa, with detailed breakdowns of production volumes, consumption trends, and regional infrastructure realities. The report also surveys end‑user industries — FMCG, healthcare, automotive, hospitality, industrial maintenance — assessing adoption rates, consumer behaviour, and procurement preferences. On the technology front, the report analyses manufacturing technologies such as seamless extrusion, high-speed digital printing, bag‑on‑valve systems, multi‑layer chemical-resistant coatings, recycled‑content alloy formulations, and automation including AI-enabled quality control and smart valve integration. It assesses regulatory and sustainability landscapes, including recycled-material mandates, VOC‑free coatings, and lifecycle‑led packaging standards. Finally, the report highlights niche and emerging segments such as medical aerosol cans, bio-propellant compatible containers, lightweight eco‑alloy units, and premium cosmetic aerosol packaging — offering insights for strategic decision‑makers assessing investments, capacity expansions, or product portfolio diversification across geographic and application-based segments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1082.35 Million |

|

Market Revenue in 2032 |

USD 1623.66 Million |

|

CAGR (2025 - 2032) |

5.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ball Corporation , CCL Industries , Trivium Packaging , Crown Holdings, Inc., Alucon Public Company Limited, Nampak Ltd, Shanghai Sunway Aluminium Packaging Co., Ltd., TUBEX GmbH, Bharat Aerosol Industries Pvt. Ltd., Aryum Metal Packaging Co. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |