Reports

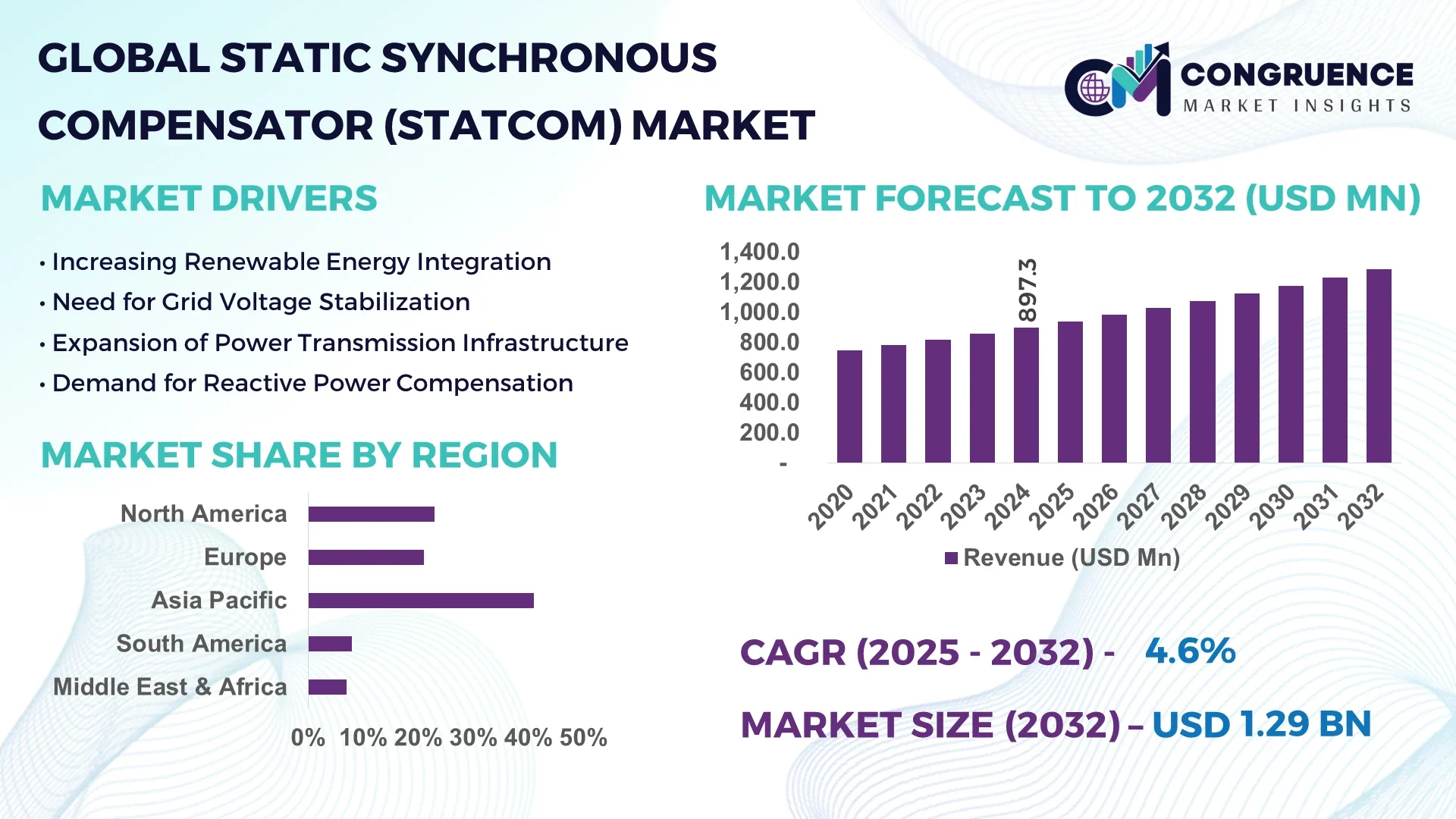

The Global Static Synchronous Compensator (STATCOM) Market was valued at USD 897.25 Million in 2024 and is anticipated to reach a value of USD 1285.79 Million by 2032 expanding at a CAGR of 4.6% between 2025 and 2032.

In the United States, the STATCOM market benefits from advanced grid modernization programs, substantial investments in renewable integration projects, and robust production capabilities for high-voltage power electronics, with several manufacturers focusing on the development of flexible AC transmission systems for wind and solar energy installations.

The Static Synchronous Compensator (STATCOM) Market is witnessing steady growth across utilities, renewable energy, steel manufacturing, and industrial automation sectors as grid stability and power quality demand rise with urban expansion and electrification trends. Technological advancements in STATCOM configurations with modular multilevel converters and advanced control systems are enhancing system response times and operational flexibility across dynamic grid conditions. Regulatory frameworks encouraging grid decarbonization, coupled with the integration of renewable energy sources, have driven utilities to adopt STATCOM systems for voltage stability and reactive power support. Environmental considerations around transmission losses are further promoting STATCOM deployment, with emerging trends in hybrid STATCOM-SVC configurations for improved dynamic reactive power compensation and voltage control. Asia-Pacific, Europe, and the Middle East are observing increased consumption of STATCOM units, driven by the demand for flexible grid stabilization solutions in line with industrial growth and renewable energy goals, supporting the future outlook of the Static Synchronous Compensator (STATCOM) Market.

AI is transforming the Static Synchronous Compensator (STATCOM) Market by enhancing operational efficiency, predictive maintenance, and dynamic grid performance optimization across utility and industrial applications. AI-driven analytics integrated into STATCOM control systems enable real-time monitoring of grid conditions, providing dynamic reactive power compensation while minimizing voltage fluctuations during peak load conditions and renewable integration. In the Static Synchronous Compensator (STATCOM) Market, machine learning algorithms are being utilized to predict equipment wear and component stress, reducing unplanned downtimes while extending asset life for utilities and grid operators. Smart diagnostics, enabled by AI-powered digital twins, are helping operators simulate various grid fault scenarios, allowing for proactive system adjustments to maintain stability and power quality under fluctuating generation and consumption patterns.

AI deployment in the Static Synchronous Compensator (STATCOM) Market is enabling adaptive control strategies, dynamically adjusting STATCOM output in milliseconds based on real-time voltage, frequency, and reactive power data, improving the reliability of grids under transient disturbances. AI models are also helping optimize energy consumption within STATCOM systems by adjusting capacitor and inductor operations precisely to meet system needs, thereby reducing operational energy use and system losses. Enhanced forecasting capabilities in the Static Synchronous Compensator (STATCOM) Market, enabled by AI, support grid operators in planning for reactive power support during renewable variability, maintaining seamless power flow and compliance with grid codes. These advancements are further facilitating the integration of STATCOM systems with energy storage solutions, opening pathways for hybrid flexible AC transmission system operations that align with global smart grid initiatives.

"In 2024, an AI-powered STATCOM project in Germany utilized machine learning algorithms within its control system to reduce voltage deviation events by 38% while optimizing dynamic reactive power delivery, achieving faster response times during grid disturbances, and improving the operational reliability of renewable energy integration projects within regional transmission networks."

The Static Synchronous Compensator (STATCOM) Market is evolving with growing emphasis on grid stability, reactive power compensation, and the seamless integration of renewable energy sources across transmission and distribution networks. Increased urbanization and the expansion of power-intensive industries are creating a surge in demand for advanced flexible AC transmission systems, where STATCOM systems are proving essential in mitigating voltage sags and flickers. Technological innovations, including the deployment of modular multilevel converters and advanced digital control algorithms, are enhancing the operational responsiveness of STATCOM systems under dynamic grid conditions. Governments and utilities are actively adopting grid modernization initiatives aligned with low-carbon goals, propelling the Static Synchronous Compensator (STATCOM) Market forward as it supports energy transition efforts. Additionally, the rising need for uninterrupted power supply and the expansion of microgrids in remote and industrial applications are stimulating consistent investments in the deployment of STATCOM systems across developing and developed economies.

The increasing integration of renewable energy sources is driving the adoption of STATCOM systems due to their ability to provide dynamic reactive power support and voltage stabilization during intermittent generation. As global renewable capacity, including wind and solar, expands, utilities are increasingly deploying STATCOM systems to manage voltage variations caused by fluctuating inputs while ensuring grid reliability and quality. For instance, the deployment of STATCOM systems in large-scale solar photovoltaic plants and offshore wind farms has enabled operators to reduce voltage instability and mitigate flicker issues effectively. These systems support grid code compliance for renewable projects, enabling seamless renewable integration with minimal curtailment. The push for decarbonization, combined with the scaling up of renewable energy targets, is set to strengthen demand for STATCOM systems within transmission and distribution networks worldwide.

The Static Synchronous Compensator (STATCOM) Market faces challenges due to the high initial capital investment required for the procurement and deployment of STATCOM systems. The installation of these advanced systems often involves substantial engineering, procurement, and construction (EPC) costs, including civil works, grid connection infrastructure, and advanced control systems. Additionally, the technical complexity associated with integrating STATCOM systems into existing grid structures can lead to project delays, increasing implementation timelines for utilities and industrial facilities. Utilities in emerging economies may find it challenging to allocate budgets for STATCOM installations while balancing other grid infrastructure priorities. Furthermore, the need for specialized expertise in system configuration and maintenance adds to operational expenditure concerns, acting as a barrier for widespread adoption, particularly among small-scale utilities and independent power producers.

The rapid development of smart grids and digital substations presents significant opportunities for the Static Synchronous Compensator (STATCOM) Market. Governments and utilities are investing in digitalization initiatives to enhance the reliability, monitoring, and operational efficiency of power systems, where STATCOM systems play a critical role in voltage regulation and dynamic reactive power compensation. Smart grid projects across Asia-Pacific, North America, and Europe are integrating STATCOM systems to manage grid fluctuations associated with distributed generation and the growing adoption of electric vehicles. These projects provide a pathway for STATCOM systems to function as key components in advanced grid control, supporting seamless demand response and frequency regulation. The evolution of grid codes requiring higher reactive power support capabilities and dynamic voltage control further amplifies opportunities for STATCOM systems, positioning them as integral to the global smart grid ecosystem.

The Static Synchronous Compensator (STATCOM) Market faces challenges in navigating diverse and evolving regulatory frameworks and grid code compliance requirements across regions. Utilities and operators must ensure that STATCOM installations adhere to specific grid codes related to reactive power support, voltage control ranges, and system stability parameters, which can vary significantly between countries and even between grid operators within the same region. The compliance process may require extensive system testing, certification, and documentation, extending project timelines and adding administrative burdens to developers and utilities. Additionally, modifications to existing grid codes in response to rising renewable penetration and grid modernization initiatives can create uncertainty, requiring periodic updates to installed STATCOM systems to maintain compliance. These complexities can hinder seamless project execution and impact the pace of STATCOM market expansion in certain regions.

• Deployment of Hybrid STATCOM-SVC Solutions: Utilities are increasingly integrating hybrid STATCOM and Static Var Compensator (SVC) systems within transmission and distribution networks to enhance reactive power compensation flexibility. These hybrid systems are being deployed across grid modernization projects to handle rapid voltage fluctuations while providing cost-effective solutions for large-scale renewable integration. Countries such as India and China have initiated pilot projects incorporating hybrid systems to stabilize grids with high renewable penetration while ensuring consistent power quality.

• Integration with Battery Energy Storage Systems (BESS): The Static Synchronous Compensator (STATCOM) market is observing a measurable trend toward coupling STATCOM units with BESS for advanced voltage regulation and frequency stabilization. Grid operators are leveraging this integration to address intermittency challenges associated with wind and solar generation while improving system inertia and grid resilience. Pilot projects in Germany and South Korea have demonstrated successful implementation of STATCOM-BESS configurations in urban transmission networks.

• Adoption of AI-Driven Predictive Maintenance: The application of AI in STATCOM systems for predictive maintenance is gaining traction, reducing downtime while improving operational performance. Using data analytics and machine learning models, operators can now predict insulation degradation, capacitor health, and semiconductor performance with higher accuracy. Utilities in Europe have reported measurable reductions in maintenance intervention times and extended component life, enhancing the reliability of deployed STATCOM assets.

• Expansion in Offshore Wind Grid Connections: STATCOM systems are being widely installed in offshore wind transmission systems to manage voltage stability and reactive power support during variable wind generation. The UK and Nordic countries have reported a significant rise in the deployment of STATCOM technology within their offshore wind farms, ensuring compliance with stringent grid codes while optimizing power transfer capability through subsea cables under fluctuating load and generation conditions.

The Static Synchronous Compensator (STATCOM) market is segmented based on type, application, and end-user categories, each shaping the evolving market landscape with unique dynamics. Types within this market include thyristor-based and voltage-source converter-based STATCOMs, each catering to specific voltage and reactive power management needs across transmission and distribution networks. Key applications span renewable energy integration, industrial voltage control, and grid stabilization for utilities, aligning with increasing demand for reliable and efficient grid operations. End-user segments include utilities, renewable energy producers, and heavy industrial consumers such as steel manufacturing units, each investing in STATCOM systems to ensure power quality and system reliability under dynamic load conditions. This segmentation provides critical insights for stakeholders aiming to align product strategies and investment decisions within the global Static Synchronous Compensator (STATCOM) market.

Thyristor-Based STATCOM systems lead the market due to their robust capability in handling high-voltage, large-scale grid stabilization requirements for transmission networks. These systems are extensively used in power utilities requiring rapid dynamic reactive power support to mitigate voltage dips and flickers under heavy load conditions. Voltage-Source Converter (VSC)-Based STATCOM systems are the fastest-growing segment, driven by their compact size, modular architecture, and precise voltage control capabilities, making them ideal for renewable energy integration and distribution grid applications. They enable seamless interfacing with wind and solar power plants where voltage and frequency fluctuations are common. Other types, such as modular multilevel converters (MMC)-based STATCOM systems, are gaining niche relevance in advanced grid applications requiring ultra-fast dynamic compensation and low harmonic distortion, ensuring operational efficiency within sensitive industrial and urban transmission networks.

Renewable energy integration remains the leading application in the Static Synchronous Compensator (STATCOM) market, supported by the increasing deployment of wind and solar energy systems globally. STATCOM systems provide essential reactive power support, ensuring voltage stability within grids experiencing fluctuating renewable generation, which is critical for regions with ambitious renewable targets. The fastest-growing application is industrial voltage control, where manufacturing facilities, data centers, and mining operations utilize STATCOM systems to maintain power quality during peak operations, minimizing equipment downtime and operational disruptions. Grid stabilization for utility transmission networks continues to be a significant application area, particularly for aging grids undergoing modernization, while emerging applications include microgrid installations where precise voltage and reactive power control is vital for maintaining stability under dynamic load and generation conditions.

Utilities are the leading end-user segment in the Static Synchronous Compensator (STATCOM) market, using these systems to enhance grid stability, manage voltage fluctuations, and provide dynamic reactive power support across transmission and distribution networks. This is driven by increasing renewable integration and the need to meet regulatory requirements for voltage and frequency stability. Renewable energy producers represent the fastest-growing end-user group, with wind and solar operators adopting STATCOM systems to manage voltage variability, ensuring grid code compliance and seamless energy dispatch into utility grids. Other end-users, including heavy industries such as steel manufacturing and mining operations, are also contributing to market growth as they seek to mitigate voltage dips and power quality issues during high-load operations, ensuring efficient and reliable power supply for critical production processes.

Asia-Pacific accounted for the largest market share at 41% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

The Static Synchronous Compensator (STATCOM) market in Asia-Pacific is driven by robust investments in grid modernization, high renewable energy integration across China and India, and rising demand for voltage stabilization within expanding industrial sectors. Countries in this region are adopting advanced STATCOM systems for large-scale solar and wind power integration while improving reactive power management to address peak demand fluctuations. Technological advancements in modular STATCOM configurations are enabling utilities and industrial facilities to enhance operational reliability, reduce transmission losses, and comply with evolving energy efficiency standards. This regional momentum is further supported by government initiatives prioritizing infrastructure upgrades and the reduction of grid instability issues, propelling the Static Synchronous Compensator (STATCOM) market outlook.

Grid Digitalization Driving Advanced Voltage Control Investments

The region holds a 23% share in the Static Synchronous Compensator (STATCOM) market, driven by the increasing deployment of flexible AC transmission systems within utility and renewable energy sectors. High demand from wind and solar energy integration projects, coupled with industrial grid stability requirements in manufacturing and data center operations, is propelling adoption across the region. Regulatory incentives encouraging grid modernization, such as transmission infrastructure upgrade programs in the United States and Canada, are further supporting deployment. Technological advancements in digital monitoring, AI-enabled predictive maintenance, and modular STATCOM configurations are transforming operational efficiencies within utility networks, aligning with smart grid initiatives and resilience goals in this high-demand market.

Renewable Integration Boosting Advanced Grid Stabilization Solutions

The region captured a 19% volume share in the Static Synchronous Compensator (STATCOM) market, driven by widespread renewable energy projects across Germany, the UK, and France. Utilities and transmission operators are prioritizing STATCOM adoption to manage voltage fluctuations and reactive power requirements under dynamic renewable generation conditions. Regulatory frameworks and sustainability initiatives such as the EU Green Deal are incentivizing investment in advanced grid stability solutions, aligning with decarbonization targets. The adoption of emerging technologies, including hybrid STATCOM-SVC systems and AI-driven control modules, is enhancing voltage control precision while supporting seamless renewable integration across complex grid infrastructures in this advanced market environment.

Infrastructure Expansion Fueling Advanced Reactive Power Solutions

The region holds the leading position in volume consumption within the Static Synchronous Compensator (STATCOM) market, supported by large-scale infrastructure development and renewable energy projects across China, India, and Japan. High industrial electricity demand and grid expansion projects in emerging economies are driving installations for voltage stability and reactive power management. Manufacturing sector growth and the push for electrification are creating new opportunities for STATCOM integration in both transmission and distribution networks. Innovation hubs across the region are investing in modular, compact STATCOM technologies to optimize power quality and grid flexibility, supporting ongoing digitalization efforts within the region’s energy and industrial sectors.

Grid Stability Initiatives Enhancing Reactive Power Deployment

Brazil and Argentina are key contributors to the Static Synchronous Compensator (STATCOM) market in the region, which currently holds a 7% share, driven by the need for advanced grid stability and voltage control. Infrastructure expansion projects within the energy sector, including renewable energy integration, are driving STATCOM demand to address intermittent generation issues while enhancing system reliability. Government incentives and trade policies supporting grid modernization are facilitating the deployment of advanced reactive power solutions within transmission and distribution networks. Growing investment in construction and industrial sectors is further boosting the application of STATCOM systems to ensure consistent voltage quality during peak load conditions in regional markets.

Energy Sector Modernization Accelerating Voltage Control Adoption

The region is witnessing increasing demand within the Static Synchronous Compensator (STATCOM) market driven by energy sector projects in UAE, Saudi Arabia, and South Africa, which together contribute to a regional market share of 10%. Oil and gas industries, along with large-scale construction and urbanization projects, are fueling demand for voltage stability solutions to maintain operational efficiency and reduce grid instability. Technological modernization trends, including the deployment of digital substations and advanced reactive power management systems, are aligning with the region’s infrastructure goals. Local regulations and trade partnerships encouraging renewable energy adoption and grid reliability are further propelling STATCOM deployments in the region’s energy and industrial sectors.

China – 31% market share

Strong manufacturing capacity and rapid renewable energy deployment drive China’s dominance in the Static Synchronous Compensator (STATCOM) market.

United States – 21% market share

High end-user demand from utilities and data centers, coupled with advanced grid modernization programs, positions the United States as a top player in the Static Synchronous Compensator (STATCOM) market.

The Static Synchronous Compensator (STATCOM) market is characterized by the presence of over 35 active competitors globally, ranging from established power systems manufacturers to specialized flexible AC transmission system solution providers. Market participants are actively engaging in strategic partnerships, technology collaborations, and regional expansion initiatives to strengthen their positioning within key renewable integration and grid stability projects across North America, Asia-Pacific, and Europe. Product launches featuring advanced modular multilevel converter-based STATCOM solutions and AI-integrated control systems are notable trends driving competition as companies seek to enhance operational responsiveness and reduce system losses under dynamic grid conditions. Mergers and targeted acquisitions are occurring as part of portfolio diversification strategies, with players expanding their reactive power management capabilities and service offerings across industrial, utility, and renewable sectors. Innovation trends, including the integration of STATCOM with battery energy storage systems and the deployment of hybrid STATCOM-SVC solutions, are reshaping competitive dynamics as companies align their products with evolving grid modernization initiatives and energy transition goals globally.

Siemens Energy

Hitachi Energy

Mitsubishi Electric Corporation

GE Grid Solutions

NR Electric Co., Ltd.

Rongxin Power Electronic Co., Ltd.

Hyosung Heavy Industries

Toshiba Energy Systems & Solutions Corporation

S&C Electric Company

American Superconductor Corporation (AMSC)

Technological advancements in the Static Synchronous Compensator (STATCOM) market are reshaping the operational landscape of voltage stabilization and reactive power management across power transmission and distribution networks. The adoption of modular multilevel converter (MMC) technology within STATCOM systems is improving dynamic response times while reducing harmonic distortion, enabling precise voltage regulation under varying load conditions. MMC-based STATCOM units also facilitate scalability for higher voltage applications, supporting large-scale grid integration projects, especially for offshore wind and utility-scale solar installations.

The integration of AI-driven predictive analytics and digital twin technology in STATCOM systems allows operators to monitor real-time equipment conditions and predict component health for maintenance optimization, reducing system downtimes and enhancing asset lifecycle. Hybrid STATCOM-SVC systems are gaining traction for their ability to combine dynamic and steady-state reactive power compensation within a single platform, enabling efficient utilization of grid infrastructure under high renewable penetration scenarios.

Emerging trends include the integration of STATCOM systems with battery energy storage solutions to address grid inertia and frequency stability challenges. Compact, prefabricated STATCOM designs are facilitating faster deployment in urban substations and remote areas, supporting flexible grid modernization initiatives. Advances in power semiconductor devices, such as the use of silicon carbide (SiC) components, are further enhancing system efficiency by reducing switching losses, improving thermal performance, and enabling high-voltage operations within compact footprints.

• In March 2024, Siemens Energy commissioned a modular STATCOM system for a 400 kV transmission substation in India, enhancing voltage stability and enabling seamless integration of 300 MW of newly added solar capacity into the regional grid while ensuring compliance with reactive power compensation standards.

• In February 2024, Hitachi Energy launched an upgraded STATCOM platform with integrated digital twin capabilities, enabling real-time system simulation and predictive diagnostics, reducing reactive power adjustment delays by 25% during transient events in utility-scale transmission applications.

• In August 2023, Mitsubishi Electric completed the delivery of STATCOM units for an offshore wind project in the UK, designed to manage voltage control over subsea cables and improve dynamic reactive power support for a 500 MW wind farm connection, ensuring stable grid operations under fluctuating wind conditions.

• In May 2023, GE Grid Solutions introduced a hybrid STATCOM-SVC system in Germany, enabling utilities to manage dynamic and steady-state reactive power compensation within a single installation, reducing space requirements by 30% while supporting grid stability during peak renewable energy generation periods.

The Static Synchronous Compensator (STATCOM) Market Report comprehensively covers the evolving landscape of advanced grid stabilization and reactive power management solutions across global power systems. It includes detailed segmentation by type, covering thyristor-based, voltage-source converter-based, and modular multilevel converter-based STATCOM systems used across high-voltage transmission and distribution networks. The report analyzes key application areas including renewable energy integration, industrial voltage control, and utility grid stabilization, reflecting the rising need for voltage regulation under dynamic load and generation conditions.

Geographically, the report covers major markets including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with country-level insights into deployment trends, regulatory environments, and grid modernization initiatives driving STATCOM adoption. The scope extends to technological advancements, including AI-enabled predictive maintenance, digital twin integration, hybrid STATCOM-SVC systems, and the use of silicon carbide-based power semiconductor devices that are improving efficiency and reducing operational losses.

The report also explores niche and emerging segments such as the integration of STATCOM systems with battery energy storage for enhanced grid flexibility, as well as prefabricated compact STATCOM solutions supporting urban substation deployments. Industry focus areas include utilities, renewable energy producers, and heavy industrial consumers requiring consistent voltage stability. By addressing these facets, the report serves as a strategic resource for stakeholders and decision-makers aiming to align investment and operational strategies with the global STATCOM market’s evolving opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 897.25 Million |

|

Market Revenue in 2032 |

USD 1285.79 Million |

|

CAGR (2025 - 2032) |

4.6% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, Hitachi Energy, Mitsubishi Electric Corporation, GE Grid Solutions, NR Electric Co., Ltd., Rongxin Power Electronic Co., Ltd., Hyosung Heavy Industries, Toshiba Energy Systems & Solutions Corporation, S&C Electric Company, American Superconductor Corporation (AMSC) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |