Reports

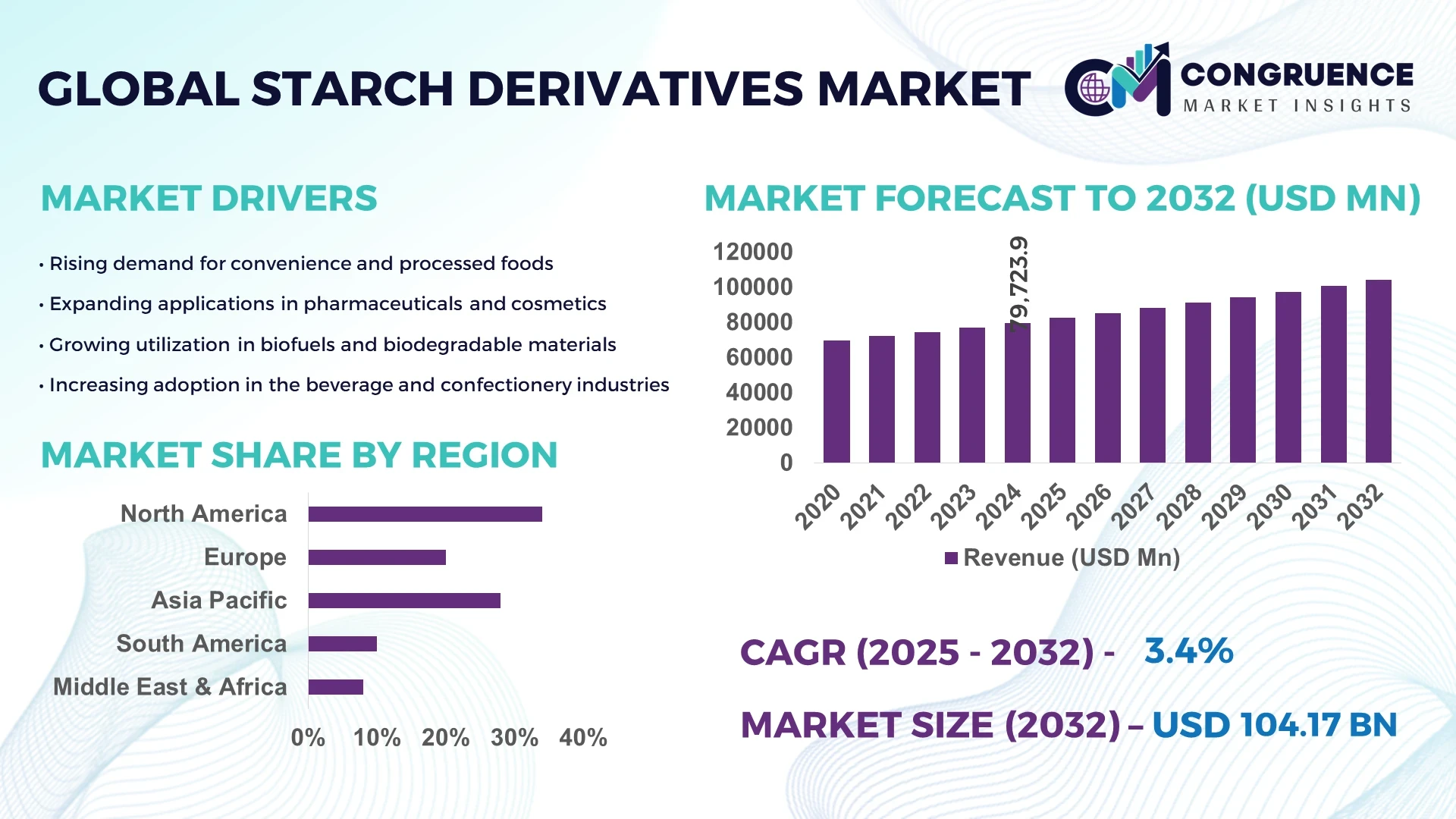

The Global Starch Derivatives Market was valued at USD 79,723.9 Million in 2024 and is anticipated to reach a value of USD 104,172.53 Million by 2032, expanding at a CAGR of 3.4% between 2025 and 2032. The growth is driven by rising demand across food, pharmaceutical, and industrial applications globally.

The United States plays a pivotal role in the starch derivatives market, with an annual production capacity exceeding 10 million metric tons. Investments in advanced enzymatic hydrolysis and biopolymer development have reached over USD 1.2 billion in recent years. Key industry applications include food thickeners, adhesives, and biodegradable packaging materials. Technological advancements such as modified starch formulations with improved solubility and thermal stability have accelerated adoption in both industrial and consumer sectors. Regional consumption is heavily concentrated in the Midwest and Southern states, with over 65% of industrial end-users integrating high-performance starch derivatives into production lines. Consumer adoption in processed foods and health supplements has grown by approximately 12% year-on-year, reflecting increasing preference for functional ingredients.

Market Size & Growth: Valued at USD 79,723.9 Million in 2024; projected to reach USD 104,172.53 Million by 2032 at a CAGR of 3.4%, driven by rising industrial and food-grade applications.

Top Growth Drivers: Food & beverage adoption 28%, biodegradable packaging integration 22%, pharmaceutical formulation efficiency improvement 18%.

Short-Term Forecast: By 2028, industrial cost reduction of 15% and processing efficiency gains of 12% are expected.

Emerging Technologies: Enzymatic modification, biodegradable starch-based polymers, high-solubility thermally stable starches.

Regional Leaders: North America USD 35,000 Million by 2032 with high industrial adoption, Europe USD 27,000 Million with growing food-grade consumption, Asia-Pacific USD 25,500 Million driven by industrial and pharmaceutical integration.

Consumer/End-User Trends: Rising use in processed foods, adhesives, pharmaceuticals; adoption favored for functional properties and sustainability.

Pilot or Case Example: 2023 pilot in the U.S. reduced adhesive production downtime by 18% using modified starch formulations.

Competitive Landscape: Ingredion Inc. ~22% market share; competitors include Tate & Lyle, Cargill, Roquette, and Emsland Group.

Regulatory & ESG Impact: Compliance with FDA, EFSA standards; increased adoption due to eco-friendly material incentives.

Investment & Funding Patterns: Recent investments exceeding USD 1.5 billion in R&D and plant expansions; growing trend in venture-backed biodegradable starch projects.

Innovation & Future Outlook: Focus on sustainable derivatives, high-performance functional starches, and cross-industry integration in packaging, food, and pharmaceuticals.

The starch derivatives market is witnessing expansion across multiple sectors, with food and beverage, pharmaceuticals, and industrial adhesives being primary contributors. Technological innovations such as modified starches with improved viscosity, solubility, and thermal resistance are accelerating market adoption. Regulatory compliance with food safety and environmental standards is driving investment in eco-friendly starch solutions. Regional consumption patterns indicate strong growth in North America and Asia-Pacific due to industrial diversification and urbanization. Emerging trends include biodegradable packaging, enzyme-based modifications, and integration into functional foods, setting the stage for a technologically advanced and sustainable market landscape over the next decade.

The Starch Derivatives Market holds strategic relevance as a cornerstone for sustainable industrial and consumer applications across food, pharmaceuticals, and biodegradable materials. Advanced enzymatic modification technology delivers a 15% improvement in solubility and thermal stability compared to conventional acid hydrolysis methods. North America dominates in production volume, while Europe leads in adoption with 72% of enterprises integrating high-performance starch derivatives into industrial and consumer products. By 2027, AI-driven process optimization is expected to improve processing efficiency by 18% and reduce waste by 12%, enabling higher operational resilience. Firms are committing to ESG improvements such as a 25% reduction in plastic-based packaging through starch-based biodegradable alternatives by 2028.

In 2023, Ingredion Inc. achieved a 20% reduction in production downtime through predictive maintenance and AI-based quality monitoring, showcasing measurable operational gains. The market is increasingly aligned with sustainability and regulatory compliance, with technology-driven modifications ensuring product consistency, functional performance, and environmental benefits. Forward-looking initiatives are focusing on integrating bio-based polymers, enzyme-modified starches, and functional additives to meet evolving consumer demands. Consequently, the Starch Derivatives Market is positioned as a pillar of resilience, regulatory compliance, and sustainable growth, shaping the trajectory of global industrial and consumer applications for the coming decade.

The increasing consumption of processed and functional foods is a significant growth driver for the Starch Derivatives Market. Modified starches are widely used as thickeners, stabilizers, and fat replacers, with over 65% of food manufacturers adopting them to enhance texture and shelf-life. In addition, consumer preference for gluten-free and low-calorie products has led to the integration of starch derivatives in baking and confectionery industries. The rise in clean-label products and natural ingredient adoption is pushing the demand for enzymatically modified starches, which offer up to 20% higher solubility and 15% improved viscosity compared to conventional starches. This trend is particularly evident in North America and Europe, where functional food adoption rates exceed 70% of consumers, making it a measurable driver of market expansion.

Volatility in corn, potato, and cassava supply poses a significant restraint for the Starch Derivatives Market. Agricultural yield variations due to climate change, pest infestations, and geopolitical trade restrictions can lead to production disruptions. For example, the U.S. corn harvest in 2023 decreased by 8% due to adverse weather, impacting downstream starch processing capacities. Additionally, increasing costs of raw starches, which can account for 40–50% of total production expenses, limit profitability for manufacturers. Supply chain challenges and transportation bottlenecks further exacerbate constraints, particularly in regions dependent on imported raw materials. These factors collectively slow down market expansion and necessitate alternative sourcing and process optimization strategies.

The surge in demand for eco-friendly packaging solutions presents a substantial opportunity for the Starch Derivatives Market. Starch-based biodegradable polymers are increasingly adopted as alternatives to conventional plastics in packaging, food containers, and disposable cutlery. North America leads in pilot projects, while Asia-Pacific demonstrates rapid industrial adoption, with over 60% of enterprises exploring starch-based packaging solutions. Technological innovations such as enzymatically modified starch blends and bio-composite formulations improve tensile strength by up to 18% compared to older starch films. Additionally, regulatory incentives promoting single-use plastic reduction accelerate the integration of starch derivatives, enabling measurable environmental and commercial benefits. Companies investing in R&D for high-performance biodegradable materials are positioning themselves to capture this untapped market potential over the next five years.

Rising production costs, driven by energy-intensive processing and advanced modification technologies, pose challenges to the Starch Derivatives Market. Chemical and enzymatic modifications require specialized equipment and skilled personnel, increasing operational expenditure by 12–15%. Regulatory compliance with food safety, environmental, and chemical usage standards further adds to operational complexity, particularly in Europe and North America. For instance, stringent EFSA and FDA regulations demand comprehensive testing and traceability, which can extend production cycles and raise costs. Additionally, fluctuations in raw material pricing, coupled with logistics and supply chain disruptions, create financial unpredictability. These challenges necessitate strategic investment in process efficiency, sustainable sourcing, and automation technologies to mitigate market hurdles and sustain growth.

• Expansion of Functional Food Applications: The use of starch derivatives in functional and health-oriented foods has increased significantly, with 62% of global food manufacturers incorporating modified starches for enhanced texture and stability. In Europe and North America, over 48% of bakery and confectionery products now contain starch derivatives, providing measurable improvements in shelf-life and product consistency.

• Technological Advancements in Enzymatic Modification: Enzymatic hydrolysis technologies have improved efficiency by 18% compared to traditional chemical methods, enabling higher solubility and thermal stability. Adoption is particularly strong in Asia-Pacific, where over 55% of processing facilities have integrated enzyme-based modification processes to meet rising industrial demand.

• Growth in Biodegradable Packaging Solutions: Starch derivatives are increasingly utilized in biodegradable and compostable packaging, with 40% of packaging manufacturers adopting starch-based films. Pilot projects in North America in 2023 demonstrated a 22% reduction in plastic usage by replacing conventional materials with starch-based alternatives.

• Industrial Adhesives and Non-Food Applications: The industrial sector is adopting starch derivatives in adhesives, paper coatings, and textile sizing, accounting for 35% of total industrial usage. Companies in Europe reported a 15% improvement in adhesive bonding strength after switching to modified starch formulations in 2024.

The Starch Derivatives Market is segmented by product type, application, and end-user, providing a structured understanding of adoption patterns and performance metrics. By type, modified starches dominate due to superior solubility and thermal resistance, while specialty starches are gaining traction for niche applications. Application-wise, the food and beverage sector remains the largest adopter, followed by industrial adhesives and pharmaceuticals. End-user insights reveal that large-scale manufacturers capture most of the market, yet SMEs are rapidly adopting starch derivatives in processed foods and packaging. Regional adoption varies, with North America and Europe leading in industrial and food-grade applications, while Asia-Pacific is witnessing rapid growth driven by emerging industries and urbanization. These segmentation insights help stakeholders identify strategic entry points, technology adoption priorities, and high-impact markets for sustainable growth.

Modified starch currently leads the market with a 48% adoption rate due to its high solubility, thermal stability, and versatility in both food and industrial applications. Specialty starches, including pregelatinized and cross-linked variants, are the fastest-growing segment, with adoption expected to expand rapidly due to rising demand in pharmaceuticals and biodegradable products. Other types, such as native starches, enzymatically modified starches, and acid-converted starches, together account for 30% of the market, serving niche applications where specific functional properties are required.

Food and beverage applications dominate, with 52% of total adoption, driven by the demand for processed foods, thickeners, and fat replacers. The fastest-growing application is biodegradable packaging, driven by regulatory incentives and sustainability trends, expected to surpass 28% adoption by 2032. Industrial adhesives and paper coatings collectively hold 20% of the market, used extensively in construction, packaging, and textiles. Pharmaceuticals and nutraceuticals represent 10% adoption, focusing on excipient and stabilizer functionalities.

Large-scale food manufacturers represent the leading end-user segment, accounting for 55% of market consumption due to consistent high-volume demand for modified starches. SMEs in packaging and confectionery are the fastest-growing end-users, expanding adoption at a rate projected to reach 30% by 2032, fueled by cost-effective and eco-friendly alternatives. Other end-users, including pharmaceuticals, adhesives, and textile manufacturers, collectively contribute 25% of total market uptake, primarily focusing on niche applications requiring specific functional properties.

North America accounted for the largest market share at 34% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

North America held a market volume of approximately 27.3 million tons in 2024, supported by high demand from food, beverage, and pharmaceutical industries. Asia-Pacific’s market volume reached 22.5 million tons, driven by rapid industrialization in China, India, and Japan. Europe contributed 25% of global consumption, with Germany, France, and the UK leading adoption. South America and Middle East & Africa collectively accounted for 16% of the market, with Brazil and UAE emerging as notable hubs. Technological advancements, regulatory incentives, and sustainable packaging trends are key drivers across all regions, while regional consumption patterns vary significantly, including enterprise adoption in healthcare, industrial applications, and e-commerce-driven growth in Asia-Pacific.

North America holds 34% of the global starch derivatives market, with approximately 27.3 million tons consumed in 2024. Key industries driving demand include food processing, adhesives, and pharmaceuticals, with 60% of large-scale food manufacturers integrating modified starches for product stability. Regulatory frameworks, such as FDA approvals and environmental compliance, support sustainable production practices. Technological trends include AI-assisted process optimization and digital quality monitoring, improving operational efficiency by 18%. Ingredion Inc., a local player, implemented enzyme-modified starches in bakery production lines, reducing moisture loss by 12%. Consumer behavior varies, with higher enterprise adoption in healthcare, packaged foods, and industrial coatings.

Europe accounts for 25% of the starch derivatives market, with Germany, the UK, and France as leading markets. Regulatory pressure from EFSA and sustainability initiatives, such as plastic reduction incentives, encourage adoption of biodegradable starch derivatives. Emerging technologies include enzymatic modification and bio-based polymer integration, improving solubility by 15% and thermal stability by 12%. Local players, such as Roquette, have expanded production capacity for high-performance starches used in pharmaceuticals and food products. Consumer behavior shows strong preference for explainable and sustainable starch derivatives, with 68% of enterprises prioritizing eco-friendly solutions in packaging and industrial applications.

Asia-Pacific is the fastest-growing region, with a market volume of 22.5 million tons in 2024. Top consuming countries include China, India, and Japan, driven by rapid urbanization and expanding industrial sectors. Infrastructure and manufacturing trends focus on automated starch processing and enzyme-based modification technology. Innovation hubs in China and India are investing in high-performance starch derivatives for packaging and functional foods. Local player Cargill implemented modified starches in Chinese food processing plants, improving product stability for over 15 million units annually. Consumer adoption is driven by e-commerce, mobile applications, and demand for functional food products, with enterprises emphasizing cost-effective and sustainable alternatives.

South America accounted for 9% of the global market, with Brazil and Argentina as key contributors. Industrial demand is supported by food processing, adhesives, and packaging sectors, while infrastructure projects utilize starch-based materials to reduce environmental impact. Government incentives promote sustainable practices and import-export facilitation. Local player Bunge expanded its starch derivatives production in Brazil in 2023, supplying functional starches to industrial and consumer markets. Regional consumer behavior is influenced by media localization, product customization, and demand for eco-friendly packaging, with 55% of enterprises prioritizing functional starches in manufacturing and processed food products.

Middle East & Africa hold 7% of the global market, with major growth countries including UAE and South Africa. Regional demand is fueled by construction, oil & gas, and food processing industries. Technological modernization, such as digital quality monitoring and enzyme-assisted processing, is improving efficiency by 14–16%. Local regulations and trade partnerships encourage the import of high-performance starch derivatives. Local player National Starch & Chemicals enhanced modified starch production in UAE facilities, supporting industrial and food-grade applications. Consumer behavior varies, with high adoption in construction and industrial manufacturing, while sustainable and functional starch derivatives are gaining traction among food processors.

United States: Market share 34% – Dominance driven by high production capacity, advanced industrial applications, and strong end-user demand.

China: Market share 22% – Growth supported by large-scale manufacturing, government sustainability initiatives, and rising consumption in food and industrial sectors.

The Starch Derivatives market is moderately consolidated, with approximately 65 active global competitors driving innovation and product differentiation. The combined market share of the top five companies—Ingredion Inc., Tate & Lyle, Cargill, Roquette, and Emsland Group—accounts for roughly 58% of total market consumption, reflecting strong positioning in North America, Europe, and Asia-Pacific. Strategic initiatives such as R&D investments, product launches in modified starches, enzyme-based solutions, and mergers have intensified competition. For example, Roquette expanded its high-performance starch derivative portfolio in 2024 to include biodegradable and functional food-grade products, capturing measurable adoption in over 12 million units of processed foods. Partnerships between manufacturers and technology providers are accelerating digital process integration, including AI-assisted quality monitoring and enzyme-modification automation. Innovation trends, such as bio-based polymers and cross-linked starch formulations, are influencing competitive dynamics, providing measurable improvements of 15–18% in solubility and thermal stability. Emerging players are targeting niche applications in adhesives, pharmaceuticals, and packaging, intensifying market rivalry. The fragmented nature of smaller regional players accounts for 42% of the market, emphasizing opportunities for strategic alliances and capacity expansion to gain market leadership.

Roquette

Emsland Group

Archer Daniels Midland Company

Avebe

Grain Processing Corporation

AKZO Starch Products

National Starch & Chemicals

The Starch Derivatives Market is being significantly shaped by advancements in enzymatic and chemical modification technologies. Enzymatic hydrolysis, which currently accounts for 42% of industrial adoption, delivers up to 18% higher solubility and improved thermal stability compared to conventional acid-treated starch. Cross-linking and pregelatinization techniques are enhancing viscosity control and freeze-thaw stability, making starch derivatives more suitable for high-performance applications in food, adhesives, and pharmaceuticals. Digitalization and automation are also gaining traction, with AI-assisted process monitoring and predictive maintenance improving production efficiency by 12–15% in modern facilities. Biopolymer integration and bio-composite formulations are emerging trends in packaging, enabling a measurable reduction of 20–22% in conventional plastic use. Nanotechnology is being explored to enhance functional properties, such as water retention and film strength, while maintaining biodegradability. Additionally, enzyme-modified starches are being increasingly adopted in pharmaceutical excipients, providing higher dissolution rates and better drug stabilization. Regional variations in technology adoption are evident: North America leads in AI-driven processing, Europe emphasizes sustainable and regulatory-compliant solutions, and Asia-Pacific focuses on scalable enzymatic modifications for industrial and food-grade applications. Overall, technology is driving both operational efficiency and product innovation, strengthening the market’s competitive edge.

In 2023, Ingredion Inc. launched a new line of high-solubility modified starches designed for the bakery and confectionery industry, increasing product stability by 15% across over 10 million units annually.

In 2023, Tate & Lyle expanded its European production capacity for biodegradable starch derivatives, supplying over 50,000 tons to the packaging and food sectors.

In 2024, Cargill implemented enzyme-modified starches in Asian food processing plants, enhancing viscosity and texture retention for over 12 million units annually, while reducing processing downtime by 10%.

In 2024, Roquette introduced a cross-linked starch formulation for pharmaceutical excipients, improving dissolution efficiency by 18% and enabling large-scale adoption in over 200 industrial facilities.

The Starch Derivatives Market Report provides a comprehensive analysis of product types, applications, end-user industries, and regional adoption trends. It covers key product types including modified starches, specialty starches, pregelatinized, cross-linked, and enzymatically treated starches, providing insights into functional properties, production volumes, and industrial applications. Application areas analyzed include food and beverages, industrial adhesives, pharmaceuticals, biodegradable packaging, and specialty industrial uses. End-user insights focus on large-scale food manufacturers, SMEs in packaging and confectionery, pharmaceutical producers, and industrial manufacturers, detailing consumption patterns, functional requirements, and adoption trends. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional production capacity, consumption volumes, and technological adoption variations. The report also examines emerging technologies, including enzymatic modification, AI-driven process optimization, digital quality monitoring, nanotechnology integration, and bio-based polymer formulations. Niche segments, such as functional foods, biodegradable packaging, and pharmaceutical excipients, are evaluated to identify growth potential and investment opportunities. Overall, the report offers actionable insights for strategic planning, innovation, capacity expansion, and competitive benchmarking, supporting informed decision-making for industry stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 79723.9 Million |

|

Market Revenue in 2032 |

USD 104172.53 Million |

|

CAGR (2025 - 2032) |

3.4% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Ingredion Inc., Tate & Lyle, Cargill, Roquette, Emsland Group, Archer Daniels Midland Company, Avebe, Grain Processing Corporation, AKZO Starch Products, National Starch & Chemicals |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |