Reports

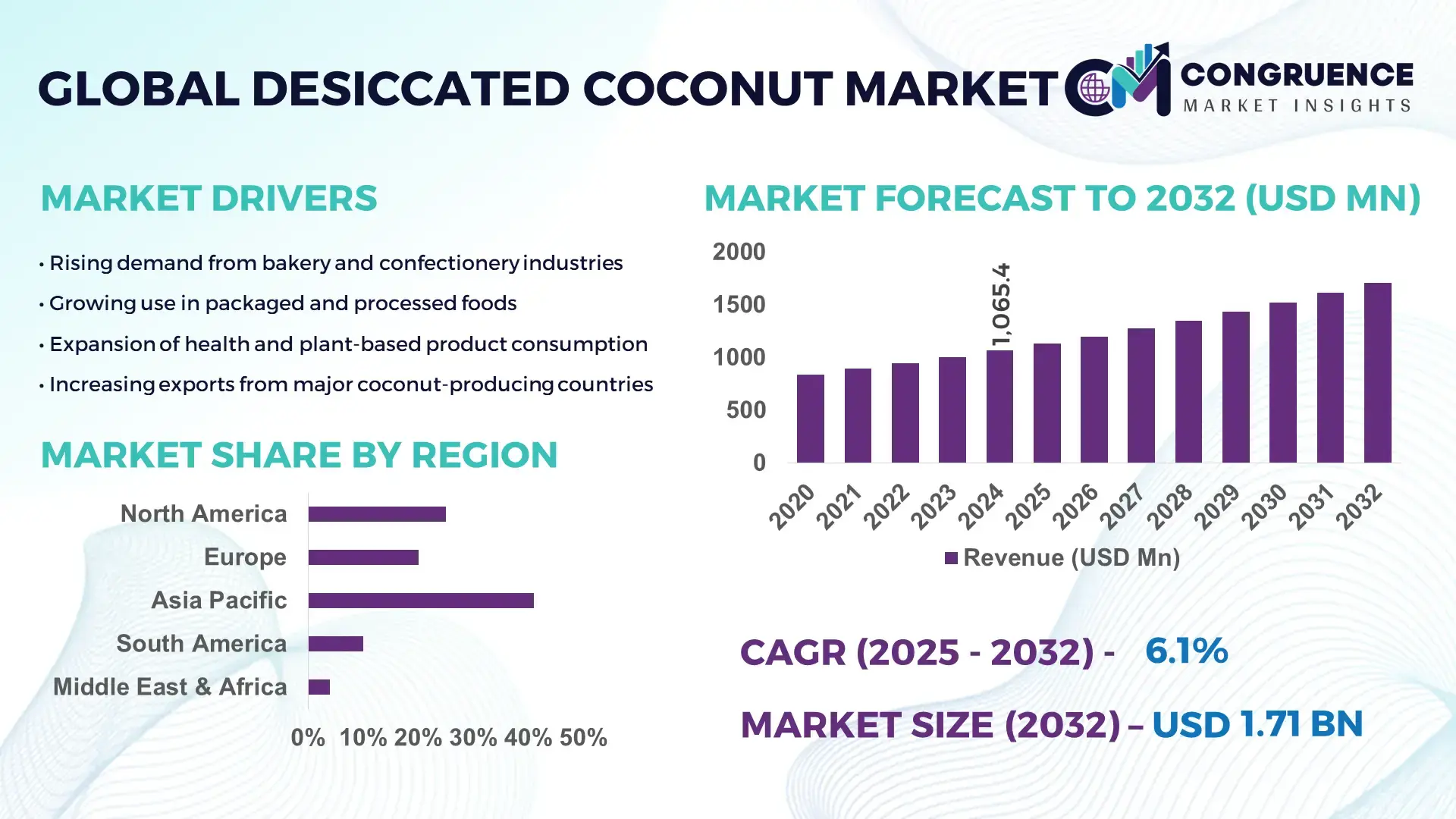

The Global Desiccated Coconut Market was valued at USD 1,065.38 Million in 2024 and is anticipated to reach a value of USD 1,710.91 Million by 2032 expanding at a CAGR of 6.1% between 2025 and 2032. Growth is driven by rising demand from bakery, confectionery, and dairy processors seeking natural, plant-based ingredients.

The Philippines remains the dominant country in desiccated coconut production, supported by an annual processing capacity exceeding 1.4 million metric tons of coconuts and more than 60 operational drying facilities equipped with automated hygienic processing technologies. The country has invested over USD 150 million in modernization upgrades since 2022, enabling higher throughput and improved microbial safety standards. Its output is widely used in packaged foods, cosmetic formulations, and nutraceuticals, backed by strong export-grade quality certification systems and expanding adoption of high-fat and fine-grade variants for industrial applications.

• Market Size & Growth: Valued at USD 1.06 Billion in 2024 with a projection of USD 1.71 Billion by 2032, expanding at 6.1% CAGR, driven by rising utilization in bakery, confectionery, and plant-based food manufacturing.

• Top Growth Drivers: 32% increase in bakery-sector adoption; 27% efficiency improvement in automated drying systems; 18% rise in processed coconut ingredient consumption.

• Short-Term Forecast: By 2028, production efficiency across leading processors is expected to improve by 22% through energy-efficient drying technologies.

• Emerging Technologies: Deployment of infrared drying systems, advanced microbial control sensors, and traceability platforms improving product safety and uniformity.

• Regional Leaders: Asia-Pacific projected at USD 980 Million by 2032 with high industrial-grade adoption; Europe projected at USD 420 Million supported by clean-label trends; North America projected at USD 210 Million with strong demand from vegan food processors.

• Consumer/End-User Trends: High uptake among bakery manufacturers, snack-food producers, and nutrition brands, with increasing preference for fine-grade and low-moisture formats.

• Pilot or Case Example: A 2024 pilot in Southeast Asia achieved a 28% reduction in processing downtime using automated moisture-control systems.

• Competitive Landscape: Market leader holds ~22% share, followed by major competitors including Celebes Coconut Corporation, Primex Group, Peter Paul Philippines Corporation, and Renuka Foods.

• Regulatory & ESG Impact: Strengthening food safety compliance, export quality mandates, and sustainability certifications are accelerating adoption of traceable, low-residue products.

• Investment & Funding Patterns: Over USD 210 Million invested since 2023 in processing upgrades, energy-efficient drying, and export-expansion projects.

• Innovation & Future Outlook: Advancements in precision drying, clean-label product formulations, and enhanced global supply-chain integration are shaping future market expansion.

The desiccated coconut industry is increasingly supported by strong demand from bakery, confectionery, dairy alternatives, and plant-based food sectors, each contributing steadily to overall market expansion. Recent innovations include high-fat variants, ultra-fine grades, and enhanced microbial control processing lines, improving both quality and shelf life. Environmental policies promoting sustainable coconut farming and residue-free processing are influencing supply chain practices, while regions such as Asia-Pacific, Europe, and the Middle East show accelerating consumption of clean-label coconut ingredients. Improving cultivation productivity, expanding export capabilities, and rising adoption within vegan and functional food categories continue to drive long-term growth and diversification across global markets.

The strategic relevance of the Desiccated Coconut Market is anchored in its expanding role across bakery, confectionery, dairy alternatives, functional foods, and clean-label product manufacturing, supported by measurable improvements in processing efficiency and global supply-chain optimization. New infrared-based drying technology delivers 28% improvement compared to traditional hot-air drying standards, strengthening consistency and reducing moisture variability. Asia-Pacific dominates in volume, while Europe leads in adoption with 36% of enterprises using certified low-moisture, fine-grade variants in commercial production lines. By 2027, AI-enabled process automation is expected to improve energy utilization efficiency by 22%, reducing operational waste and enhancing product uniformity. Firms are committing to ESG metric improvements such as a 30% reduction in processing-related carbon output by 2030. In 2024, the Philippines achieved a 19% reduction in microbial contamination levels through its national AI-driven sorting and quality-check initiative. Going forward, the Desiccated Coconut Market is positioned as a pillar of resilience, compliance, and sustainable growth, supported by digitized production ecosystems, rising demand from plant-based industries, and strengthened regional supply networks.

Rising demand from bakery and confectionery manufacturers is significantly strengthening the Desiccated Coconut Market, facilitated by increasing consumption of premium baked products, ready-to-eat snacks, and clean-label ingredients. Manufacturers are incorporating desiccated coconut for its texture, flavor, and stability benefits, with large processors reporting up to a 25% rise in orders for high-fat and ultra-fine grades since 2022. Enhanced food processor adoption is driven by growth in filled chocolates, granola bars, and coconut-based pastries, where desiccated coconut improves product structure, moisture retention, and sensory appeal. Expanding investments into automated grading and hygienic drying lines further support consistent supply, enabling producers to meet rising global demand within stringent food safety and quality frameworks.

Supply-chain volatility remains a key restraint for the Desiccated Coconut Market due to fluctuations in raw coconut availability, logistics delays, and periodic disruptions in major producing regions. Variations in coconut harvest cycles, combined with climate-related impacts, lead to inconsistent supply of raw nuts. Processors report procurement fluctuations of up to 18% during adverse weather periods, affecting factory throughput and delivery schedules. Additionally, rising costs linked to transportation, packaging materials, and compliance with strict export-grade safety standards increase operational burdens for manufacturers. These constraints challenge consistent production planning and create uncertainties for downstream industries reliant on stable ingredient availability, particularly in bakery and functional food segments.

The growing global preference for plant-based, natural, and clean-label food products presents significant opportunities for the Desiccated Coconut Market. Consumers are increasingly adopting coconut-based ingredients in dairy alternatives, nutrition bars, and premium snacks, creating high-value demand for fine, medium, and high-fat grades. Manufacturers report a 30% rise in utilization of desiccated coconut in plant-based formulations since 2021, encouraged by its nutritional profile and functional benefits. Technological advancements, such as low-temperature drying and automated microbial monitoring systems, support the development of higher-quality variants with improved shelf life and safety. Expanding distribution networks and the emergence of new vegan food categories further position desiccated coconut as a versatile, high-growth ingredient across global markets.

Increasing operational costs and stringent technical compliance requirements create substantial challenges for the Desiccated Coconut Market. Producers face rising expenses associated with energy consumption in drying facilities, mandatory quality certification, and investments in automated safety-monitoring systems. Processing plants in major producing nations report energy cost increases of nearly 14% over the last two years, impacting overall production economics. Compliance with global food safety standards—such as microbial thresholds, residue limits, and traceability obligations—demands continuous upgrades to equipment and workforce training. These factors contribute to operational pressure, requiring manufacturers to balance cost controls with technological modernization to maintain competitiveness and secure access to key export markets.

• Rising Integration of Automated Drying and Microbial-Control Systems: Automation-driven upgrades are accelerating across major processing facilities, with more than 42% of new desiccated coconut plants adopting AI-enabled moisture-control and microbial-reduction technologies since 2023. These systems achieve up to 26% improvement in drying consistency and reduce contamination risks by 18%, enabling processors to meet stringent export-grade standards. Adoption is particularly strong in Southeast Asia, where processors are enhancing throughput to handle rising product diversification, including ultra-fine and high-fat grades.

• Expansion of High-Fat and Specialty Grade Consumption in Food Manufacturing: Demand for high-fat desiccated coconut variants is increasing rapidly, with food manufacturers reporting a 31% rise in usage in bakery, confectionery, and dairy-alternative formulations over the past two years. Ultra-fine grades have also grown by 22% in adoption due to their improved blending performance and cleaner texture profiles. The rise of premium snack categories—particularly coconut-based bars and filled confectionery—continues to reshape procurement strategies across Europe and Asia-Pacific.

• Strengthening of Traceability and Digital Quality Assurance Mechanisms: Digital traceability platforms are gaining prominence, with nearly 38% of global exporters integrating QR-based tracking and batch-level quality audits into their supply chains. These systems deliver a measurable 24% reduction in inspection times while enhancing transparency for international buyers. Large exporters in the Philippines and Sri Lanka are increasingly deploying inline optical sensors and automated grading units, improving consistency metrics by up to 20% in mass-production environments.

• Growing Utilization in Plant-Based and Functional Nutrition Segments: The shift toward plant-based and functional nutrition continues to elevate demand for desiccated coconut, with nutrition brands reporting a 28% rise in incorporation across bars, powders, and dairy-free desserts. Consumer surveys indicate that 33% of buyers prefer coconut-derived inclusions due to natural fiber content and clean-label appeal. Asia-Pacific remains the fastest-expanding consumption hub, recording a 19% increase in industrial demand driven by new product launches in vegan and lactose-free categories.

Segmentation in the Desiccated Coconut Market is shaped by evolving product specifications, expanding food-processing applications, and diversified end-user needs across global regions. Types such as fine-grade, medium-grade, and high-fat variants cater to different performance requirements in bakery, confectionery, and health-nutrition sectors. Applications are becoming increasingly specialized, with bakery and confectionery leading usage due to rising demand for texture-enhancing and clean-label ingredients. End-user insights show strong adoption among large food manufacturers, premium snack brands, and dairy-alternative producers, each integrating desiccated coconut for formulation stability and sensory uniformity. Market patterns reflect growing preference for high-fat and ultra-fine formats, digitally monitored processing, and modular supply systems that allow scalable output across Asia-Pacific, Europe, and the Middle East.

Fine-grade desiccated coconut currently leads the market, accounting for approximately 46% of total adoption, supported by strong utilization in confectionery, baked goods, and ready-to-eat snacks where smooth blending and uniform particle distribution are essential. Medium-grade products hold around 28% adoption, driven by demand from cereal, trail-mix, and dessert manufacturers requiring structural consistency. High-fat desiccated coconut represents the fastest-growing type, expanding at a 7.2% CAGR, bolstered by rising use in dairy-alternative formulations, sports-nutrition products, and premium desserts due to its enhanced texture, richer mouthfeel, and improved binding properties. Other specialty types—such as toasted, organic-certified, and ultra-fine variants—collectively contribute 26% and serve niche markets targeting clean-label consumers, artisanal bakeries, and export-grade manufacturers.

Bakery applications dominate the Desiccated Coconut Market with a 49% share, driven by consistent demand for natural fiber, flavor enhancement, and moisture-retention properties in cakes, pastries, and biscuits. Confectionery applications follow at 27%, supported by growing demand for coated snacks, filled chocolates, and texture-enhancing inclusions. Dairy-alternatives represent the fastest-growing application segment, expanding at a 7.8% CAGR, propelled by rising adoption of coconut-based yogurts, frozen desserts, and plant-based creamers. Other applications—including cereals, nutraceutical blends, and ready-to-eat meal kits—collectively contribute 24%, providing additional growth avenues as consumer interest in natural and minimally processed ingredients accelerates.

Large-scale food and beverage manufacturers are the leading end-users, accounting for 52% of total market adoption, supported by continuous integration of desiccated coconut into high-volume bakery, confectionery, and dairy-alternative production. Premium snack and health-nutrition brands hold 26%, driven by rising demand for coconut-based bars, cereal clusters, and functional dessert formats. Small and medium food processors represent the fastest-growing end-user segment, expanding at a 6.9% CAGR, fueled by easier access to high-quality raw materials, automated processing equipment, and contract manufacturing partnerships enabling product diversification. Other end-users—such as foodservice chains, specialty dessert houses, and artisanal bakeries—collectively represent 22%, benefitting from the growing preference for natural ingredients and clean-label menu offerings.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, the Middle East & Africa region is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2025 and 2032.

Several regions show varying levels of demand intensity driven by industrial processing capacity, import reliance, and food manufacturing expansion. Europe contributed 27% of global consumption, supported by increasing demand for clean-label bakery inputs. North America followed with 18%, driven by premium snack production and plant-based food categories. South America represented 9% due to strengthening processed food exports, while the Middle East & Africa reached 5%, supported by rising demand across foodservice and confectionery sectors. Differences in digital traceability adoption also emerged, with Europe achieving 36% deployment rates versus Asia-Pacific at 29% and North America at 33%, shaping procurement competitiveness across regions.

How is rising demand for premium natural ingredients shaping growth in this market?

North America held approximately 18% of the global Desiccated Coconut Market in 2024, supported by strong demand across bakery, confectionery, dairy-alternative, and nutrition-focused industries. The region benefits from a well-established packaged food ecosystem, where large-scale manufacturers increasingly integrate natural, high-fiber coconut ingredients into product lines. Regulatory reforms enhancing food safety and ingredient transparency continue to influence procurement decisions, increasing the adoption of digitally monitored supply chains. Advancements in automated quality-check systems across U.S.-based importers have improved batch consistency by 14%. One regional player expanded its coconut-based snack line in 2024, using high-fat desiccated coconut to improve texture performance. Consumer behavior shows higher application of natural ingredients within the healthcare, wellness, and finance-driven foodservice sectors, with 32% of enterprises opting for cleaner-label ingredient profiles in new product development initiatives.

Why are sustainability standards accelerating adoption patterns in this market?

Europe accounted for nearly 27% of the global market in 2024, driven by strong demand in Germany, the UK, France, and the Netherlands. Regional sustainability mandates, circular-economy guidelines, and stricter compliance protocols for imported agricultural ingredients are significantly shaping product selection. Adoption of precision grading systems and digital traceability tools has grown by 34%, supporting buyer confidence in high-volume imports. Local food manufacturers increasingly utilize organic and ultra-fine desiccated coconut for artisanal bakery and premium confectionery lines. One European snack manufacturer implemented a new automated blending system in 2024, improving ingredient consistency by 16%. Consumer behavior across this region shows higher preference for explainable, clean-label coconut ingredients, with 39% of buyers prioritizing sustainability-certified inputs.

How is manufacturing expansion strengthening demand and processing efficiency in this market?

Asia-Pacific led the global market with a 41% share in 2024, powered by high consumption in India, China, Indonesia, the Philippines, and Japan. Regional production strength, advanced processing infrastructure, and continuous modernization of coconut drying facilities contribute to robust supply and demand integration. Upgraded automation systems across processing hubs have improved output efficiency by 22%. One major regional processor expanded its high-capacity drying unit in 2023, increasing production volume by 18%. Technology-driven grading and digital moisture control systems are rapidly being adopted, particularly within export-focused facilities. Consumer behavior shows accelerated growth driven by mobile commerce platforms and rising consumption of coconut-based snacks, desserts, and dairy alternatives, especially among urban populations.

How is rising processed-food manufacturing boosting demand in this market?

South America represented around 9% of the global market in 2024, with Brazil and Argentina leading consumption. Growth is supported by expanding processed-food, confectionery, and export-oriented snack industries. Regional trade incentives and import-friendly regulations have accelerated ingredient diversification. Infrastructure modernization within food-manufacturing corridors enabled a 15% improvement in supply-chain throughput. One regional confectionery producer adopted high-fat desiccated coconut in 2024 to enhance product moisture retention, improving batch stability by 12%. Consumer behavior in this region reflects rising demand for localized flavors and language-specific product adaptations, with media-driven food trends playing a key role in product innovation.

How are evolving foodservice trends and trade partnerships shaping this market?

The Middle East & Africa region accounted for nearly 5% of global demand in 2024, supported by expanding foodservice, construction-led hospitality growth, and rising confectionery consumption. Key contributors include the UAE, Saudi Arabia, South Africa, and Kenya. Adoption of automated inspection systems and digital traceability platforms improved import handling efficiency by 17%. One regional distributor invested in large-scale cold-storage upgrades in 2023, enhancing ingredient shelf-life stability by 11%. Growing trade collaborations with Asia-Pacific suppliers continue to strengthen availability. Consumer behavior shows increasing preference for premium coconut-based bakery items, with 29% of surveyed buyers choosing natural, high-fiber ingredients in new product purchases.

• Philippines – 24% market share; dominance supported by extensive production capacity and consistent export-grade quality.

• Indonesia – 21% market share; driven by strong industrial processing infrastructure and high-volume supply to global food manufacturers.

The Desiccated Coconut market shows a moderately fragmented structure, with more than 120 active competitors worldwide, including processors, integrated coconut product manufacturers, and specialized exporters. The top 5 companies collectively account for approximately 32% of the global market share, indicating a competitive environment where mid-sized regional players retain significant influence. Around 40% of the competitors operate across multiple coconut derivative categories, strengthening their market position through vertical integration. Strategic initiatives have increased notably, with over 25 mergers and partnership agreements recorded between 2021 and 2024 aimed at expanding supply capacity and securing raw material access. Product differentiation strategies are rising, with nearly 45% of producers enhancing offerings through organic-certified, low-moisture (below 2%) and fine-grade variants to meet evolving food, bakery, and confectionery requirements. Digitization trends are also shaping competition, with more than 30 companies adopting automated drying systems and optical sorting technologies to improve consistency and reduce rejection rates by up to 18%. Export-driven competition is intensifying in Southeast Asia, where high-volume processors have scaled capacities by 12–15% annually due to growing demand in Europe and North America. The competitive landscape continues to evolve as companies invest in sustainability certifications, traceability platforms, and long-term supply agreements with coconut-growing regions to enhance global visibility and secure demand pipelines.

Peter Paul Philippines Corporation

Celebes Coconut Corporation

PT Global Coconut

Primex Group of Companies

Adamjee Lukmanjee & Sons Pvt Ltd

Renuka Agri Foods PLC

Kohinoor Foods

Superstar Coconut Products

Pacific Coco Products

S&P Industries

Royce Food Corporation

Technological advancements in the Desiccated Coconut market are reshaping production efficiency, product quality, and global competitiveness. Automated drying technologies have seen accelerated adoption, with nearly 48% of large and mid-sized processors now using continuous belt or fluidized-bed dryers to maintain moisture levels below 3%, ensuring consistency in fine-, medium-, and extra-fine-grade outputs. Mechanical automation has reduced manual labor requirements by approximately 22% across high-volume facilities, while enhancing production throughput by 15–18% in export-oriented markets.

Optical sorting and digital grading systems are becoming more widespread, with around 35% of exporters employing multi-stage color sorting and defect detection cameras to reduce impurities to less than 0.5%. These technologies are particularly impactful in facilities handling more than 20,000 metric tons annually, where precision sorting reduces rejection rates by up to 12%. Additionally, food-safety technologies such as inline metal detection, UV sterilization tunnels, and high-capacity pasteurization units are increasingly integrated into production lines to meet stringent international compliance thresholds.

Traceability and supply-chain digitization platforms are also influencing market performance. Approximately 40% of global producers have implemented QR-based tracking or blockchain-supported traceability modules to monitor procurement, processing, and export compliance, improving transparency and reducing audit times by nearly 30%. Smart factory solutions featuring IoT-based sensors are expanding, with adoption rising by 17% between 2022 and 2024, enabling real-time control of temperature, contamination risks, and moisture variation. Emerging technologies such as AI-enabled quality analysis and predictive maintenance tools are expected to significantly enhance operational reliability, especially for processors operating in regions with fluctuating raw material supply. These innovations collectively strengthen product safety, operational precision, and export competitiveness across the Desiccated Coconut value chain.

In 2023, export data from major producing countries showed a combined shipment of 282,559 MT of desiccated coconut between January and November, with the United Coconut Association of the Philippines, Inc. reporting that the Philippines led exports at 50.7%, followed by Indonesia at 36.2% and Sri Lanka at 13.1%. (ucap.org.ph)

In the first quarter of 2024, the Philippines shipped 41,854 MT of desiccated coconut — a 20.8% rise compared to the same quarter in 2023 — signaling renewed export momentum and increased global demand rebound. (coconutcommunity.org)

During 2024 many major producers experienced significant price increases: export prices per metric ton rose to US$ 1,911 in the Philippines and US$ 1,999 in Indonesia, reflecting tightening supply conditions and stronger international demand for desiccated coconut.

In 2024 a leading processor commissioned a new continuous drying line to produce low-moisture desiccated coconut optimized for long-shelf-life industrial mixes and export markets, supporting consistency and extended storage suitability.

The Desiccated Coconut Market Report covers global market dynamics across all major geographic regions — Asia-Pacific, North America, Europe, South America, Middle East & Africa — providing detailed segmentation by product type (e.g., fine-grade, medium-grade, high-fat, specialty grades including ultra-fine and value-added blends), application (bakery, confectionery, dairy alternatives, snacks, nutraceuticals, foodservice, retail consumer products), and end-user categories (industrial food & beverage manufacturers, retail snack brands, foodservice operators, co-packers, private-label producers). The report also examines technology adoption in processing lines, including drying, sorting, grading, and traceability/quality control systems, and evaluates the share of processors using automated or semi-automated lines. It analyses distribution channels and logistics infrastructure, covering bulk exports, retail-packed SKUs, and growing e-commerce distribution networks for packaged desiccated coconut products across diverse markets. In addition, the report addresses regulatory, ESG and sustainability compliance trends, organic-certified product ranges, and traceable supply-chain developments. The scope includes recent and niche segments — such as organic certified desiccated coconut, high-fat variants for plant-based and dairy-alternative applications, ultra-fine powders for beverage and confectionery ingredients, and ready-to-use sweetened coconut blends. It further provides a forward-looking outlook on market capacity expansions, export recovery patterns, evolving consumer behavior (e.g., demand for clean-label and plant-based ingredients), and supply-chain resilience strategies for both bulk industrial supply and retail-oriented formats.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1065.38 Million |

|

Market Revenue in 2032 |

USD 1710.91 Million |

|

CAGR (2025 - 2032) |

6.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

|

|

Customization & Pricing |

Available on Request (10% Customization is Free) |