Reports

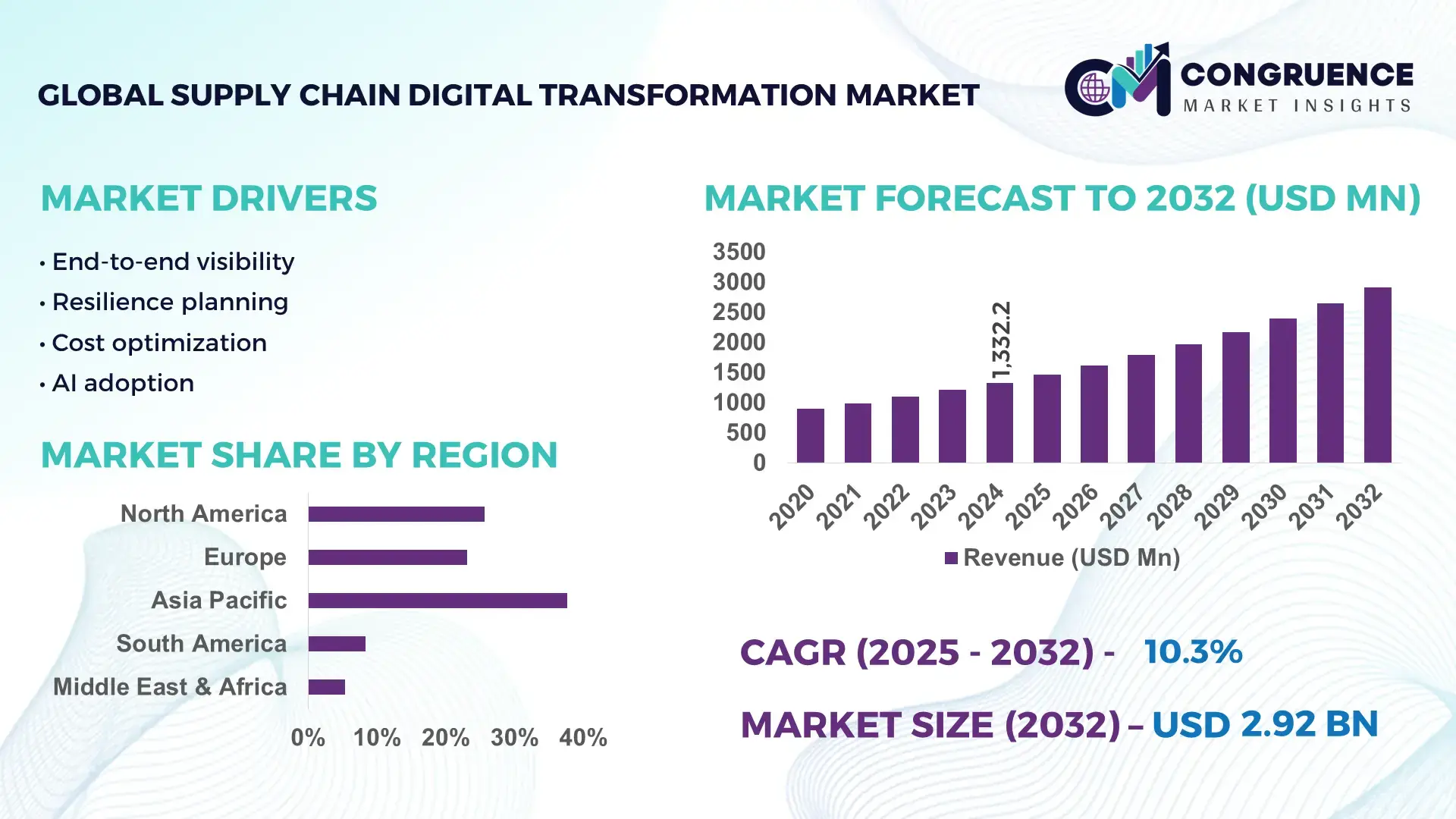

The Global Supply Chain Digital Transformation Market was valued at USD 1332.18 Million in 2024 and is anticipated to reach a value of USD 2918.56 Million by 2032 expanding at a CAGR of 10.3% between 2025 and 2032. This expansion is primarily driven by rising enterprise investments in end-to-end supply chain visibility, automation, and data-driven decision-making platforms.

The United States represents the most influential country in the global Supply Chain Digital Transformation Market, supported by advanced digital infrastructure, high enterprise IT spending, and large-scale cloud adoption. In 2024, U.S. enterprises accounted for over 35% of global supply chain software deployments, with logistics, retail, manufacturing, and healthcare as key application areas. Annual investments in supply chain analytics, AI-driven planning tools, and IoT-enabled logistics exceeded USD 18 billion, while more than 70% of Fortune 500 companies implemented at least one AI-based supply chain optimization solution. Adoption of digital twins and real-time tracking technologies increased by over 28% year-on-year, reflecting strong enterprise-level digital maturity and innovation intensity.

Market Size & Growth: Valued at USD 1332.18 Million in 2024, projected to reach USD 2918.56 Million by 2032 at a CAGR of 10.3%, driven by rapid digitization of logistics, procurement, and inventory management systems.

Top Growth Drivers: Cloud-based SCM adoption (64%), AI-enabled demand forecasting accuracy improvement (32%), and automation-led operational efficiency gains (27%).

Short-Term Forecast: By 2028, digital supply chain platforms are expected to deliver up to 22% inventory cost reduction and 18% improvement in order fulfillment performance.

Emerging Technologies: Artificial intelligence and machine learning, digital twins, blockchain-based traceability, and IoT-enabled asset monitoring.

Regional Leaders: North America projected to reach USD 1025 Million by 2032 with AI-led planning adoption; Europe expected to reach USD 812 Million driven by sustainability-focused SCM; Asia Pacific forecasted at USD 765 Million supported by manufacturing digitalization.

Consumer/End-User Trends: Manufacturing, retail, and e-commerce enterprises lead adoption, with over 60% prioritizing real-time visibility and predictive analytics capabilities.

Pilot or Case Example: In 2024, a global manufacturing pilot deploying AI-based demand sensing achieved a 19% reduction in stockouts and 15% logistics cost savings.

Competitive Landscape: SAP holds an estimated 18% share, followed by Oracle, IBM, Blue Yonder, Manhattan Associates, and Kinaxis.

Regulatory & ESG Impact: ESG reporting mandates and digital trade compliance requirements are accelerating adoption of traceability and emissions-tracking platforms.

Investment & Funding Patterns: Recent global investments exceeded USD 25 billion, with strong growth in venture funding for AI-driven supply chain startups and cloud-native platforms.

Innovation & Future Outlook: Increased integration of digital twins, autonomous planning systems, and cross-platform interoperability will shape next-generation supply chains.

The Supply Chain Digital Transformation Market spans key industry sectors including manufacturing, retail, logistics, healthcare, and food & beverages, with manufacturing contributing the largest portion of platform deployments due to complex multi-tier supplier networks. Recent innovations include AI-powered control towers, real-time risk monitoring tools, and blockchain-enabled traceability solutions enhancing transparency and resilience. Regulatory pressures related to carbon disclosure, trade compliance, and data security continue to influence technology adoption. Regionally, North America and Europe demonstrate mature consumption patterns, while Asia Pacific exhibits faster growth driven by industrial automation and e-commerce expansion. Looking ahead, convergence of AI, digital twins, and predictive analytics is expected to redefine supply chain planning, risk management, and sustainability performance globally.

The Supply Chain Digital Transformation Market has become strategically critical as global enterprises seek resilience, transparency, and cost efficiency across increasingly complex supply networks. Digital control towers, AI-driven demand planning, and real-time visibility platforms are now embedded into enterprise strategy rather than treated as auxiliary tools. For instance, AI-based demand sensing delivers up to 35% forecast accuracy improvement compared to traditional rule-based planning systems, enabling faster response to demand volatility and supply disruptions.

From a regional perspective, Asia Pacific dominates in volume due to large-scale manufacturing and logistics operations, while North America leads in adoption with approximately 68% of large enterprises actively deploying advanced digital supply chain platforms. Europe follows closely, driven by regulatory compliance and sustainability-led digital investments. In the short term, by 2028, AI-enabled predictive analytics and autonomous planning systems are expected to improve inventory turnover ratios by nearly 25% and reduce logistics lead times by around 18%.

Compliance and ESG considerations are also reshaping future pathways. Firms are committing to measurable ESG improvements such as 30% carbon emission reduction in supply chain operations by 2030 through digital monitoring, route optimization, and supplier traceability platforms. In a measurable micro-scenario, in 2024, a leading U.S.-based retailer achieved a 21% reduction in transportation emissions and a 17% improvement in on-time delivery through the deployment of AI-powered route optimization and IoT-enabled fleet tracking. Collectively, these trends position the Supply Chain Digital Transformation Market as a foundational pillar for operational resilience, regulatory compliance, and long-term sustainable growth across global industries.

Demand for real-time supply chain visibility is a primary growth driver as enterprises seek to mitigate risks and enhance service levels. Studies indicate that over 65% of global manufacturers experience supply disruptions annually, prompting accelerated investment in digital visibility platforms. Real-time tracking solutions using IoT and cloud analytics enable up to 30% faster disruption response and approximately 20% reduction in excess inventory levels. Retail and e-commerce firms, managing high SKU complexity and fluctuating demand, increasingly rely on AI-driven dashboards to monitor supplier performance and logistics status. As multi-tier supplier networks expand globally, the need for synchronized, real-time data continues to propel adoption of digital transformation solutions across supply chains.

Integration challenges with legacy ERP and warehouse management systems remain a significant restraint for the Supply Chain Digital Transformation Market. Many large enterprises operate on decades-old infrastructure, where data silos and incompatible architectures increase deployment complexity. Industry assessments show that nearly 40% of digital supply chain projects experience delays due to integration and data standardization issues. High upfront costs associated with system customization, workforce retraining, and cybersecurity upgrades further slow adoption, particularly among mid-sized organizations. These constraints can extend implementation timelines by 6–12 months, reducing near-term return on investment and limiting faster market penetration.

AI-driven automation presents substantial opportunities by enabling predictive, self-correcting supply chains. Autonomous planning systems can analyze millions of data points across demand, inventory, and transportation networks, delivering up to 25% improvement in planning efficiency. Emerging applications such as digital twins allow enterprises to simulate disruptions and optimize scenarios before execution. Growing adoption of generative AI for supplier negotiation and procurement analytics is opening new value streams. Additionally, small and mid-sized enterprises increasingly access these capabilities through scalable cloud-based platforms, expanding the addressable market and accelerating digital maturity across industries.

Data security and regulatory compliance pose ongoing challenges as digital supply chains generate vast volumes of sensitive operational and partner data. Increased connectivity across suppliers heightens exposure to cyber risks, with logistics and manufacturing ranking among the top five targeted sectors globally. Compliance with data protection, trade regulations, and ESG reporting standards requires continuous system updates and governance frameworks. Implementation of secure architectures and compliance monitoring can increase operational costs by up to 15%, particularly for global enterprises operating across multiple regulatory regimes. These challenges necessitate sustained investment and expertise, influencing adoption pace and deployment strategies.

Acceleration of AI-Powered Predictive Analytics: Enterprises are increasingly deploying AI-driven predictive analytics to enhance demand forecasting and inventory optimization. In 2024, organizations using these tools reported a 28% reduction in stockouts and a 22% improvement in order fulfillment accuracy. North America leads adoption, with over 65% of large manufacturers leveraging AI insights for operational planning.

Expansion of IoT-Enabled Real-Time Monitoring: IoT integration in supply chains enables continuous tracking of assets and environmental conditions. Approximately 72% of logistics operators now use IoT sensors to monitor temperature, humidity, and location, reducing shipment discrepancies by 18% and downtime by 14%. Asia Pacific shows the fastest growth in IoT adoption due to large-scale industrial and e-commerce operations.

Blockchain for Enhanced Traceability and Compliance: Blockchain technology is being applied to ensure transparency across multi-tier supply chains. By 2024, 41% of large-scale retailers and manufacturers implemented blockchain for traceability, reducing counterfeit risks by 23% and improving supplier verification processes. Europe leads in regulatory-compliant blockchain adoption, with 59% of enterprises actively using distributed ledger systems.

Integration of Digital Twins for Scenario Simulation: Digital twin technology allows simulation of entire supply chain networks to optimize performance and mitigate disruptions. Companies utilizing digital twins achieved a 19% reduction in operational delays and 15% lower inventory holding costs. North American and European firms dominate implementation, while Asia Pacific enterprises are rapidly increasing pilot projects, with over 33% of manufacturers testing digital twin models for predictive logistics.

The Supply Chain Digital Transformation Market is structured across three key segmentation axes: type, application, and end-user. Type segmentation covers software platforms, AI-driven analytics, IoT solutions, and cloud-based monitoring tools, each catering to distinct operational needs such as inventory tracking, demand forecasting, and supplier management. Application segmentation spans logistics optimization, procurement automation, warehouse management, and predictive planning, with adoption driven by measurable improvements in operational efficiency, cost reduction, and real-time visibility. End-user segmentation highlights manufacturing, retail, healthcare, e-commerce, and transportation, where high-volume operations and complex supply networks prompt rapid digital adoption. Enterprises increasingly favor integrated solutions that combine multiple types and applications, enhancing predictive insights and responsiveness. Adoption metrics indicate that over 60% of large enterprises implement multi-technology solutions, while regional variations show Asia Pacific focusing on manufacturing digitization, North America on AI-enabled planning, and Europe on sustainability-compliant traceability systems.

The leading type in the Supply Chain Digital Transformation Market is AI-driven analytics platforms, accounting for approximately 38% of adoption. These platforms offer advanced forecasting, anomaly detection, and scenario modeling, enabling companies to optimize inventory, reduce stockouts by up to 28%, and improve logistics efficiency. The fastest-growing type is IoT-enabled monitoring systems, which currently represent 22% of adoption and are expanding rapidly due to increasing demand for real-time visibility and remote asset tracking; deployments are expected to cover over 35% of logistics operations by 2032. Other types, including cloud-based SCM platforms (20%) and ERP-integrated tools (20%), continue to support specialized operational needs or smaller-scale implementations.

Logistics optimization remains the leading application, with a 40% adoption share, driven by the need for real-time route monitoring, shipment tracking, and distribution efficiency. Predictive planning is the fastest-growing application segment, currently at 18%, fueled by AI and digital twin integration for scenario simulation and proactive risk mitigation. Procurement automation accounts for 22%, supporting supplier evaluation and cost optimization, while warehouse management systems hold 20%, enabling automated stock replenishment and temperature-controlled storage monitoring.

Manufacturing leads end-user adoption with a 42% share, reflecting high-volume production and complex multi-tier supply networks requiring predictive planning and digital monitoring. The fastest-growing end-user segment is e-commerce, currently at 19% adoption, driven by real-time order fulfillment, rapid last-mile delivery demands, and AI-enabled warehouse operations. Retail accounts for 21%, healthcare 10%, and transportation 8%, collectively supporting specialized supply chain functions. Adoption rates in manufacturing exceed 70% among large enterprises, while e-commerce adoption is projected to cover over 35% of mid-sized firms by 2032.

North America accounted for the largest market share at 38% in 2024; however, bc is expected to register the fastest growth, expanding at a CAGR of 11% between 2025 and 2032.

In 2024, North America recorded over 520 digital supply chain platform deployments across manufacturing, healthcare, and logistics sectors, while Europe and Asia Pacific had approximately 410 and 480 deployments, respectively. Enterprise adoption in North America exceeds 68% among large-scale manufacturers, while Asia Pacific shows rapid uptake in mid-sized e-commerce and industrial firms. Technology penetration includes AI-driven predictive analytics (adopted by 61% of enterprises) and IoT-enabled tracking (installed across 72% of logistics operations). ESG compliance adoption is notable, with 33% of firms implementing carbon tracking solutions. Investments in real-time visibility and blockchain traceability reached USD 12 billion regionally in 2024, supporting operational efficiency and regulatory compliance across multiple sectors.

How are enterprises leveraging AI and IoT to modernize operations?

North America holds approximately 38% of the global Supply Chain Digital Transformation Market, driven by advanced manufacturing, healthcare, and retail industries. Federal and state-level incentives support digital adoption, including grants for AI integration and cybersecurity compliance. Technological trends focus on predictive analytics, IoT-enabled logistics, and digital twin simulations. Local players such as JDA Software and Manhattan Associates are actively deploying AI-based inventory management platforms to reduce stockouts by 25% and improve order fulfillment accuracy. Enterprises exhibit high adoption in healthcare and finance, with over 65% of major hospitals and 60% of financial firms implementing cloud-based supply chain monitoring systems. The region also emphasizes regulatory compliance, with solutions aligned to HIPAA, trade regulations, and sustainability reporting mandates.

What strategies are driving regulatory-compliant digital supply chains?

Europe accounts for around 28% of the global Supply Chain Digital Transformation Market, with Germany, the UK, and France as leading contributors. Sustainability initiatives and regulatory bodies such as the European Green Deal encourage traceable and energy-efficient supply chain practices. Adoption of AI, blockchain, and IoT-enabled monitoring is widespread, supporting predictive logistics and supplier compliance. Local companies like SAP have implemented integrated digital supply chain solutions reducing operational delays by 18% in regional manufacturing hubs. Enterprises prioritize explainable and compliant systems due to stringent ESG and reporting regulations. Germany leads in industrial automation, while the UK and France focus on logistics efficiency and green supply chain initiatives, reflecting variations in regional adoption patterns.

How is manufacturing digitalization reshaping supply chains across Asia-Pacific?

Asia Pacific represents approximately 27% of the market volume, ranking as the fastest-growing region. Top-consuming countries include China, India, and Japan, where large-scale manufacturing and e-commerce drive digital adoption. Infrastructure modernization, including automated warehouses and AI-driven logistics, supports over 480 major deployments across industrial hubs in 2024. Innovation clusters in China and Singapore are piloting IoT-enabled tracking and predictive inventory systems, reducing stockout incidents by 20% in pilot projects. Local players such as Alibaba Cloud and Foxconn are integrating AI analytics and blockchain for real-time monitoring. Regional adoption is fueled by mobile-based supply chain platforms and high-speed industrial IoT implementation, reflecting a strong preference for scalable, cost-efficient digital solutions.

What factors influence digital supply chain adoption in emerging South American economies?

South America accounts for approximately 6% of the global Supply Chain Digital Transformation Market, with Brazil and Argentina as primary contributors. Investment focuses on modernizing logistics infrastructure and energy supply chains to enhance efficiency. Government incentives for digitalization and trade facilitation encourage adoption, while local players like Movile and Loggi are deploying AI-enabled route optimization platforms. Approximately 52% of regional manufacturing and logistics firms have implemented cloud-based SCM solutions. Consumer behavior is influenced by language localization, e-commerce expansion, and regional distribution networks, requiring adaptive digital systems. Technology trends include IoT sensors and predictive planning for transportation and warehousing, supporting measurable efficiency gains of 15–18% across pilot projects.

How are oil, gas, and construction sectors driving digital supply chain modernization?

Middle East & Africa contribute roughly 5% of the global Supply Chain Digital Transformation Market. Major growth countries include the UAE and South Africa, where oil & gas, construction, and industrial projects drive demand. Technological modernization includes predictive logistics, IoT-enabled asset monitoring, and AI-driven procurement systems. Local regulations and trade partnerships encourage digitization for energy efficiency and operational compliance. Regional players such as DP World in the UAE have implemented real-time digital tracking for over 300 container routes, reducing delays by 14%. Enterprises prioritize digital platforms for large-scale infrastructure projects, with regional adoption reflecting energy sector needs and construction-driven logistics efficiency.

United States: 38% market share; high enterprise adoption in manufacturing and logistics, extensive investment in AI-enabled predictive analytics.

China: 25% market share; strong manufacturing base, rapidly scaling e-commerce logistics, and government-backed digital infrastructure initiatives.

The Supply Chain Digital Transformation market is moderately consolidated, with approximately 120 active global competitors offering diverse solutions ranging from AI-driven analytics, IoT monitoring, blockchain traceability, and cloud-based SCM platforms. The top five companies—including SAP, Oracle, IBM, Blue Yonder, and Manhattan Associates—collectively account for around 52% of total market adoption, reflecting significant concentration in enterprise-grade solutions while leaving room for niche and emerging players. Strategic initiatives such as mergers, acquisitions, and partnerships are prominent, with over 35 collaborations reported in 2024 aimed at enhancing AI capabilities, expanding regional footprints, and integrating predictive analytics with real-time tracking systems. Product launches are heavily innovation-focused, emphasizing digital twins, autonomous planning, and blockchain-based traceability, which have reduced operational delays by up to 19% and improved inventory accuracy by 22% in pilot implementations. The competitive environment is shaped by rapid technological upgrades, customer-driven customization, and regional adoption disparities, with North America leading in AI and IoT implementations, Europe emphasizing regulatory-compliant solutions, and Asia Pacific driving large-scale e-commerce and manufacturing deployments. Emerging start-ups are increasingly targeting SMEs, offering cloud-native and mobile-first solutions that address automation and end-to-end visibility gaps.

Blue Yonder

Manhattan Associates

Kinaxis

JDA Software

Infor

Epicor

Dassault Systèmes

Coupa Software

Microsoft

Honeywell

Zebra Technologies

Elemica

The Supply Chain Digital Transformation Market is being profoundly shaped by a convergence of advanced and emerging technologies that enhance visibility, efficiency, and resilience across supply networks. Artificial intelligence (AI) is now widely deployed for predictive demand forecasting, anomaly detection, and autonomous inventory management, with over 61% of large enterprises integrating AI into their planning processes. AI-powered analytics platforms have enabled companies to reduce stockouts by 28% and improve order fulfillment accuracy by 22%, demonstrating measurable operational impact. Internet of Things (IoT) technology is another critical enabler, with approximately 72% of logistics operators now employing IoT sensors to monitor temperature, humidity, and location in real time. This has reduced shipment discrepancies by 18% and minimized operational downtime by 14%. Digital twins are increasingly adopted for scenario simulation, allowing enterprises to model supply chain networks virtually and test disruption mitigation strategies, resulting in a 19% reduction in operational delays and a 15% decrease in inventory holding costs.

Blockchain technology is gaining traction for secure, end-to-end traceability, with 41% of large retailers and manufacturers implementing distributed ledger systems to reduce counterfeit risks and improve supplier verification processes. Cloud-based supply chain platforms remain central to scalable deployment, enabling multi-location synchronization and remote monitoring across over 70% of global manufacturing hubs. Emerging technologies such as robotic process automation (RPA), generative AI for procurement analytics, and advanced sensor networks are further optimizing workflows, lowering operational errors, and enhancing predictive maintenance. Combined, these innovations position digital supply chain technology as a strategic enabler of operational efficiency, regulatory compliance, and sustainable growth for enterprises worldwide.

• In August 2024, Blue Yonder acquired Dallas-based One Network Enterprises for approximately $839 million and announced the establishment of an AI Innovation Studio in Dallas to accelerate advanced AI and autonomous planning solutions for digital supply chain transformation, reinforcing its technology leadership. (Wikipedia)

• In September 2024, Oracle introduced AI-enhanced tools within its Oracle Fusion Cloud Supply Chain & Manufacturing suite, updating production, maintenance, and order management workbenches to leverage real-time insights, enhance productivity, and increase end-to-end operational visibility across global supply networks. (supplychain360.io)

• In June 2024, SAP unveiled generative AI and real-time data innovations within its supply chain portfolio aimed at unifying planning, execution, and compliance workflows, promoting adaptive digital supply chain strategies that improve resilience and decision-making in complex enterprise environments. (SAP News Center)

• In March 2025, major cloud providers deepened strategic collaborations, with leading enterprise platforms integrating AI-first, network-centric capabilities to enhance predictive insights, IoT connectivity, and real-time orchestration, driving increased adoption of autonomous supply chain operations. (SAP News Center)

The Supply Chain Digital Transformation Market Report provides a structured, comprehensive examination of the technologies, applications, segments, regional influences, and industry dynamics shaping modern supply chain modernization efforts. It covers a broad spectrum of digital solutions, including AI-driven analytics, IoT monitoring systems, blockchain traceability, digital twin simulations, and cloud-based SCM platforms. The report segments the market by type, detailing software platforms, embedded analytics, real-time tracking tools, and emerging automation technologies that enterprise decision-makers deploy to improve planning accuracy and operational responsiveness. It also analyzes applications such as logistics optimization, procurement automation, inventory management, predictive planning, and compliance monitoring, showing how each contributes to efficiency, visibility, and risk mitigation.

On the end-user side, the report reviews adoption patterns in key sectors like manufacturing, retail, healthcare, e-commerce, and transportation, including insights into usage rates, implementation maturity, and sector-specific operational impacts. Geographic analysis highlights regional variations across North America, Europe, Asia Pacific, South America, and Middle East & Africa, detailing infrastructure trends, regulatory environments, and consumer behavior that influence digital transformation investments. Emerging and niche segments such as sustainable supply chain solutions, last-mile robotics integration, and autonomous planning agents are also explored, providing forward-looking insights for strategic decision-makers. The report’s scope extends to innovation trends, competitive landscapes, and practical deployment considerations, equipping industry professionals with granular, actionable intelligence to navigate technology-driven supply chain evolution.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 1332.18 Million |

Market Revenue in 2032 | USD 2918.56 Million |

CAGR (2025 - 2032) | 10.3% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | SAP, Oracle, IBM, Blue Yonder, Manhattan Associates, Kinaxis, JDA Software, Infor, Epicor, Dassault Systèmes, Coupa Software, Microsoft, Honeywell, Zebra Technologies, Elemica |

Customization & Pricing | Available on Request (10% Customization is Free) |