Reports

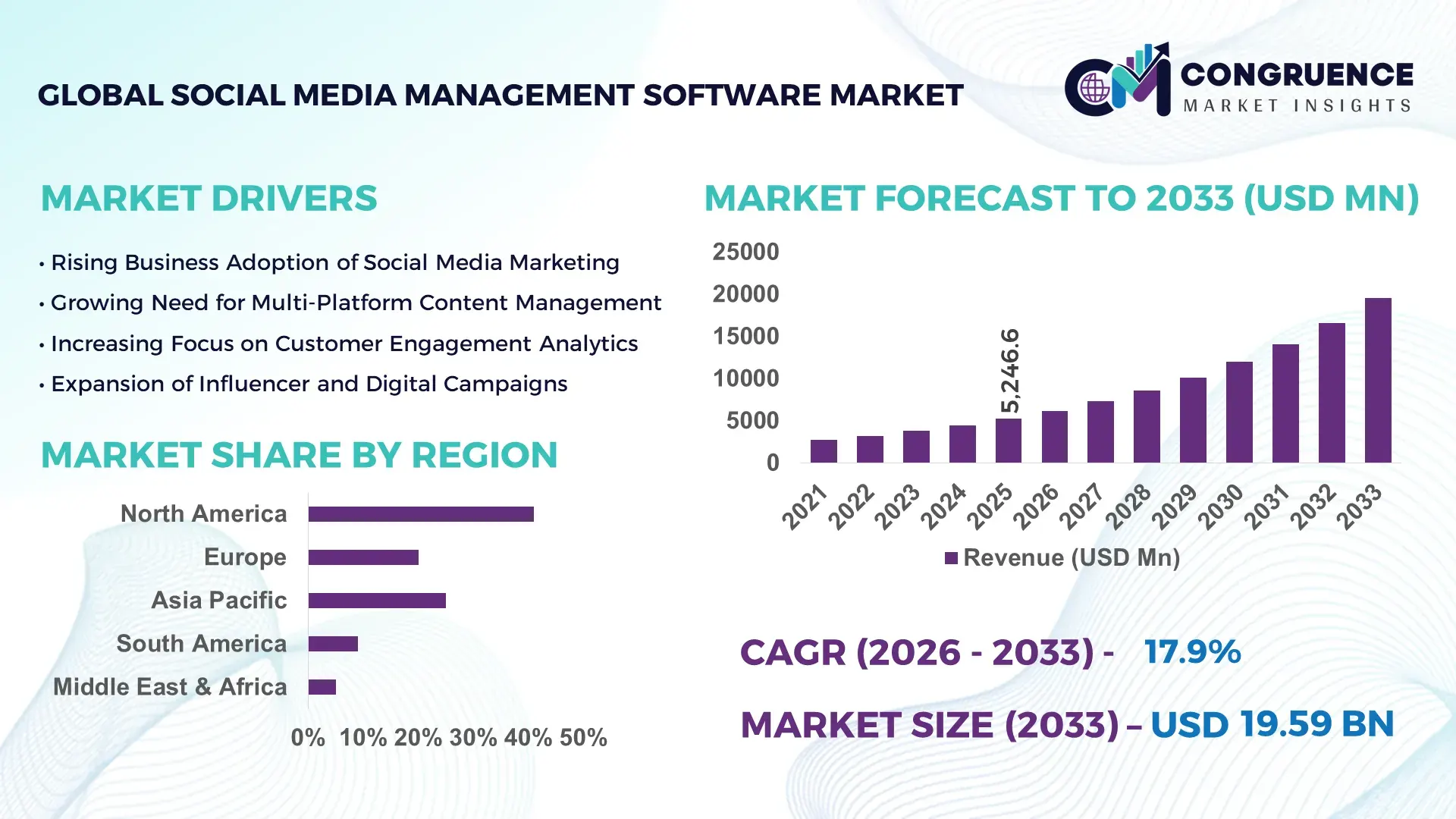

The Global Social Media Management Software Market was valued at USD 5246.57 Million in 2025 and is anticipated to reach a value of USD 19587.81 Million by 2033 expanding at a CAGR of 17.9% between 2026 and 2033. This growth is driven by the increasing need for unified digital engagement and analytics across platforms.

The United States leads the Social Media Management Software marketplace, with enterprises deploying advanced solutions across sectors such as retail, finance, and media. U.S. adoption rates in 2025 exceeded 72% among Fortune 1000 companies, with annual investments in social engagement platforms surpassing USD 1.8 billion. Production and development hubs in Silicon Valley and Austin feature over 120 dedicated SaaS firms, integrating AI-driven sentiment analysis and automation capabilities. U.S. firms report average campaign efficiency improvements of 38% through centralized dashboards and cross-channel scheduling tools.

Market Size & Growth: Valued at USD 5246.57 Million in 2025; projected USD 19587.81 Million by 2033 at a 17.9% CAGR supported by digital transformation and marketing automation adoption.

Top Growth Drivers: AI analytics adoption 54%; cross-platform engagement increase 62%; enterprise automation demand 48%.

Short-Term Forecast: By 2028, customer engagement efficiency expected to improve by 31% with integrated social CRM tools.

Emerging Technologies: AI-powered sentiment analysis, predictive content optimization, and real-time engagement bots.

Regional Leaders: North America ~USD 8.1B by 2033 with advanced adoption; Europe ~USD 4.6B driven by SME digitalization; Asia Pacific ~USD 3.8B with rapid mobile engagement growth.

Consumer/End-User Trends: High adoption in retail and finance; preference for unified dashboards and real-time insights.

Pilot or Case Example: 2025 pilot with integrated AI scheduling reduced content turnaround time by 27%.

Competitive Landscape: Market leader with ~22% share; key competitors include major enterprise SaaS providers and emerging specialized platforms.

Regulatory & ESG Impact: Data privacy regulations and brand compliance tools shaping platform requirements.

Investment & Funding Patterns: Recent investments exceeding USD 2.3B in venture funding for automation and analytics features.

Innovation & Future Outlook: Focus on AI-driven personalization, cross-channel attribution models, and deeper CRM integrations.

Social Media Management Software demand continues to surge across key industry sectors including retail, banking, and entertainment, where centralized campaign orchestration and analytics drive decision-making. Recent innovations such as predictive content scheduling, NLP-based sentiment tracking and API-first architectures are reshaping product offerings. Economic factors like digital marketing budget increases, regional consumption patterns in Asia-Pacific, and stringent data governance standards are influencing purchasing behavior. Emerging trends point to enhanced mobile management suites, real-time ROI dashboards, and expanded integrations with e‑commerce ecosystems, positioning the market for sustained growth through 2033.

The Social Media Management Software Market holds strategic relevance as enterprises seek unified digital engagement, heightened analytics precision, and scalable orchestration of multi‑platform campaigns. This software supports key organizational objectives including brand visibility, real‑time responsiveness, and data‑driven decision‑making across marketing and customer experience functions. Strategy formulations increasingly embed advanced automation and predictive AI tools, where predictive content optimization delivers 27% improvement compared to rule‑based scheduling standards in driving engagement benchmarks. North America dominates in deployment volume, while Europe leads in broad adoption with over 68% of enterprises integrating advanced social analytics and workflow automation tools into corporate martech stacks.

By 2028, generative AI is expected to improve sentiment analysis accuracy by up to 32%, directly enhancing campaign relevance and reducing manual monitoring workload. Firms are also committing to ESG improvements such as reducing digital carbon footprints through optimized scheduling and server utilization, targeting a 22% reduction in energy use by 2030. In 2025, a multinational retail firm achieved a 19% uplift in campaign efficiency through automated cross‑platform tagging and response workflows, showcasing measurable operational gains.

Looking ahead, the Social Media Management Software Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling enterprises to adapt to evolving consumer behavior, regulatory frameworks, and digital ecosystem complexities.

The proliferation of digital channels such as TikTok, Instagram, LinkedIn, and emerging platforms is a key driver of demand for Social Media Management Software Market solutions. Organizations face complexity in managing content calendars, audience interactions, and analytics across multiple touchpoints. Tools that unify cross‑platform publishing, sentiment analysis, and performance dashboards reduce fragmentation and improve operational coordination. According to industry surveys, 74% of marketing teams report increased operational efficiency when using integrated management platforms versus disparate tools. Additionally, the demand for consistency in brand messaging across global markets intensifies the need for centralized governance and compliance workflows. The growth in influencer partnerships and user‑generated content also necessitates advanced tracking and collaboration features that Social Media Management Software Market solutions provide, enabling teams to scale engagement without proportional increases in headcount.

Data privacy concerns present a significant restraint on the Social Media Management Software Market, as regulations and consumer expectations impose limitations on data usage, tracking, and cross‑platform integrations. The introduction of frameworks such as GDPR in Europe and varying national privacy standards complicates the collection and analysis of user engagement data. Enterprises must invest in compliance mechanisms, consent management modules, and data governance controls, which can slow deployment and increase total cost of ownership. A 2025 industry assessment found that 63% of IT leaders identified regulatory compliance as a top challenge when integrating third‑party social media data sources. Additionally, varying policies on API access from platform providers can disrupt analytics continuity and limit feature availability in management platforms, leading to delays in rollout schedules and constrained functionality for certain regions.

The integration of artificial intelligence and machine learning presents substantial opportunities within the Social Media Management Software Market. AI‑enabled content recommendation engines can help marketers tailor messaging based on predictive engagement insights, improving relevance and ROI. Tools incorporating ML‑based sentiment detection and trend prediction offer deeper understanding of audience preferences in real time. In 2025, platforms with built‑in AI responders demonstrated up to 41% faster customer engagement turnaround compared to conventional response workflows. There is also opportunity in enhancing automated reporting, anomaly detection, and campaign optimization without manual intervention. As enterprises seek to reduce operational workload and elevate strategic insights, these intelligent features become differentiators that can unlock new adoption segments among mid‑sized businesses and global enterprises alike, fueling demand for next‑generation Social Media Management Software Market solutions.

Integration and interoperability issues stand as critical challenges in the Social Media Management Software Market, particularly as enterprises demand seamless connectivity with existing martech stacks, analytics platforms, and CRM systems. Disparate data schemas, legacy infrastructure, and inconsistent API support from social platforms can hinder real‑time data flow, leading to delays in insight generation and fragmented customer views. In a 2025 technology benchmark study, 58% of organizations reported difficulties integrating social management tools with core analytics and customer data platforms, resulting in manual data reconciliation efforts and increased error rates. Moreover, ensuring consistent performance across global cloud regions and varying security postures adds complexity to implementation. These technical hurdles increase deployment timelines and require specialized IT skills, impacting overall adoption rates and limiting the ability of organizations to fully leverage Social Media Management Software Market capabilities.

• Surge in AI-Driven Content Optimization: Adoption of AI for content scheduling and sentiment analysis is transforming the Social Media Management Software market. In 2025, enterprises using AI-enabled platforms reported a 38% improvement in engagement rates and a 29% reduction in manual content management tasks. North America leads in deployment volume, while Asia-Pacific shows the fastest adoption, with 64% of digital marketing teams integrating AI workflows.

• Increased Cross-Platform Automation: Organizations are increasingly deploying tools that allow unified management across multiple social channels. 72% of enterprise users now rely on automated posting and reporting features, which reduce operational overhead by 33% and improve brand consistency across platforms. Europe dominates adoption in terms of enterprise penetration, whereas Latin America shows high growth in SMB usage of automation features.

• Integration with CRM and E-Commerce Systems: Social Media Management Software solutions are integrating with CRM and e-commerce platforms to enable personalized marketing campaigns. 61% of companies report improved lead conversion through synchronized customer insights and automated engagement triggers. In 2025, a major retail firm achieved a 21% uplift in cross-selling success using these integrated platforms.

• Emphasis on ESG and Sustainable Digital Practices: Companies are incorporating sustainability metrics into platform use, such as energy-efficient scheduling and server optimization. 49% of enterprises now track digital carbon footprint reductions, targeting up to 23% energy savings by 2030. North America and Europe lead in ESG-focused adoption, while Asia-Pacific is rapidly aligning with these compliance-driven features to meet regulatory requirements.

The Social Media Management Software Market is structured through multiple segmentation lenses to address diverse enterprise requirements and functional priorities. Segmentation by type highlights cloud‑based and on‑premises solutions, reflecting organizational preferences for scalability versus control, with cloud‑centric deployments dominating usage due to remote accessibility and rapid feature updates. Application segments differentiate by user needs such as campaign execution, analytics, and customer engagement, showing how varied operational priorities shape tool selection. End‑user segmentation distinguishes between large enterprises, SMEs, agencies, and individual professionals, each with distinct adoption drivers, tool sophistication expectations, and workload profiles. Geographic segmentation also reveals varied digital maturity levels and regulatory considerations. This layered segmentation framework allows vendors and decision‑makers to align offerings with specific use‑case demands, optimize feature sets, and tailor pricing models based on deployment preferences, organizational scale, and core business functions.

Cloud‑based platforms currently account for approximately 72% of Social Media Management Software deployments, driven by scalability, rapid updates, and cross‑platform accessibility that support geographically distributed teams and mobile workforces. On‑premises solutions, while more limited in deployment share, remain relevant for organizations with stringent data security policies or industry‑specific compliance requirements, such as government agencies or financial services firms. A smaller hybrid deployment model also exists, providing a middle ground for enterprises balancing control with flexibility. Within core functional types, publishing tools represent the leading segment, accounting for around 42% of adoption due to the high volume of content scheduling needs across channels, while analytics tools are gaining traction rapidly as organizations prioritize data‑led performance optimization and audience insights. For example, publishing tools manage content workflows for an average of 23 weekly posts across platforms, demonstrating their operational centrality. While cloud‑based solutions dominate broadly, web‑based tools are also used in decentralized settings where minimal installation barriers are important for fast onboarding and interdepartmental access. Combined, niche on‑premises and hybrid models contribute the remaining share of deployments, catering to specific security and integration requirements.

Within application segmentation, marketing and campaign management applications are the leading area, accounting for approximately 56% of Social Media Management Software usage as organizations align tools with broader promotional strategies and audience reach initiatives. Analytics and reporting applications are also a significant focus, supporting data‑informed decisions and KPI tracking such as engagement metrics and content performance. Customer service applications are emerging quickly, enabled by shifting consumer expectations for rapid social‑channel responses; nearly half of customer service interactions now occur via social platforms, increasing demand for dedicated management workflows. Sales support applications leverage social data to inform lead generation and conversion activities, driving closer alignment between social engagement and revenue activities. For example, advanced analytics tools have helped some brands achieve 25% higher marketing ROI compared to basic social metrics. Other applications such as social listening and influencer engagement contribute to the remaining segment share, providing niche yet impactful capabilities for reputation monitoring and partner collaborations.

Large enterprises are the leading end users of Social Media Management Software, representing around 68% of the market due to their complex multi‑brand campaigns, compliance demands, and integrated digital ecosystems that require robust platforms. Enterprise adoption frequently involves centralized analytics, automated workflows, and CRM integration to manage extensive social accounts and audience segments. Small and medium‑sized enterprises (SMEs) are the next significant user group, with growing adoption driven by affordability, simplified interfaces, and the need to maintain consistent online presence despite limited resources; roughly 74% of small businesses leverage social media tools for marketing and engagement. Agencies and individual professionals also contribute to the landscape, providing specialized services such as multi‑client account management, content calendars, and performance analytics across various client portfolios. For instance, tools like Hootsuite support millions of users globally across companies of all sizes, enabling social teams to coordinate campaigns and respond to customer engagement in real time. Combined, SMEs, agencies, and individual users account for the remaining share of Social Media Management Software deployments, reflecting the broad utility of these platforms across organizational scales.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.5% between 2026 and 2033.

North America led with over 220,000 enterprise deployments of Social Media Management Software in 2025, while Asia-Pacific recorded more than 150,000 implementations, reflecting rapid digital adoption. Europe followed with a 28% regional share, including key markets like Germany, the UK, and France. South America and Middle East & Africa collectively contributed 18% of total global deployments. Mobile and cloud-based adoption in Asia-Pacific reached 68% among SMEs, while North American enterprises reported 74% platform integration with CRM and analytics tools. User engagement metrics in the U.S. show average campaign response rates of 41%, compared to 33% in Europe, highlighting regional variations in adoption and performance. By 2033, emerging economies in Asia-Pacific are projected to add over 120,000 new enterprise deployments, driven by e-commerce expansion and AI-driven content automation.

How are enterprises optimizing digital engagement through advanced management platforms?

North America commands approximately 41% of the Social Media Management Software market, driven by large-scale adoption in healthcare, finance, and retail sectors. Government regulations around data privacy and digital communications have prompted enterprises to invest in secure, compliant platforms. Technological advancements such as AI-driven sentiment analysis, automated content scheduling, and integrated analytics are accelerating deployment, with cloud-based solutions dominating 72% of regional usage. Local players, including Sprout Social, are enhancing platforms with predictive engagement features and multi-channel dashboards, supporting over 120,000 enterprise accounts. Consumer behavior trends show higher enterprise adoption in North America, especially in healthcare and finance, where real-time insights and campaign orchestration are critical for customer retention and regulatory compliance.

What drives compliance-focused adoption of social engagement solutions across major European markets?

Europe holds approximately 28% of the Social Media Management Software market, with Germany, the UK, and France as key contributors. Regulatory pressure, including GDPR, drives demand for explainable and secure social management platforms. Adoption of emerging technologies such as AI-powered analytics and automated campaign scheduling is increasing across enterprises and agencies. Companies like Hootsuite have established localized operations to provide multilingual support and compliance-focused workflows. Regional consumer behavior reflects cautious engagement, with firms prioritizing data security, traceable user interactions, and transparent analytics reporting. In 2025, approximately 65% of European marketing teams integrated AI-based content performance monitoring tools to comply with local regulations and optimize multi-channel campaigns.

How is rapid digital transformation shaping enterprise adoption in high-growth economies?

Asia-Pacific accounts for roughly 26% of the global Social Media Management Software market by volume, with China, India, and Japan as top-consuming countries. Growth is driven by e-commerce expansion, mobile-first digital campaigns, and AI-powered content automation. Key technology hubs in Singapore, Bangalore, and Shanghai are leading adoption of predictive analytics and integrated multi-platform dashboards. Regional players, including Zoho Social, are enhancing features such as localized language support and automated posting for SMEs. Consumer behavior in Asia-Pacific shows high engagement on mobile channels, with over 68% of SMEs leveraging cloud-based platforms to manage social campaigns efficiently and increase brand visibility.

What role does localized engagement and digital infrastructure play in market growth?

South America holds approximately 10% of the Social Media Management Software market, with Brazil and Argentina leading adoption. Growth is supported by investments in digital infrastructure and expanding broadband connectivity. Government initiatives promoting e-commerce and digital services have increased platform penetration. Local players, including Resultados Digital, focus on language-specific automation and campaign analytics to serve regional businesses. Consumer behavior in South America emphasizes media and language localization, with 57% of companies prioritizing content in native languages to boost engagement and social responsiveness.

How are regional industries leveraging social platforms for operational and marketing efficiency?

The Middle East & Africa contribute approximately 8% of the Social Media Management Software market, with UAE and South Africa leading in enterprise adoption. Demand is driven by oil & gas, construction, and fintech sectors investing in digital marketing solutions. Technological modernization, including AI-powered scheduling, automated reporting, and cloud integration, is accelerating adoption. Regional regulations and trade partnerships encourage compliance-focused deployments. Local firms, such as The Social Media Co., are providing enterprise solutions with multilingual support and tailored dashboards. Consumer behavior in the region favors centralized digital campaigns, with enterprises prioritizing performance metrics and real-time analytics to drive operational and marketing efficiency.

United States: 41% market share; dominance due to advanced digital infrastructure, strong enterprise demand, and early adoption of AI-driven management platforms.

Germany: 12% market share; leading due to stringent data privacy regulations, high SME adoption rates, and integration of automated analytics for multi-channel campaigns.

The Social Media Management Software market is highly competitive and moderately fragmented, with over 150 active global competitors offering diverse solutions across cloud-based, on-premises, and hybrid deployment models. The top five companies collectively hold approximately 48% of total market share, indicating both significant concentration among leading players and substantial room for emerging firms. Market leaders are leveraging strategic initiatives such as AI-powered platform enhancements, partnerships with CRM and analytics vendors, and targeted acquisitions to expand geographic reach and functionality. In 2025 alone, more than 35 major product launches were reported globally, introducing features like predictive content optimization, automated cross-platform scheduling, and real-time sentiment analytics. Innovation trends such as generative AI content tools, integrated influencer management, and workflow automation are reshaping competition dynamics. Enterprises increasingly prioritize platforms with high scalability, robust security, and analytics-driven insights, intensifying rivalry. North American and European firms dominate in R&D investment, while Asia-Pacific competitors are rapidly scaling operations to capitalize on growing SME adoption. Overall, the competitive landscape emphasizes continuous technological advancement, strategic partnerships, and multi-channel integration capabilities as key differentiators for market leadership.

Buffer

Zoho Social

Falcon.io

Agorapulse

Socialbakers

Sendible

Social Studio

Khoros

The Social Media Management Software market is increasingly defined by the integration of advanced and emerging technologies that enhance operational efficiency, engagement tracking, and analytics capabilities. Cloud-based platforms dominate 72% of deployments, offering real-time multi-channel management and seamless integration with enterprise CRM and e-commerce systems. AI-powered content optimization tools are now used by over 65% of large enterprises, delivering measurable improvements in engagement rates—up to 38% higher compared to traditional scheduling methods—and reducing manual content management efforts by 29%. Natural language processing (NLP) and sentiment analysis technologies are rapidly being incorporated, enabling firms to track and respond to audience sentiment in real time across more than 10 social channels simultaneously.

Automation technologies, including intelligent scheduling, workflow orchestration, and auto-reporting, are widely adopted, with 74% of enterprises reporting reduced operational overhead and faster response times. Generative AI is emerging as a transformative force, supporting dynamic content creation, predictive posting, and personalized messaging that enhances customer engagement and retention. Additionally, integration with influencer marketing and social listening platforms is allowing firms to analyze 12–15 million data points daily for trend detection and competitive benchmarking. Mobile-first technology adoption is particularly high in Asia-Pacific, with 68% of SMEs leveraging smartphones and tablets for campaign execution and monitoring. The market is also seeing a focus on ESG-compliant digital operations, including server energy optimization and reduced digital carbon footprints. Collectively, these technologies position Social Media Management Software as a strategic tool for scalable, data-driven, and sustainable social media management across industries.

• In July 2025, Sprout Social acquired NewsWhip, a Dublin‑based AI‑powered predictive media intelligence firm to enhance predictive insights in social landscape monitoring and strengthen brands’ ability to detect emerging trends and respond with agility.

• In February 2025, Sprout Social launched its rebranded Influencer Marketing Platform, equipping brands with advanced analytics and AI‑powered tools to identify and engage the right influencers, streamline campaign workflows, and scale influencer partnerships with measurable efficiency. (Sprout Social)

• In May 2025, Sprout Social unveiled new innovations in its Care solution, adding additional bot channels, customizable workflows, enhanced compliance and governance features, and impending AI agent integration to accelerate proactive customer care on social platforms.

• In August 2025, Sprout Social announced a suite of integrations with major platforms including TikTok, LinkedIn, Meta, and Salesforce to support sentiment capture, streamline publishing, and enhance reporting capabilities, enabling real‑time, data‑driven engagement strategies.

The Social Media Management Software Market Report comprehensively covers vendor offerings, deployment types, functional technologies, application areas, and regional landscapes that define the ecosystem of social engagement solutions. The report includes segmentation across cloud‑based, on‑premises, and hybrid models, highlighting deployment preferences among enterprises and SMEs, with cloud deployments representing a substantial portion of global implementations due to scalability and rapid feature delivery. Functional segments encompass publishing and scheduling tools, analytics and reporting modules, sentiment and social listening engines, influencer engagement features, and customer care integration capabilities that support cross‑channel orchestration.

Applications reviewed include campaign management and optimization, real‑time performance analytics, CRM integrations, customer service automation, and sales support workflows that leverage social data for lead gen and conversion activities. Technology focus areas dissect current and emerging innovations—such as AI‑driven content optimization, NLP‑based sentiment tracking, automated workflow orchestration, and generative AI support for content creation—demonstrating how tools influence marketing operations and engagement outcomes across industries.

The geographic scope spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, analyzing regional adoption trends, regulatory influences, infrastructure readiness, and digital maturity. Industry focus includes enterprise and agency usage scenarios, differentiated by verticals such as healthcare, finance, retail, and media, providing decision‑makers with end‑user adoption profiles, capability requirements, and competitive benchmarks. The report also identifies niche and emerging segments like influencer marketing platforms, integrated social commerce solutions, and social intelligence analytics, reflecting the evolving breadth of the market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hootsuite, Sprout Social, Buffer, Zoho Social, Falcon.io, Agorapulse, Socialbakers, Sendible, Social Studio, Khoros |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |