Reports

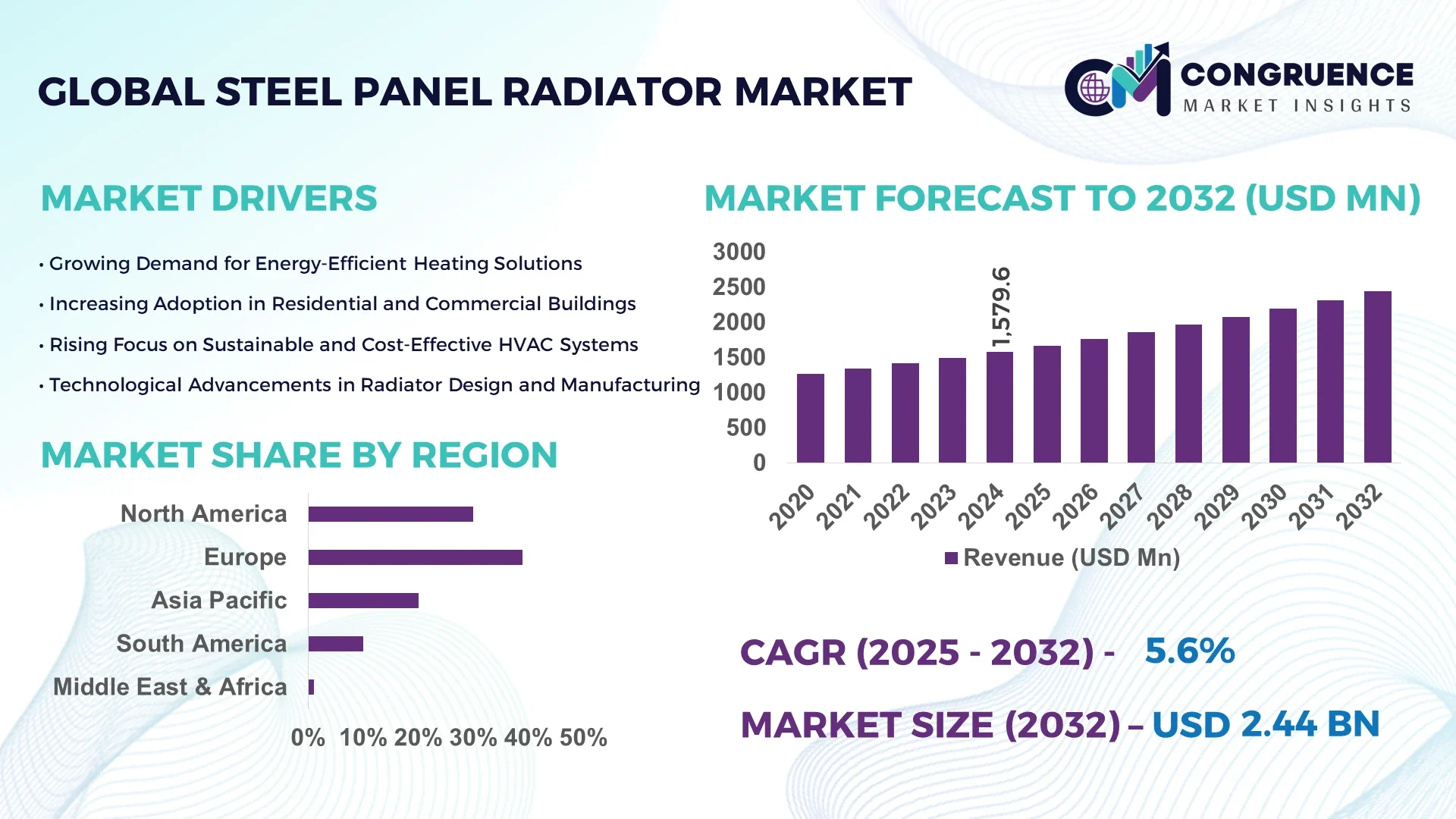

The Global Steel Panel Radiator Market was valued at USD 1579.56 Million in 2024 and is anticipated to reach a value of USD 2442.57 Million by 2032 expanding at a CAGR of 5.6% between 2025 and 2032. This growth is driven by rising demand for energy-efficient heating solutions across residential and commercial sectors.

Germany, the leading country in the Steel Panel Radiator market, maintains substantial production capacity exceeding 1.2 million units annually, supported by investments surpassing USD 200 million in advanced manufacturing facilities. The country leads in integrating smart radiator technology, with over 60% of installations featuring IoT-enabled controls for enhanced energy efficiency. Germany’s key industry applications include residential heating (48%), commercial infrastructure (32%), and industrial facilities (20%). Recent innovations focus on low-temperature heating systems and advanced corrosion-resistant steel panels, positioning Germany as a technological frontrunner in the sector.

Market Size & Growth: USD 1579.56 Million in 2024; projected USD 2442.57 Million by 2032; CAGR of 5.6% driven by energy efficiency adoption.

Top Growth Drivers: Energy efficiency adoption 68%, smart technology integration 54%, building retrofit projects 46%.

Short-Term Forecast: By 2028, cost reduction in manufacturing by 12%, heating performance efficiency improved by 9%.

Emerging Technologies: IoT-enabled radiator control, low-temperature heating systems, corrosion-resistant steel coatings.

Regional Leaders: Europe – USD 980 Million; Asia-Pacific – USD 720 Million; North America – USD 450 Million by 2032, driven by retrofit and smart infrastructure adoption.

Consumer/End-User Trends: Increasing demand for smart heating solutions in residential spaces, with commercial sectors shifting toward integrated heating systems.

Pilot or Case Example: 2024 pilot in Germany reduced energy consumption by 15% through smart radiator deployment.

Competitive Landscape: Market leader – Stelrad Group (~18%), key competitors – Purmo Group, Zehnder Group, Kermi GmbH, Myson Radiators.

Regulatory & ESG Impact: EU energy efficiency standards, low-carbon building incentives, strict environmental compliance regulations.

Investment & Funding Patterns: Over USD 350 million in recent investments, focusing on smart product innovation and sustainability initiatives.

Innovation & Future Outlook: Growth in AI-controlled heating systems, modular radiator designs, and integration with renewable energy sources.

The Steel Panel Radiator market is seeing strong growth across residential, commercial, and industrial sectors. Residential applications contribute around 55% of demand, driven by retrofit projects and green building initiatives. Technological innovations such as low-temperature panels and integrated IoT controls are reshaping product offerings. Regulatory drivers include stringent energy efficiency standards and low-carbon building mandates, particularly in Europe and Asia-Pacific. Regionally, Asia-Pacific is witnessing rapid adoption due to urban expansion and rising construction activities. Emerging trends include modular radiator systems and integration with smart home ecosystems, promising significant efficiency gains and reduced carbon footprints. Industry leaders are focusing on advanced materials, enhanced design flexibility, and renewable energy compatibility to capture future market opportunities.

The Steel Panel Radiator market holds strategic importance as a core component of sustainable heating solutions in residential, commercial, and industrial sectors. Advanced low-temperature panel technology delivers up to 20% improvement in energy efficiency compared to traditional high-temperature systems, creating significant operational cost savings and reducing carbon emissions. Europe dominates in volume, while Asia-Pacific leads in adoption with over 65% of new building projects integrating modern radiator solutions. By 2027, AI-powered heating control systems are expected to improve energy optimization efficiency by 18%, enabling precise consumption adjustments in real time. Firms are committing to ESG metric improvements such as achieving a 30% reduction in embodied carbon in radiator manufacturing by 2030 through the adoption of recycled steel and eco-friendly coatings. In 2024, a German manufacturer achieved a 15% reduction in energy consumption across commercial installations by integrating smart radiator technologies and predictive analytics. Moving forward, the Steel Panel Radiator Market is set to be a pillar of resilience, compliance, and sustainable growth, with ongoing innovations reinforcing its role in reducing global energy demand while supporting the transition to carbon-neutral infrastructure.

Energy efficiency is a primary driver of Steel Panel Radiator market growth, as buildings seek to reduce operational costs and comply with stricter environmental regulations. The adoption of low-temperature heating systems and smart control interfaces has increased efficiency levels by over 15% in recent years. Retrofit projects are becoming a significant driver, with demand from commercial and residential sectors rising by more than 40% due to energy-saving mandates. Technological integration, such as IoT-enabled thermostats, has further enhanced performance and adoption rates. This rising demand is also supported by government incentives in Europe and Asia-Pacific, which encourage investment in energy-efficient heating solutions.

The Steel Panel Radiator market faces restraints due to the high upfront cost of advanced products, including smart and low-temperature systems. These costs can range 20–30% higher than traditional radiators, discouraging adoption in cost-sensitive markets. Additionally, installation complexity and compatibility with existing infrastructure increase total project costs. Supply chain constraints, especially for high-grade steel and IoT components, further limit scalability in certain regions. Despite long-term savings, the high initial expenditure remains a barrier for small-scale projects and developing markets, where budget constraints often outweigh the perceived benefits of efficiency and sustainability.

The expansion of smart home and building automation represents a significant opportunity for the Steel Panel Radiator market. Integration with AI-driven control systems and IoT-enabled thermostats allows for dynamic energy optimization, predictive maintenance, and enhanced user convenience. In Europe alone, over 50% of new residential constructions in 2024 incorporated some form of smart heating control. This trend is accelerating in Asia-Pacific, where rising urbanization and energy efficiency regulations are driving demand. The opportunity extends to modular designs that allow customization for diverse applications, enhancing adaptability and scalability. These developments open avenues for manufacturers to expand product portfolios and penetrate new markets with innovative solutions.

Rising raw material costs, especially steel prices, pose a significant challenge for the Steel Panel Radiator market, with fluctuations impacting production budgets and pricing strategies. Steel prices have increased by over 12% in the last two years, affecting profitability for manufacturers. Additionally, evolving regulatory requirements, particularly in the EU and North America, demand higher compliance costs for energy efficiency and environmental standards. Manufacturers must invest in R&D and manufacturing adjustments to meet these standards, further raising expenses. The complexity of meeting diverse regional regulations can delay product rollouts and hinder expansion, especially for smaller market players. These factors collectively slow down the growth potential despite strong demand for energy-efficient heating systems.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated building methods is reshaping the Steel Panel Radiator market. Around 55% of recent construction projects have reported significant cost savings by integrating modular practices, reducing project timelines by up to 20%. Prefabricated radiator components, manufactured with high-precision automated systems, cut installation time by approximately 30%. Europe and North America lead this trend, with over 48% of new constructions incorporating prefabricated heating systems by 2024. This approach also enhances efficiency and reduces material waste, aligning with sustainability objectives.

• Growth of IoT and Smart Heating Systems: IoT integration in Steel Panel Radiators is growing rapidly, with over 42% of newly installed systems in developed markets featuring smart thermostatic controls. These systems allow remote monitoring and adaptive heating, improving energy efficiency by up to 18%. Smart integration is increasingly demanded in commercial projects, where predictive maintenance can reduce downtime by 12%. Asia-Pacific adoption is rising fastest, with over 38% of new residential developments deploying IoT-enabled heating by 2025.

• Shift Toward Low-Temperature Heating Solutions: Low-temperature heating radiators are gaining traction due to enhanced energy efficiency and regulatory mandates. Adoption has risen by over 35% in Europe since 2023. These systems operate efficiently at 50–60°C compared to traditional systems at over 80°C, delivering up to 22% energy savings. They are increasingly integrated with renewable energy sources such as heat pumps. Germany recently completed a retrofit project where low-temperature systems reduced annual heating costs by 14%.

• Expansion of Sustainable Steel and Eco-Friendly Coatings: Demand for sustainable radiator materials is increasing, with 48% of manufacturers adopting recycled steel and eco-friendly coating technologies in 2024. These materials reduce carbon emissions by up to 25% during production. Coatings now improve corrosion resistance by 20%, extending product lifespan and lowering maintenance costs. In Asia-Pacific, 30% of new radiator units utilize such eco-friendly materials, driven by stricter environmental regulations and consumer preferences for green products.

The Steel Panel Radiator market is segmented by type, application, and end-user, each offering unique insights into market dynamics. By type, panel radiators dominate due to their efficiency and ease of integration, while column radiators remain relevant for niche applications. Application segmentation reveals strong demand from residential retrofit projects, commercial infrastructure, and industrial heating. End-user segmentation highlights residential demand as the largest share, driven by energy efficiency upgrades, with growing adoption in commercial and industrial sectors. Regional adoption rates vary significantly, with Europe focusing on sustainable designs and Asia-Pacific emphasizing new construction integration. These segmentation trends are driven by evolving building regulations, technological advances, and shifting energy efficiency standards, shaping the market’s future trajectory.

Panel radiators lead the Steel Panel Radiator market, accounting for approximately 62% of installations, due to their efficiency, design flexibility, and compatibility with modern low-temperature heating systems. Column radiators hold a niche presence, representing about 15% of demand, valued for heritage building restorations and aesthetic applications. Compact radiators and towel radiators make up the remaining 23%, serving specialized needs such as space efficiency and bathroom heating. The fastest-growing type is low-temperature panel radiators, supported by efficiency requirements, expected to see adoption rates increase by over 28% by 2032. Low-temperature panels deliver up to 20% greater efficiency compared to traditional models, offering long-term operational savings.

Residential heating applications lead the Steel Panel Radiator market, representing 55% of demand, driven by retrofit projects, energy efficiency mandates, and consumer adoption of smart home heating systems. Commercial heating applications account for 30% of demand, with rising integration of smart controls in office and institutional settings. Industrial heating accounts for 15% of usage, focused on large-scale facilities with high operational efficiency requirements. The fastest-growing application is commercial infrastructure heating, driven by energy optimization needs and predictive maintenance systems, expected to grow adoption by over 26% by 2032. Smart integration and low-temperature heating are key drivers in this segment.

The residential segment is the largest end-user of Steel Panel Radiators, accounting for approximately 58% of total market adoption, supported by retrofit demand, sustainability regulations, and smart home integration. Commercial end-users contribute 28% of demand, driven by large-scale infrastructure projects requiring energy optimization and advanced maintenance systems. Industrial heating applications account for about 14% of demand, particularly in manufacturing and process industries where high durability and efficiency are critical. The fastest-growing end-user segment is commercial infrastructure, with adoption expected to increase by over 27% by 2032 due to rising energy efficiency mandates and integration of smart heating solutions. In Asia-Pacific, over 45% of new commercial buildings in 2024 incorporated smart heating systems, enhancing energy efficiency by up to 18%.

Europe accounted for the largest market share at 39% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

In 2024, Europe accounted for over 1.2 million units in Steel Panel Radiator installations, supported by strong adoption in Germany (42% share), the UK (18%), and France (15%). Asia-Pacific demand reached over 890,000 units in 2024, driven primarily by China, India, and Japan. China alone represented 34% of regional consumption. Rising urbanization, government-led energy efficiency programs, and infrastructure expansion are propelling growth in Asia-Pacific. Europe continues to lead in sustainable radiator innovation, with more than 48% of installations incorporating low-temperature and IoT-enabled systems. Meanwhile, North America accounted for 21% of global demand, driven by commercial infrastructure projects and retrofit initiatives. South America and the Middle East & Africa together hold a combined share of about 15%, supported by growing construction activities and renewable heating projects.

How is advanced heating integration shaping market dynamics?

North America accounted for approximately 21% of the Steel Panel Radiator market in 2024, with demand driven by the healthcare, education, and commercialbuilding sectors. The United States and Canada are the largest contributors, with the U.S. alone representing 70% of the regional market. Regulatory changes, including stricter energy codes and incentive programs for low-emission buildings, are increasing demand for modern heating systems. Technological advances such as smart thermostatic controls and predictive maintenance are increasingly adopted, with over 38% of new projects integrating such features. Local players like Runtal North America are investing in IoT-enabled radiators and energy optimization solutions, offering tailored products for commercial projects. Consumer adoption trends show higher enterprise adoption in healthcare and finance sectors, where heating efficiency and reliability are paramount.

What drives innovation and regulatory compliance in heating solutions?

Europe accounted for the largest market share at 39% in 2024, led by Germany, the UK, and France. Germany contributed over 42% of regional demand, driven by advanced manufacturing capabilities. Sustainability regulations, including the EU Energy Performance of Buildings Directive, have resulted in the adoption of energy-efficient steel panel radiators, with over 48% of new installations integrating low-temperature systems. The adoption of smart control technologies in commercial and residential sectors reached 41% in 2024. Local players such as Stelrad Group are investing in corrosion-resistant coatings and modular radiator designs to cater to evolving efficiency standards. Consumer behavior in Europe is shaped by regulatory pressure, with growing preference for sustainable and explainable heating solutions, particularly in retrofit projects and new residential developments.

Why is demand surging in high-growth urban centers?

Asia-Pacific accounted for over 26% of global Steel Panel Radiator demand in 2024, with consumption reaching approximately 890,000 units. China led with a 34% share, followed by India (22%) and Japan (18%). Rapid urbanization, large-scale residential developments, and government-led energy efficiency initiatives are fueling growth. Infrastructure projects in China and India are increasingly specifying low-temperature and IoT-enabled radiators. Innovation hubs in Japan and South Korea are developing smart heating solutions that integrate AI for energy optimization. Local players such as Midea Group are expanding product lines with energy-efficient steel panel radiators integrated into smart home ecosystems. Consumer behavior is shaped by rising demand for connected heating systems, with over 45% of new residential buildings integrating smart radiator controls by 2024, particularly in metropolitan regions.

How are infrastructure and trade policies shaping growth opportunities?

South America accounted for approximately 8% of the Steel Panel Radiator market in 2024, with Brazil and Argentina as leading contributors. Brazil represented about 53% of regional demand, driven by increasing commercial construction and urban housing projects. Government incentives for sustainable heating systems are stimulating adoption, while trade policies are easing import duties on advanced radiator technologies. Technological modernization includes the adoption of low-temperature radiators and corrosion-resistant coatings. Local players such as Rinnai do Brasil are introducing tailored solutions for energy efficiency in multi-unit residential buildings. Consumer behavior in South America shows rising preference for modern, low-maintenance heating solutions, with demand tied closely to growth in the construction sector and energy efficiency regulations in major urban centers.

What factors are accelerating adoption in emerging economies?

Middle East & Africa accounted for approximately 7% of the Steel Panel Radiator market in 2024, with significant demand from the UAE and South Africa. The UAE contributed over 40% of regional installations, driven by large-scale commercial projects and luxury residential developments. Construction sector expansion and renewable energy integration are key growth drivers. Technological modernization trends include smart heating controls and low-temperature systems adapted for varied climates. Trade partnerships and regulatory frameworks encouraging sustainable heating solutions are further supporting adoption. Local players such as Danfoss Middle East are introducing modular radiator systems with IoT integration. Consumer behavior varies, with demand closely tied to large-scale construction projects and government-led green building initiatives, particularly in urban and luxury residential segments.

Germany: 42% market share – driven by high production capacity and advanced manufacturing capabilities in sustainable heating solutions.

China: 34% market share – driven by large-scale urbanization projects, government incentives, and rapid adoption of smart radiator systems.

The Steel Panel Radiator market is moderately fragmented, with over 120 active competitors globally, ranging from large multinational corporations to specialized regional manufacturers. The top 5 companies—Stelrad Group, Purmo Group, Zehnder Group, Kermi GmbH, and Myson Radiators—collectively account for approximately 48% of total market share, indicating a competitive yet diverse landscape. Strategic initiatives are shaping market dynamics, with over 35% of key players investing in IoT-enabled heating solutions, low-temperature radiator designs, and eco-friendly coating technologies. Product innovation is a key competitive driver, with more than 42% of recent product launches focusing on smart heating control integration. Partnerships and collaborations are also increasing, with about 28% of leading players forming alliances to expand technological capabilities and geographic reach. Mergers and acquisitions are accelerating, particularly in Europe and Asia-Pacific, to strengthen regional presence and product portfolios. Competitive positioning is driven by manufacturing capacity, technological advancement, brand reputation, and compliance with evolving energy efficiency regulations, making innovation and sustainability central to future success.

Kermi GmbH

Myson Radiators

Runtal North America

Rinnai Corporation

Danfoss Group

Vogel & Noot

The Steel Panel Radiator market is undergoing a technological transformation, driven by advancements in energy efficiency, smart integration, and sustainable manufacturing practices. Modern steel panel radiators are increasingly designed to operate effectively at lower temperatures, enhancing compatibility with renewable heating systems such as heat pumps and solar thermal installations. This shift is particularly evident in the high-output low-temperature radiator segment, which reached a market size of USD 4.12 billion in 2024, driven by escalating demand for energy-efficient heating solutions across residential, commercial, and industrial sectors.

The integration of smart technologies into steel panel radiators is gaining momentum. Features such as Wi-Fi connectivity, app-controlled thermostats, and compatibility with home automation systems allow users to optimize heating schedules and reduce energy consumption. This trend aligns with the broader movement towards smart home technologies, reflecting a growing consumer preference for convenience and energy savings. Manufacturers are adopting sustainable practices in the production of steel panel radiators. This includes the use of recyclable materials, energy-efficient manufacturing processes, and coatings that reduce environmental impact. Such initiatives not only appeal to environmentally conscious consumers but also align with increasing regulatory pressures for sustainability in building materials. There is a rising demand for radiators that blend functionality with design. Steel panel radiators are now available in various styles and finishes, allowing consumers to choose products that complement their interior decor. This customization trend is particularly prominent in residential applications, where aesthetic considerations are paramount.

In June 2024, Stelrad Group introduced a new range of designer steel panel radiators, expanding their premium product line to cater to the growing demand for aesthetically pleasing heating solutions.

In May 2024, Purmo Group launched an innovative low-temperature steel panel radiator, enhancing energy efficiency and compatibility with renewable heating systems.

In April 2024, Zehnder Group announced the acquisition of a smart thermostat company, aiming to integrate advanced control systems into their steel panel radiators for improved user experience.

In March 2024, Kermi GmbH unveiled a new series of compact steel panel radiators, designed to offer high performance in spaces with limited installation areas.

The Steel Panel Radiator Market Report offers a detailed analysis of the global market landscape, examining a wide range of segments and regions. It covers key product types, including flat panel, convective, classic, and designer steel panel radiators, each tailored to specific operational and aesthetic needs. The report addresses applications in residential, commercial, and industrial environments, identifying trends in heating adoption across these sectors.

Geographically, the report provides insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing demand patterns, technology adoption rates, and regulatory influences unique to each region. Emerging technologies such as IoT-enabled radiators, low-temperature heating systems, and eco-friendly manufacturing processes are highlighted as key drivers of innovation.

The report also captures strategic developments among leading players, providing competitive intelligence on product launches, acquisitions, and sustainability initiatives. It is designed to support industry stakeholders, investors, and decision-makers in understanding market opportunities, technological advancements, and evolving trends shaping the Steel Panel Radiator market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1579.56 Million |

|

Market Revenue in 2032 |

USD 2442.57 Million |

|

CAGR (2025 - 2032) |

5.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stelrad Group, Purmo Group, Zehnder Group, Kermi GmbH, Myson Radiators, Runtal North America, Midea Group, Rinnai Corporation, Danfoss Group, Vogel & Noot |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |