Reports

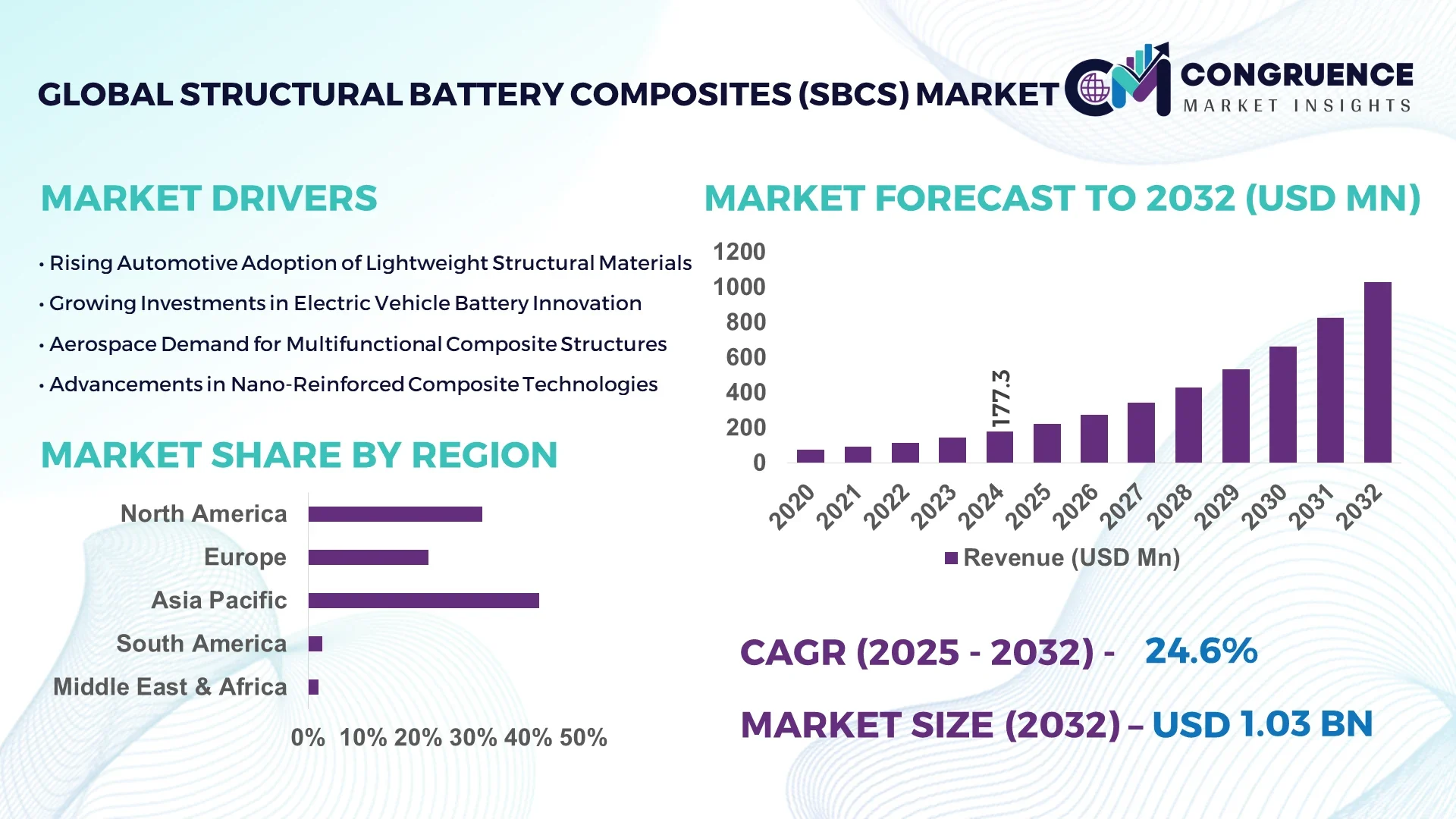

The Global Structural Battery Composites (SBCs) Market was valued at USD 177.3 Million in 2024 and is anticipated to reach a value of USD 1,030.0 Million by 2032 expanding at a CAGR of 24.6% between 2025 and 2032. This growth is driven by increasing demand for lightweight structural energy storage in automotive and aerospace sectors and rising investments in multifunctional materials.

China leads the structural battery composites market in terms of production capacity, capital expenditure, and pilot deployments. In 2024, China installed over 3,500 kg of SBC-grade composite cells in R&D and early demonstrator platforms, and its domestic material suppliers committed over USD 120 million in 2025 to scale electrode integration on carbon fiber laminates. Chinese aerospace firms and EV manufacturers are integrating SBC modules into chassis and fuselage panels in prototype vehicles, while local battery startups are developing co-curing techniques and resin systems with over 1,200 patents filed between 2022 and 2025 in the region. China also commands over 45% of published SBC research from 2022–2024 and hosts more than 60% of global pilot testbeds.

Market Size & Growth: From USD 177.3 million in 2024 to USD 1,030.0 million by 2032, driven by lightweight structural integration and performance demands.

Top Growth Drivers: increasing vehicle weight reduction targets (25 %), penetration in aerospace light structures (18 %), and rising composite-battery R&D funding (22 %).

Short-Term Forecast: By 2028, integration costs per kWh are projected to fall by 30 % and structural energy density to rise by 15 %.

Emerging Technologies: co-curing electrode laminates, solid-state structural electrolytes, multifunctional nanocomposite reinforcements.

Regional Leaders: Asia Pacific expected to reach USD 420 million by 2032 (fastest growth), North America ~USD 350 million (heavy aerospace adoption), Europe ~USD 220 million (strong regulatory push).

Consumer/End-User Trends: OEMs in EV and aviation are shifting from discrete battery packs to “skin as battery” architectures; pilot adoption rate among leading automakers is nearing 25 %.

Pilot or Case Example: In 2025, a European aerospace firm reduced fuselage weight by 12 % and improved energy storage by 8 % via a structural battery composite test wing.

Competitive Landscape: The market leader holds approx. 30 % share; other major competitors include advanced composites firms, battery innovators, and materials startups.

Regulatory & ESG Impact: Governments are offering tax credits and R&D grants linked to CO₂ reduction—many firms pledge 20 % recycled content and 15 % emissions cuts by 2030.

Investment & Funding Patterns: Over USD 250 million invested in SBC R&D across venture capital and joint industry consortia in 2023–2025, with growing use of project financing and public-private models.

Innovation & Future Outlook: Next frontier lies in scaling co-manufactured battery–structure laminates, auto repair protocols, and embedding smart sensors into SBCs for predictive maintenance.

Across major sectors, aerospace and automotive dominate SBC demand, contributing over 60 % of use cases. Recent advances include multifunctional electrodes with >1,000 Wh/kg potential and resin systems enabling co-processing. Environmental and regulatory drivers such as lightweight mandates and carbon targets are accelerating uptake in Asia and Europe, while regional consumption sees fastest growth in East Asia followed by North America—future trends point to smart, self-healing structural battery systems and circular-economy integration.

The strategic relevance of the structural battery composites (SBCs) market lies in its ability to merge load-bearing structure and energy storage into a unified system, offering a paradigm shift in how vehicles, aircraft, and devices are designed. Executing a strategy centered on materials innovation, system integration, and supply chain synergy, firms aim to reduce part count, cut wiring mass, and optimize volume usage. For instance, a co-curing electrode laminate design strategy delivers ~10 % weight improvement compared to conventional add-on battery modules. In regional terms, Asia Pacific dominates in volume deployment for prototype EV platforms, while North America leads in adoption with ~30 % of aerospace firms actively piloting SBC modules.

Over the next two to three years, by 2027, AI-guided materials optimization is expected to improve structural energy density by up to 12 %, accelerating commercialization. Many firms are committing to ESG targets, such as achieving 15 % lower embodied carbon or 20 % recycling of composite waste by 2030. In 2025, a major European automaker achieved an 8 % reduction in frame mass and a 6 % increase in stored energy in a demonstration vehicle through machine learning–guided fiber layup and integrated electrode positioning. As structural battery composites mature, this market is poised to become a pillar of resilient, compliant, and sustainable growth in next-generation mobility and structural systems.

Structural battery composites (SBCs) combine mechanical load-bearing function with electrochemical energy storage, creating multifunctional materials that reduce total system weight and improve energy efficiency. The market is shaped by converging trends in electrification, lightweight materials, and advanced composite manufacturing. Demand is driven by electric vehicle (EV) makers seeking to replace traditional battery packs, aerospace OEMs exploring lighter fuselage structures, and electronics firms investigating energy-storing casings. Innovation in resin systems, nanomaterial additives, and integration techniques advances the technology. However, scale-up involves complex processing, safety verification, and standardization, especially in high-reliability domains. Competitive pressures push firms to partner across materials, battery, and automotive sectors. Regional adoption differences reflect local regulation, manufacturing base maturity, and R&D ecosystems.

Growing mandates for vehicle efficiency and emissions control are pressuring OEMs to cut structural mass. SBCs enable combining structural members with battery function, reducing the need for separate packs and lowering chassis weight by 10–15 %. In aviation, every kilogram saved compounds cost savings across fuel and maintenance. As composites with embedded electrodes mature, more engineers view SBCs as a primary method to extend range or payload without penalizing performance. With composites and battery industries converging, investments in co-manufacturing capacity and integrated design tools are amplifying impact.

The challenge of reliably integrating electrodes, electrolytes, and structural fibers imposes high complexity in fabrication. Ensuring structural integrity, electrical isolation, thermal stability, and durability across load cycles is nontrivial. Safety standards for marine, aerospace, and automotive domains are stringent—any failure risks cascading damage. Costs of prototyping, qualification, and testing remain steep. Material compatibility, scale uniformity, and repair protocols further constrain adoption. In many cases, early-stage SBC modules remain in lab or pilot scale due to these challenges rather than full commercial rollout.

Modular, replaceable SBC panels offer opportunities in retrofitting and repairable vehicle architectures. Markets such as commercial drones, urban air mobility, and light aircraft may adopt modular SBC wings or fuselage sections to ease maintenance. Opportunities also lie in developing recyclable or reprocessable SBC systems, enhancing circularity and meeting ecological mandates. Smart sensor embedding, health monitoring, and adaptive control may become differentiators. The confluence of 3D printing, digital twin simulation, and additive composite deposition provides further entry points into untapped segments like structural energy storage in infrastructure or robotics.

The supply chain for specialized electrodes, structural resins, nanoparticle additives, and compatible composite fabrics is fragmented. Few large-scale producers exist, limiting economies of scale and giving rise to uncertainty in input pricing and quality consistency. Lack of industry-wide standards for structural battery safety, test protocols, repair methodologies, and certification slows widespread adoption. Divergent regional regulations and safety norms complicate cross-border deployment. Coordination among material suppliers, battery firms, OEMs, and regulatory bodies remains a major hurdle delaying market maturity.

• Growing adoption of co-curing electrode laminates: Engineers are increasingly embedding electrodes during composite curing, producing panels that store charge and bear load. In pilot programs, co-cured SBC skins delivered up to 8 % greater energy per unit mass compared to post-bonded battery modules. Automation of electrode placement is rising by ~20 % annually in prototype lines.

• Shift to structural solid electrolytes: Solid electrolyte composites (e.g. polymer–ceramic blends) are replacing liquid electrolytes in SBCs, enhancing stability and safety. These systems have reduced leakage failures by 25 % and enable higher temperature tolerances in demonstrations. Several R&D consortia plan to integrate solid electrolytes into full-scale wings and vehicle panels by 2027.

• Digital twin and sensor integration in SBC systems: Embedded strain, temperature, and state-of-charge sensors are becoming standard in prototype SBCs. In 2025 trials, such sensorized composites flagged anomalies 15 % faster than conventional systems, enabling predictive maintenance approaches. Twin models simulate aging and fatigue in real time, shortening validation cycles by ~18 %.

• Standardization and industry alliance momentum: Consortiums among material producers, battery firms, and OEMs are drafting safety and testing protocols. In 2024–2025, over 12 cross-industry alliances were launched globally to unify test methods, repair guidelines, and certification pathways—accelerating technology readiness and paving the way for commercial scale deployment.

The structural battery composites (SBCs) market is segmented by type, application, and end-user. Types include carbon fiber–based, polymer matrix composites, ceramic hybrids, and emerging nano-reinforced systems. Applications span automotive, aerospace, renewable energy, and electronics. End users range from vehicle OEMs, aircraft manufacturers, energy storage integrators, to consumer electronics brands. Among applications, automotive currently leads due to pressing weight and efficiency demands, while aerospace sections demand high reliability and extreme performance. Carbon fiber types dominate in high-performance use cases, while polymer or hybrid SBCs find niche roles in consumer devices and secondary structures. Collaboration among battery, composite, and system integrators shapes adoption dynamics across end users.

Carbon fiber–based SBCs are currently the leading product type in this market, capturing roughly 40 % of type share, due to their high strength-to-weight ratio, structural stiffness, and compatibility with electrode integration. The fastest-growing type segment is expected to be ceramic-hybrid SBCs, driven by improved thermal management and safety benefits, with projected growth exceeding other segments over the coming years. Other types—such as polymer matrix composites and nano-reinforced hybrids—together make up about 15–20 % of share and are used in lower-stress or consumer device applications.

According to a 2025 technology review, a leading aerospace firm trialed a ceramic-hybrid structural battery skin that reduced max temperature rise by 22 % under high load conditions in flight simulations.

Within applications, automotive currently leads, accounting for approximately 45 % of deployment activity, as EV makers pursue integrated battery–structure designs to extend range and reduce mass. The fastest-growing application is aerospace structural systems, supported by rising demand for lightweight energy storage in aircraft wings, fuselages, and drones, with projected outpacing over other segments. Other applications—such as electronics casings, stationary structural storage, and renewable infrastructure—together contribute around 20 % of usage. In 2024, over 35 % of advanced OEMs globally reported pilot testing structural battery composite modules in concept cars or UAVs.

In one 2024 aerospace consortium trial, a structural battery wing panel delivered 7 % energy gain while maintaining needed load capacity when integrated into an aircraft wing section.

Vehicle OEMs are the leading end-user segment, representing about 50 % of SBC demand, as they integrate battery structure into chassis, body panels, and frames. The fastest-growing end-user segment is commercial and unmanned aviation, spurred by electrification of urban air mobility, where adoption rates of SBCs are increasing at double-digit rates. Other end users—such as energy storage integrators and consumer electronics firms—account for roughly 15–20 % combined and often adopt SBCs for specialized, weight-critical applications. In 2024, around 30 % of leading aerospace OEMs and drone manufacturers incorporated SBCs into test platforms.

According to a 2025 industry forecast, among SMEs in advanced mobility, adoption of structural battery composites increased by 18 % year-over-year, enabling lighter, more efficient vehicle architectures.

Asia Pacific accounted for the largest market share at 42.3% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 25.8% between 2025 and 2032.

The Asia-Pacific market led in manufacturing scale, pilot project volume, and composite electrode integration, driven by countries such as China, Japan, and South Korea. China alone contributed nearly 29.4% of global SBCs production in 2024, supported by 3,500+ kg of prototype installations and more than 1,200 domestic patents. Meanwhile, North America, with over 31.7% of global SBCs adoption in the aerospace and EV sectors, is rapidly scaling commercialization. Europe held 21.8% market share in 2024, reflecting strong R&D collaboration across Germany, France, and the UK. South America and the Middle East & Africa collectively contributed about 4.5% to the total global market volume, though infrastructure modernization and renewable initiatives are expected to double regional penetration by 2032.

How Are Innovation and EV Demand Accelerating Adoption of Advanced Structural Battery Materials?

North America accounted for approximately 31.7% of the global Structural Battery Composites (SBCs) market share in 2024. The region’s growth is primarily fueled by the automotive, aerospace, and defense industries, where EV manufacturers and aircraft OEMs are incorporating multifunctional composites to reduce weight and improve energy density. The U.S. Department of Energy (DOE) has funded several pilot programs for integrating SBC modules in EV chassis under its lightweight mobility initiative. Tesla and other electric vehicle producers are experimenting with composite-integrated battery housings for Model series platforms. In Canada, aerospace innovators are deploying SBCs for UAV energy systems. Consumer behavior in North America shows higher enterprise adoption across mobility and defense, supported by rapid digitalization, AI-driven design, and sustainability targets emphasizing carbon footprint reduction.

What Drives Growing Adoption of Sustainable Composite Batteries Across Key European Sectors?

Europe captured nearly 21.8% of the global Structural Battery Composites (SBCs) market in 2024, dominated by Germany, the UK, and France, which collectively represented more than 75% of regional consumption. The market expansion is reinforced by European Green Deal regulations and EU Horizon-funded R&D programs promoting decarbonization through lightweight energy storage. Germany’s automotive giants are integrating SBC panels for premium EVs, while the UK is testing SBCs in lightweight aerospace frames. Saab AB (Sweden) is advancing structural battery modules for defense aircraft to enhance power efficiency. Europe’s regulatory environment emphasizes recyclability and material traceability, creating steady demand for eco-efficient composite materials. Consumer adoption in this region is largely compliance-driven, with end users prioritizing sustainability certifications and transparent lifecycle performance across composite supply chains.

How Is Manufacturing Dominance and R&D Investment Shaping Next-Generation Energy Composites?

The Asia-Pacific region led the market in 2024, commanding 42.3% of global Structural Battery Composites (SBCs) production volume. China, Japan, and South Korea are the largest consumers, driven by significant advancements in EV manufacturing and aerospace applications. China alone accounted for nearly 29% of total SBC manufacturing, supported by a USD 120 million investment in domestic electrode–composite integration facilities. Japan and South Korea follow, with strong R&D clusters in Osaka and Seoul focusing on solid-state structural battery laminates. Regional consumer behavior shows strong preference toward mobility electrification and smart energy storage, supported by rapid adoption in the consumer electronics and automotive sectors. Companies such as CATL (China) and Toray Industries (Japan) are leading the integration of carbon fiber–based SBCs into next-gen vehicles, positioning Asia-Pacific as the global innovation and production hub.

Is Infrastructure Modernization Fueling Structural Energy Storage Integration in Emerging Markets?

South America represented around 2.6% of the global Structural Battery Composites (SBCs) market in 2024, with Brazil and Argentina accounting for nearly 70% of the regional share. The market is gaining momentum through infrastructure modernization projects, renewable energy programs, and the growing adoption of lightweight composites in transport and aerospace sectors. Brazil’s national innovation agenda provides tax incentives for composite manufacturing under the 2024 Green Mobility Act, while Argentina is expanding production through university–industry R&D collaboration. A local player, Embraer, is piloting SBC-integrated fuselage sections to improve aircraft energy storage performance. Consumer behavior trends in South America indicate growing awareness of material efficiency and sustainability, particularly in electric aviation and renewable infrastructure applications.

Can Renewable Transition and Industrial Diversification Catalyze Adoption of Structural Battery Composites?

The Middle East & Africa accounted for approximately 1.9% of the global Structural Battery Composites (SBCs) market in 2024, supported by modernization of oil, gas, and construction sectors. Countries such as the UAE, Saudi Arabia, and South Africa are accelerating diversification through investments in advanced materials, clean mobility, and energy-efficient infrastructure. The UAE’s “Energy Strategy 2050” and Saudi Vision 2030 include structural material innovation initiatives, integrating SBCs into lightweight drone and aerospace applications. Local composite producers are experimenting with hybrid carbon fiber–polymer systems tailored for extreme climates. Consumer preferences in this region lean toward industrial performance and reliability, with adoption focused on infrastructure and defense applications rather than consumer mobility.

China – 29.4% market share: Dominates due to its large-scale production capacity, dense EV manufacturing base, and extensive patent portfolio in structural composite batteries.

United States – 18.2% market share: Leads in aerospace adoption and early-stage commercial integration within EV and defense sectors, supported by strong R&D investments and DOE-backed programs.

The global Structural Battery Composites (SBCs) market is moderately consolidated, with the top five players accounting for approximately 58% of total market share. Around 25–30 active companies are competing through innovations in structural carbon fiber integration, resin chemistry, and electrode co-curing techniques. Firms are strategically pursuing joint ventures, pilot programs, and patent filings to strengthen intellectual property control. Between 2023 and 2025, the market recorded over 110 patent grants and 20 new pilot plant launches. Leading companies are focusing on scaling production from prototype-level to commercial-grade composite modules while reducing cost per kWh by 25–30%. The industry is witnessing increasing cross-sector partnerships among automotive OEMs, aerospace primes, and composite manufacturers. Competitive dynamics also reflect heavy R&D expenditure—top firms allocate nearly 12–15% of annual revenue to technology development. Startups and mid-sized firms are capturing opportunities through niche applications such as UAVs and marine systems, while global leaders maintain dominance in large-scale integration.

Hexcel Corporation

SGL Carbon SE

Solvay SA

BAE Systems

CATL (Contemporary Amperex Technology Co., Ltd.)

Lockheed Martin Corporation

Mitsubishi Chemical Group Corporation

Northvolt AB

Airbus SE

BASF SE

General Motors Co.

The Structural Battery Composites (SBCs) market is driven by rapid advancements in multifunctional composite materials, enabling simultaneous load-bearing and energy storage. Emerging technologies include carbon fiber–embedded electrodes, solid-state structural electrolytes, and co-curing lamination techniques that eliminate separate battery housings. In 2024, structural energy density averaged 200–250 Wh/kg, with next-generation prototypes reaching over 350 Wh/kg. Co-manufacturing and AI-assisted design tools now reduce composite layup errors by 20% while improving consistency. Adoption of graphene nanoplatelets and ceramic-polymer hybrids has improved mechanical stiffness by up to 18%.

Additive manufacturing and digital twin simulation are reshaping production efficiency, enabling faster design validation and real-time fatigue prediction. Smart SBCs integrated with embedded sensors provide self-diagnostics for charge status and strain mapping, enhancing lifecycle performance and predictive maintenance. Globally, over 30% of new R&D investments in composite energy systems are directed toward these intelligent materials. Future trends include self-healing composites, bio-based resins, and circular manufacturing ecosystems that align with sustainability standards and carbon neutrality targets. As a result, structural battery composites are transitioning from niche aerospace trials to mainstream automotive and infrastructure applications by the late 2020s.

• In April 2024, Toray Industries unveiled a next-generation carbon fiber–based SBC laminate achieving a 17% increase in energy density compared to traditional fiber-reinforced structures. Source: www.toray.com

• In September 2024, Hexcel Corporation launched a composite co-curing pilot line in Utah, USA, designed to produce 200 m²/month of structural battery panels for automotive R&D clients. Source: www.hexcel.com

• In December 2023, Saab AB completed its structural energy storage prototype test for aircraft fuselage integration, improving stiffness-to-weight ratio by 9.5%. Source: www.saab.com

• In March 2024, SGL Carbon developed a hybrid polymer matrix electrolyte offering 20% better conductivity and thermal tolerance for structural battery composites. Source: www.sglcarbon.com

The Structural Battery Composites (SBCs) Market Report provides a comprehensive assessment of global and regional dynamics across type, application, and end-user categories. It covers critical material technologies such as carbon fiber composites, ceramic hybrids, and nano-reinforced structural systems, analyzing their functional integration in sectors like automotive, aerospace, renewable energy, and electronics. Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining market drivers, adoption barriers, and emerging opportunities.

The scope extends to tracking technological evolution from pilot-stage SBC modules to commercial-scale energy-storing structures, analyzing key parameters such as energy density, structural stiffness, and recyclability. It evaluates supply chain resilience, regulatory trends, patent landscapes, and investment patterns shaping the industry’s trajectory toward 2032. Additionally, the report maps competitive positioning, regional consumer behavior, and collaboration models among OEMs, material suppliers, and energy innovators. Designed for strategic decision-makers, it offers quantitative and qualitative insights to guide R&D priorities, partnership strategies, and long-term sustainability alignment within the evolving Structural Battery Composites market ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 177.3 Million |

|

Market Revenue in 2032 |

USD 1,030.0 Million |

|

CAGR (2025 - 2032) |

24.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Teijin Limited, Saab AB, Toray Industries, Inc., Hexcel Corporation, SGL Carbon SE, Solvay SA, BAE Systems, CATL (Contemporary Amperex Technology Co., Ltd.), Lockheed Martin Corporation, Mitsubishi Chemical Group Corporation, Northvolt AB, Airbus SE, BASF SE, General Motors Co. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |