Reports

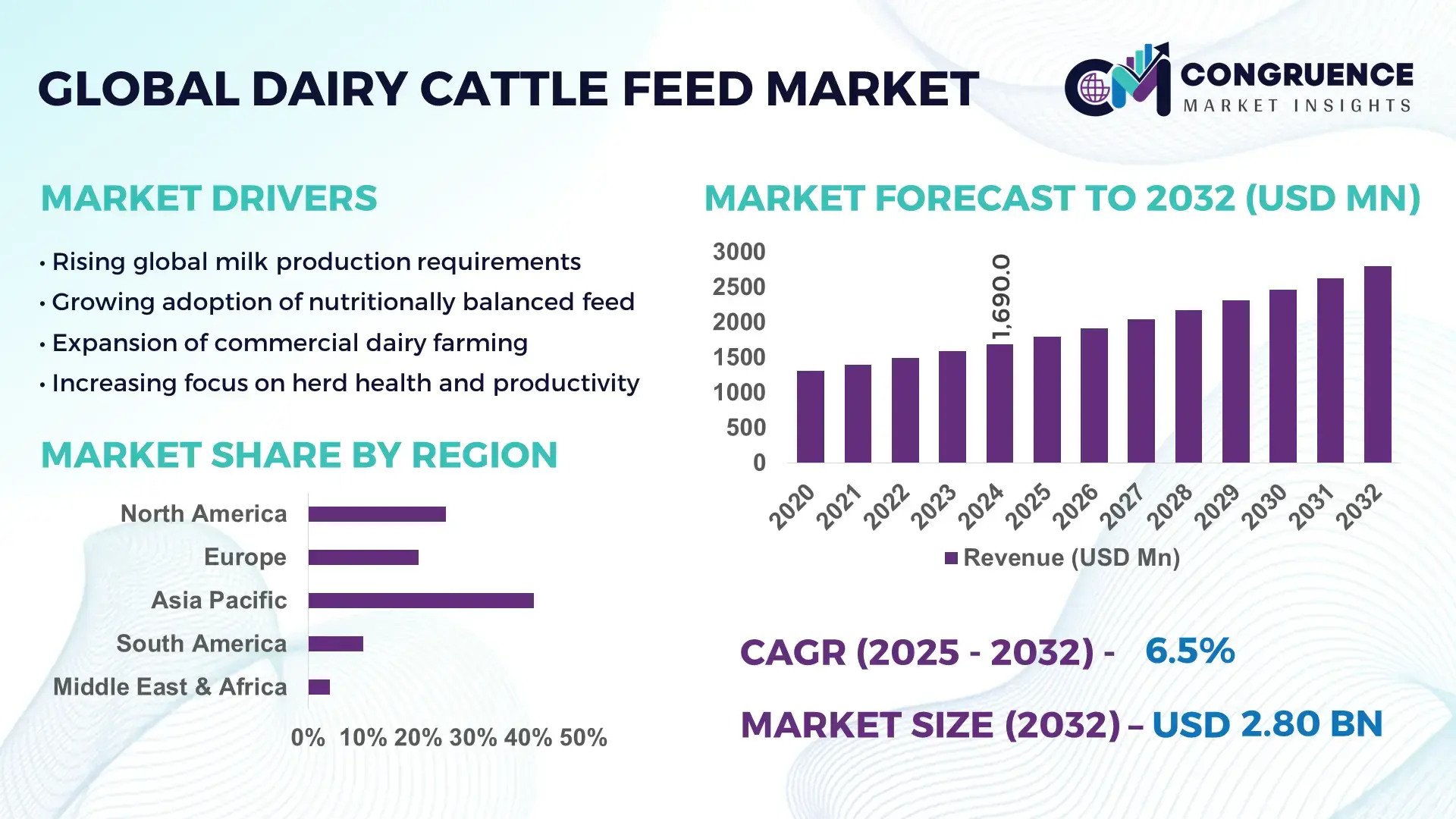

The Global Dairy Cattle Feed Market was valued at USD 1689.99 Million in 2024 and is anticipated to reach a value of USD 2796.93 Million by 2032 expanding at a CAGR of 6.5%% between 2025 and 2032. This growth is supported by rising global demand for high-quality milk and enhanced herd nutrition practices.

In the leading country — India — dairy cattle feed demand has strengthened significantly, supported by milk output rising from 146.3 million tonnes in 2014-15 to 239.3 million tonnes in 2023-24. India’s dairy sector has expanded its investment in modern feed mills, additive-enriched rations and structured nutrition programmes. The Asia-Pacific region, with India as a major contributor, consumed an estimated 185 million metric tons of dairy cattle feed in 2023, reflecting widespread adoption of concentrate feeds, balanced rations and productivity-enhancing nutritional solutions across both smallholder and commercial dairy farms.

Market Size & Growth: Current market value ~ USD 1689.99 M (2024), projected to reach ~ USD 2796.93 M by 2032, CAGR 6.5% — driven by rising dairy consumption and improved feed efficiency solutions.

Top Growth Drivers: Balanced feed adoption (≈ 45%), herd intensification (≈ 38%), yield-improving nutrition practices (≈ 27%).

Short-Term Forecast: By 2028, feed cost per litre of milk production expected to reduce by ~ 8%, with average milk yield per cow increasing by ~ 10%.

Emerging Technologies: Precision nutrition systems, data-based ration optimisation, methane-reducing feed additives.

Regional Leaders (by 2032): Asia-Pacific ~ USD 1.25 B with strong technology adoption; North America ~ USD 680 M with efficiency-driven feeding systems; Europe ~ USD 520 M with growing demand for low-emission feeds.

Consumer/End-User Trends: Rapid shift toward mixed rations and formulated concentrates among dairy farmers seeking higher yield and herd health stability.

Pilot or Case Example: In 2024, a major dairy cooperative trialled additive-rich concentrate feed across 10,000 cows, achieving a 12% rise in average milk yield and 7% reduction in the feed-to-milk cost ratio.

Competitive Landscape: Market leader — Cargill (approx. 22–25% share), followed by Purina Animal Nutrition LLC, Godrej Agrovet, Kent Nutrition Group and Hi-Pro Feeds LP.

Regulatory & ESG Impact: Strengthening sustainability policies are increasing adoption of low-emission diets, with incentives encouraging environmentally responsible livestock nutrition.

Investment & Funding Patterns: Recent global investments in feed manufacturing, R&D and infrastructure exceeded USD 6.2 B, with more than 120 new feed plants established.

Innovation & Future Outlook: Precision feeding, nutrient-dense additive systems and methane-mitigating formulations are reshaping product innovation, with expanding feed facilities and deeper agritech-dairy collaboration driving long-term market growth.

Unique developments in the dairy cattle feed market show increasing contributions from advanced feed formulations, functional additives and digitalised nutrition management across major dairy-producing sectors. Regulatory shifts toward sustainable livestock systems have accelerated the use of low-emission feed blends, while regional consumption patterns point to strong uptake in Asia-Pacific and steady premium-feed adoption in North America and Europe. Technological progress, including ration-modelling tools, enzyme-fortified feeds and customised nutrition programs, is expected to significantly enhance productivity, support herd health, and drive the next phase of market expansion.

The strategic relevance of the Dairy Cattle Feed Market lies in its role as a critical enabler of global dairy productivity, nutritional efficiency and sustainable livestock operations. Modern formulations, including precision-balanced concentrates and additive-enhanced blends, are reshaping feeding systems, improving overall feed conversion efficiency and strengthening farm-level profitability. Advanced feed optimisation software delivers up to 18% improvement compared to traditional manual ration planning, creating measurable gains in nutrient utilisation and milk output. Regional performance continues to diverge, with Asia-Pacific dominating in volume, while Europe leads in adoption with nearly 62% of enterprises implementing advanced nutritional technologies. By 2027, AI-integrated feed modelling systems are expected to improve feed-cost efficiency by approximately 12% across medium and large dairy farms. ESG compliance is becoming a central driver, with firms committing to operational sustainability metrics such as 20% waste reduction and ingredient-sourcing traceability improvement by 2028. In 2024, a leading dairy cooperative in Southeast Asia achieved a 14% reduction in feed wastage through automated IoT-linked feed dispensers, demonstrating the real impact of digital nutrition management systems. Collectively, these developments position the Dairy Cattle Feed Market as a pillar of operational resilience, regulatory alignment and sustainable industry growth over the coming decade.

The shift toward high-efficiency nutrition solutions is significantly influencing the Dairy Cattle Feed Market, as dairy farms increasingly adopt formulations that optimise nutrient absorption and support higher milk yields. Modern fortified concentrates, vitamins, enzymes and amino-acid supplements enhance rumen function and improve milk productivity by measurable margins, with some formulations yielding up to 10–15% improvement in milk output compared to basic feed regimes. Rising adoption of Total Mixed Ration (TMR) systems further accelerates market expansion, as farms using structured TMR diets report up to 20% enhancement in feed utilisation efficiency. Additionally, nutrition-focused herd management practices are becoming standard across commercial dairy operations, supported by increased availability of high-quality raw materials and feed-integrated health additives.

Fluctuations in raw material availability pose a significant restraint to the Dairy Cattle Feed Market, primarily due to heavy dependence on commodities such as maize, soymeal and oilseed cakes. Climatic irregularities, supply chain bottlenecks and inconsistent crop yields can lead to volatility in ingredient quality and availability. This variability affects the stability of feed production cycles and increases operational costs for manufacturers. Additionally, competition from other livestock segments for the same raw materials intensifies supply constraints, resulting in inconsistent nutrient profiles. Limited storage infrastructure in developing markets compounds the challenge, making it harder to maintain year-round feed quality. Environmental pressures and land-use restrictions further limit the expansion of raw material cultivation, tightening the long-term supply outlook.

The rise of sustainable and functional feed innovations offers compelling opportunities for the Dairy Cattle Feed Market, driven by increasing demand for environmentally responsible and performance-enhancing solutions. Methane-reducing feed additives, enzyme-enriched supplements and organic mineral blends are gaining traction as dairy farms worldwide seek to enhance productivity while meeting evolving sustainability mandates. Functional additives can reduce enteric emissions by up to 10–12% and simultaneously improve digestion efficiency. Growing interest in alternative ingredients such as algae-based proteins and fermented feed inputs also expands diversification opportunities for manufacturers. With more than 30% of dairy enterprises in advanced regions expected to adopt low-emission feed systems by 2028, opportunities for innovation, product differentiation and value-added formulations are expanding rapidly.

Regulatory pressures and quality-compliance requirements present a significant challenge to the Dairy Cattle Feed Market due to increasingly stringent standards related to feed safety, ingredient traceability and environmental impact. Manufacturers must adhere to rigorous nutrient composition guidelines, residue limits and sustainability benchmarks, requiring substantial investment in monitoring systems and testing infrastructure. Ensuring compliance across diverse supply chains—especially in regions with fragmented procurement systems—creates operational burdens. Additionally, mandates to reduce carbon footprints and promote sustainable ingredient sourcing increase overall production complexity. Meeting these requirements, while maintaining consistent feed quality and cost-effectiveness, is a persistent challenge for producers operating in competitive and resource-constrained environments.

• Expansion of Precision Nutrition and Data-Driven Feeding Systems: Precision nutrition is accelerating across dairy operations, with automated rationing systems now used by more than 40% of large-scale farms in high-productivity regions. These systems improve feed-to-milk conversion efficiency by 12–18%, supported by real-time nutrient profiling and digital monitoring tools. Adoption of AI-enabled feed optimisation platforms has increased by nearly 28% over the last two years, significantly reducing nutrient wastage and improving herd health outcomes.

• Rapid Growth of Methane-Reducing and Functional Feed Additives: The integration of methane-reducing additives and functional supplements has risen sharply, with usage expanding by 35% among commercial dairy farms. Trials show that these additives lower enteric emissions by 10–14% while increasing digestion efficiency by 8–11%. Enzyme-enriched and micro-mineral formulations are also seeing double-digit adoption growth, driven by regulatory pressure and producer demand for sustainability-aligned feed strategies.

• Shift Toward High-Protein Alternative Feed Ingredients: There is rising adoption of high-protein alternative ingredients such as algae-based proteins, fermented inputs and single-cell proteins, with usage increasing by 30% in regions facing conventional raw material shortages. These alternatives deliver 15–20% higher protein density compared to traditional oilseed cakes, enabling farms to maintain nutritional performance while mitigating supply chain volatility associated with maize and soymeal.

• Growth in Total Mixed Ration (TMR) and Mechanised Feeding Systems: Mechanised TMR systems are expanding rapidly, with implementation rates rising by 25% across medium- and large-scale dairy farms. These systems support consistent nutrient delivery, resulting in 10–16% improvements in overall feed utilisation efficiency. Automated mixers, distribution units and sensor-integrated feed wagons further enhance feeding precision, contributing to measurable gains in milk output and labour productivity.

The Dairy Cattle Feed Market is segmented across product types, applications and end-user categories, each contributing distinct strategic value. Types include compound feed, concentrates, Total Mixed Ration (TMR), forages and additives, each supporting different nutritional and operational needs. Applications span milk production enhancement, cattle health improvement, reproduction efficiency and immune support. End-user insights highlight commercial dairy farms, smallholder farms and integrated dairy cooperatives as primary consumers, with commercial farms driving the highest volume consumption due to structured feeding systems and technology adoption. Segment performance varies across regions, with advanced economies showing higher uptake of precision feed technologies and developing markets recording stronger reliance on conventional feed types.

Compound feed remains the leading type, accounting for approximately 46% of total adoption, supported by its balanced nutrient profiles and consistent performance across diverse dairy herd sizes. Concentrates follow with about 28% adoption due to their targeted nutrient density and widespread integration into intensive dairy production models. Total Mixed Ration (TMR) is the fastest-growing type, driven by structured feeding practices and measurable improvements in nutritional uniformity, expanding at an estimated 7.2% growth rate. Forages and specialty additives collectively contribute around 26%, forming niche yet essential components for rumen health, immunity and lactation efficiency. These smaller categories serve critical functional roles, especially in regions with variable forage quality.

Milk production enhancement dominates applications with roughly 48% market adoption, driven by measurable improvements in feed conversion efficiency and nutrient absorption across dairy herds. Health and immunity support applications follow at 27%, reflecting increased usage of supplements, mineral blends and functional additives that strengthen cattle resistance to metabolic and infectious disorders. Reproductive efficiency improvement is rising fastest, growing at about 6.8%, supported by improved micronutrient formulations and targeted fertility-enhancing feed components. Other applications, including growth performance and early-stage calf nutrition, collectively account for 25% of adoption, primarily contributing to long-term herd development and lifecycle productivity.

Commercial dairy farms lead end-user adoption with nearly 52%, supported by structured feeding protocols, high-volume feed requirements and rapid uptake of mechanised and precision nutrition tools. Smallholder farms hold approximately 30%, maintaining steady reliance on cost-effective feed formulations and regionally available ingredients. Integrated dairy cooperatives are the fastest-growing segment, advancing at an estimated 7.5% due to their coordinated procurement systems, shared technology infrastructure and centralised feeding strategies. Remaining end-users, including specialty breeders and research farms, contribute about 18% combined, typically focusing on targeted nutrition optimization or genetic improvement programs.

Asia-Pacific accounted for the largest market share at 41% in 2024; however, Europe is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

Asia-Pacific’s dominance is supported by its extensive dairy herd population exceeding 330 million cattle and high annual feed consumption surpassing 190 million tons. North America accounted for 27% share, driven by advanced precision nutrition and digital feeding systems adopted across more than 65% of commercial farms. Europe captured 22% of the market with strong sustainability mandates and methane-reducing feed adoption rates reaching 34%. South America and the Middle East & Africa collectively accounted for 10%, supported by expanding dairy production clusters and rising investment in feed formulation technologies.

How is digitalisation transforming the next phase of feed optimisation?

North America holds nearly 27% of the global Dairy Cattle Feed market, supported by large-scale commercial dairy operations and advanced livestock management systems. Key industries such as commercial dairy farming, feed manufacturing and livestock genetics drive consistent demand for high-nutrient formulations. Regulatory support promoting methane-reducing feed additives and animal welfare standards is reshaping formulation requirements. Technology adoption is high, with over 60% of large farms using automated feeding systems, sensor-driven TMR mixers and digital herd nutrition platforms. A notable regional player recently expanded its automated feed-mill capacity by 18% to support rising demand for precision-milled ingredients. Consumer behaviour in this region reflects early adoption of high-tech feeding solutions, mirroring broader enterprise behaviour in sectors like healthcare and finance where digital transformation exceeds 70% adoption.

How are sustainability-driven innovations influencing feed strategies across advanced markets?

Europe represents approximately 22% of the Dairy Cattle Feed market, led by major dairy-producing countries such as Germany, France and the Netherlands. Regional regulators enforce stringent sustainability mandates, driving adoption of low-emission feed additives and alternative protein sources. Over 34% of farms have adopted methane-reducing feed strategies, and precision nutrition tools are integrated into more than 45% of commercial dairy operations. Local producers continue to introduce fortified feed blends aligned with welfare and traceability standards. A leading European feed manufacturer recently implemented a high-efficiency pelletising line that improved production output by 14%. Consumer behaviour is strongly shaped by regulatory compliance, resulting in heightened demand for explainable and environmentally responsible feed solutions.

What drives the rapid expansion of high-performance feed systems across emerging dairy economies?

Asia-Pacific accounts for the highest market volume globally, anchored by China, India and Japan, which collectively host over 65% of the global dairy cattle population. Regional consumption of dairy cattle feed surpassed 190 million tons, supported by rapid industrialisation of dairy farms and expanding manufacturing infrastructure. Technological adoption is rising, including digitally optimised TMR systems, AI-integrated feed rationing and fermentation-based protein ingredients. A large regional feed producer recently scaled its amino-acid enriched feed production capacity by 22%, reflecting strong demand for performance-enhancing formulations. Consumer behaviour is influenced by rapid digital adoption, similar to trends seen in mobile-first sectors where app-based decision tools exceed 75% usage.

How are production clusters reshaping the nutritional strategies across emerging dairy zones?

South America, led by Brazil and Argentina, accounts for roughly 7% of the Dairy Cattle Feed market, supported by expanding dairy clusters and improving agricultural infrastructure. Brazil alone contributes over 60% of the region’s dairy feed consumption due to its large herd population and feedgrain availability. Governments in key countries continue to promote feed quality standards and offer incentives for local production of protein concentrates and by-product-based feeds. A regional feed company recently reported a 16% increase in protein concentrate output to meet growing demand from organised dairy farms. Consumer behaviour reflects strong localisation needs, similar to media and language-centric industries where regional content consumption exceeds 68%.

How are modernisation and sustainability shaping next-generation feed models?

The Middle East & Africa region holds approximately 3% of global Dairy Cattle Feed demand, driven by developing dairy operations in the UAE, Saudi Arabia, Egypt and South Africa. Regional demand trends are influenced by growing food security initiatives, large-scale dairy farm investments and rising reliance on imported feed ingredients. Technological modernisation is accelerating, with automated feeding systems and climate-responsive feed formulations being adopted across high-temperature regions. A leading dairy enterprise in the Middle East recently commissioned a new feed-optimisation facility achieving 12% higher formulation accuracy. Consumer behaviour reflects increasing preference for consistent, welfare-driven dairy production models supported by government-backed innovation and trade partnerships.

India – 24% share

High production capacity supported by the world’s largest dairy cattle population and rapid adoption of structured feeding systems.

China – 20% share

Strong end-user demand driven by industrialised dairy farms and expanding advanced feed manufacturing infrastructure.

The Dairy Cattle Feed market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 38% of the global share. More than 120 active competitors operate across regional and international levels, driving product diversification and continuous innovation. Companies are increasingly focusing on fortified feed formulations, enhanced amino acid profiles, and rumen-protected nutrients to strengthen their market positions. Strategic initiatives such as partnerships with dairy cooperatives, mergers to expand distribution networks, and investments in precision nutrition technologies are shaping the competitive dynamics.

Over the past two years, over 30 new feed formulations have been introduced globally, targeting efficiency improvement, higher milk yield, and improved animal health. Digital transformation is also accelerating competition, with around 45% of leading manufacturers integrating data-driven nutrition platforms to optimize feed recommendations. Sustainability-focused strategies—such as low-methane feed solutions and organic-certified formulations—are gaining traction, with nearly 28% of market leaders adopting eco-friendly production standards. The landscape continues to evolve as companies emphasize traceability, supply chain modernization, and advanced quality assurance systems to maintain competitive differentiation.

Cargill Incorporated

Archer Daniels Midland Company (ADM)

Nutreco N.V.

Land O’Lakes Inc.

Charoen Pokphand Foods Public Company Limited (CP Foods)

Alltech Inc.

De Heus Animal Nutrition

Purina Animal Nutrition

ForFarmers N.V.

Kent Nutrition Group

Technological advancements are reshaping the Dairy Cattle Feed market, driving higher productivity, improved animal health, and greater operational efficiency across dairy farms. Precision nutrition is one of the most transformative developments, with nearly 48% of large dairy farms now adopting data-driven feed formulation tools that analyze herd performance, forage quality, and metabolic needs to create optimized rations. Automated feed mixers and robotic distribution systems are also seeing increased deployment, particularly in high-volume farms where labor efficiency and consistency are critical; approximately 35% of commercial dairy operations have integrated automated feeding technologies to reduce wastage and improve feed uniformity.

Sensor-enabled health monitoring systems are becoming central to feed optimization strategies. Around 40% of mid-to-large dairy farms utilize wearable or bolus-based sensors to track rumination patterns, feed intake, and early signs of nutritional deficiencies. These real-time insights enable producers to adjust feed composition promptly, reducing health-related losses and increasing milk yield potential. Advanced fermentation technologies are further impacting the market by improving digestibility and enhancing nutrient absorption in silage and compound feed formulations.

Emerging technologies include methane-reducing feed additives, which have been adopted by nearly 18% of leading dairy producers seeking sustainability-linked performance improvements. Enzyme-based solutions and rumen-protected amino acids are also gaining traction, accounting for a combined 22% share of specialized feed inputs. Digital platforms that integrate herd management, feed budgeting, and procurement are expanding rapidly, with adoption rates nearing 30% globally. Collectively, these technological innovations are strengthening the efficiency, traceability, and environmental performance of dairy cattle feed systems, positioning technology as a major strategic differentiator in this evolving market.

In 2024, Cargill Incorporated acquired two feed mills from Compana Pet Brands in the U.S., strengthening its Animal Nutrition and Health business and expanding production and distribution capabilities across its full feed portfolio. (Feed and Additive)

In 2023, Trouw Nutrition expanded its research campus in the Netherlands by adding a dedicated dairy facility aimed at advancing sustainable dairy farming practices, including development of functional nutrition solutions and young-animal feed innovations. (Feed and Additive)

In 2024, global dairy feed tonnage rebounded by 3.2%, marking a recovery after a 2023 downturn, thanks to increased demand in regions including Asia-Pacific, Europe, Latin America, and Africa. (Feed Strategy)

In 2024, Novus International entered a partnership with Ginkgo Bioworks to develop advanced enzyme-based feed additives, targeting improved feed efficiency and enhanced nutritional outcomes for dairy cattle. (Dairy Global)

This Dairy Cattle Feed Market Report provides comprehensive coverage of all major dimensions shaping the industry: product types (compound feed, concentrates, TMR, forages, feed additives and premixes), application areas (milk yield enhancement, herd health and immunity, reproductive performance, calf nutrition, growth performance) and end-user segments (commercial dairy farms, smallholder farms, dairy cooperatives, specialty breeders and research farms). The geographic analysis spans all global regions — Asia-Pacific, North America, Europe, Latin America, South America, Middle East and Africa — capturing regional consumption patterns, production tonnage trends, feed mill growth, and shifts in feed formulation practices. The report also explores technology adoption, including precision nutrition systems, automated mixing and distribution equipment, sensor-based herd monitoring, enzyme and methane-reducing feed additives, and emerging nutritional innovations.

Additionally, the report analyses regulatory, environmental and sustainability drivers — including emissions mitigation, feed traceability, climate-adapted formulations and eco-compliance standards — and assesses how these pressures influence feed design, quality assurance and supply-chain investments. It incorporates data on feed production volumes, annual tonnage shifts, regional feed mill counts, and comparative adoption rates across various farm scales and geographies. Niche segments such as functional feed additives, organic/eco-certified feed, and methane-reducing premixes are also addressed, reflecting evolving market priorities. This breadth ensures that decision-makers and industry stakeholders gain a detailed understanding of current market structure, technological trends, regional dynamics and future growth pathways — enabling informed strategic planning, investment appraisal, and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1689.99 Million |

|

Market Revenue in 2032 |

USD 2796.93 Million |

|

CAGR (2025 - 2032) |

6.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Cargill Incorporated, Archer Daniels Midland Company (ADM) , Nutreco N.V. , Land O’Lakes Inc., Charoen Pokphand Foods Public Company Limited (CP Foods), Alltech Inc. , De Heus Animal Nutrition, Purina Animal Nutrition, ForFarmers N.V., Kent Nutrition Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |