Reports

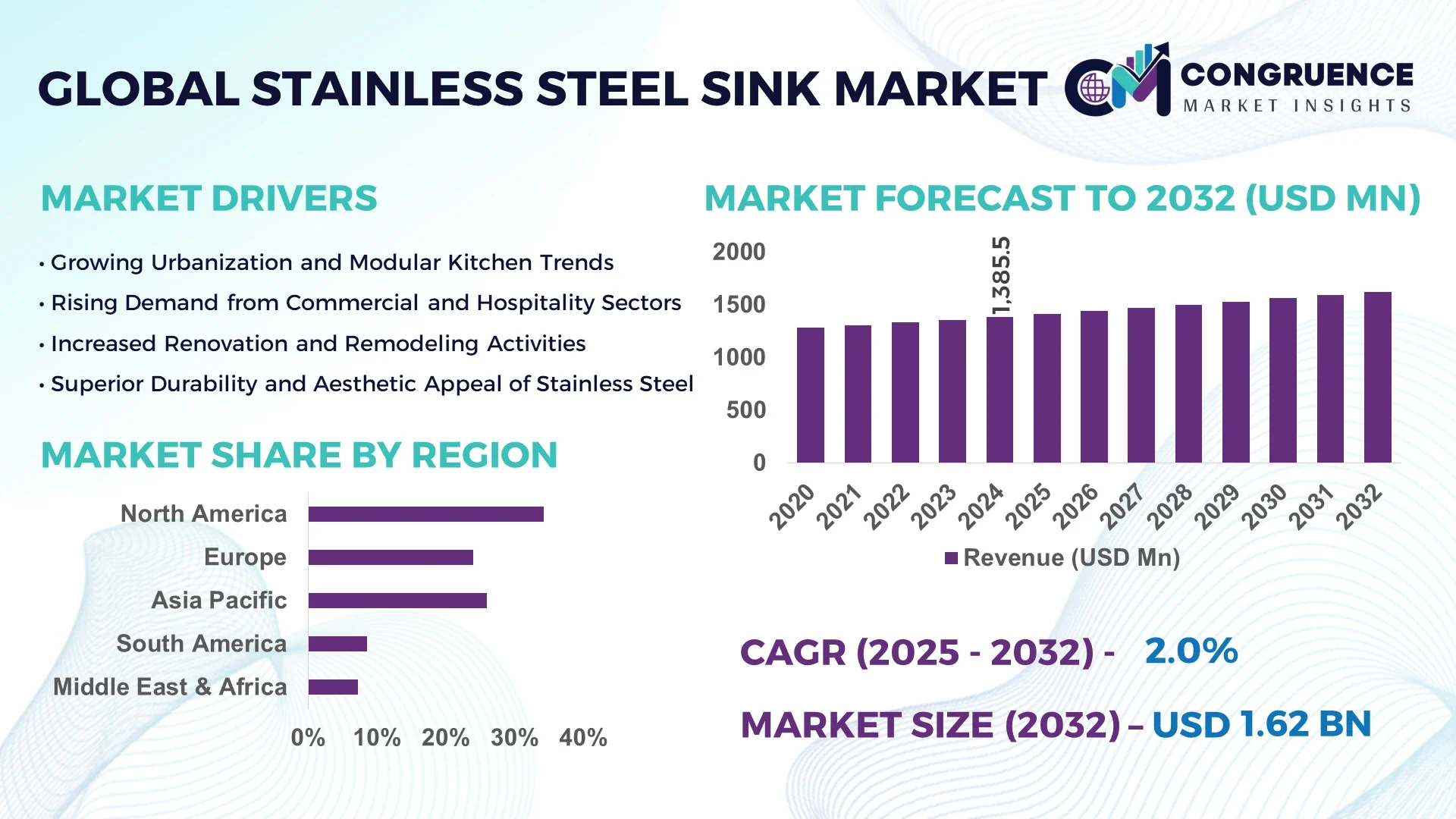

The Global Stainless Steel Sink Market was valued at USD 1,385.46 Million in 2024 and is anticipated to reach a value of USD 1,623.29 Million by 2032 expanding at a CAGR of 2.0% between 2025 and 2032.

China, as the leading country in the Stainless Steel Sink Market, has witnessed consistent investments in advanced stamping and seamless welding technologies, along with expanding automated sink fabrication lines and the integration of robotics for consistent quality across high-volume residential and commercial sink production.

The Stainless Steel Sink Market is experiencing a structured shift driven by the increasing demand for hygienic, durable, and corrosion-resistant kitchen solutions across the residential, commercial, and hospitality sectors. Recent product innovations, including integrated draining boards and anti-scratch coatings, are supporting premium product adoption, while smart sink designs with touchless faucet integration are aligning with evolving consumer preferences in urban centers. Regulatory drivers related to green building initiatives and water conservation are influencing manufacturers to adopt water-efficient and recyclable designs. Regionally, North America and Europe are observing a steady uptake of designer stainless steel sinks in modern residential projects, while the Asia-Pacific region continues to witness growing consumption supported by infrastructural growth and rising disposable incomes. The emerging trend of modular kitchens and commercial kitchen renovations is expected to strengthen the Stainless Steel Sink Market outlook further, aligning with evolving consumer focus on quality, design flexibility, and sustainability.

Artificial Intelligence is playing a pivotal role in the evolution of the Stainless Steel Sink Market by enhancing operational performance, production quality, and efficiency across manufacturing facilities. AI-powered visual inspection systems are now being used to detect micro-defects during sink fabrication, reducing rejection rates and ensuring consistent quality, which is critical for premium product lines targeting luxury residential and commercial installations. Additionally, AI-driven demand forecasting is helping manufacturers align production volumes with regional and seasonal consumption patterns, reducing inventory overhead and optimizing the supply chain across the Stainless Steel Sink Market. Machine learning algorithms are being applied to predictive maintenance for hydraulic presses and robotic welding systems, minimizing unplanned downtime and ensuring seamless operations in large-scale stainless steel sink production lines.

Smart design software leveraging AI is facilitating custom sink design for B2B clients in the hospitality and real estate sectors, accelerating prototyping while reducing design cycle time. Furthermore, AI-integrated robotic arms are enabling precision cutting and seamless welding, ensuring the sinks meet consistent dimensional accuracy requirements, which is critical in modern modular kitchen fittings. AI is also helping optimize water flow simulations during sink design, ensuring compliance with green building standards and water-saving initiatives, which is increasingly relevant in the Stainless Steel Sink Market as sustainability becomes a competitive differentiator. With growing global demand, AI is expected to further elevate efficiency and cost optimization, helping manufacturers adapt quickly to shifting design trends and regulatory requirements without compromising on quality, reinforcing its transformative impact across the Stainless Steel Sink Market.

“In March 2025, a leading stainless steel sink manufacturer integrated an AI-powered surface defect detection system in its production facility, which enabled the identification of micro-cracks and surface inconsistencies with a 98% accuracy rate, reducing quality inspection times by 40% while improving finished product consistency across large production batches.”

The Stainless Steel Sink Market is witnessing steady evolution driven by changing consumer preferences, regulatory pushes for sustainable and recyclable materials, and advancements in seamless sink design for residential and commercial applications. Increasing urbanization and a growing trend of modular kitchens have heightened the demand for aesthetically pleasing and durable stainless steel sinks. Additionally, the market is influenced by the rise of smart kitchen integrations, pushing manufacturers to innovate with anti-bacterial coatings and noise-reduction technologies in stainless steel sinks. Fluctuating raw material prices and stringent environmental standards on stainless steel production are also shaping the operational landscape. The market is further supported by the consistent growth of the construction and hospitality sectors across Asia-Pacific and the Middle East, where infrastructural developments are driving the adoption of modern kitchen fixtures. As design flexibility and premium quality become critical decision points for B2B and B2C consumers, manufacturers are focusing on enhancing production efficiency and expanding their distribution networks, making the Stainless Steel Sink Market dynamic and competitive.

The increasing consumer focus on hygiene and long-lasting kitchen solutions is a key driver for the Stainless Steel Sink Market. Stainless steel offers corrosion resistance, easy maintenance, and a non-porous surface, aligning with evolving consumer demands for hygiene, particularly in urban residential and commercial kitchen environments. The World Health Organization’s emphasis on hygiene has further accelerated the adoption of stainless steel sinks in healthcare, hospitality, and food service sectors. Additionally, consumers in North America and Europe prefer stainless steel sinks for their aesthetic compatibility with modern kitchen designs, while their ability to withstand high temperatures and resist stains contributes to their preference over other sink materials. This driver is also reinforced by the increasing adoption of modular kitchens, where stainless steel sinks are integral due to their flexibility in design and integration with smart faucets and accessories, ensuring continued growth across diverse sectors within the Stainless Steel Sink Market.

Fluctuating prices of stainless steel, driven by volatility in the global steel and nickel markets, act as a restraint on the Stainless Steel Sink Market, influencing production costs for manufacturers globally. Stainless steel prices are sensitive to global supply chain disruptions, energy costs, and geopolitical events, leading to unpredictable procurement expenses for sink manufacturers. Inconsistent raw material costs challenge manufacturers in maintaining stable pricing strategies, impacting competitiveness, especially in markets with high price sensitivity. Additionally, smaller manufacturers in emerging markets often face difficulties absorbing price fluctuations, which can lead to reduced profitability or delayed production schedules. This cost variability can influence the purchasing decisions of construction and real estate developers, who may delay projects or shift to alternative sink materials during periods of price spikes, temporarily restraining the market expansion for stainless steel sinks despite sustained demand.

The rising adoption of smart kitchen systems and sustainable living trends offers significant opportunities in the Stainless Steel Sink Market. Consumers are increasingly inclined toward smart sinks integrated with touchless faucets, water-saving technologies, and sensor-based filtration systems, aligning with environmentally conscious lifestyles. Additionally, the recyclable nature of stainless steel aligns with green building initiatives globally, creating an opportunity for manufacturers to position eco-friendly stainless steel sinks as preferred options for sustainable construction projects. Innovations such as anti-bacterial coatings and noise-reduction sink designs are capturing attention in the premium segment, meeting consumer demand for both functionality and comfort. This trend is particularly evident in North America and parts of Asia-Pacific, where modern housing projects and luxury hospitality developments are investing in advanced kitchen fixtures. By leveraging these opportunities, manufacturers can diversify their offerings and cater to evolving consumer expectations, thereby expanding their footprint in the Stainless Steel Sink Market.

Technological adaptation and the availability of a skilled workforce are significant challenges impacting the Stainless Steel Sink Market. The market’s transition toward AI-driven inspection systems, robotic welding, and advanced surface treatment technologies requires substantial investment in automation and skilled technicians capable of managing and maintaining these systems. Small and medium-sized manufacturers in developing economies often face challenges in adopting these technologies due to financial constraints and limited technical expertise, affecting their production efficiency and product quality consistency. Additionally, the training and retention of skilled labor for operating advanced fabrication machinery and ensuring high-precision manufacturing remain challenging in regions with labor shortages. These factors can slow the market’s ability to meet the increasing demand for premium stainless steel sinks with enhanced features, impacting the competitive dynamics and scalability of production across the Stainless Steel Sink Market.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping demand within the Stainless Steel Sink market, particularly in Europe and North America, where construction efficiency and waste reduction are critical. Manufacturers are investing in advanced CNC and laser-cutting machines to produce pre-bent, high-precision sink components for modular kitchens and commercial installations. These prefabricated stainless steel sink units are helping developers reduce on-site labor requirements and project turnaround times by up to 30%, aligning with the rising demand for quick-deployment housing and hospitality projects.

• Integration of Smart Features in Sink Designs: The Stainless Steel Sink market is witnessing the integration of touchless faucets, sensor-driven water management systems, and anti-bacterial coatings in sink products. This trend is fueled by heightened hygiene awareness in both residential and commercial sectors, with manufacturers reporting a 25% increase in demand for sinks compatible with smart kitchen ecosystems. This shift is encouraging the development of sinks that can seamlessly integrate with water filtration and greywater recycling systems, aligning with green building standards globally.

• Advances in Noise Reduction and Anti-Scratch Technology: Manufacturers in the Stainless Steel Sink market are increasingly focusing on adding anti-scratch coatings and soundproofing undercoatings to their sink products to enhance user experience and durability. These advancements are gaining traction in the premium residential and hospitality sectors, with sound-deadening sink models reducing operational noise levels by up to 40%. The anti-scratch technologies are proving vital for urban residential consumers seeking durable yet stylish kitchen fixtures.

• Demand Surge in Luxury Residential and Hospitality Projects: The increasing construction of luxury residential apartments and high-end hotels across Asia-Pacific and the Middle East is fueling demand for designer stainless steel sinks with seamless finishes and premium aesthetics. Projects are specifying sinks with integrated drainboards and sleek under-mount designs to complement high-value modular kitchens. Manufacturers are responding by expanding their designer lines, offering customizable sink sizes and finishes, which is supporting a differentiated product landscape within the Stainless Steel Sink market.

The Stainless Steel Sink market is segmented based on type, application, and end-user categories to analyze evolving patterns shaping its competitive landscape. By type, the market encompasses single-bowl, double-bowl, integrated drainboard sinks, and custom-built sink variants, each catering to different residential and commercial requirements. Application segmentation covers household, hospitality, healthcare, and food service sectors, with household and hospitality showing strong consumption trends. End-user segmentation reveals trends across residential, commercial kitchens, hospitals, and institutional facilities, each demanding sinks with durability, hygiene, and specific design compatibilities. Manufacturers are aligning product development strategies with these segmentation insights to optimize production planning, innovation pipelines, and distribution channels to address market-specific requirements efficiently.

The Stainless Steel Sink market includes single-bowl, double-bowl, triple-bowl, integrated drainboard, and custom sinks, with single-bowl sinks leading due to their space efficiency and suitability for compact kitchens, particularly in urban residential projects. Double-bowl sinks are witnessing increasing demand in the hospitality and food service industries, driven by their functionality for multitasking and efficient cleaning operations in high-use environments. Integrated drainboard sinks are emerging as the fastest-growing type, favored for their convenience in modern modular kitchens, reducing countertop clutter while supporting ergonomic kitchen designs. Triple-bowl sinks maintain a niche presence, primarily in high-capacity commercial kitchens where separation of cleaning processes is essential. Custom sinks are gaining traction among premium residential buyers seeking design flexibility, supporting the trend toward personalization in luxury kitchen projects while maintaining the core durability and hygiene advantages of stainless steel sinks.

Applications in the Stainless Steel Sink market span residential households, commercial kitchens, hospitality, healthcare facilities, and food service industries. The residential household segment leads due to the continuous demand for durable, hygienic, and design-flexible kitchen fixtures, aligned with the rise of modular kitchens and urban apartment constructions. The hospitality segment is the fastest-growing application area, driven by the boom in luxury hotel and restaurant developments requiring aesthetically advanced and functional sink solutions to meet premium interior standards and operational efficiency. Healthcare facilities increasingly utilize stainless steel sinks for their anti-bacterial and corrosion-resistant properties, essential for maintaining hygiene standards, while food service industries depend on high-capacity sinks for consistent cleaning and food preparation workflows, further supporting the steady expansion of the Stainless Steel Sink market across applications.

In the Stainless Steel Sink market, the residential end-user segment leads due to consistent demand from urban housing and apartment renovations requiring reliable, space-efficient sink solutions. The commercial kitchen segment, covering restaurants and catering businesses, is the fastest-growing end-user segment as the global hospitality sector expands, requiring durable sinks capable of withstanding high-frequency usage while maintaining hygiene. Hospitals and healthcare facilities represent a steady end-user base due to strict hygiene requirements and a preference for easy-to-clean stainless steel fixtures, ensuring compliance with sanitation standards. Institutional facilities, including schools and community kitchens, contribute to the market landscape with demand for durable sinks capable of handling heavy daily use, further reinforcing the market’s comprehensive reach across end-user categories while emphasizing product versatility and reliability in diverse operational settings.

North America accounted for the largest market share at 34.2% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 3.2% between 2025 and 2032.

The Stainless Steel Sink market in North America remains dominant due to advanced manufacturing capacities and strong demand from premium residential and commercial projects. The region benefits from widespread renovation activities and modular kitchen adoption, particularly in the United States and Canada, where technological integration in sink designs is rapidly advancing. Asia-Pacific, led by China and India, is witnessing accelerated urbanization, infrastructural growth, and expanding disposable incomes, creating a rising demand for durable, hygienic, and design-flexible stainless steel sinks across residential, hospitality, and healthcare sectors. Government initiatives promoting smart cities and sustainable construction further bolster growth in the region. Europe continues to maintain a stable position with environmentally driven demand, while South America and the Middle East & Africa display steady uptake due to expanding urban infrastructure, evolving consumer preferences, and rising hospitality sector investments, collectively supporting the stainless steel sink market’s balanced global growth trajectory.

Premium Kitchen Upgrades Drive Sink Innovation

The Stainless Steel Sink market in this region held a market share of 34.2% in 2024, supported by robust demand from the residential remodeling and luxury housing sectors. The market benefits from the rising adoption of modular kitchen designs across urban centers, driven by evolving consumer preferences for hygienic, durable, and noise-resistant sink solutions. The healthcare and hospitality industries are key contributors to demand, with hospitals and hotels emphasizing easy-to-maintain kitchen fixtures that align with health standards. Regulatory support for water conservation and building efficiency codes is shaping product development, encouraging the introduction of touchless faucets and water-saving sinks. Technological advancements, including AI-powered quality checks and precision fabrication, are enhancing production consistency while supporting digital transformation initiatives in manufacturing, ensuring premium sink quality that aligns with sustainability and design flexibility expectations in the Stainless Steel Sink market.

Eco-Friendly Kitchen Solutions Boost Market Demand

The Stainless Steel Sink market in this region accounted for a market share of 28.7% in 2024, driven by consistent demand from the residential renovation and hospitality sectors. Germany, the UK, and France are among the top markets, emphasizing energy efficiency and sustainability in kitchen fixtures. Regulatory bodies focusing on green building initiatives and recycling are influencing manufacturers to adopt eco-friendly production processes and recyclable material use in sinks. The market is witnessing increased adoption of integrated drainboard sinks and under-mount sink designs that align with modern European kitchen aesthetics. Technological advancements such as precision robotic welding, advanced surface treatments for anti-scratch properties, and noise reduction features are enhancing product offerings. These innovations are integrated into the Stainless Steel Sink market as part of digital transformation efforts by manufacturers to meet evolving European Union environmental standards and consumer expectations for functional, stylish kitchen solutions.

Urbanization Fuels Stainless Steel Sink Adoption

The Stainless Steel Sink market in this region is ranked as the fastest-growing globally, with China, India, and Japan being the top consuming countries for stainless steel sinks across residential and commercial applications. The region’s demand is fueled by rapid urbanization and the expansion of middle-class housing, driving the uptake of durable, corrosion-resistant sinks in modular kitchens. Manufacturing hubs in China are leveraging automated fabrication lines and robotic welding for cost-effective, high-volume sink production. Infrastructure projects across India and Southeast Asia are further supporting demand from the hospitality and healthcare sectors, where stainless steel sinks align with hygiene and durability needs. Regional technology adoption includes the implementation of AI-driven surface inspections and digital quality control to enhance consistency in sink production, supporting evolving consumer preferences for premium, design-flexible sinks across diverse applications within the Stainless Steel Sink market.

Construction Expansion Spurs Sink Market Growth

The Stainless Steel Sink market in this region is witnessing steady demand growth, particularly in Brazil and Argentina, where expanding urban infrastructure and commercial construction are driving sink installations. Brazil leads the regional market with a strong residential construction pipeline and hospitality sector investments, contributing to the adoption of stainless steel sinks for their durability and ease of maintenance. The regional market share stood at 6.8% in 2024, supported by rising disposable incomes and modernization initiatives in urban centers. Energy sector expansions and government incentives promoting infrastructural development are indirectly supporting demand for high-quality kitchen fixtures, while trade policies facilitating the import of stainless steel components help stabilize supply chains. Manufacturers in the Stainless Steel Sink market are leveraging regional growth trends to introduce premium, ergonomically designed sink models that cater to evolving urban residential and hospitality sector needs.

Hospitality and Healthcare Investments Elevate Demand

The Stainless Steel Sink market in this region is experiencing growing demand driven by construction activities across the hospitality and healthcare sectors, with the UAE and South Africa being the major growth contributors. Regional demand trends align with infrastructure development, including luxury hotel projects and hospital expansions that require durable, hygienic kitchen solutions. The market accounted for a share of 5.1% in 2024, supported by technological modernization in construction and the rising adoption of modular kitchen designs in premium residential projects. Digital transformation in local manufacturing facilities includes the implementation of advanced fabrication methods and precision welding to improve product quality and meet international standards. Trade partnerships and local regulations encouraging the use of recyclable and water-efficient kitchen fixtures are further supporting the Stainless Steel Sink market, as regional consumers increasingly prioritize quality and sustainability in kitchen installations.

China – 22.5% market share: Dominates the Stainless Steel Sink market due to its high production capacity and widespread integration of automated manufacturing technologies.

United States – 18.4% market share: Leads with strong end-user demand from premium residential remodeling and commercial sectors within the Stainless Steel Sink market.

The Stainless Steel Sink market features a highly competitive environment with over 150 active global and regional manufacturers strategically positioned to cater to residential, commercial, and hospitality sectors. The competitive landscape is shaped by continuous product innovation, with companies focusing on introducing sinks with anti-bacterial coatings, noise-reduction underlayers, and integrated drainboard designs to align with evolving consumer preferences for hygiene and convenience. Strategic initiatives such as partnerships with modular kitchen manufacturers and collaborations with real estate developers are strengthening distribution networks, particularly in North America, Europe, and Asia-Pacific. Recent product launches featuring touchless faucet compatibility and under-mount sink designs are gaining traction in premium segments, while players are investing in advanced CNC machining and AI-powered quality inspection to improve consistency and reduce defect rates. Mergers and acquisitions are also reshaping the competitive dynamics, with key players acquiring regional manufacturers to expand their production capacities and local market presence. This competitive environment compels market players to focus on quality, design flexibility, and regional customization to retain their positioning in the Stainless Steel Sink market while addressing regulatory shifts and consumer demand for sustainable products.

Franke Holding AG

Elkay Manufacturing Company

Kohler Co.

Blanco GmbH + Co KG

Teka Group

Kraus USA

Moen Incorporated

Zuhne

Ruvati USA

American Standard Brands

Technological advancements are reshaping the Stainless Steel Sink market by enhancing manufacturing efficiency, product durability, and design flexibility. Robotic welding systems are increasingly utilized to achieve seamless joints and consistent quality in sink fabrication, supporting high-volume production while maintaining precision. Advanced CNC laser-cutting machines are enabling manufacturers to produce complex sink shapes and integrated drainboard designs with reduced material waste, aligning with sustainable manufacturing goals. AI-powered surface inspection systems have been adopted to detect micro-defects and inconsistencies during production, improving overall product quality and reducing rejection rates by up to 30%. Noise-reduction technologies, including specialized undercoatings and layered construction, are being implemented in premium sink models to address consumer demand for quieter kitchen environments.

Emerging anti-bacterial coating technologies are also gaining traction, providing sinks with enhanced hygiene and surface protection in residential and commercial applications. Water-efficient and smart sink designs, capable of integrating touchless faucets and filtration systems, are being developed to align with growing demand for sustainable and smart kitchen solutions. The use of recyclable and high-grade stainless steel alloys in sink manufacturing is supporting environmental goals while providing corrosion resistance and longevity. Collectively, these technological innovations are advancing the Stainless Steel Sink market by improving operational efficiency, aligning with environmental standards, and meeting evolving consumer expectations in design and performance.

• In March 2024, Franke launched a new series of stainless steel sinks featuring integrated anti-bacterial coatings, providing 99% bacteria reduction on sink surfaces and supporting enhanced hygiene in residential and commercial kitchen installations.

• In August 2023, Elkay Manufacturing introduced an AI-powered surface inspection system at its Illinois facility, enabling real-time defect detection and reducing quality inspection time by 35% across high-volume sink production lines.

• In October 2023, Kohler unveiled a premium under-mount stainless steel sink line equipped with advanced noise-reduction undercoatings, reducing operational noise by up to 40% to enhance user comfort in high-end residential kitchens.

• In February 2024, Blanco implemented automated robotic welding lines in its European manufacturing plant, increasing production efficiency by 28% while achieving precise, seamless sink finishes for its latest design-focused product range.

The Stainless Steel Sink Market Report comprehensively covers the competitive and operational landscape across key global regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It examines product segmentation, including single-bowl, double-bowl, integrated drainboard, and custom sinks, highlighting their adoption across residential, hospitality, healthcare, and food service applications. The report explores emerging trends such as the adoption of modular kitchen systems, anti-bacterial coatings, and noise-reduction technologies that align with evolving consumer and regulatory demands for hygiene, sustainability, and design flexibility in kitchen fixtures.

It analyzes the technological landscape, focusing on AI-powered quality inspection, robotic welding, advanced CNC fabrication, and smart sink integrations with water-saving and touchless faucet systems. The scope also extends to identifying demand drivers within premium residential projects, modular housing developments, and high-capacity commercial kitchens, as well as detailing factors influencing procurement strategies, including raw material quality, design customization, and regulatory compliance requirements. By covering the operational strategies, technological advancements, and emerging opportunities across market segments, the report provides a structured, data-driven foundation for stakeholders seeking informed insights and actionable perspectives in the Stainless Steel Sink market globally.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1,385.46 Million |

|

Market Revenue in 2032 |

USD 1,623.29 Million |

|

CAGR (2025 - 2032) |

2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Franke Holding AG, Elkay Manufacturing Company, Kohler Co., Blanco GmbH + Co KG, Teka Group, Kraus USA, Moen Incorporated, Zuhne, Ruvati USA, American Standard Brands |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |