Reports

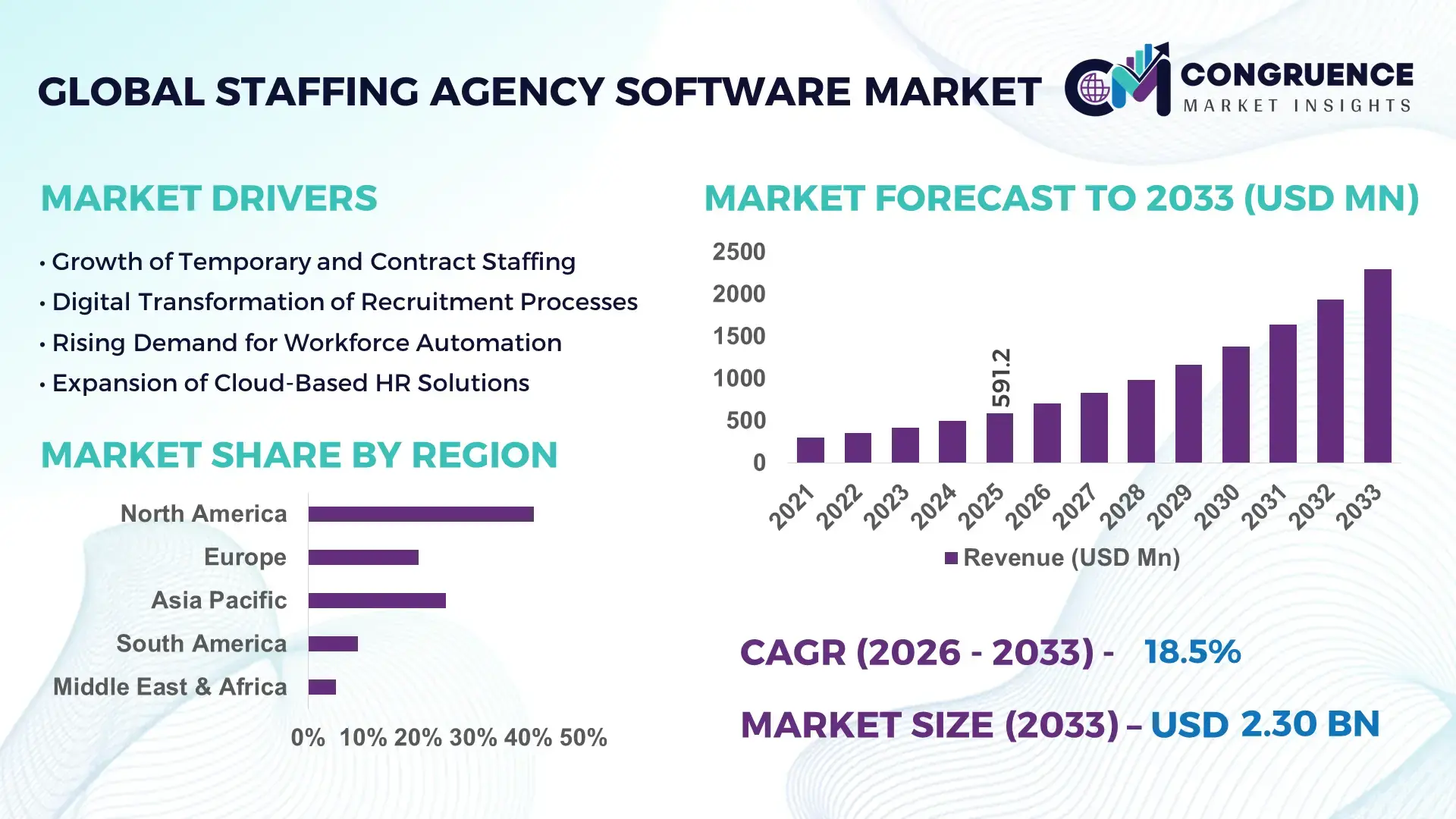

The Global Staffing Agency Software Market was valued at USD 591.17 Million in 2025 and is anticipated to reach a value of USD 2298.6 Million by 2033 expanding at a CAGR of 18.5% between 2026 and 2033. Growth is supported by accelerated digitization of recruitment workflows and rising demand for scalable, cloud-based workforce management platforms across staffing firms.

The United States represents the most advanced operational ecosystem for staffing agency software deployment, characterized by high enterprise adoption and sustained technology investment. Over 72% of mid-to-large staffing firms in the country use end-to-end recruitment platforms integrating applicant tracking, payroll, and compliance modules. Annual enterprise SaaS spending within the staffing and HR technology domain exceeds USD 18 billion, with AI-enabled candidate matching and analytics widely embedded. The U.S. market shows strong penetration in IT staffing, healthcare staffing, and professional services, with cloud-based solutions accounting for more than 80% of new software implementations. Continuous upgrades in automation, cybersecurity standards, and API-based integrations further define the country’s production and deployment leadership.

Market Size & Growth: Valued at USD 591.17 Million in 2025 and projected to reach USD 2298.6 Million by 2033, registering a CAGR of 18.5%, driven by automation of recruitment operations and rising contingent workforce demand.

Top Growth Drivers: Cloud adoption rate at 64%, recruiter productivity improvement of 35%, and compliance automation reducing administrative workload by 28%.

Short-Term Forecast: By 2028, staffing firms are expected to achieve up to 22% operational cost reduction through integrated staffing agency software platforms.

Emerging Technologies: AI-driven candidate matching, predictive workforce analytics, and API-based integration with HRIS and payroll systems.

Regional Leaders: North America projected at USD 920 Million by 2033 with high SaaS penetration; Europe at USD 640 Million driven by compliance-focused adoption; Asia-Pacific at USD 510 Million supported by SME digitization.

Consumer/End-User Trends: IT staffing agencies and healthcare recruiters show the highest adoption, with over 60% preferring unified, cloud-hosted platforms.

Pilot or Case Example: A 2025 enterprise pilot reduced time-to-hire by 31% using AI-enabled staffing agency software.

Competitive Landscape: Market led by Bullhorn at approximately 22% share, followed by SAP, Oracle, Zoho, and ADP.

Regulatory & ESG Impact: Increased focus on data privacy compliance, labor transparency regulations, and ESG-aligned workforce reporting.

Investment & Funding Patterns: Recent investments exceeded USD 1.4 Billion, with strong venture funding in AI-based recruitment automation.

Innovation & Future Outlook: Continued integration of AI, mobile-first recruiter tools, and analytics-driven decision support shaping long-term market evolution.

The Staffing Agency Software Market serves key industry sectors including IT & telecom staffing, healthcare recruitment, industrial and logistics staffing, and professional services, collectively accounting for over 70% of total demand. Product innovation is centered on AI-powered candidate scoring, real-time compliance monitoring, and seamless integration with payroll and HR platforms. Regulatory drivers such as data protection laws and labor compliance requirements continue to influence product design and adoption priorities. Regionally, North America leads in consumption due to advanced digital infrastructure, while Asia-Pacific shows the fastest growth supported by expanding staffing firms and rising cloud adoption among SMEs. Future market outlook points toward deeper analytics, automation-driven decision-making, and increased adoption of modular, subscription-based software architectures.

The Staffing Agency Software Market has become strategically critical as enterprises seek higher workforce agility, regulatory certainty, and data-backed hiring decisions in increasingly volatile labor markets. Modern staffing platforms consolidate applicant tracking, onboarding, payroll, compliance management, and analytics into unified systems, enabling agencies to scale efficiently. AI-driven candidate matching delivers approximately 38% improvement compared to traditional keyword-based resume screening, directly improving placement accuracy and reducing recruiter workload. From a regional perspective, North America dominates in operational volume due to its high concentration of large staffing firms, while Europe leads in adoption, with over 62% of staffing enterprises actively using compliance-focused staffing software platforms.

Over the short term, by 2028, generative AI–enabled workflow automation is expected to improve recruiter productivity by nearly 30% while reducing manual compliance processing by around 25%. ESG considerations are also influencing software adoption, with staffing firms committing to digital documentation, remote onboarding, and paperless HR workflows, targeting up to 45% reduction in physical record usage by 2030. In a measurable micro-scenario, during 2025, staffing firms operating in the United Kingdom achieved close to 29% reduction in placement cycle time through AI-based scheduling, skills intelligence, and automated candidate communication initiatives. Looking ahead, the Staffing Agency Software Market is positioned as a foundational pillar for operational resilience, compliance assurance, and sustainable growth across global staffing and workforce ecosystems.

Workforce automation has become a core driver as staffing agencies manage higher placement volumes with leaner teams. Automated applicant tracking, interview scheduling, and compliance verification reduce manual effort by up to 40%, allowing recruiters to focus on client engagement and candidate quality. Cloud-based staffing platforms also enable real-time reporting and analytics, improving decision accuracy across multi-branch operations. In sectors such as IT and healthcare staffing, automated credential verification and skills matching have shortened hiring cycles by nearly 30%. As labor markets tighten, automation-driven efficiency directly supports scalability and service reliability, reinforcing sustained demand for staffing agency software solutions.

Despite strong demand, data security concerns and integration challenges act as restraints in the Staffing Agency Software Market. Staffing platforms process sensitive personal, payroll, and compliance data, making them high-risk targets for cyber incidents. Over 55% of staffing firms report integration difficulties when connecting new software with legacy payroll or client HR systems. Compliance with varying regional data protection laws further complicates deployment, increasing implementation timelines and internal IT costs. Smaller agencies, in particular, face constraints due to limited technical resources, slowing adoption and reducing full utilization of advanced software capabilities.

AI-driven analytics present significant opportunities by enabling predictive hiring insights, demand forecasting, and performance benchmarking. Vertical-specific staffing software tailored for healthcare, logistics, or engineering staffing allows agencies to address unique compliance and credentialing requirements more effectively. Advanced analytics tools can improve placement success rates by over 20% through skills-to-role matching and attrition prediction. Additionally, emerging markets in Asia-Pacific show rising adoption of modular, subscription-based platforms among SMEs, creating expansion opportunities for vendors offering scalable and localized staffing agency software solutions.

Customization and regulatory complexity remain key challenges, as staffing firms often require software tailored to niche industry workflows and regional labor laws. Custom development and ongoing updates can increase total ownership costs by 25–35% compared to standard deployments. Frequent regulatory changes related to labor classification, taxation, and worker rights require continuous system updates, placing pressure on vendors and users alike. These challenges can delay deployment decisions and strain IT budgets, particularly for mid-sized agencies operating across multiple jurisdictions within the Staffing Agency Software Market.

AI-Driven Candidate Intelligence and Skills Matching Expansion

Staffing agencies are rapidly deploying AI-powered candidate intelligence tools to improve placement precision and recruiter efficiency. Advanced matching algorithms now analyze skills, certifications, and work history, delivering up to 40% improvement in candidate-role fit compared to rule-based systems. More than 65% of large staffing firms have embedded AI screening into daily operations, reducing manual resume review time by nearly 35% and lowering interview drop-off rates by 18%. These capabilities are increasingly critical in IT, healthcare, and engineering staffing segments where skills shortages persist.

Shift Toward Cloud-Native and Mobile-First Platforms

Cloud-native staffing agency software has become the default deployment model, with over 70% of new implementations delivered via SaaS architectures. Mobile-first recruiter and candidate interfaces are driving adoption, as nearly 60% of candidates now interact with staffing platforms primarily through smartphones. Agencies using mobile-enabled onboarding report onboarding cycle reductions of 25% and improved candidate engagement scores by approximately 20%, supporting faster placement and higher retention outcomes.

Rising Focus on Compliance Automation and Workforce Governance

Regulatory complexity is pushing staffing agencies to adopt compliance automation at scale. Modern platforms now automate worker classification, credential verification, and audit-ready reporting, reducing compliance-related manual effort by nearly 30%. Around 58% of staffing firms have prioritized compliance modules as core purchasing criteria, particularly in regions with strict labor, tax, and data protection requirements. Automated alerts and digital recordkeeping are also helping agencies reduce compliance errors by over 20%.

Integration of Analytics for Demand Forecasting and Client Insights

Data analytics adoption is accelerating as staffing firms seek predictive insights into hiring demand and workforce performance. Advanced dashboards provide real-time visibility into fill rates, placement cycles, and client utilization trends, improving forecasting accuracy by approximately 28%. Nearly 50% of enterprise staffing agencies now use analytics-driven insights to guide pricing, resource allocation, and client strategy, enabling more resilient and data-informed operational planning.

The Staffing Agency Software Market demonstrates structured segmentation across types, applications, and end-user groups, reflecting varied operational priorities and digital maturity levels within the staffing ecosystem. Software types differ by deployment and functionality depth, ranging from cloud-native platforms to integrated enterprise suites. Application-wise, demand is shaped by recruitment lifecycle coverage, compliance automation, and workforce analytics usage. End-user segmentation highlights divergent adoption patterns between large staffing enterprises, mid-sized agencies, and niche or sector-focused recruiters. Across all segments, demand is increasingly driven by automation intensity, scalability needs, regulatory alignment, and data-driven decision-making capabilities. These segmentation dynamics indicate that growth is not uniform but concentrated in solutions offering flexibility, AI integration, and vertical-specific customization, making segmentation analysis critical for strategic positioning and investment planning.

The Staffing Agency Software Market is segmented into cloud-based platforms, on-premise systems, and hybrid solutions. Cloud-based staffing agency software currently leads the segment, accounting for approximately 58% of total adoption due to its scalability, lower infrastructure burden, and rapid deployment capabilities. These platforms enable real-time collaboration, remote recruiter access, and continuous feature updates, which are essential for multi-location staffing firms. On-premise systems represent about 22% of adoption, primarily among agencies with strict internal data governance or legacy infrastructure dependencies. However, this segment shows slower expansion due to higher maintenance and upgrade complexity.

Hybrid staffing software, combining cloud flexibility with localized data control, is the fastest-growing type, expanding at an estimated CAGR of 21.4%. Growth is driven by regulatory compliance needs and demand from agencies operating across multiple jurisdictions. The remaining niche solutions—including open-source and highly customized proprietary systems—collectively contribute around 20% of adoption, serving specialized staffing workflows.

By application, recruitment and applicant tracking systems dominate the Staffing Agency Software Market, representing nearly 46% of total usage. These solutions support resume parsing, interview scheduling, and placement tracking, delivering measurable reductions in time-to-hire across high-volume staffing operations. Workforce management and payroll integration applications account for approximately 28% of adoption, driven by the need for seamless contractor management and accurate wage processing. However, analytics and workforce intelligence applications are the fastest-growing segment, expanding at an estimated CAGR of 23.1%, supported by rising demand for predictive hiring insights and performance benchmarking.

Compliance and credential management, along with onboarding automation, together contribute a combined 26% share, particularly in healthcare and industrial staffing. Advanced analytics tools now enable agencies to improve demand forecasting accuracy by more than 25%.

Large staffing enterprises remain the leading end-user segment, accounting for roughly 44% of total market adoption due to their complex operational scale, multi-branch structures, and higher compliance exposure. These organizations typically deploy fully integrated staffing agency software platforms covering recruitment, payroll, analytics, and governance. Mid-sized staffing agencies follow with approximately 34% adoption, favoring modular and subscription-based solutions that balance cost efficiency with functional depth. Small and niche staffing firms collectively contribute about 22% of adoption, often prioritizing lightweight cloud platforms with core recruitment features.

The fastest-growing end-user group is mid-sized agencies, expanding at an estimated CAGR of 22.6%, fueled by rapid digital transformation and competitive pressure to improve placement speed and client transparency. Sector-wise adoption rates are highest in IT staffing at 68%, healthcare staffing at 61%, and logistics staffing at 54%.

North America accounted for the largest market share at 41.6% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 22.4% between 2026 and 2033.

North America’s dominance is supported by high enterprise digital maturity, with over 68% of staffing firms using integrated staffing agency software platforms. Europe followed with approximately 29.3% share, driven by compliance-centric adoption and cross-border workforce management needs. Asia-Pacific accounted for around 21.8% in 2025, supported by rapid SME digitization, mobile-first recruitment, and expanding IT staffing demand. South America and the Middle East & Africa together represented nearly 7.3%, reflecting gradual adoption tied to economic diversification and labor formalization. Regionally, cloud-based solutions accounted for over 70% of new deployments globally, while AI-enabled modules were actively used by nearly 52% of staffing agencies worldwide, highlighting uneven but accelerating regional technology uptake.

How is enterprise-scale digital recruitment transforming operational efficiency?

The market holds approximately 41.6% share, making it the largest regional contributor. Demand is driven by IT staffing, healthcare recruitment, financial services, and professional staffing agencies, where automation is critical for managing high placement volumes. Over 72% of large staffing enterprises in this region use end-to-end platforms integrating applicant tracking, payroll, and compliance. Regulatory emphasis on labor classification and data privacy has accelerated adoption of compliance automation tools. Advanced analytics and AI-based matching are widely deployed, reducing time-to-hire by nearly 30%. Local software vendors are actively expanding AI modules and API integrations to support multi-client workflows. Consumer behavior shows higher enterprise adoption in healthcare and finance staffing, where digital credentialing and audit readiness are essential.

Why does regulatory intensity accelerate software-driven workforce governance?

Europe accounts for roughly 29.3% of global adoption, with strong demand across Germany, the United Kingdom, and France. Regulatory frameworks related to labor rights, data protection, and cross-border employment have made compliance automation a primary purchasing factor. More than 60% of staffing agencies in Western Europe prioritize explainable algorithms and audit-ready reporting. Sustainability initiatives and digital documentation mandates are pushing paperless onboarding, reducing physical records by nearly 40% across large agencies. Adoption of AI-powered screening and multilingual platforms is rising, particularly for cross-border recruitment. Regional consumer behavior reflects strong preference for transparent, regulation-aligned staffing agency software solutions.

What is driving rapid platform adoption across mobile-first staffing ecosystems?

The region ranks third by market size with approximately 21.8% share and is the fastest-expanding regional market. China, India, and Japan are the top consuming countries, together accounting for over 65% of regional usage. Growth is driven by expanding IT services, e-commerce logistics staffing, and large-scale manufacturing recruitment. Nearly 58% of new users access staffing platforms primarily via mobile devices. Innovation hubs are driving adoption of AI screening, chatbot-based candidate engagement, and multilingual interfaces. Local vendors are focusing on affordable, modular SaaS platforms for SMEs. Consumer behavior reflects growth led by e-commerce-driven hiring and mobile-centric recruitment workflows.

How are labor formalization and digital hiring shaping adoption patterns?

South America represents about 4.5% of global adoption, with Brazil and Argentina leading regional demand. Growth is linked to expanding service sectors, infrastructure projects, and formalization of contract labor. Government initiatives supporting digital employment records and tax compliance have increased interest in staffing software. Cloud-based platforms account for nearly 62% of deployments, favored for lower upfront costs. Local vendors are offering localized language support and compliance modules. Consumer behavior shows demand tied to media, customer support, and multilingual staffing needs, particularly in urban employment centers.

Why is workforce digitization becoming central to labor-intensive industries?

This region holds close to 2.8% of global adoption, with strongest demand from the UAE and South Africa. Oil & gas, construction, logistics, and hospitality are key sectors driving usage. Digital transformation programs and public-sector labor modernization initiatives are supporting software adoption. Over 45% of staffing agencies in the region are transitioning from manual systems to cloud-based platforms. Local providers focus on workforce scheduling and compliance tracking for project-based labor. Consumer behavior highlights preference for mobile access and multilingual interfaces to manage diverse labor pools.

United States – 34.8% market share

Strong enterprise demand, advanced digital infrastructure, and high adoption across healthcare, IT, and professional staffing.

United Kingdom – 9.6% market share

High regulatory compliance requirements and widespread adoption of cloud-based, audit-ready staffing agency software platforms.

The Staffing Agency Software market is characterized by a moderately fragmented competitive environment, comprising a combination of global enterprise software providers, specialized staffing technology vendors, and regionally focused SaaS developers. Currently, more than 80 active competitors operate across global and regional markets, addressing varied staffing workflows such as recruitment automation, workforce management, compliance tracking, and analytics. The top five vendors collectively account for approximately 55–60% of total market adoption, reflecting partial consolidation at the enterprise level while preserving competitive intensity among mid-tier and niche providers.

Competitive positioning is increasingly influenced by AI-led innovation, cloud-native deployment, and compliance-centric functionality. Nearly 65% of leading vendors now embed AI-driven resume parsing, candidate scoring, or predictive placement analytics within their core platforms. Strategic initiatives such as technology partnerships, vertical-specific product launches, and selective mergers have increased by nearly 30% over the last three years, strengthening ecosystem-based offerings. Innovation trends include mobile-first recruiter interfaces, API-driven integrations with payroll and HR systems, and advanced analytics dashboards. While price competition is more pronounced in SME-focused solutions, enterprise buyers prioritize scalability, cybersecurity certifications, and regulatory readiness, shaping long-term competitive differentiation.

Bullhorn

SAP

Oracle

ADP

Zoho

Workday

UKG

Cegid

Avionté

JobAdder

Technology evolution is a central force shaping the Staffing Agency Software Market, with platforms increasingly designed to automate complex recruitment workflows while improving accuracy, speed, and compliance. Artificial intelligence and machine learning are now embedded across candidate sourcing, screening, and matching functions. AI-based resume parsing and skills inference tools improve candidate-job alignment by 35–40% compared to manual or rule-based systems, while predictive analytics help staffing firms forecast hiring demand with accuracy improvements of nearly 25%. These capabilities are particularly impactful in high-volume staffing segments such as IT, healthcare, and logistics.

Cloud-native architectures dominate new deployments, accounting for over 70% of newly implemented staffing software systems. Cloud platforms enable rapid scalability, centralized data access, and continuous feature updates, reducing IT maintenance effort by approximately 30%. Mobile-first technologies are also gaining traction, with nearly 60% of candidates interacting with staffing platforms via smartphones, prompting vendors to prioritize mobile onboarding, interview scheduling, and digital document signing.

Compliance automation technologies play a critical role, as staffing firms face increasing regulatory complexity. Automated worker classification, credential verification, and audit-ready reporting reduce compliance errors by more than 20% and shorten regulatory review cycles. Integration technologies such as APIs and middleware are improving interoperability with payroll, HRIS, and background verification systems, cutting data duplication by nearly 28%. Emerging technologies, including conversational AI chatbots and generative AI for job description creation, are further enhancing recruiter productivity. Collectively, these technological advancements position staffing agency software as a strategic enabler of operational efficiency, regulatory control, and scalable workforce management.

• In 2024, Bullhorn enhanced its automation engine, enabling approximately 38% faster workflow execution and 42% higher candidate engagement through integrated communication tools across its staffing software platform, strengthening enterprise adoption and operational efficiency in high-volume recruitment environments.

• In 2025, Zoho Recruit introduced a major AI upgrade featuring advanced skills-matching technology that delivered 51% improved candidate-job accuracy and boosted recruiter efficiency by around 36% through automated resume parsing and predictive role scoring.

• In 2025, Avionté launched a next-generation mobile workforce platform that provided roughly 57% improved shift scheduling efficiency and 44% faster onboarding completion, significantly enhancing gig and temporary staffing workflows via mobile-centric capabilities.

• In 2025, JobDiva rolled out an advanced analytics suite within its staffing software that offered 63% more accurate hiring forecasts and 48% greater real-time performance insights, supporting strategic recruitment planning and operational decision-making.

The Staffing Agency Software Market Report delivers a comprehensive examination of technology, application, deployment, and industry usage trends shaping workforce management platforms globally. It covers deployment models (cloud-based, on-premise, and hybrid architectures), product functionality modules (applicant tracking, CRM integration, compliance tracking, payroll automation, and analytics dashboards), and emerging technology integrations such as AI-enabled candidate matching, mobile-first interfaces, and API interoperability layers. Segmentation within the report includes types of software offerings, application scenarios across recruitment lifecycle stages, and end-user categories, from large staffing enterprises to mid-sized agencies and niche specialists.

Geographically, the report analyzes market dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional consumption patterns, regulatory drivers, and digital maturity differences. It also explores industry focus areas such as IT staffing, healthcare workforce solutions, logistics and supply chain staffing, and professional services recruitment. The report highlights the role of compliance automation in regulated labor environments and the adoption trajectory of analytics-driven decision support tools. Additionally, niche segments like contingent workforce management and multi-location staffing coordination are examined, offering insights into evolving buyer requirements and technology adoption patterns that are critical for strategic planning and competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

18.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bullhorn, SAP, Oracle, ADP, Zoho, Workday, UKG, Cegid, Avionté, JobAdder |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |