Reports

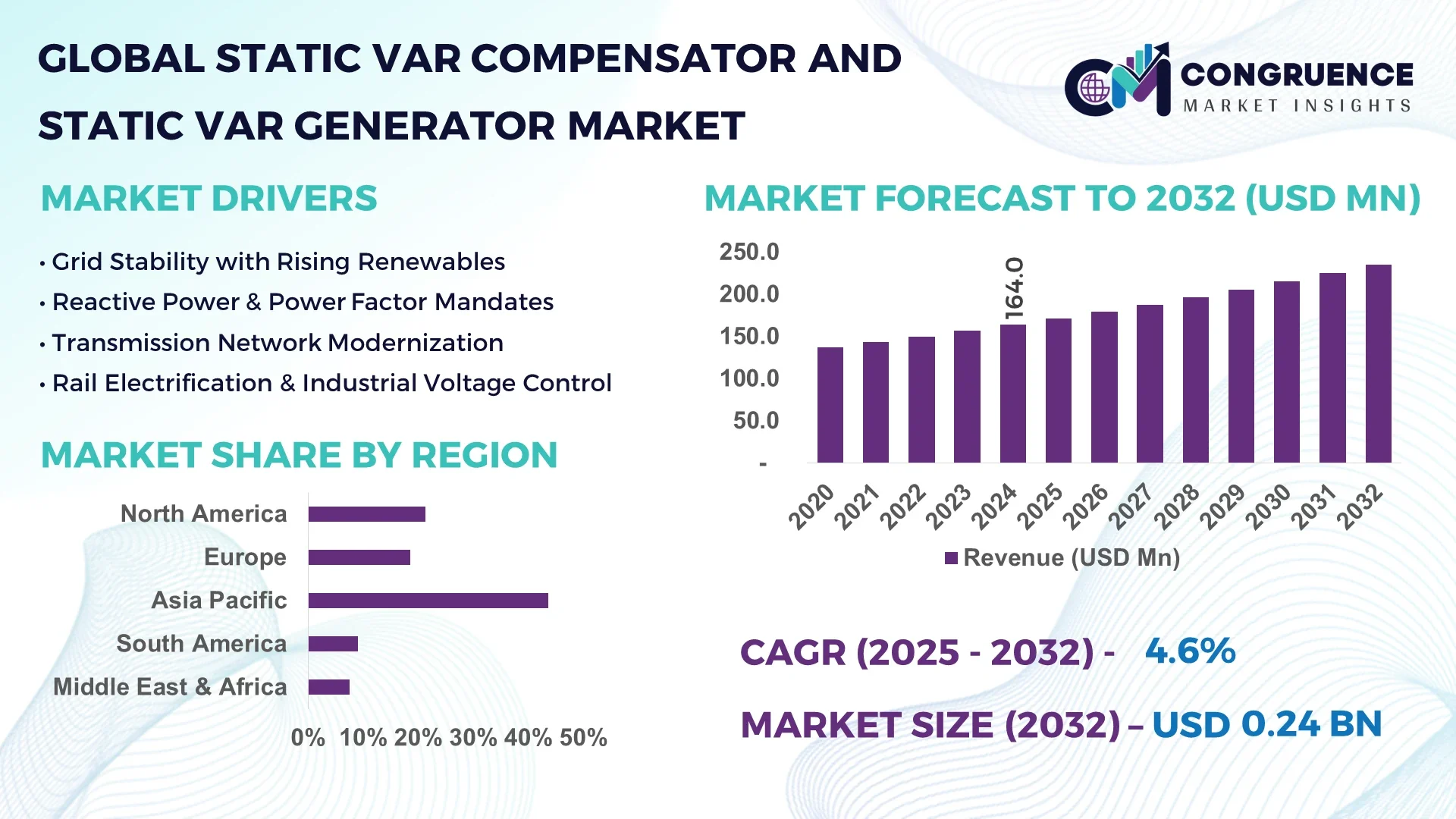

The Global Static Var Compensator and Static Var Generator Market was valued at USD 164.0 Million in 2024 and is anticipated to reach a value of USD 235.0 Million by 2032, expanding at a CAGR of 4.6% between 2025 and 2032.

China leads in the production capacity of Static Var Compensators and Static Var Generators, with substantial state-backed investments in smart grid infrastructure and high-voltage power transmission. The country boasts advanced local manufacturing hubs in provinces such as Jiangsu and Guangdong, where the integration of AI-enhanced control systems has significantly improved energy efficiency across utilities and large-scale industrial zones.

The Static Var Compensator and Static Var Generator Market is driven by robust demand across sectors such as power utilities, steel manufacturing, rail transportation, and renewable energy. These systems are instrumental in enhancing grid stability, reactive power compensation, and voltage regulation. Technological advancements such as thyristor-controlled reactors, digitally enabled control modules, and modular architectures are transforming the market landscape. Regulatory focus on grid modernization and emission reduction is further reinforcing deployment, especially across Asia-Pacific and Europe. Increasing investment in solar and wind power infrastructure has fueled demand for SVGs in particular, as they offer rapid response times and minimal harmonic distortion. Moreover, the integration of energy storage solutions and the expansion of high-voltage direct current (HVDC) systems have underscored the market’s strategic importance. Looking ahead, adoption of AI and IoT-driven control systems, regional industrial electrification, and cross-border interconnectivity will significantly influence market direction and innovation cycles.

Artificial Intelligence (AI) is reshaping the operational, diagnostic, and predictive maintenance aspects of the Static Var Compensator and Static Var Generator Market. By enabling real-time performance analytics and condition monitoring, AI technologies allow grid operators and utilities to optimize reactive power flow, reduce harmonic disturbances, and extend equipment life. Advanced machine learning algorithms are being embedded within SVG and SVC controllers, enabling automated tuning and self-adaptive load balancing based on grid demand variations. These AI-enhanced systems deliver faster response times, improved power factor correction, and lower total harmonic distortion across complex transmission environments. AI also facilitates remote diagnostics and cloud-based firmware updates, which minimize downtime and manual interventions.

In industrial applications, AI-driven analytics are improving dynamic voltage regulation performance by detecting transient anomalies and adjusting var output preemptively. Power utilities benefit from AI-enabled predictive maintenance, which uses historical equipment data to forecast potential failure points, thereby preventing outages. Additionally, digital twins are being developed to simulate operating environments of static var systems, supporting system design optimization and training. As grid complexity increases due to renewable integration, AI ensures that SVC and SVG technologies remain agile, responsive, and efficient across evolving load conditions.

"In 2025, a leading Chinese power technology firm implemented AI-driven condition monitoring in over 120 SVG units deployed across ultra-high voltage substations. This upgrade reduced system-level reactive power fluctuations by 22% and improved dynamic response time by 17 milliseconds compared to conventional systems."

The Static Var Compensator and Static Var Generator Market is characterized by rapid technological progress, grid modernization mandates, and an increasing need for power quality assurance. With the global shift toward renewables, particularly solar and wind, utilities are investing heavily in reactive power management systems to stabilize fluctuating voltage and frequency conditions. Simultaneously, industries such as steel, petrochemical, and transportation are deploying SVGs and SVCs to mitigate harmonics and optimize energy use. The market is also experiencing regulatory pressure for energy efficiency, leading to a surge in demand for smart, compact, and digitally integrated solutions. Environmental compliance, particularly in Europe and East Asia, is further catalyzing innovation in low-loss and eco-friendly compensator designs.

Governments worldwide are investing in smart grid infrastructure to improve grid resilience and efficiency. These initiatives are directly increasing demand for the Static Var Compensator and Static Var Generator Market, as these systems are vital for maintaining voltage stability and reactive power balance. In India, for instance, the Green Energy Corridor project involves large-scale deployment of SVCs and SVGs to integrate renewable energy with the national grid. Similarly, the U.S. Department of Energy’s funding under the Grid Resilience and Innovation Partnerships (GRIP) program includes support for power flow control systems like SVGs. These efforts are leading to broader adoption of modular and AI-enabled var compensators.

The deployment of Static Var Compensators and Static Var Generators often requires substantial capital investment, particularly for high-capacity and digitally integrated systems. Installation complexity, along with the need for precise system design and tuning, can pose technical hurdles for grid operators and industries. Smaller utilities and mid-sized manufacturing firms may hesitate to adopt such technologies due to upfront expenses and the necessity of skilled workforce for commissioning. Moreover, legacy grid infrastructure in developing regions may require costly upgrades to accommodate advanced var compensation equipment, limiting market penetration despite long-term benefits.

As nations transition to cleaner energy sources, SVG and SVC technologies are becoming critical for integrating variable power from wind and solar farms into the grid. These technologies help in voltage stabilization and power quality enhancement, making them essential in utility-scale renewable installations. For example, offshore wind farms in the UK and Germany are increasingly using SVG systems to manage rapid power fluctuations and maintain synchronization. With more than 300 GW of new renewable capacity projected globally by 2027, there is significant growth potential for var compensation technologies, especially those capable of fast-response and grid-code compliance.

Despite technological advancements, a key challenge in the Static Var Compensator and Static Var Generator Market is the shortage of trained professionals for system design, integration, and maintenance. SVGs and SVCs require complex calibration and real-time monitoring, often demanding cross-disciplinary knowledge in power electronics, control systems, and software. Furthermore, compatibility issues arise when integrating modern var compensation units with aging transmission infrastructure or diverse grid codes across countries. These factors can delay project timelines, increase operational risks, and drive up overall deployment costs, particularly in multi-vendor environments.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Static Var Compensator and Static Var Generator Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical. Utilities are increasingly specifying pre-configured var compensation modules to accelerate deployment and reduce commissioning errors.

Integration of IoT and Cloud Monitoring Systems: Modern SVC and SVG systems are being embedded with IoT sensors and cloud-based monitoring platforms that provide continuous performance diagnostics. These platforms deliver predictive maintenance alerts, usage statistics, and firmware updates, reducing downtime by up to 28% and optimizing system longevity. North America leads this transition with over 60% of new installations incorporating remote data access and analytics capabilities by mid-2025.

Deployment in High-Speed Rail and Metro Networks: Rapid urbanization is driving investment in high-speed electric rail networks, particularly in China, India, and parts of the Middle East. SVCs are being deployed extensively in these networks to stabilize voltage and reduce harmonics. By 2025, more than 150 new high-speed rail projects globally are expected to include var compensation systems as part of their core electrical design standards.

Focus on Environmentally Friendly and Compact Designs: Environmental compliance and space constraints are prompting a shift toward compact, eco-efficient SVC/SVG units. Dry-type capacitors and advanced semiconductors are replacing older oil-based components. Manufacturers are prioritizing sustainable material sourcing and lower heat emissions, especially for indoor installations in densely populated regions like Japan and South Korea. These green innovations are reducing system footprint by up to 35%.

The Static Var Compensator and Static Var Generator Market is segmented based on type, application, and end-user. Each segment plays a critical role in shaping the competitive and operational dynamics of the industry. Product-wise, technological evolution and performance requirements influence adoption rates across voltage levels and installation types. Application areas span a wide range of sectors, with power infrastructure and heavy industry representing major demand hubs. From an end-user perspective, growth is driven by the increasing need for stable and efficient power flow, particularly in energy-intensive and grid-sensitive industries. The segmentation also reflects emerging demand from renewable energy installations and urban infrastructure development, underscoring the market’s expanding footprint. These segments collectively define market performance by aligning solutions with specialized power system requirements, operational environments, and compliance needs.

The Static Var Compensator and Static Var Generator Market includes several types such as Thyristor-Based SVCs (TSC and TCR), Mechanically Switched Capacitor systems (MSC), and Static Var Generators (SVG). Among these, Static Var Generators (SVG) are currently leading the market due to their fast response time, low harmonic emission, and adaptability in modern grid systems. SVGs provide superior dynamic performance, especially in renewable energy installations and industrial automation settings.

The fastest-growing type is also SVG, primarily due to increased integration with smart grids and renewable energy sources. Their ability to operate efficiently under a wide range of load conditions and respond instantly to voltage fluctuations makes them a preferred choice for utilities and renewable operators.

Thyristor-Controlled Reactors (TCR) and Thyristor-Switched Capacitors (TSC) remain relevant, particularly in traditional grid setups and high-voltage transmission environments where large reactive power control is necessary. Mechanically Switched Capacitor (MSC) systems hold a niche role in cost-sensitive, fixed-load applications but are gradually being overshadowed by digital alternatives.

Key applications in the Static Var Compensator and Static Var Generator Market include power generation and transmission, steel and metal manufacturing, railway electrification, oil and gas refineries, and renewable energy integration. Among these, power generation and transmission is the dominant application, as maintaining voltage stability and reactive power compensation is essential for modern electricity grids. SVCs and SVGs are critical in preventing voltage collapse and supporting peak demand requirements.

The fastest-growing application is renewable energy integration, driven by global energy transition efforts and the need to stabilize output from intermittent sources like solar and wind. SVGs are especially favored in this area due to their dynamic and responsive nature, ensuring consistent power quality under fluctuating conditions.

Steel and heavy industrial manufacturing continues to rely on var compensation for mitigating voltage flicker and harmonics, while railway electrification projects, particularly high-speed and metro networks, are expanding the market with dedicated compensation systems integrated into substations and traction systems. Oil and gas applications maintain a steady demand due to the sector's reliance on high-load electrical equipment and sensitive power systems.

The Static Var Compensator and Static Var Generator Market serves a diverse range of end users, including utilities, industrial sectors, transportation infrastructure, and renewable energy developers. Utilities represent the leading end-user segment due to the widespread need for grid stability, voltage regulation, and reactive power control across national and regional transmission systems. These organizations deploy large-scale SVG and SVC units to manage load fluctuations and integrate diverse energy sources.

The fastest-growing end-user group is renewable energy developers, who require efficient var compensation to maintain power quality in utility-scale solar and wind installations. As new capacity additions grow globally, especially in offshore wind and hybrid solar-storage projects, the demand for compact, digitally managed SVG units is increasing.

Heavy industries, including steel and petrochemical plants, continue to play a crucial role in the market due to their high reactive power demand and susceptibility to voltage instability. Additionally, transportation authorities investing in electric rail and metro projects are emerging as significant contributors, integrating var compensators within electrification infrastructure to ensure power quality and system longevity.

Asia-Pacific accounted for the largest market share at 43.6% in 2024; however, the Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2025 and 2032.

The Asia-Pacific region benefits from large-scale industrialization, rapid urban infrastructure growth, and substantial investment in smart grid systems, particularly in China and India. Meanwhile, the Middle East & Africa region is undergoing rapid energy diversification, including renewable energy integration and power infrastructure modernization, especially in countries like the UAE and South Africa. These regional trends are transforming market dynamics, driving demand for advanced static var compensators and generators. Both regions exhibit high deployment potential due to increased electricity consumption, voltage regulation requirements, and the rollout of next-generation grid technologies.

In 2024, North America held approximately 21.3% of the global Static Var Compensator and Static Var Generator Market. The United States is the dominant contributor, supported by a strong base of electric utility companies and energy-intensive industries. Key sectors such as steel production, semiconductor manufacturing, and data centers are driving demand for var compensation technologies to stabilize voltage and reduce harmonic distortions. Government support programs like grid resiliency grants and decarbonization initiatives are further accelerating adoption. Technological upgrades across transmission networks and the rollout of AI-enabled predictive maintenance systems have improved operational performance. The increasing penetration of renewable power sources and electric vehicle charging infrastructure is prompting utilities to integrate dynamic compensation systems, creating a stable demand pipeline across the region.

Europe accounted for roughly 18.5% of the global Static Var Compensator and Static Var Generator Market in 2024. Germany, the UK, and France are the primary markets, driven by sustainability commitments and high penetration of renewables in the national grid. European regulatory bodies, including ENTSO-E and EU Clean Energy for All Europeans Package, have established grid codes requiring dynamic reactive power compensation in renewable projects. Investments in offshore wind and smart substation technologies are pushing demand for SVG units with fast response capabilities. Countries across the region are adopting wide-scale digital grid technologies, including AI-driven diagnostics and modular var compensator systems. These efforts are reinforcing system reliability and facilitating the clean energy transition across the European grid landscape.

Asia-Pacific recorded the highest volume of installations and held the largest share in 2024 at 39.6%. China, India, and Japan are the major consumers of Static Var Compensators and Generators due to high industrial activity, expanding railway electrification, and large-scale power grid modernization. China continues to deploy these systems across ultra-high-voltage substations to manage massive transmission volumes, while India is incorporating SVGs into its green energy corridors and solar park infrastructure. Japan is emphasizing precision var control in urban power grids. Technological innovation hubs in South Korea and China are driving AI-based monitoring and IoT-integrated compensator development, enabling real-time analytics and reduced maintenance costs. The region's growth is also supported by state-owned utility reforms and significant public-private investment in electric infrastructure.

Brazil and Argentina are leading the Static Var Compensator and Static Var Generator Market in South America. The region's overall market share was approximately 9.1% in 2024. Investments in high-voltage transmission lines, substation automation, and renewable energy integration are key trends shaping demand. Brazil’s continued development of solar and wind energy clusters has increased the deployment of reactive power compensation systems to maintain grid reliability. Government-backed energy transition plans, including modernization of the power sector and public-private partnerships in grid stability initiatives, are driving steady uptake. Argentina’s industrial growth, particularly in metallurgy and chemicals, is also encouraging adoption of SVCs and SVGs in localized power management. Importantly, trade incentives for power equipment and regional interconnection programs are further enhancing market prospects.

The Middle East & Africa region is emerging as the fastest-growing market for Static Var Compensator and Static Var Generator technologies, with significant demand driven by oil & gas, construction, and renewable energy sectors. Countries such as the UAE and Saudi Arabia are investing heavily in grid modernization to support diversified energy portfolios that include solar, hydrogen, and thermal storage. South Africa is deploying SVCs in its national grid to address stability challenges caused by aging infrastructure and rising peak loads. Technological modernization is advancing rapidly, with smart substations, digital controllers, and AI-based grid analytics becoming standard in new installations. Local governments are promoting trade partnerships and incentivizing technology transfer to build domestic capabilities in power equipment manufacturing and deployment, creating a long-term growth trajectory for var compensator solutions in the region.

The Static Var Compensator and Static Var Generator Market is characterized by moderate to high competition, with more than 30 active players globally operating across multiple regions. Key market participants are strategically positioning themselves through technology-driven innovations, customized solutions, and long-term supply contracts with utilities and industrial clients. Several leading companies are focusing on expanding their manufacturing capacity and deploying advanced control systems integrated with digital communication protocols. The competitive landscape is being reshaped by a wave of strategic partnerships, such as grid modernization alliances and region-specific distribution agreements. Notably, product differentiation through compact design, modular architecture, and faster response times has become a focal point for competitive advantage. Market incumbents are increasingly adopting AI-based monitoring, IoT-enabled diagnostics, and predictive maintenance platforms to offer added value. Furthermore, mergers and acquisitions are being used as growth tactics to strengthen technological capabilities and geographic reach, particularly in high-growth markets such as Asia-Pacific and the Middle East.

ABB Ltd.

Siemens Energy

General Electric

Mitsubishi Electric Corporation

NR Electric Co., Ltd.

Toshiba Energy Systems & Solutions Corporation

American Superconductor Corporation

Hyosung Heavy Industries

Rongxin Power Electronic Co., Ltd.

Nidec Industrial Solutions

RXHK Power Electronics

Eaton Corporation

Beijing In-power Electric Co., Ltd.

The technology landscape of the Static Var Compensator (SVC) and Static Var Generator (SVG) Market is rapidly evolving, driven by the integration of intelligent electronics, real-time control algorithms, and compact system design. SVC systems, traditionally based on thyristor-controlled reactors and capacitors, are now incorporating digital triggering systems to improve accuracy and reduce losses. Modern SVGs employ voltage source converters (VSC) using IGBT or IGCT-based technology, which offers rapid response times below 5 milliseconds and precise reactive power compensation. These technologies are increasingly embedded with IoT modules that enable remote diagnostics, performance monitoring, and predictive maintenance. AI-based control systems are being used to dynamically adjust var injection in response to real-time load conditions. The adoption of modular, containerized SVG systems is rising, especially in distributed power grids and renewable energy parks. Additionally, hybrid systems combining both SVC and SVG functionalities are emerging, offering flexibility in both steady-state and dynamic voltage regulation. Utility-scale installations are seeing the use of fiber-optic communication networks and digital substation frameworks to optimize integration with SCADA systems. Technology trends indicate a clear move toward scalable, maintenance-efficient solutions that support grid stability in environments with high renewable energy penetration and fluctuating load conditions.

• In February 2024, Siemens Energy launched a new series of hybrid SVC systems combining STATCOM and traditional SVC modules for dynamic grid applications, targeting smart grid deployments across Europe and Asia.

• In October 2023, ABB Ltd. signed a long-term agreement with a major Middle Eastern utility to deliver over 30 modular SVG units integrated with AI-enabled performance analytics to improve substation efficiency.

• In March 2024, Mitsubishi Electric introduced a compact static var generator designed for offshore wind farms, with water-cooled systems and space-saving architecture suited for floating platforms.

• In July 2023, GE Grid Solutions commissioned a large-scale SVC project in India’s renewable energy corridor, stabilizing over 2,000 MW of wind and solar capacity with advanced dynamic compensation systems.

The Static Var Compensator and Static Var Generator Market Report offers a comprehensive analysis of the market's full spectrum, spanning multiple technologies, applications, and regional landscapes. The scope includes coverage of all major types such as thyristor-based SVCs, voltage source converter-based SVGs, and emerging hybrid compensator systems. The report segments the market by application areas including power transmission, industrial manufacturing, railway electrification, and renewable energy grid integration. End-users analyzed include electric utilities, heavy industrial sectors, transportation authorities, and renewable energy operators. Geographically, the report provides focused insights into key regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—highlighting specific market trends, regulatory frameworks, and technological adoption patterns. It also touches on niche and emerging segments, such as offshore renewable installations, microgrids, and AI-enabled compensation technologies. The report identifies market drivers like energy decentralization, smart grid expansion, and grid stability concerns as primary influencers of demand. It offers decision-makers a structured and insightful view into the market's present dynamics and potential future shifts.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 164.0 Million |

| Market Revenue (2032) | USD 235.0 Million |

| CAGR (2025–2032) | 4.6 % |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End‑User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technological Trends, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia‑Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ABB Ltd., Siemens Energy, General Electric, Mitsubishi Electric Corporation, NR Electric Co., Ltd., Toshiba Energy Systems & Solutions Corporation, American Superconductor Corporation, Hyosung Heavy Industries, Rongxin Power Electronic Co., Ltd., Nidec Industrial Solutions, RXHK Power Electronics, Eaton Corporation, Beijing In-power Electric Co., Ltd. |

| Customization & Pricing | Available on Request (10 % Customization is Free) |