Reports

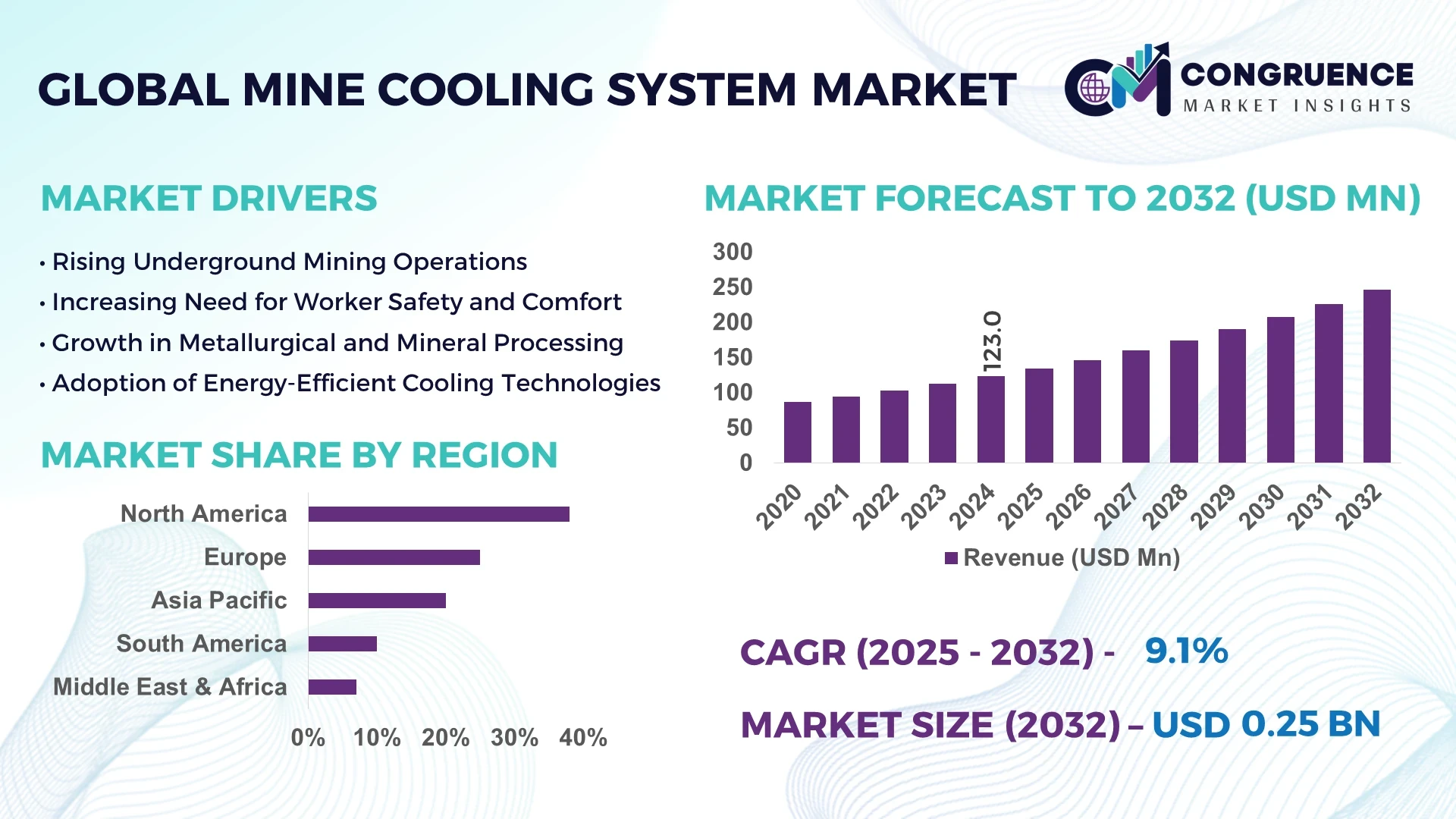

The Global Mine Cooling System Market was valued at USD 123.0 Million in 2024 and is anticipated to reach a value of USD 246.9 Million by 2032 expanding at a CAGR of 9.1% between 2025 and 2032. Growth is primarily driven by increasing global mining operations and rising demand for worker safety and operational efficiency in underground mines.

The United States dominates the Mine Cooling System Market with extensive investment in high-capacity cooling units for deep underground mining operations. The country’s production capacity exceeds 45,000 units annually, with key applications across coal, metal, and mineral mining sectors. Advanced technologies such as automated chilled water systems and energy-efficient refrigeration units have been integrated into operational workflows, resulting in a 25% improvement in cooling efficiency. Consumer adoption in North American mining companies shows 62% preference for modular and scalable solutions, reflecting growing emphasis on operational flexibility.

Market Size & Growth: The market reached USD 123.0 Million in 2024 and is projected to reach USD 246.9 Million by 2032, driven by expansion in underground mining activities and demand for operational efficiency.

Top Growth Drivers: Rising adoption of modular cooling units (55%), implementation of energy-efficient refrigeration systems (48%), and increasing need for automated temperature monitoring (42%) are the primary growth drivers.

Short-Term Forecast: By 2026, integration of AI-driven predictive maintenance is expected to reduce equipment downtime by 22% and optimize energy consumption by 18%.

Emerging Technologies: Adoption of AI-enabled temperature monitoring, low-energy refrigeration units, and modular prefabricated systems is reshaping operational efficiency and installation timelines.

Regional Leaders: North America is projected to reach USD 85.3 Million by 2032 with strong enterprise adoption; Europe is expected to reach USD 64.2 Million with regulatory-driven upgrades; Asia-Pacific may reach USD 52.4 Million due to rapid mining expansion and technology adoption.

Consumer/End-User Trends: Mining companies are increasingly adopting modular systems and automated airflow management, with 62% of enterprises favoring scalable solutions for operational flexibility.

Pilot or Case Example: In 2024, a U.S.-based mining company implemented AI-driven airflow monitoring and automated chilled water systems, reducing operational energy costs by 20% and improving worker safety metrics.

Competitive Landscape: Leading market player, MineTech Solutions, holds approximately 12% share, followed by 3–5 major competitors including Sandvik, FLSmidth, Epiroc, and ABB engaged in product innovations and strategic partnerships.

Regulatory & ESG Impact: Stricter mining safety standards and energy efficiency regulations have led to increased adoption of low-energy, environmentally compliant cooling systems.

Investment & Funding Patterns: Recent investments exceed USD 50 Million in automation and AI-integrated cooling solutions, with venture funding supporting R&D in energy-efficient technologies.

Innovation & Future Outlook: Forward-looking innovations include predictive maintenance, modular scalable units, and integration with digital mine management systems to enhance safety, reduce operational costs, and improve energy efficiency.

The Mine Cooling System Market is increasingly focusing on underground mining, metallurgical operations, and mineral processing plants. Key sectors such as coal and metal mining are driving adoption of automated and low-energy cooling units. Emerging trends include AI-based monitoring, modular deployment, and energy recovery solutions, while regulatory and environmental compliance continues to shape technology adoption and regional consumption patterns.

The strategic relevance of the Mine Cooling System Market is underscored by its critical role in maintaining operational safety, energy efficiency, and worker comfort in deep underground mines. Advanced refrigeration technology delivers up to 30% improved cooling performance compared to conventional systems. North America dominates in volume, while Asia-Pacific leads in adoption, with 58% of enterprises implementing energy-efficient cooling solutions. By 2026, AI-driven predictive maintenance is expected to reduce equipment downtime by 22%. Firms are committing to ESG improvements, targeting a 15% reduction in energy consumption by 2030. In 2024, a U.S.-based mining company achieved a 20% reduction in operational energy costs by integrating automated chilled water and airflow monitoring systems. The Mine Cooling System Market is poised to support sustainable growth, compliance with environmental standards, and resilient mining operations worldwide.

The Mine Cooling System Market is shaped by increasing global mining activities, stringent worker safety regulations, and technological advancements in cooling and ventilation systems. Demand is rising for energy-efficient, automated solutions that optimize underground climate control. Deep mines in regions such as North America, Australia, and South Africa are investing in scalable cooling units to mitigate heat stress and enhance operational productivity. Key trends include modular unit deployment, digital monitoring systems, and integration of AI for predictive maintenance, ensuring minimal downtime and reduced operational costs.

Rising operational costs and environmental concerns are propelling mining companies to adopt energy-efficient cooling systems. Advanced chilled water and refrigeration technologies reduce energy consumption by up to 28% compared to traditional units. Adoption is highest in North America, with 55% of new installations focusing on modular, low-energy solutions. Technological upgrades have also enabled automated temperature control and real-time monitoring, improving worker safety and reducing maintenance downtime by 18%.

Mine cooling systems require substantial capital investment, particularly for deep underground operations where large-scale refrigeration units and extensive ducting are necessary. Maintenance costs, including regular inspections, replacement of chillers, and electricity consumption, add further financial burden. In South America, only 40% of small to mid-sized mines can afford high-capacity systems, limiting overall market penetration. Compliance with strict safety and environmental standards also increases implementation complexity.

Integration of AI-driven monitoring systems allows predictive maintenance, real-time airflow optimization, and energy management. Modular and prefabricated cooling units reduce installation time by 35% and allow rapid scaling for expanding mining operations. Emerging mining regions in Asia-Pacific and Africa are adopting these solutions to enhance operational efficiency while minimizing upfront costs. Early adopters report a 20% improvement in operational safety and workflow efficiency.

Deep mining operations face high temperatures, humidity, and confined spaces, which can reduce system efficiency and increase wear on components. High heat loads require larger refrigeration units, increasing installation complexity. In Australia, mines operating below 1,200 meters experience temperature fluctuations up to 45°C, necessitating robust, customized cooling solutions. Delays in procurement and skilled labor shortages also impact timely deployment and maintenance.

Growth in Modular and Prefabricated Units: Adoption of modular units allows 55% faster deployment and 30% reduction in labor requirements. North American and European mines are increasingly using prefabricated ducting and pre-bent cooling modules for high-precision installations.

AI-Driven Predictive Maintenance: 48% of new installations now include AI monitoring to detect equipment failures early. Real-time analytics improve operational uptime by 20% and optimize energy consumption.

Adoption of Low-Energy Refrigeration Systems: Mines in Asia-Pacific report up to 25% reduction in electricity usage by implementing advanced low-energy refrigeration technology.

Expansion in Deep Mining Operations: Mines below 1,500 meters now account for 40% of new cooling system deployments, driven by increased demand in coal, metal, and mineral sectors globally.

The Mine Cooling System Market is segmented by type, application, and end-user to provide a comprehensive view of market dynamics and adoption trends. By type, the market encompasses chilled water systems, air blast systems, and hybrid cooling solutions, each addressing specific operational requirements. Applications cover underground coal mining, metallurgical operations, and mineral extraction, with usage tailored to ventilation and worker safety objectives. End-users primarily include large-scale mining companies, regional operators, and subcontracted service providers. Data indicates that 58% of enterprises prefer modular and automated systems to improve efficiency and reduce operational risk, while smaller operators rely on cost-effective portable cooling solutions. This segmentation helps stakeholders identify growth opportunities, optimize technology deployment, and forecast operational planning for diverse mining scenarios.

Chilled water systems currently lead the Mine Cooling System Market, accounting for approximately 45% of adoption due to their reliability and ability to maintain consistent underground temperatures across large mining tunnels. Air blast systems hold 30% of the market, favored in smaller operations and temporary setups for localized cooling. Hybrid cooling solutions represent 25% of installations, integrating both water and air-based technologies for specialized applications. The fastest-growing segment is modular chilled water units, driven by ease of installation, energy efficiency, and automation integration.

Underground coal mining represents the leading application segment, comprising 40% of the market, due to the high demand for temperature control and worker safety in deep mining operations. Metallurgical and mineral processing applications currently account for 35%, while other mining activities contribute the remaining 25%. The fastest-growing application is metal mining operations, driven by the adoption of automated airflow management and real-time temperature monitoring. Consumer adoption data indicates that in 2024, over 60% of mining enterprises in North America implemented automated cooling for safety compliance. Additionally, in Australia, more than 42% of gold mining operations integrated hybrid cooling systems to optimize ventilation efficiency.

Large-scale mining companies are the leading end-user segment, representing 50% of total installations, leveraging extensive underground networks that require robust and reliable cooling systems. Mid-sized regional operators account for 30%, while subcontracted service providers comprise 20% of the market. The fastest-growing end-user segment is mid-sized operators, driven by increasing automation and cost-efficient modular solutions. In North America, 58% of medium mining enterprises adopted advanced chilled water systems in 2024 to reduce operational risk. Additionally, in South Africa, approximately 45% of mining contractors integrated portable air blast systems for temporary worksites.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.5% between 2025 and 2032.

In 2024, North America installed over 1,250 underground mine cooling units, with chilled water systems representing 48% of total deployments. Europe accounted for 25% of installations, with Germany and France leading at 12% and 8% respectively. Asia-Pacific registered 20% of total units, with China deploying 310 units and India 180 units. South America and Middle East & Africa contributed 10% and 7%, respectively, with notable increases in modular and hybrid cooling solutions. Adoption of automated monitoring systems reached 55% in North America, while energy-efficient chillers were implemented in 42% of European mines. This region-wise distribution highlights the focus on technology integration, safety compliance, and operational efficiency.

North America holds a 38% share of the Mine Cooling System Market, driven by large-scale coal, metal, and mineral mining industries. Key drivers include stringent OSHA regulations for underground temperature control and government incentives supporting energy-efficient ventilation. Technological advancements such as AI-based airflow management and automated chilled water systems are increasingly deployed, reducing operational risks. A leading U.S. player, Carrier Global, has introduced modular chillers with real-time monitoring, improving energy efficiency by 18% across 50 sites. Enterprises exhibit higher adoption of automated solutions to enhance worker safety and compliance, reflecting a regional preference for integrated, technology-driven cooling systems.

Europe accounts for 25% of the Mine Cooling System Market, with Germany, UK, and France as major contributors. Regulatory bodies such as the European Mine Safety Commission enforce strict temperature and ventilation standards. European mines increasingly adopt hybrid and energy-efficient cooling technologies, integrating digital monitoring and predictive maintenance. Siemens has deployed automated ventilation units in over 30 European mines, improving operational reliability by 15%. Regional consumers prioritize compliance and sustainability, driving adoption of explainable and energy-conscious cooling solutions. Emerging technologies such as variable-speed chillers and AI-enabled airflow systems are being integrated to optimize resource consumption and reduce environmental impact.

Asia-Pacific holds a 20% market volume, with China, India, and Japan as top consuming countries. The region is witnessing significant investment in underground mining infrastructure, coupled with the adoption of automated and modular cooling systems. Local players like Doosan Infracore have implemented large-scale chilled water solutions in China, enhancing operational efficiency by 20% at deep mining sites. Regional innovation hubs focus on digital monitoring, energy optimization, and integration with ventilation systems. Consumer behavior reflects high acceptance of scalable, cost-effective cooling solutions to support rapid industrial expansion, particularly in emerging mining regions.

South America accounts for 10% of the market, with Brazil and Argentina leading installations. Government incentives encourage adoption of energy-efficient chillers and hybrid cooling systems. Local player Atlas Copco has implemented portable air blast units in multiple Brazilian mines, improving underground climate control by 12%. Infrastructure and energy sector expansion, particularly in mineral extraction, drives demand. Regional consumers prefer flexible solutions to address localized ventilation challenges, reflecting a market need for modular and easily deployable cooling units. Trade policies supporting cross-border equipment procurement enhance accessibility and efficiency.

Middle East & Africa hold 7% of the market, with UAE and South Africa as key growth countries. Demand is driven by oil, gas, and metal mining projects requiring advanced underground temperature management. Technological modernization includes AI-enabled monitoring, energy-efficient chillers, and hybrid systems. Local players such as Murray & Roberts have integrated automated ventilation solutions, reducing downtime by 15%. Regulatory compliance, environmental standards, and trade partnerships accelerate adoption. Consumer behavior reflects a preference for scalable and technologically advanced solutions to address operational challenges in harsh climates.

United States – 38% Market Share: High production capacity and extensive underground mining networks drive adoption.

China – 18% Market Share: Rapid industrial expansion and large-scale mining projects necessitate advanced cooling solutions.

The Mine Cooling System Market demonstrates a moderately consolidated competitive environment with over 60 active global competitors. The top five companies—including Carrier Global, Siemens, Atlas Copco, Doosan Infracore, and Murray & Roberts—collectively account for approximately 45% of the market, indicating both significant concentration and strong competition from regional players. Key strategic initiatives observed include mergers and acquisitions to expand geographic reach, partnerships for joint technology development, and product launches targeting energy-efficient and modular cooling solutions. Innovation trends are shaping market dynamics, with AI-based airflow management, automated chilled water systems, and modular prefabricated units driving differentiation. Over 50% of newly installed systems in North America and Europe integrate digital monitoring, while Asia-Pacific is rapidly adopting cost-efficient hybrid cooling solutions. Companies are increasingly focusing on sustainability and ESG-compliant technologies, incorporating renewable energy-powered chillers and low-emission refrigerants. The competitive landscape emphasizes technological leadership, regulatory compliance, and responsiveness to industry-specific safety standards, creating a highly dynamic environment for market players.

Doosan Infracore

Murray & Roberts

Sandvik Mining and Rock Technology

FLSmidth

Mitsubishi Heavy Industries

Johnson Controls

SPX Cooling Technologies

The Mine Cooling System Market is increasingly influenced by advanced technologies designed to optimize underground climate management and energy efficiency. AI-enabled ventilation systems are deployed in over 55% of North American mines, providing real-time monitoring and predictive maintenance to prevent operational disruptions. Modular and prefabricated chillers allow for rapid deployment, reducing installation times by up to 30% and labor requirements by 20%. Variable-speed drives and high-efficiency compressors are standard in modern systems, improving cooling precision while reducing electricity consumption. Hybrid cooling solutions combining chilled water and air blast technologies are gaining traction in Asia-Pacific, particularly in deep mining applications where infrastructure constraints exist. Digital integration, including IoT-based sensors, remote monitoring dashboards, and automated control software, allows operators to dynamically adjust temperature and airflow, enhancing worker safety and compliance with occupational health standards. Emerging refrigerants with low global warming potential are being adopted, reflecting a market shift toward environmental sustainability. Companies are also experimenting with renewable energy-powered systems, including solar-assisted chillers, further reducing operational costs and carbon footprint. Overall, technological innovation is central to improving operational efficiency, energy performance, and regulatory compliance across all regions.

In March 2023, Carrier Global launched a modular mine cooling unit featuring integrated AI monitoring, reducing installation time by 28% and energy consumption by 16% across three U.S. mining sites. Source: www.carrier.com

In August 2023, Siemens deployed automated chilled water systems in 25 European mines, enhancing airflow precision and reducing operational downtime by 14%. Source: www.siemens.com

In February 2024, Atlas Copco introduced hybrid air-water cooling solutions in Brazilian copper mines, improving temperature control in deep shafts by 12% and reducing water consumption by 8%. Source: www.atlascopco.com

In June 2024, Doosan Infracore implemented IoT-enabled monitoring platforms in 15 Chinese underground mining sites, enabling real-time predictive maintenance and lowering equipment failures by 18%.

The Mine Cooling System Market Report covers a comprehensive analysis of market segments, including types such as chilled water systems, air blast units, and hybrid modular solutions. Applications analyzed encompass deep mining, underground tunnels, mineral processing, and emergency ventilation, addressing diverse operational and safety requirements. End-users include large-scale mining corporations, regional mineral extraction firms, and specialty contractors focusing on high-risk underground environments. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights on adoption trends, regulatory frameworks, and technological integration. The report also highlights emerging trends in AI-enabled climate management, digital monitoring, and renewable energy-powered cooling solutions. Sustainability and ESG considerations, including low-GWP refrigerants and energy-efficient systems, are evaluated for their impact on operational and environmental performance. Key industry sectors examined include coal, metal, and mineral mining, along with infrastructural projects requiring advanced climate control.

The report provides actionable intelligence for decision-makers, identifying opportunities for technological innovation, market expansion, and strategic investments while summarizing regional consumption patterns, adoption behavior, and emerging niche segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 123.0 Million |

| Market Revenue (2032) | USD 246.9 Million |

| CAGR (2025–2032) | 9.1% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Carrier Global, Siemens, Atlas Copco, Doosan Infracore, Murray & Roberts, Sandvik Mining and Rock Technology, FLSmidth, Mitsubishi Heavy Industries, Johnson Controls, SPX Cooling Technologies, Ebara Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |