Reports

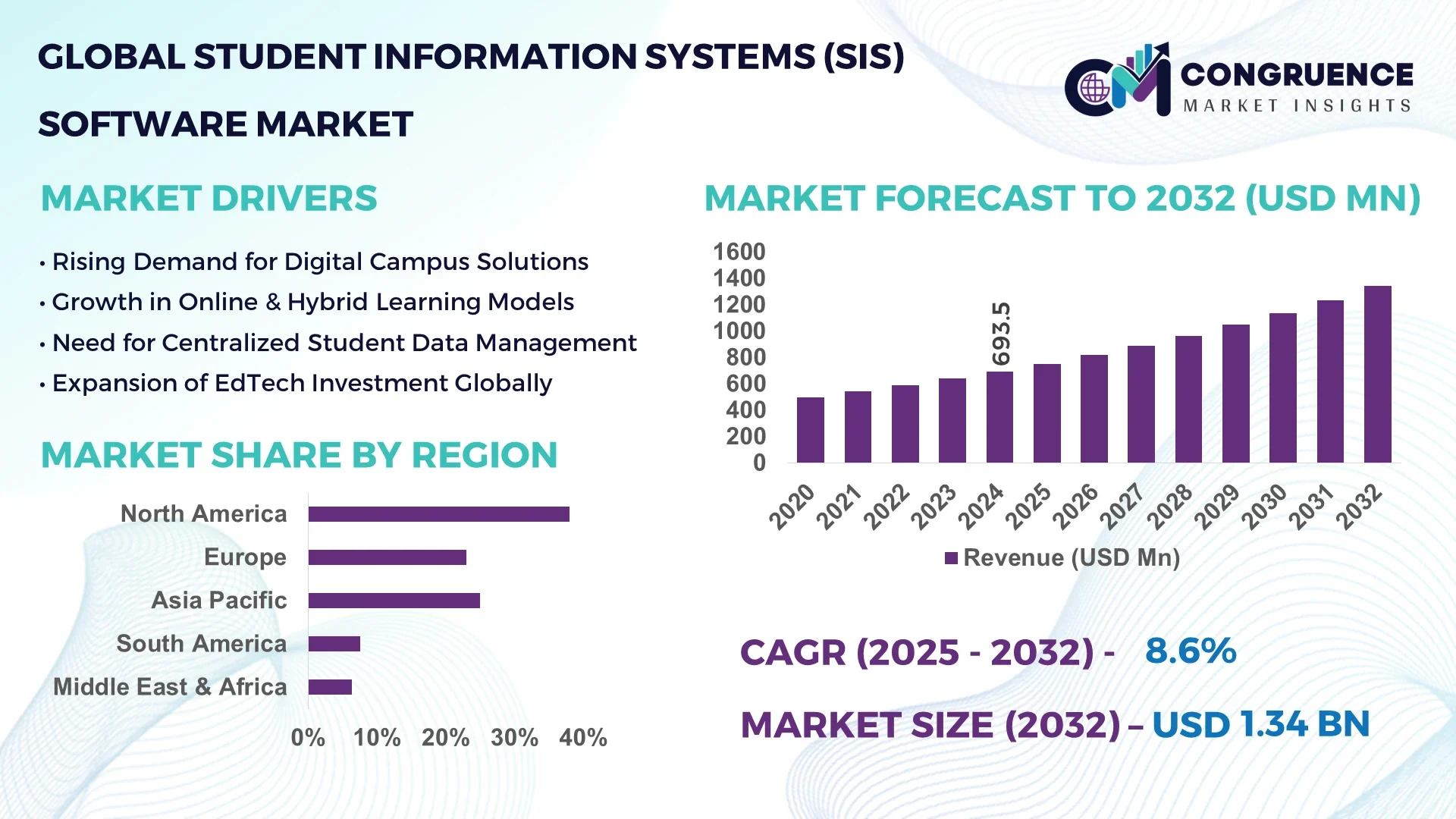

The Global Student Information Systems (SIS) Software Market was valued at USD 693.48 Million in 2024 and is anticipated to reach a value of USD 1341.76 Million by 2032 expanding at a CAGR of 8.6% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

The United States leads the global SIS software market with significant investments in cloud-based education technologies and extensive integration of digital platforms across K-12 and higher education institutions. The country exhibits advanced production capacities for scalable SIS solutions, supported by continuous government and private sector funding focused on enhancing educational data management and security protocols.

The Student Information Systems (SIS) Software market is primarily driven by the increasing adoption across various education sectors including K-12 schools, universities, and vocational training centers. Key industry sectors contribute diversely, with higher education institutions showing substantial demand for features like student lifecycle management, online registration, and analytics-enabled performance tracking. Recent technological innovations such as AI-powered automation, cloud migration, and mobile accessibility are transforming user experience and operational efficiency. Regulatory frameworks emphasizing data privacy and student information security are prompting vendors to develop compliance-focused software solutions. Additionally, economic factors like increased digital education budgets in emerging regions are fueling market expansion. Regional consumption patterns reveal rapid growth in Asia-Pacific and Europe, driven by government digital initiatives and rising smartphone penetration. Emerging trends such as personalized learning analytics and integrated communication tools forecast a robust future outlook, positioning the market for sustainable growth and continuous innovation.

Artificial Intelligence (AI) is revolutionizing the Student Information Systems (SIS) Software Market by significantly enhancing operational efficiencies and decision-making capabilities. AI integration enables real-time data processing and intelligent automation of routine administrative tasks such as attendance tracking, grading, and student performance analysis, which reduces manual errors and accelerates workflows. Advanced machine learning algorithms empower SIS platforms to offer predictive analytics, providing educators and administrators with actionable insights to identify at-risk students and personalize academic interventions effectively. AI-powered chatbots and virtual assistants are also streamlining student support services, improving responsiveness while reducing institutional workload.

In addition, natural language processing (NLP) technologies within SIS software enhance communication by facilitating automated messaging and feedback tailored to individual students and parents. AI-driven analytics support resource optimization in areas like class scheduling, enrollment forecasting, and faculty allocation, resulting in cost savings and improved institutional planning. Moreover, AI enables dynamic content management systems that adapt learning materials based on student progress and engagement levels. The deployment of AI within the Student Information Systems (SIS) Software Market is not only boosting productivity but also fostering data-driven, personalized educational environments. These advancements underscore the critical role AI plays in transforming traditional education management systems into smart, adaptive platforms that meet evolving institutional demands.

“In 2024, a leading SIS software provider launched an AI-enhanced module capable of reducing administrative processing time by 40%, while improving student data accuracy through automated anomaly detection algorithms applied across millions of records in real-time.”

The rising adoption of cloud-based Student Information Systems (SIS) Software significantly propels market growth by offering flexible, scalable, and cost-efficient solutions. Educational institutions, especially in higher education and K-12 sectors, prefer cloud SIS for its ability to facilitate seamless data access, reduce IT infrastructure costs, and support remote learning environments. Cloud deployment enables automatic updates and real-time data synchronization across multiple campuses, improving administrative efficiency and user experience. Moreover, the scalability of cloud-based SIS accommodates fluctuating enrollment sizes, making it attractive to both small schools and large universities. This shift toward cloud-centric platforms is driven by increased internet penetration and growing investments in digital education infrastructure worldwide, thus reinforcing the Student Information Systems (SIS) Software market expansion.

Concerns related to data security and privacy regulations pose significant restraints on the Student Information Systems (SIS) Software market. Educational institutions manage sensitive student data, including personal identification and academic records, making them prime targets for cyberattacks. Ensuring compliance with stringent data protection laws such as FERPA in the U.S. and GDPR in Europe requires continuous investment in robust security frameworks. Many institutions face challenges implementing these protections due to limited IT resources and expertise. Additionally, apprehensions about data breaches and unauthorized access may delay SIS adoption or limit the deployment of cloud-based solutions, thereby affecting market growth. The evolving regulatory landscape necessitates ongoing updates to SIS software, which can increase development costs and complexity.

The growing demand for mobile-accessible Student Information Systems (SIS) presents a significant opportunity for market players. With increasing smartphone penetration and the rise of remote and hybrid learning models, stakeholders are seeking SIS solutions that offer seamless mobile interfaces for students, educators, and parents. Mobile accessibility facilitates real-time communication, instant access to academic records, attendance, and assignment submissions, enhancing user engagement and satisfaction. The integration of mobile apps with SIS platforms also supports notifications, alerts, and personalized learning resources, creating an interactive educational environment. This trend opens new avenues for software developers to innovate and tailor solutions that cater to the evolving preferences of digital-native users, driving further growth within the Student Information Systems (SIS) Software market.

A key challenge faced by the Student Information Systems (SIS) Software market is the complex integration with existing legacy educational systems and diverse technology stacks. Many educational institutions rely on outdated or customized software that lacks standard interoperability, making it difficult to implement new SIS solutions without significant customization and cost. This complexity can result in prolonged deployment timelines and increased resource allocation for training and technical support. Moreover, ensuring seamless data migration and maintaining system stability during transition phases remains a critical hurdle. Vendors must address these integration challenges by developing flexible, compatible software architectures, which adds to the development complexity and limits rapid market penetration, impacting overall growth potential.

• Surge in AI-Driven Predictive Analytics: The Student Information Systems (SIS) Software market is witnessing widespread integration of AI-powered predictive analytics tools. These tools analyze historical student data to forecast academic performance, attendance patterns, and dropout risks. Educational institutions report improvements in early intervention strategies, resulting in up to a 25% increase in student retention rates. This trend is particularly prominent in universities and large school districts seeking data-driven decision-making capabilities to enhance educational outcomes.

• Expansion of Cloud-Native SIS Solutions: Cloud-native Student Information Systems are becoming the preferred choice for educational organizations globally. These systems enable seamless scalability and offer enhanced data security protocols that align with evolving privacy standards. Over 60% of new SIS deployments in 2024 incorporated cloud-first architectures, reflecting a shift away from traditional on-premises solutions to more agile, remote-accessible platforms.

• Mobile-First SIS User Interfaces: There is a notable shift toward mobile-first designs in SIS software, addressing the growing demand for accessibility on smartphones and tablets. Educational stakeholders benefit from real-time notifications, assignment submissions, and communication features on mobile apps, leading to a 30% increase in daily active users across K-12 and higher education sectors. This enhances engagement among students, parents, and faculty alike.

• Enhanced Integration with Learning Management Systems (LMS): The market is seeing deeper integration of SIS platforms with Learning Management Systems to create unified education ecosystems. This synergy facilitates seamless transfer of student performance data, course materials, and attendance records between systems. Institutions leveraging integrated SIS-LMS solutions report a 40% reduction in administrative workload, improving operational efficiency and resource allocation.

The Student Information Systems (SIS) Software market is segmented by product type, application, and end-user, providing comprehensive insights into demand patterns and usage across diverse educational settings. Product types include cloud-based, on-premises, and hybrid SIS solutions, each tailored to specific institutional needs. Applications range from student enrollment management and attendance tracking to performance analytics and communication management. End-users primarily consist of K-12 schools, higher education institutions, and vocational training centers, reflecting varied adoption rates influenced by organizational size and digital infrastructure maturity. This segmentation aids decision-makers in understanding market dynamics and identifying targeted opportunities for customized SIS software development and deployment.

Cloud-based Student Information Systems dominate the market due to their scalability, cost-effectiveness, and seamless remote access capabilities. Institutions benefit from automatic updates and enhanced data security without the need for extensive on-site IT support, making this type ideal for large school districts and universities. The fastest-growing segment is hybrid SIS solutions, combining cloud flexibility with on-premises control, driven by organizations requiring compliance with strict data privacy laws and localized data storage. On-premises SIS solutions, while less prevalent, remain relevant in regions with limited internet infrastructure or where institutions prefer in-house management of sensitive student data. Other niche types include mobile-specific SIS apps that focus on accessibility and user experience for students and parents. Together, these types provide a spectrum of options catering to varying institutional demands.

Student enrollment management remains the leading application area within the Student Information Systems (SIS) Software market, as institutions prioritize streamlined admission processes to handle large volumes of applicants efficiently. Attendance tracking follows closely, as accurate daily attendance is critical for compliance and academic monitoring. The fastest-growing application is performance analytics, bolstered by increasing interest in data-driven educational strategies and personalized learning. Communication management tools integrated within SIS platforms also see steady growth, enabling real-time engagement between students, parents, and educators. Other applications such as fee management and scheduling contribute to overall operational efficiency but are generally secondary in market impact. These application trends highlight evolving institutional priorities towards integrated, multi-functional SIS platforms.

K-12 educational institutions constitute the leading end-user segment of the Student Information Systems (SIS) Software market due to widespread adoption driven by government initiatives and increasing digital literacy among educators. Higher education institutions represent the fastest-growing segment, propelled by expanding student populations, diverse course offerings, and the demand for sophisticated analytics to support academic advising and retention efforts. Vocational and professional training centers also contribute to market growth by adopting SIS platforms to manage certifications, course scheduling, and compliance with industry standards. Additionally, private and charter schools represent niche users that emphasize customized SIS solutions tailored to smaller, more flexible educational models. Collectively, these end-users define the varied landscape of SIS software utilization and innovation.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

North America continues to lead the Student Information Systems (SIS) Software market with widespread adoption in K-12 and higher education sectors, driven by robust digital infrastructure and government initiatives supporting educational technology upgrades. Meanwhile, Asia-Pacific’s surge is fueled by rapid digitization, increasing investment in smart education infrastructure, and expanding student populations in countries like China and India. Additionally, Europe maintains significant market contributions with ongoing regulatory advancements and strong sustainability policies influencing SIS software integration across educational institutions. The Middle East & Africa and South America regions are also gradually increasing their adoption of innovative SIS solutions, supported by government funding and infrastructure modernization projects.

Robust Digital Infrastructure and Strategic Policy Support Driving Growth

North America holds approximately 38% of the Student Information Systems (SIS) Software market share by volume. The region benefits from advanced technological adoption in education, with key industries including K-12 schools, universities, and vocational training centers driving demand. Recent regulatory changes emphasize data privacy and security compliance, prompting institutions to upgrade their SIS platforms. Additionally, significant government grants and funding initiatives for digital transformation in education have accelerated SIS software deployments. The market also sees continuous innovation in AI-enabled analytics and cloud-based SIS solutions, enhancing institutional efficiency and personalized learning experiences. Digital transformation trends such as mobile-first access and integrated communication modules further strengthen the market’s presence in this region.

Leading European Education Systems Accelerate SIS Adoption

Europe commands around 28% of the Student Information Systems (SIS) Software market volume, with major contributors including Germany, the UK, and France. These countries are integrating SIS platforms to support large, diverse student bodies and comply with stringent data protection regulations enforced by the GDPR framework. Sustainability initiatives in education, such as paperless administration and energy-efficient data centers, are increasingly influencing SIS software requirements. European institutions also focus on adopting emerging technologies, including blockchain for secure student record verification and AI-enhanced administrative automation. Digital learning ecosystems combining SIS and Learning Management Systems (LMS) are becoming standard practice, enhancing data coherence and user experience across multiple educational stages.

Rapid Technological Advancement Fuels Market Expansion

Asia-Pacific ranks as the fastest-growing region in the Student Information Systems (SIS) Software market, accounting for about 22% of global volume in 2024. China, India, and Japan lead consumption, driven by government-led initiatives to digitize education and improve student data management across rapidly expanding academic institutions. Investments in digital infrastructure and manufacturing of educational hardware support SIS software deployments, especially in urban and semi-urban areas. Technology innovation hubs across Asia-Pacific emphasize the development of cloud-native SIS platforms and AI integration, which enhances analytics and personalized student services. The growing middle-class population and increased focus on education quality propel adoption across public and private education sectors.

Emerging Infrastructure and Educational Reform Promote SIS Growth

South America holds approximately 6% market share in the Student Information Systems (SIS) Software market, with Brazil and Argentina as key contributors. These countries are actively modernizing educational infrastructure, leveraging SIS software to improve student management and institutional efficiency. Growth in energy and infrastructure sectors indirectly supports the adoption of digital educational technologies through improved connectivity. Government incentives and trade policies promoting international technology partnerships encourage the introduction of advanced SIS platforms tailored to regional needs. The market is increasingly driven by private and public school networks adopting cloud-based and mobile-friendly SIS solutions to enhance educational administration and student engagement.

Technological Modernization and Regulatory Alignment Accelerate Demand

The Middle East & Africa region represents around 6% of the Student Information Systems (SIS) Software market volume, with the UAE and South Africa leading growth. Key industries such as education, construction, and oil & gas contribute to increasing digital technology investments, including SIS solutions to support workforce development and academic administration. Technological modernization efforts emphasize AI, cloud computing, and mobile accessibility to improve educational outcomes. Local regulations focus on data security and privacy compliance, aligning with global standards to facilitate SIS software adoption. Strategic trade partnerships and government-backed digital education programs further stimulate the demand for advanced student information management systems in the region.

United States: Holds approximately 35% market share due to its high production capacity of SIS software solutions and strong demand from a vast network of K-12 and higher education institutions embracing digital transformation.

China: Accounts for nearly 20% of the market share, driven by substantial government investment in digitizing education, expanding student enrollment, and rapid adoption of cloud-based SIS platforms across urban and rural regions.

The Student Information Systems (SIS) Software market is characterized by a highly competitive environment with over 40 active global and regional players vying for market share. Market leaders have established strong positions through continuous innovation, strategic partnerships, and expansion of product portfolios tailored to diverse educational institutions. Companies are increasingly focusing on cloud-based SIS solutions, AI integration for advanced analytics, and mobile accessibility to differentiate their offerings. Recent strategic initiatives include mergers and acquisitions aimed at broadening geographic reach and enhancing technology capabilities. Partnerships with educational technology providers and government agencies are also prominent to facilitate seamless SIS adoption and integration with broader digital learning ecosystems. Innovation trends such as blockchain for secure student data management and real-time communication tools are further intensifying competition, pushing companies to invest heavily in R&D. As educational institutions increasingly prioritize scalable, user-friendly, and secure SIS platforms, the market remains dynamic with constant evolution in product features and customer engagement strategies.

PowerSchool Group LLC

Infinite Campus Inc.

Ellucian Company L.P.

Blackbaud Inc.

Oracle Corporation

SAP SE

Jenzabar Inc.

Skyward, Inc.

Tyler Technologies, Inc.

FACTS Management LLC

The Student Information Systems (SIS) Software market is experiencing rapid technological advancements that are reshaping the way educational institutions manage student data and administrative functions. Cloud computing remains a foundational technology, enabling scalable and accessible SIS solutions that support remote learning and administrative agility. Integration of Artificial Intelligence (AI) and Machine Learning (ML) technologies has enhanced predictive analytics, personalized learning paths, and automated administrative tasks, increasing operational efficiency and improving student engagement. Blockchain technology is emerging as a critical tool for ensuring data security and integrity, offering tamper-proof student records and seamless verification processes.

Moreover, mobile-first solutions and API-driven architectures are enabling greater interoperability between SIS platforms and third-party educational applications, fostering more cohesive digital ecosystems. The adoption of Internet of Things (IoT) devices and smart campus technologies complements SIS by providing real-time data that enhances campus safety and resource management. Additionally, advancements in user interface design and accessibility are making SIS software more intuitive and inclusive for diverse user groups, including administrators, teachers, students, and parents. These technology trends collectively empower institutions to optimize educational delivery, comply with evolving regulatory requirements, and address the increasing demand for data-driven decision-making.

In March 2024, PowerSchool launched a new AI-powered analytics module designed to enhance student performance tracking and early intervention strategies, enabling educators to personalize support based on real-time data insights.

In September 2023, Ellucian introduced an upgraded cloud-based SIS platform featuring enhanced cybersecurity protocols and multi-factor authentication, improving data privacy and compliance with global educational data regulations.

In November 2023, Infinite Campus expanded its integration capabilities by partnering with leading e-learning platforms, facilitating seamless data exchange and unified student experience across diverse digital education tools.

In January 2024, Blackbaud released a mobile-optimized SIS application enabling on-the-go access to student records and communication tools, significantly improving parent and teacher engagement in K-12 environments.

The Student Information Systems (SIS) Software Market Report provides a comprehensive analysis covering a wide range of market segments, including various software types such as cloud-based, on-premise, and hybrid solutions. It evaluates application areas spanning K-12 education, higher education institutions, vocational training centers, and corporate learning environments, reflecting the diverse end-user landscape. The report also explores technology trends, highlighting AI integration, mobile applications, data security advancements, and interoperability with third-party educational platforms.

Geographically, the analysis encompasses key regions such as North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, each examined for market share, demand drivers, and regional developments. The report further investigates niche segments, including emerging markets in developing economies and specialized SIS solutions tailored for remote learning and special education needs.

In addition to technological and regional coverage, the report addresses regulatory frameworks, data privacy concerns, and institutional requirements shaping SIS adoption. It assesses competitive dynamics and profiles major global players to provide strategic insights for stakeholders. Overall, the scope ensures a detailed understanding of market opportunities, challenges, and evolving trends, equipping business leaders and decision-makers with actionable intelligence to navigate the SIS software market effectively.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 693.48 Million |

|

Market Revenue in 2032 |

USD 1341.76 Million |

|

CAGR (2025 - 2032) |

8.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

PowerSchool Group LLC, Infinite Campus Inc., Ellucian Company L.P., Blackbaud Inc., Oracle Corporation, SAP SE, Jenzabar Inc., Skyward, Inc., Tyler Technologies, Inc., FACTS Management LLC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |