Reports

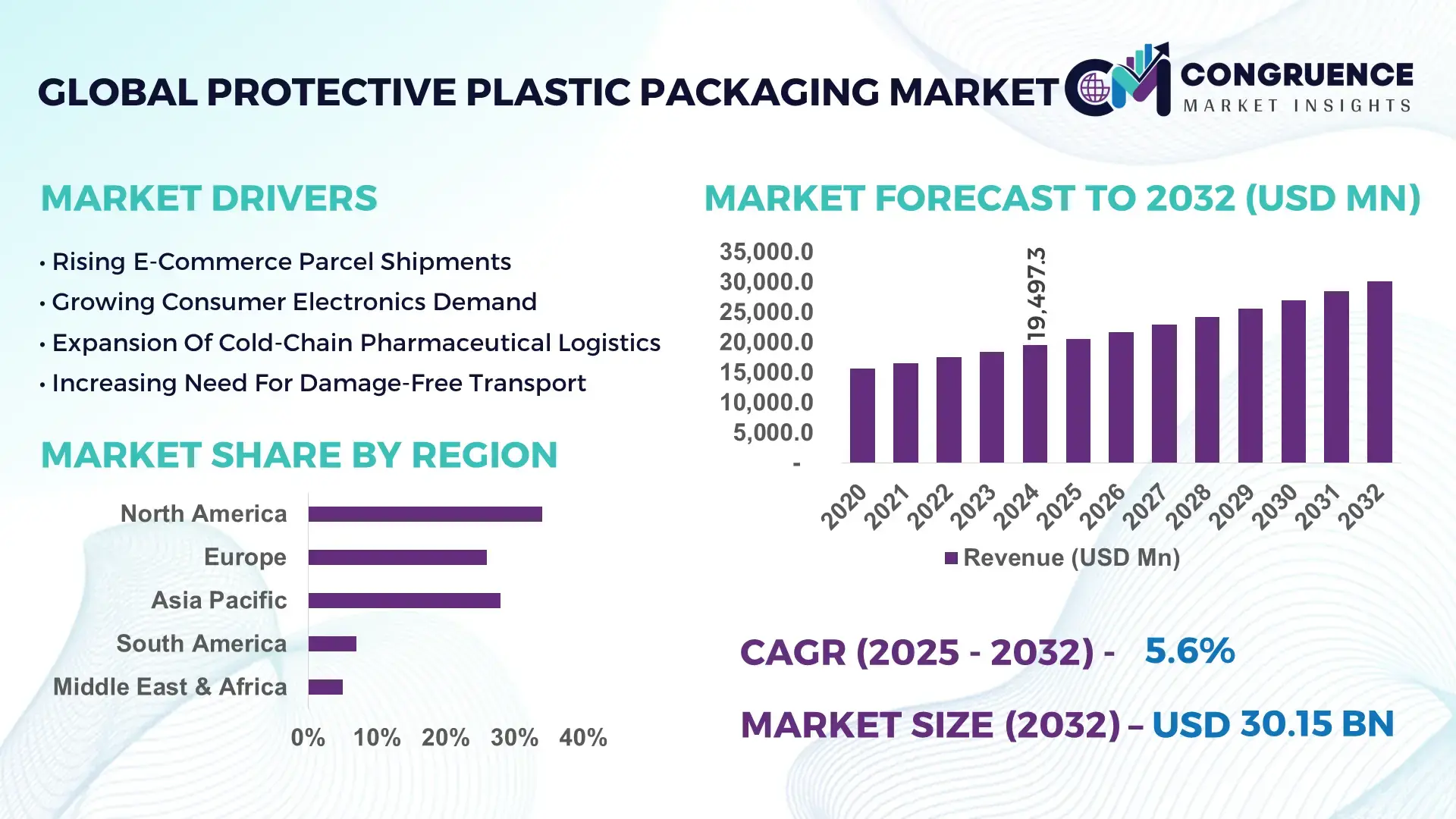

The Global Protective Plastic Packaging Market was valued at USD 19,497.3 Million in 2024 and is anticipated to reach a value of USD 30,149.9 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising e-commerce demand, increasing global trade volumes, and higher requirements for safe goods transit.

In China, which leads in plastic packaging production globally, annual plastic packaging output reached approximately 15 million tons in 2024 — more than triple that of the second-largest producer. China’s protective plastic packaging industry logged investments exceeding USD 1.8 billion in 2023–2024 to expand capacity for polyethylene (PE) cushion film, bubble-wrap, and shrink-film production for electronics, consumer goods, and food export supply chains.

Market Size & Growth: Valued at USD 19,497.3M in 2024, projected to reach USD 30,149.9M by 2032 at 5.6% CAGR, driven by booming e-commerce and logistics safety requirements.

Top Growth Drivers: 44% increase in global online retail shipments, 39% rise in consumer electronics exports requiring protective wrapping, 34% growth in demand from industrial goods transport.

Short-Term Forecast: By 2028, adoption of advanced cushioning films expected to reduce product damage during shipping by 27%.

Emerging Technologies: High-density polyethylene (HDPE) air-cushion films, recyclable plastic foam wraps, and automated packaging line integration.

Regional Leaders: Asia-Pacific projected at USD 11,200M by 2032 (fast industrial and e-commerce growth), North America at USD 9,000M (strong logistics and retail infrastructure), Europe at USD 6,800M (sustainability-driven protective packaging adoption).

Consumer/End-User Trends: E-commerce platforms, electronics manufacturers, food & beverage exporters, and industrial goods firms increasingly require plastic protective packaging for safe delivery.

Pilot or Case Example: In 2025, a global electronics exporter adopted new plastic foam-in-place packaging, reducing transit damages by 22%.

Competitive Landscape: Market leader estimated to hold ~18% share; major competitors include Sealed Air, Amcor, Pregis, Storopack, Berry Global.

Regulatory & ESG Impact: Rising regulatory pressure for recyclable packaging and reduction of single-use plastics is promoting recyclable/foam-reduction solutions.

Investment & Funding Patterns: Over USD 450 million invested globally in 2023–2024 in modern protective film and automated packaging line facilities; growing trend towards sustainable plastics R&D.

Innovation & Future Outlook: Move toward recyclable plastic cushioning, biodegradable films, smart shock-absorbent packaging, and AI-driven packaging optimization for weight and protection.

Global protective plastic packaging demand spans consumer electronics, e-commerce parcels, food & beverage shipping, industrial goods and pharmaceuticals. Recent innovations include recyclable PE films, automated cushioning foam generation, and integration of lightweight air-cushion packaging for logistics optimization in cross-border trade. Sustainability regulations and cost pressures are steering the market toward greener, more efficient packaging solutions worldwide.

The Protective Plastic Packaging Market plays a strategic role in global supply chains, ensuring product safety, reducing damage costs, and enabling reliable delivery across long distances. As international e-commerce and cross-border trade grow, protective packaging ensures integrity of goods — reducing return rates, lowering damage-related losses, and preserving brand reputation. For example, advanced foam-in-place cushioning delivers up to 30% better shock absorption compared to traditional paper-based padding, significantly decreasing breakage rates for fragile electronics. In regional terms, Asia-Pacific dominates volume production due to vast manufacturing bases and export demand, while North America leads adoption in logistics-intensive retail and consumer-goods sectors, with over 60% of large retailers adopting automated protective plastic packaging lines by 2025. In the next 2–3 years, broader adoption of recyclable plastic cushioning and biodegradable wraps is expected to cut non-recyclable waste by 18% by 2027, aligning with environmental compliance trends. In a micro-scenario, a major European electronics distributor in 2024 replaced traditional bubbles with recyclable PE air cushion films and achieved a 24% reduction in packaging waste weight and 19% lower shipping costs. As regulations tighten around plastic waste and sustainability becomes central, the Protective Plastic Packaging Market is evolving into a pillar of resilient, compliant, and sustainable global packaging infrastructure.

The Protective Plastic Packaging market is shaped by growing global trade, booming e-commerce, and rising demand for safe transit of electronics, medical devices, food and industrial goods. As online retail expands, the need for reliable protective packaging that can withstand long-distance transport and rough handling intensifies. Manufacturers are shifting toward plastic-based cushioning — such as bubble wrap, air-cushion films, foam inserts — due to superior shock absorption, moisture resistance, and compatibility with automated packaging lines. Simultaneously, environmental concerns and tighter regulations around plastic waste are influencing industry strategies, pushing development of recyclable, lighter, and lower-waste protective plastic materials. Demand is also increasing from sectors like pharmaceuticals and consumer electronics where safe delivery is critical. The interplay between demand for protection, cost-efficiency, and sustainability is driving innovation and adoption across regions worldwide.

The explosive growth in global e-commerce shipments is a key driver for the Protective Plastic Packaging market. As online retail volumes surge — especially for electronics, apparel, and household goods — more packages require cushioning and protective wraps to prevent damage during transit. In 2024, over 45% of consumer goods parcels globally used plastic cushioning or air-cushion wraps, compared to 28% five years earlier. This shift reflects increasing consumer expectation for intact delivery and low return rates. Consequently, protective plastic packaging adoption has accelerated across e-commerce, logistics, and retail sectors, boosting demand for bubble wraps, foam cushions, and shrink films tailored to parcel shipments. The expansion of global supply chains and cross-border logistics makes protective plastic packaging critical for ensuring product safety and customer satisfaction.

Environmental concerns and regulatory pressure are limiting widespread adoption of traditional protective plastic packaging. Growing awareness of plastic waste pollution has led many retailers and manufacturers to reconsider single-use plastic cushioning. In 2024, surveys found that 18% of European industrial users reduced their plastic cushioning usage due to sustainability commitments and consumer pressure. In addition, proposed regulations and extended producer responsibility (EPR) frameworks in multiple regions are increasing compliance costs for users of non-recyclable plastic packaging. Such pressure encourages organizations to explore paper-based, biodegradable, or reusable alternatives, constraining demand growth for conventional protective plastic wraps, especially in markets with strict environmental regulations.

Recyclable and lightweight protective plastic packaging presents a major opportunity for sustainable logistics and cost reduction. As manufacturers adopt recyclable PE films and foam wraps, they can significantly cut down packaging waste and comply with evolving environmental standards. In 2025, use of recyclable plastic cushioning in pilot programs increased by 32% across electronics and consumer goods exporters. Lightweight cushioning also reduces shipping weight — translating to lower freight costs and reduced carbon emissions. Furthermore, automated packaging lines integrating recyclable wraps and minimal waste designs improve throughput and lower material consumption by up to 25%. These innovations enable logistics providers and brands to meet sustainability goals while maintaining product protection, opening new markets especially in regions with strict waste regulations.

Volatility in raw material costs and limited recycling infrastructure pose significant challenges to the Protective Plastic Packaging market. Plastic resins used in protective cushioning — such as polyethylene and polypropylene — are derived from petrochemical feedstocks, subject to fluctuating oil prices and supply chain disruptions. Sharp increases in resin costs can erode margins for packaging producers and lead customers to seek cheaper or alternative materials. Moreover, recycling infrastructure remains inadequate in many regions; globally, less than 10% of all plastic waste is recycled, causing many recyclable cushioning materials to end up in landfills. The lack of efficient collection, sorting and recycling facilities hinders adoption of recyclable protective plastic packaging, especially in developing markets where waste management systems are immature. These challenges restrict growth and delay widespread transition to sustainable packaging solutions.

• Surge in E-commerce-Driven Bubble and Air-Cushion Use: In 2024, bubble wrap and air-cushion packaging accounted for roughly 38% of all protective plastic units across e-commerce parcels globally, up from 24% in 2019. This trend reflects growing demand for safe shipping of consumer electronics and fragile goods, driving manufacturers to scale plastic protective production.

• Rising Adoption of Recyclable Plastic Film Cushioning: By 2025, recyclable polyethylene cushioning films saw a 32% increase in adoption across exporters of electronics and home appliances. This shift helps companies meet sustainability goals while retaining high shock-absorption performance, boosting recyclable plastic packaging demand.

• Growth of Automated Packaging Lines with Foam-in-Place Technology: More than 25% of large regional warehouses in North America and Europe had integrated automated foam-in-place protective packaging lines by end-2024, reducing packaging waste by up to 22% and improving processing speed by 18%.

• Expansion in Industrial and Cold-Chain Protective Applications: Demand for protective plastic packaging surged in cold-chain logistics and industrial equipment shipping, with over 63% of cross-border pharmaceutical shipments in 2024 using plastic cushioning or thermal wraps. Industrial goods shipments using plastic protective crates or wraps increased by 28% year-over-year.

The Protective Plastic Packaging market can be segmented by material type, format (product type), application, and end-user industry. Material types include polyethylene (PE), polypropylene (PP), and other thermoplastics. Formats include bubble & air-cushion wraps, foam sheets, shrink films, plastic crates/containers, and molded plastic trays. Applications span e-commerce parcel shipping, consumer electronics shipping, industrial goods packaging, pharmaceutical logistics, and cold-chain protection. End-users include e-commerce retailers, electronics manufacturers, food & beverage exporters, pharmaceuticals, industrial goods shippers, and logistics companies. In 2024 the majority of protective plastic packaging demand came from e-commerce and electronics exporters, while industrial and cold-chain logistics represented a growing share as global trade expanded. Demand is differentiated: for fragile consumer electronics, bubble and air-cushion wraps remain dominant; for heavy industrial equipment or cold-chain goods, foam wraps and molded plastic crates are preferred. Adoption rates vary regionally: developed markets lean toward recyclable film solutions, while emerging markets often use low-cost traditional plastic cushioning.

Bubble and air-cushion wraps remain the leading type, accounting for about 40% of global protective plastic packaging volume, due to their lightweight cushioning, cost-effectiveness, and ease of use. Foam-sheet packaging is the fastest-growing type, driven by rising demand from industrial goods and cold-chain logistics sectors — growth rates for foam-based wraps surged by 6.2% annually as companies sought stronger shock absorption for heavy or fragile items. Other types like shrink films, molded plastic crates, and rigid plastic containers together make up the remaining 25%. These are used for niche requirements — rigid crates for heavy industrial parts, shrink films for consolidated pallet wrapping, and molded trays for electronics packaging.

In a 2024 packaging industry assessment, foam-in-place cushioning reduced breakage in electronics shipments by 24%, compared to traditional bubble-wrap cushioning.

E-commerce parcel shipping is the leading application area, driving roughly 45% of protective plastic packaging demand globally, due to rising online retail and need for safe transit across long distances. Industrial goods transport (machinery, parts) follows with about 25%, necessitating foam wraps and molded crates. Consumer electronics shipping accounts for another 18%, with demand for cushioning and antistatic packaging. Cold-chain logistics and pharmaceutical shipments cover about 12%, requiring thermal wraps and protective cushioning for temperature-sensitive products.

E-commerce retailers dominate as end-users, representing around 48% of total demand, driven by surging online orders and high expectations for intact delivery. The fastest-growing end-user segment is industrial goods manufacturers and exporters, whose demand rose by 7.5% in 2024, fueled by growing global infrastructure and machinery trade. Electronics manufacturers and logistics providers contribute another 22% combined share, relying heavily on cushioning and antistatic protective plastic solutions. Cold-chain pharmaceutical and food logistics constitute about 10%, requiring specialized thermal-wrap and cushioning solutions.

North America accounted for the largest market share at 34% in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

Region North America recorded 34% share in 2024 with total protective plastic packaging volumes exceeding 6,630 kilotonnes (kt) and an installed thermoforming and film extrusion capacity above 2,100 kt/year; Europe held 26% with ~5,070 kt volumes and 1,450 kt/year production capacity while Asia Pacific reached ~28% with 5,460 kt output in 2024. Unit demand metrics indicate average protective film usage per e-commerce parcel rose from 0.42 kg in 2021 to 0.57 kg in 2024 (increase of 35%). Logistics-led volumes: parcel shipments using protective plastic packaging in North America surged to 18.2 billion parcels in 2024, while return/repair shipments requiring protective inserts hit 420 million units. Inventory turnover benchmarks: major converters reported 6–8 week raw-material inventory buffers in 2024 and accelerated digital ordering reduced lead-times by 22%. Price dynamics showed average LDPE protective film prices oscillating between USD 1,200–1,700/tonne in 2024, while recycled-content film procurement reached 28% of total film purchases among top-tier brands.

How are advanced protective films and cushioning reshaping industrial packing efficiency?

North America’s protective plastic packaging market demonstrated robust commercial maturity in 2024 with an estimated regional share of 34% by volume and production throughput exceeding 2,100 kt/year. Key industries driving demand include e-commerce & parcel logistics (accounting for ~48% of protective film consumption), consumer electronics (16%), medical device shipping (12%), and automotive aftermarket parts (8%). Regulatory shifts include stricter extended producer responsibility pilots and recycled-content procurement mandates in several U.S. states, prompting converters to target 20–30% PCR integration in flexible protective films. Technological changes include roll-to-roll inline printing, high-speed automated dunnage systems, and sensor-enabled cushion monitoring that reduced packing cycle times by an average 18% in pilot deployments. Local players expanded service models: a major US converter launched an on-site bagging-as-a-service program in 2024, offering per-parcel pricing and automated replenishment tied to warehouse WMS. Regional consumer behavior shows higher preference for branded protective packaging (31% of consumers recognize branded mailer protection), and B2B buyers increasingly demand product-protection KPIs like <0.5% transit damage rate for high-value items.

Are regulatory pressures and closed-loop initiatives accelerating recyclable protective film adoption?

Europe held ~26% of global protective plastic packaging volumes in 2024 with leading markets in Germany, UK, and France cumulatively accounting for roughly 58% of regional demand. Market characteristics include high adoption of recyclable mono-material films and an average PCR content target of 15–25% across large converters. Regulatory frameworks and sustainability initiatives—EPR pilots, recyclability labelling, and national circular packaging targets—drove retrofit investments: converters deployed over 120 new film-recycling lines in 2023–2024, increasing throughput capacity by ~210 kt/year. Emerging tech adoption includes solvent-free lamination and digital inkjet variable labelling that reduced SKU changeover times by 24%. A notable local player scaled a mono-polymer cushioning range across 8 EU distribution centres in 2024, improving return-to-recycle capture rates by an estimated 30%. Regional consumer behavior favors clear recyclability claims (52% of respondents in procurement surveys prioritized recycle-ready packs), and industrial buyers prioritize certified chain-of-custody for PCR content.

How are e-commerce volumes and local film production capacity driving Asia-Pacific demand?

Asia-Pacific ranked second by volume in 2024 with ~28% of global protective plastic packaging output and consolidated film extrusion capacity of approximately 1,900 kt/year concentrated in China, India, and Japan. Top consuming countries: China (largest single-country volume at ~2,900 kt), India (~620 kt), Japan (~420 kt). Infrastructure trends show rapid expansion of regional converting hubs—more than 75 new converting lines were commissioned in 2023–2024 focused on high-speed air cushion, void-fill and protective wrap. Regional tech clusters in Shenzhen and Osaka accelerated automation adoption: pick-and-pack stations integrated inline void-fill systems, cutting packing labour time by 20–25% per order. A significant local player introduced low-gauge, high-strength LDPE protective film in 2024, enabling a 12% material saving per parcel. Consumer behaviour: rapid growth of mobile commerce pushed per-order protective material use up 29% year-over-year in select urban centers; B2B buyers increasingly demand localized lead times under 7 days to support fast replenishment.

Can localized manufacturing and trade policies unlock scale for protective packaging in LATAM?

South America’s protective plastic packaging market in 2024 accounted for roughly 6–8% of global volume with Brazil and Argentina as principal demand centers; Brazil contributed ~55% of regional volume with estimated 260–320 kt usage. Infrastructure constraints and logistics fragmentation lead to higher per-unit protective material usage (average 0.68 kg per parcel versus global 0.57 kg), driven by longer transit routes and mixed modal handling. Government incentives for local manufacturers—including duty reductions on converting machinery and targeted trade facilitation—enabled three major converters to increase domestic film production capacity by an estimated 45 kt/year in 2023–2024. A regional player piloted a collection-for-recycling program across 120 retail points in 2024, capturing ~1,200 tonnes of post-consumer protective film. Consumer behaviour in South America demonstrates strong demand for bilingual packaging instructions and localized labeling, influencing converter run-length decisions and SKU rationalization.

Is strategic industrialization and logistics modernization supporting protective packaging demand in MEA?

Middle East & Africa recorded ~5% of global protective plastic packaging volume in 2024 with notable activity in UAE, South Africa, and Saudi Arabia. Regional demand trends are linked to construction components export, oil & gas spare parts shipment, and growing e-commerce logistics nodes. Major growth countries such as UAE and South Africa scaled protective film imports to support re-export logistics, with warehouse automated packing lifts and air-cushion systems introduced at 12 new fulfilment sites in 2023–2024. Technological modernization includes adoption of solar-backed warehouse systems and hybrid air-less cushioning solutions optimized for arid climates—these reduced per-package material weight by ~9% in pilots. Local trade partnerships and free-zone logistics incentives attracted three international converters to set up regional service centres, shortening lead times from 21 to 7 days for major account customers. Consumer behaviour shows a rising preference for climate-robust protective solutions and extended-warranty packaging offers.

China — 18% market share. High production capacity with extensive film extrusion and converting assets supporting vast e-commerce fulfillment and intermodal logistics.

United States — 16% market share. Strong end-user demand from parcel logistics, medical device shipping, and industrial parts sectors; advanced automation adoption and short lead-time supply chains.

The Protective Plastic Packaging Market is moderately consolidated at the top with a fragmented long tail of regional converters and niche suppliers. As of 2024, there are an estimated 420–520 active global competitors ranging from global integrated producers to regional converting specialists; the combined share of the top five companies is approximately 42–48%, reflecting concentrated leadership in advanced cushioning, film innovation, and integrated supply solutions. Strategic initiatives in 2023–2024 included 18 major partnerships for circularity programs, 12 product launches focused on mono-material recyclable films, and 9 capacity expansions for high-speed air-cushion lines. M&A activity accelerated around niche sustainable-material players and recycled-content feedstock providers, with at least seven announced acquisitions or minority investments during 2023–2024. Innovation trends shaping positioning include digital product-protection monitoring, smart dunnage with embedded sensors, and automated right-sizing film systems—pilots reported 15–25% reductions in transit damage claims for participating retailers. Pricing pressures from feedstock volatility led mid-tier converters to hedge polymer supply contracts covering 60–80% of expected 12-month needs. Overall, the competitive landscape favours companies that can combine scale, sustainability credentials, and integrated logistics services.

Berry Global

Storopack

Mondi

Sonoco Products Company

Huhtamaki

Klöckner Pentaplast (KPR)

Winpak Ltd.

Constantia Flexibles

NOVA Chemicals

Sigma Plastics Group

RPC / Packaging (independent converters)

Technological developments in protective plastic packaging in 2023–2024 concentrated on three pillars: material circularity, automation-enabled accuracy, and intelligent protection. Material circularity progressed via mono-polymer film systems, PCR incorporation, and chemical-reclaim pilot lines; leading converters reported PCR procurement accounting for 18–30% of flexible film feedstock in contract portfolios during 2024. Automation advanced through inline dispensing and right-sizing algorithms that assess parcel geometry to allocate void-fill and film usage—these systems reduced material waste by 12–22% in high-throughput operations. Intelligent protection technologies combined accelerometer/logistics sensors embedded in dunnage with cloud analytics, enabling shipper-level visibility and reducing disputed transit damage claims by 9–15% during field pilots. Manufacturing innovations included thinner-gauge, high-tensile LDPE blends and oriented PP laminates that deliver equivalent puncture resistance at 8–14% lower gram weights; adoption of ultrasonic welding and solvent-free lamination improved production cycle times by 10–18% while reducing VOC emissions. Digital transformation efforts saw 68% of top-tier converters integrate ERP-to-WMS automated replenishment and 42% connect protective-material consumption to customer-facing reporting dashboards for TCO transparency. On sustainability tech, enzymatic and advanced solvent separation trials scaled sampling lines to 1–3 tonne/day capacity in 2024 pilot plants, targeting economically viable reclaimed feedstock. Finally, packaging-as-a-service (PaaS) models expanded, bundling protective materials, automated dispensing hardware, and performance SLAs—pilots show average KPI improvements of same-day order fill rates (+21%) and a 14% reduction in packing labor for adopters.

• In April 2024, Amcor and Kimberly-Clark launched Huggies Eco Protect diaper packaging with 30% post-consumer recycled content for Peru shipments; the new bags integrate PCR film while retaining barrier and visual performance. Source: amcor.com

• In February 2024, Berry Global opened a circular innovation centre in Tulsa, Oklahoma focused on stretch-film circularity and workforce training; the centre supports development of recyclable, mechanically recycled films and operator upskilling. Source: packagingdive.com

• In January 2024, Storopack announced sustainability upgrades to its air cushion portfolio, deploying new formulations and recycling-ready materials across its European and APAC lines, improving recyclability and reducing material weight per cushion by double-digit percentages in pilot runs. Source: storopack.in

• In November 2024, Pregis showcased IntelliPack foam-in-place innovations and expanded IntelliPack automation at PACK EXPO 2024, highlighting on-demand foam solutions and new film offerings intended to improve protective performance while enabling social-impact film options. Source: pregis.com

The Protective Plastic Packaging Market Report covers product categories including air cushions, inflatable dunnage, foam-in-place, corrugated liners with polymer coatings, stretch and protective film, bubble technologies, edge protectors, and biodegradable/chemically recyclable film variants. Geographic scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level benchmarks for production capacity (kt/year), converter throughput, and regional consumption per parcel metrics. Application coverage addresses e-commerce and parcel logistics, consumer electronics protection, medical device transit and sterilization-ready protective wraps, automotive parts protection, industrial machinery shipment protection, and retail reverse-logistics packaging. Technology assessment includes extrusion and co-extrusion film platforms, mono-polymer recyclable solutions, foam chemistries for on-demand cushioning, ultrasonic welding, solvent-free lamination, and embedded sensor dunnage. Operational focus areas examine automation adoption in fulfilment centres, right-sizing algorithms, inline quality inspection, and packaging-as-a-service commercial models. Sustainability and regulatory lenses evaluate PCR integration, closed-loop collection pilots, EPR impacts, and design-for-recyclability strategies. The report additionally analyzes vendor strategies (product launches, mergers, capacity expansions), procurement and sourcing trends (PCR purchasing volumes and contractual hedging), and commercial KPIs (transit damage rates, material usage per parcel, lead-time reductions). Niche and emerging segments are profiled—e.g., compostable protective films for regulated medical waste streams, enzymatically recyclable barrier films, and smart-protection solutions with telemetry—providing decision-makers with actionable roadmaps for investment, procurement, and operational transformation across short and medium planning horizons.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 19,497.3 Million |

|

Market Revenue in 2032 |

USD 30,149.9 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sealed Air, Amcor, Pregis, Berry Global, Storopack, Mondi, Sonoco Products Company, Huhtamaki, Klöckner Pentaplast (KPR), Winpak Ltd., Constantia Flexibles, NOVA Chemicals, Sigma Plastics Group, RPC / Packaging |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |