Reports

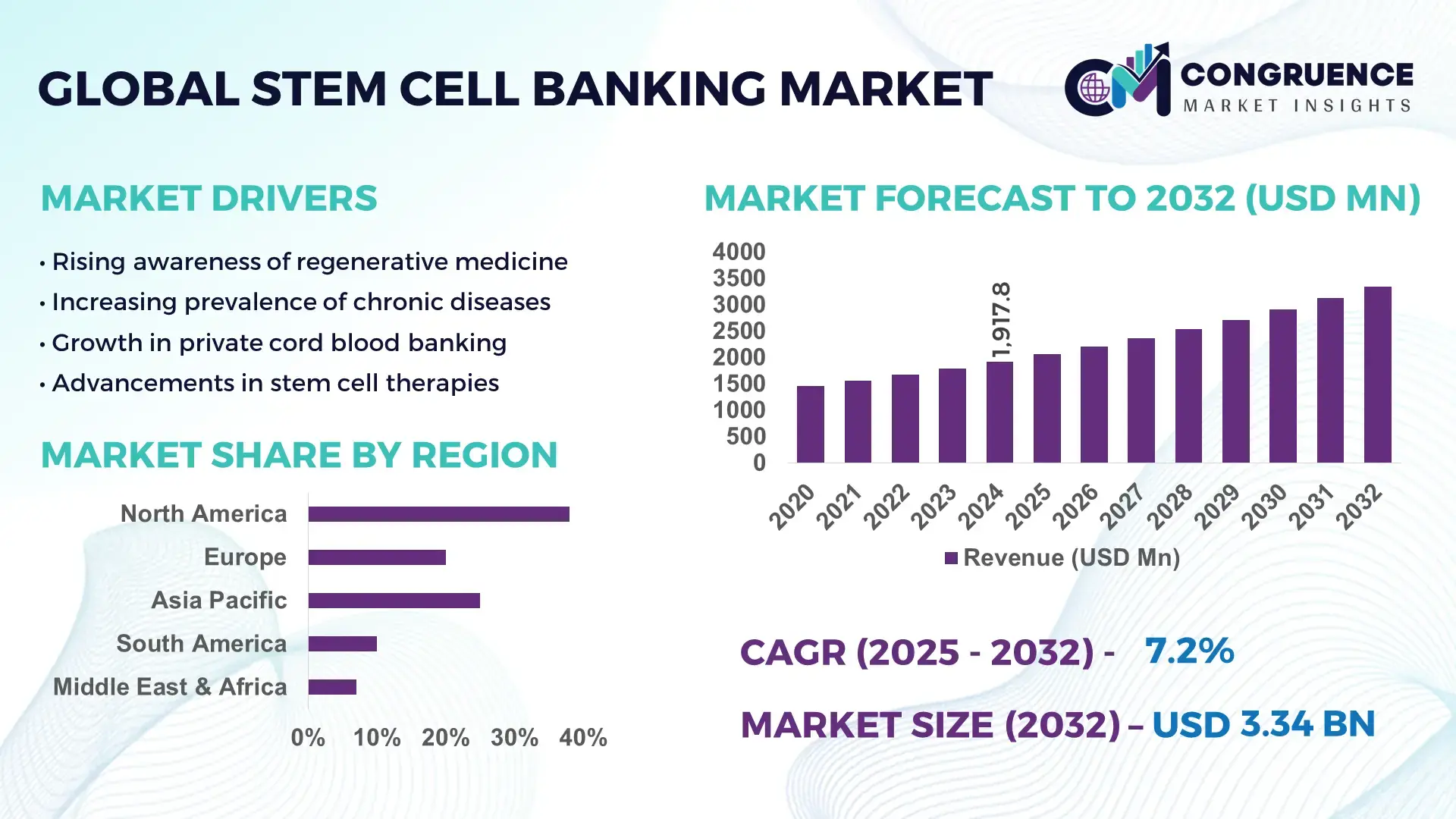

The Global Stem Cell Banking Market was valued at USD 1917.8 Million in 2024 and is anticipated to reach a value of USD 3344.74 Million by 2032 expanding at a CAGR of 7.2% between 2025 and 2032. This growth is supported by rising clinical utilization of stem cells in regenerative medicine, increased parental awareness of cord blood preservation, and expanding applications in oncology and immunological disorders.

The United States represents the most established Stem Cell Banking ecosystem globally, supported by advanced infrastructure, high procedural volumes, and sustained investment. More than 20 million stem cell units are stored across public and private banks nationwide, with annual processing capacity exceeding 1.2 million samples. The country attracts over USD 3.5 billion annually in regenerative medicine and cell-therapy-related investments, including biobanking infrastructure and cryopreservation technologies. Key applications include hematopoietic stem cell transplants, which exceed 25,000 procedures per year, and emerging uses in gene-modified cell therapies. Technological advancements such as automated cryogenic storage systems, AI-based sample tracking, and next-generation viability testing are increasingly adopted across U.S. facilities, improving long-term storage reliability and operational scalability.

Market Size & Growth: Valued at USD 1917.8 Million in 2024, projected to reach USD 3344.74 Million by 2032 at a CAGR of 7.2%, driven by expanding therapeutic indications and higher long-term storage enrollment rates.

Top Growth Drivers: Rising cord blood banking adoption (↑18%), increase in stem-cell-based clinical trials (↑22%), and improved cryopreservation efficiency (↑15%).

Short-Term Forecast: By 2028, automated storage and digital chain-of-custody systems are expected to reduce sample handling errors by approximately 30%.

Emerging Technologies: Automated cryogenic storage, AI-enabled sample integrity monitoring, and next-generation cell viability analytics.

Regional Leaders: North America projected at ~USD 1.35 Billion by 2032 with strong private banking adoption; Europe ~USD 0.95 Billion driven by public bank networks; Asia-Pacific ~USD 0.78 Billion supported by rising birth rates and medical tourism.

Consumer/End-User Trends: Private family banking dominates urban regions, while public stem cell banks see higher utilization from hospitals and transplant centers.

Pilot or Case Example: In 2024, a large-scale automated biobank pilot achieved a 28% improvement in retrieval efficiency and a 20% reduction in operational downtime.

Competitive Landscape: Market leader holds approximately 18–20% share, followed by Cryo-Cell, ViaCord, Cord Blood Registry, Lifecell, and Vita 34.

Regulatory & ESG Impact: Strengthening biobanking standards, informed-consent regulations, and sustainability-focused cold-chain optimization are shaping adoption.

Investment & Funding Patterns: Over USD 6 Billion invested globally in cell therapy and biobanking infrastructure during 2022–2024, with growing venture participation.

Innovation & Future Outlook: Integration of stem cell banking with gene therapy platforms and personalized medicine pipelines is expected to accelerate long-term demand.

The Stem Cell Banking Market serves key sectors including hospitals and transplant centers, which account for roughly 45% of utilization, followed by research institutions at around 30% and private family banking services contributing nearly 25%. Recent innovations such as closed-system cell processing, long-duration cryogenic preservation exceeding 25 years, and digital sample traceability platforms are reshaping operational standards. Regulatory frameworks emphasizing ethical sourcing, long-term storage compliance, and data security continue to influence market practices. Regionally, North America and Europe show higher per-capita storage penetration, while Asia-Pacific records faster growth due to rising healthcare expenditure and expanding private banking awareness. Looking ahead, convergence with gene editing, immunotherapy, and personalized regenerative treatments is expected to redefine the strategic role of stem cell banks globally.

The Stem Cell Banking Market holds growing strategic relevance within global healthcare systems as it underpins long-term regenerative medicine capacity, advanced oncology treatments, and precision immunotherapies. From a strategic standpoint, banks are transitioning from passive storage models to integrated bio-infrastructure platforms aligned with clinical trials, cell therapy manufacturing, and hospital networks. Automated cryogenic storage systems deliver nearly 35% improvement in sample retrieval speed and viability assurance compared to conventional manual cryostorage standards, directly enhancing operational scalability and compliance reliability.

Regionally, North America dominates in volume of stored stem cell units, while Asia-Pacific leads in adoption with nearly 42% of new private banking users originating from urban centers in China, India, and South Korea. By 2028, AI-enabled sample monitoring and predictive quality analytics are expected to cut long-term storage loss and handling deviations by approximately 30%, improving cost efficiency and audit readiness. From an ESG and compliance perspective, firms are committing to sustainability metrics such as 25% reduction in liquid nitrogen consumption and energy-efficient cold-chain operations by 2030, aligning with healthcare decarbonization targets.

In a measurable micro-scenario, in 2024, a U.S.-based stem cell bank achieved a 22% reduction in operational downtime through deployment of AI-driven inventory management and automated alarm response systems. Looking ahead, the Stem Cell Banking Market is positioned as a foundational pillar supporting healthcare resilience, regulatory compliance, and sustainable growth, enabling nations and providers to future-proof advanced therapeutic ecosystems.

The rapid expansion of regenerative medicine and cell-based therapies is a primary driver of the Stem Cell Banking Market. Globally, more than 7,000 active clinical trials now involve stem cells or related cellular therapies, increasing demand for reliable, long-duration storage solutions. Hematopoietic stem cell transplants exceed 90,000 procedures annually worldwide, requiring consistent access to high-quality banked samples. Advances in oncology, autoimmune disease management, and gene-modified cell therapies have broadened the clinical utility of stored stem cells beyond traditional transplant use. Hospitals and research institutions increasingly rely on accredited stem cell banks to support trial pipelines and therapy scale-up. This clinical integration elevates storage volumes, drives adoption of higher-grade preservation technologies, and reinforces the Stem Cell Banking Market as an essential component of modern therapeutic infrastructure.

High capital and operating expenditures remain a significant restraint for the Stem Cell Banking Market, particularly for smaller or emerging providers. Establishing compliant cryogenic facilities requires substantial investment in liquid nitrogen systems, backup power infrastructure, validated storage equipment, and continuous environmental monitoring. Annual maintenance and quality assurance costs can account for over 30% of total operating budgets. Additionally, compliance with stringent regulatory frameworks governing biological material storage, data security, and long-term traceability increases administrative and staffing burdens. In developing regions, these cost structures limit scalability and slow the establishment of new public banking facilities. As a result, market expansion is uneven, with smaller players facing barriers to entry and sustained profitability.

The increasing alignment of stem cell banking with personalized medicine and gene therapy presents a significant opportunity for market expansion. Gene-edited cell therapies, CAR-T treatments, and autologous regenerative applications require secure, patient-specific cell storage over extended timelines. Demand for customized biobanking services is rising as healthcare shifts toward individualized treatment pathways. Technological innovations such as closed-system processing and digital identity tagging enable banks to support complex, therapy-linked storage models. Emerging markets are also investing in national biobank initiatives to support precision medicine programs. These developments open new revenue-neutral service pathways, deepen partnerships with biotech firms, and position the Stem Cell Banking Market as a strategic enabler of next-generation therapeutics.

Regulatory complexity and long-term custodial liability present ongoing challenges for the Stem Cell Banking Market. Banks must guarantee sample integrity for storage periods exceeding 20–25 years, creating long-duration legal and operational obligations. Regulatory requirements vary across jurisdictions, complicating cross-border sample transfer and multinational operations. Failure risks include sample degradation, data breaches, or non-compliance penalties, all of which carry reputational and financial consequences. Additionally, evolving ethical standards around consent, secondary use, and data ownership require continuous policy updates. These challenges demand sustained investment in compliance systems, insurance coverage, and governance frameworks, increasing operational risk and management complexity across the Stem Cell Banking Market.

• Expansion of Modular and Prefabricated Biobank Infrastructure: The adoption of modular and prefabricated construction models is reshaping infrastructure development within the Stem Cell Banking Market. Approximately 55% of newly commissioned biobanking facilities reported measurable cost benefits through modular designs, with project timelines reduced by nearly 30%. Pre-fabricated cryogenic rooms, automated storage vaults, and pre-calibrated HVAC modules are increasingly manufactured off-site using precision automation, lowering on-site labor requirements by around 25%. This trend is particularly pronounced in Europe and North America, where regulatory timelines and space optimization are critical for rapid capacity expansion.

• Accelerated Deployment of Automation and Robotics in Sample Handling: Automation in stem cell processing and storage is gaining strong traction, with over 60% of large-scale banks integrating robotic handling systems for sample intake, retrieval, and relocation. Automated systems have demonstrated up to 40% reduction in manual handling errors and a 35% improvement in retrieval turnaround time. Robotic cryogenic arms and barcode-linked inventory platforms are enabling higher-density storage configurations, increasing usable storage capacity per facility by approximately 20% without physical expansion.

• Growth in Digital Monitoring and Predictive Quality Analytics: Digitalization of long-term sample monitoring is emerging as a critical trend in the Stem Cell Banking Market. More than 50% of advanced facilities now employ real-time sensor networks tracking temperature, humidity, and nitrogen levels, generating millions of data points annually. Predictive analytics platforms are improving early fault detection by nearly 28%, while automated alert systems have reduced incident response times by over 35%. This shift supports stronger compliance performance and minimizes long-duration sample integrity risks.

• Increasing Integration with Clinical and Research Ecosystems: Stem cell banks are increasingly embedding operations within hospital networks, research institutions, and therapy development pipelines. Around 45% of newly stored units are now contractually linked to clinical or translational research programs. Integrated data-sharing frameworks have improved sample utilization rates by nearly 22%, while collaborative storage agreements reduce redundant collections by approximately 18%. This trend strengthens the strategic positioning of stem cell banks as active participants in therapeutic development rather than passive storage providers.

The Stem Cell Banking Market is segmented by type, application, and end-user, reflecting diverse storage needs, utilization pathways, and institutional demand patterns. By type, differentiation is driven by cell origin and clinical usability, influencing storage duration, processing complexity, and regulatory requirements. Application-based segmentation highlights the transition from traditional transplant-focused use toward broader clinical, research, and personalized medicine workflows. End-user segmentation demonstrates a mixed landscape where hospitals and transplant centers coexist with research institutions and private family banking providers. Across segments, decision-making is shaped by factors such as long-term viability assurance, accreditation standards, automation readiness, and integration with downstream therapies. Understanding these segmentation dynamics enables stakeholders to align capacity planning, technology investment, and service models with evolving demand structures in the Stem Cell Banking Market.

Stem cell banking by type is primarily categorized into cord blood stem cells, cord tissue stem cells, adult stem cells, and embryonic stem cells. Cord blood stem cells currently account for approximately 48% of total stored units, driven by established clinical protocols for hematopoietic stem cell transplantation and standardized collection at birth. Cord tissue stem cells hold around 27% of adoption, benefiting from their higher mesenchymal stem cell concentration and expanding use in regenerative therapies. However, adult stem cell banking is growing fastest, supported by increasing autologous cell therapies and orthopedic applications, expanding at an estimated CAGR of 11.4%. Embryonic and niche-derived stem cells together represent the remaining 25%, primarily serving research-focused and highly regulated clinical programs.

By application, stem cell banking is segmented into clinical transplantation, regenerative medicine, research and drug development, and personalized or preventive healthcare. Clinical transplantation remains the leading application, accounting for nearly 46% of utilization, supported by consistent demand for hematological disorder treatments and immune system reconstitution procedures. Regenerative medicine applications hold approximately 29%, reflecting growing use in orthopedic, cardiovascular, and neurological therapy pipelines. Research and drug development is the fastest-growing application, expanding at an estimated CAGR of 12.1%, driven by rising numbers of cell-based clinical trials and translational research programs. Preventive and personalized healthcare applications collectively contribute around 25%, primarily through private family banking.

End-user segmentation of the Stem Cell Banking Market includes hospitals and transplant centers, research institutions, private family banking providers, and biotechnology companies. Hospitals and transplant centers lead with approximately 44% share, reflecting their central role in stem cell transplantation and regulated clinical use. Research institutions account for about 31%, supported by expanding academic and government-funded cell therapy programs. Private family banking providers represent around 19%, driven by parental awareness and preventive healthcare preferences. Biotechnology and pharmaceutical companies form the fastest-growing end-user group, expanding at an estimated CAGR of 13.2%, fueled by rising investment in cell and gene therapy pipelines.

North America accounted for the largest market share at 38.6% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2025 and 2032.

The global Stem Cell Banking Market demonstrates clear regional divergence driven by healthcare infrastructure maturity, regulatory frameworks, birth rates, and clinical adoption intensity. Europe followed North America with approximately 27.4% share, supported by strong public banking networks and regulatory-backed transplant programs. Asia-Pacific contributed nearly 24.1%, led by high annual birth volumes exceeding 70 million births, accelerating private banking adoption. South America and Middle East & Africa collectively represented around 9.9%, constrained by infrastructure gaps but supported by rising government-backed healthcare initiatives. Globally, over 40 million stem cell units are currently stored, with more than 55% concentrated in North America and Europe, while Asia-Pacific accounts for the highest annual additions, exceeding 4 million new units per year, highlighting its long-term expansion trajectory.

How is advanced clinical integration shaping long-term biobanking strategies?

North America holds approximately 38.6% of the global Stem Cell Banking Market, supported by mature healthcare systems and high clinical utilization. The region records over 25,000 stem cell transplants annually, driving sustained demand from hospitals and transplant centers. Government support through national donor programs and standardized accreditation frameworks has strengthened public banking capacity. Digital transformation is advanced, with over 65% of large banks using automated cryogenic storage and AI-based monitoring systems. A leading regional player has expanded automated vault capacity by 30%, improving retrieval accuracy and reducing manual handling risks. Consumer behavior reflects higher adoption of private banking among urban populations, with family banking penetration exceeding 45% in metropolitan areas, driven by preventive healthcare awareness.

Why is regulatory alignment influencing storage and utilization decisions?

Europe accounts for nearly 27.4% of global stem cell banking activity, led by Germany, the UK, and France, which together contribute over 60% of regional stored units. Strong public healthcare systems support centralized public stem cell banks, with over 500 accredited collection centers across the region. Regulatory bodies emphasize ethical sourcing, long-term traceability, and sustainability, accelerating adoption of explainable digital inventory systems. Advanced cryopreservation and energy-efficient cold storage technologies are used by more than 50% of European facilities. A prominent regional operator recently expanded cross-border sample exchange capabilities, increasing utilization efficiency by 18%. Consumer behavior shows higher reliance on public banking and regulated donation pathways compared to private-only storage models.

How are demographics and technology convergence accelerating adoption momentum?

Asia-Pacific ranks third in current market size at 24.1% but leads globally in annual volume growth. China, India, and Japan together contribute over 65% of regional storage additions, supported by high birth volumes and expanding middle-class healthcare spending. Infrastructure investments have increased processing capacity by nearly 40% over five years, with rapid deployment of modular biobank facilities. Innovation hubs in Singapore, South Korea, and Japan are advancing automation and digital consent platforms. A major regional provider processes more than 500,000 samples annually, reflecting scale-driven expansion. Consumer behavior is increasingly digital-first, with over 50% of new enrollments initiated through mobile platforms and online healthcare channels.

What role do healthcare modernization efforts play in shaping demand?

South America represents approximately 6.1% of the global Stem Cell Banking Market, led by Brazil and Argentina, which together account for nearly 70% of regional storage capacity. Expansion is supported by gradual healthcare infrastructure upgrades and growing private hospital networks. Government incentives aimed at improving transplant readiness have increased public bank participation by 15% in recent years. Energy-efficient cryogenic systems are being adopted to manage high operating costs. A regional private bank expanded collection partnerships across 120 hospitals, increasing national coverage significantly. Consumer behavior shows demand closely linked to private healthcare access and urban hospital concentration.

How are national healthcare initiatives enabling early-stage market development?

The Middle East & Africa region holds around 3.8% of the global Stem Cell Banking Market, with growth concentrated in the UAE, Saudi Arabia, and South Africa. National healthcare modernization programs and public-private partnerships are increasing awareness and storage capacity. More than 20 national transplant and biobanking initiatives are active across the region. Technological modernization includes centralized digital registries and automated cold-chain systems. A UAE-based stem cell center recently expanded national storage capacity by 25%, supporting domestic transplant demand. Consumer behavior reflects higher adoption among medical tourism hubs and government-supported healthcare beneficiaries.

United States Stem Cell Banking Market – 32.1% share: Dominance driven by high storage capacity, advanced clinical utilization, and strong regulatory-backed public and private banking infrastructure.

China Stem Cell Banking Market – 14.8% share: Leadership supported by large annual birth volumes, rapid private banking adoption, and expanding national regenerative medicine programs.

The Stem Cell Banking Market features a moderately consolidated competitive structure, with a mix of large multinational operators and regionally focused specialists. Globally, more than 120 active stem cell banking organizations operate across public and private models, ranging from hospital-affiliated public banks to privately owned family banking providers. The top five companies collectively account for approximately 55–60% of total stored stem cell units, reflecting scale advantages in infrastructure, accreditation, and clinical partnerships.

Competition is primarily shaped by storage capacity expansion, technology integration, geographic coverage, and service differentiation rather than pricing alone. Leading players operate facilities capable of storing 2–5 million samples each, supported by automated cryogenic vaults and redundant cold-chain systems. Strategic initiatives include multi-country partnerships with maternity hospitals, integration with regenerative medicine companies, and acquisitions to expand regional footprints. Over 40% of large operators have entered formal collaborations with biotech or cell-therapy developers to align storage services with downstream therapeutic pipelines.

Innovation is a key competitive lever. Around 65% of tier-one players have deployed AI-enabled monitoring, automated retrieval systems, or digital consent platforms to enhance compliance and operational efficiency. Mergers and capacity expansions remain active, with facility expansions averaging 20–30% increases in storage volume per project. Overall, competitive intensity is driven by scale, regulatory compliance strength, and technological sophistication rather than short-term market entry.

Cord Blood Registry (CBR)

Cryo-Cell International

ViaCord

Lifecell International

Vita 34

China Cord Blood Corporation

CryoHoldco

The Stem Cell Banking Market is increasingly driven by technological advancements that enhance sample integrity, operational efficiency, and regulatory compliance. A significant portion of leading facilities—over 70% of top-tier banks—have implemented automated cryogenic storage systems capable of maintaining ultra-low temperatures with redundant backup mechanisms. These systems support precise temperature stability within ±0.5°C and reduce manual intervention by more than 40%, directly improving long-term viability of stored stem cells. Enhanced digital chain-of-custody platforms are now standard in approximately 65% of advanced biobanks, enabling real-time tracking of sample movements and environmental conditions across distributed facilities. Emerging AI-enabled monitoring and predictive quality analytics have become a cornerstone of technology strategy. These systems analyze millions of data points from temperature, humidity, and liquid nitrogen sensors to anticipate anomalies and trigger alerts, reducing risk incidents by roughly 30%. In parallel, blockchain-based consent and record-keeping platforms are being piloted by nearly 25% of medium to large operators, providing immutable audit trails that strengthen regulatory compliance for long-term storage contracts.

High-throughput automated sample processing lines are reshaping operational workflows. These lines integrate robotics for intake, labeling, and storage placement, delivering up to 50% faster processing times compared to semi-manual methods. In addition, next-generation viability assays that quantify cellular health through multivariate imaging and molecular profiling are being adopted by over 35% of research-aligned banks, offering higher fidelity insights into stored unit quality. Technology ecosystems are also expanding around digital customer engagement tools. Mobile-enabled enrollment platforms and portals now facilitate consent, documentation, and status updates for over 55% of new private banking clients, aligning with broader digital healthcare trends. Together, these technologies are shaping a more resilient, transparent, and scalable Stem Cell Banking Market, providing competitive differentiation and operational resilience for industry leaders.

In September 2024, Cordlife Group obtained approval to resume its cord blood banking operations in Singapore under controlled conditions, allowing up to 30 new collections per month while it reinforces enhanced processing and monitoring systems to rebuild trust and operational robustness. (Cordlife)

In May 2024, Bioz partnered with WiCell to launch the Bioz Content Hub, an AI-driven platform providing real-time product citation insights for researchers accessing stem cell line data, improving data visibility and research workflows across academic and commercial segments.

As of end of 2024, ViaCord reported that 620 cord blood units were released to families for therapeutic use, with 48% used in transplants and 52% in regenerative medicine applications, underscoring practical clinical engagement of stored stem cells. (Parent's Guide to Cord Blood)

In September 2023, LifeCell International expanded its Community Cord Blood Stem Cell Registry to over 75,000 qualified cord blood units, enhancing donor match potential and community access for treatment of blood disorders and related conditions.

The scope of the Stem Cell Banking Market Report encompasses a comprehensive analysis of the global service ecosystem for cryogenic preservation and utilization of stem cells spanning a variety of biological sources, including umbilical cord blood, cord tissue, bone marrow, adipose tissue, and emerging derivatives such as placental and dental pulp. It covers segmentation by type, including private, public, and hybrid banking models, and product variants, with detailed breakdowns on processing, storage, collection, and transportation services.

Geographically, the report evaluates core regional dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing volume, adoption patterns, infrastructure readiness, regulatory frameworks, and end-user demand profiles across hospital networks, research institutions, private banking clientele, and biotech/pharmaceutical integration. Within applications, the report delineates usage in clinical transplantation, regenerative medicine, research and development, preventive healthcare, and personalized treatment pathways. It also includes technology assessment of cryopreservation innovations, digital monitoring systems, automated handling solutions, and quality compliance platforms shaping operational excellence.

Focus areas further extend to emerging niches such as community banking models, integration with genetic and genomic services, and value-added offerings linked to reproductive healthcare services. The report assesses competitive positioning, strategic initiatives, partnership activities, and service differentiation among active market participants. Industry trends, policy influences, accreditation impacts, customer behavior shifts, and infrastructure investment priorities are also analyzed, offering decision-makers a multi-dimensional perspective on market breadth and future strategic opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1917.8 Million |

|

Market Revenue in 2032 |

USD 3344.74 Million |

|

CAGR (2025 - 2032) |

7.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cord Blood Registry (CBR) , Cryo-Cell International , ViaCord , Lifecell International , Vita 34 , China Cord Blood Corporation , CryoHoldco |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |