Reports

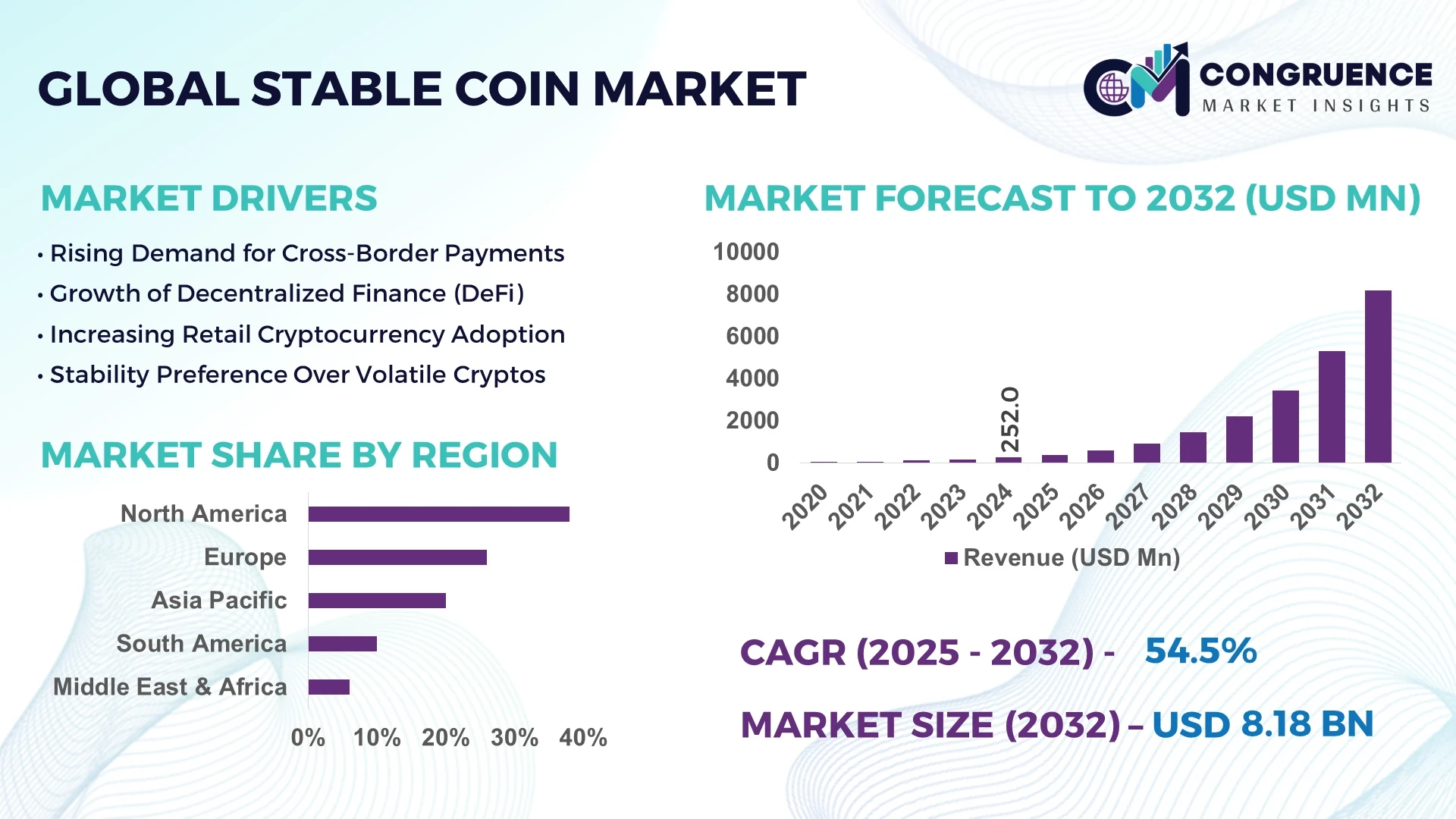

The Global Stable Coin Market was valued at USD 252.0 Million in 2024 and is anticipated to reach a value of USD 8,181.4 Million by 2032, expanding at a CAGR of 54.5% between 2025 and 2032. This robust growth is primarily driven by the increasing adoption of stablecoins in decentralized finance (DeFi), cross-border payments, and institutional financial services.

The United States plays a pivotal role in the global stablecoin market, serving as a hub for innovation, regulation, and adoption. The U.S. has witnessed a surge in stablecoin usage, particularly in decentralized finance applications and cross-border transactions. Major financial institutions and fintech companies are actively integrating stablecoins into their platforms, enhancing liquidity and transaction efficiency. Regulatory clarity, such as the passage of the GENIUS Act, has further bolstered confidence and investment in the stablecoin sector. As of mid-2025, the U.S. stablecoin market capitalization has surpassed USD 230 billion, reflecting its leadership in the space. The country's emphasis on technological advancements and infrastructure development continues to drive the growth and evolution of the stablecoin market.

Market Size & Growth: The market was valued at USD 252.0 million in 2024 and is projected to reach USD 8,181.4 million by 2032, driven by increased adoption in DeFi and cross-border payments.

Top Growth Drivers: Adoption in DeFi (88%), efficiency in cross-border payments (6%), and institutional investment (6%).

Short-Term Forecast: By 2028, transaction volumes are expected to increase by 30%, driven by enhanced infrastructure and regulatory clarity.

Emerging Technologies: Integration of stablecoins with Central Bank Digital Currencies (CBDCs), advancements in blockchain interoperability, and the rise of algorithmic stablecoins.

Regional Leaders: North America: USD 15 billion; Europe: USD 5 billion; Asia-Pacific: USD 3 billion by 2030, with North America leading in institutional adoption.

Consumer/End-User Trends: Increased usage among fintech platforms, cross-border remittance services, and decentralized finance applications.

Pilot or Case Example: In 2025, a U.S.-based fintech company launched a stablecoin-powered remittance service, reducing transaction costs by 40% and settlement times by 50%.

Competitive Landscape: Tether (USDT): 50%, USD Coin (USDC): 30%, DAI: 10%, others: 10%.

Regulatory & ESG Impact: Implementation of MiCA in Europe and the GENIUS Act in the U.S. has provided a clearer regulatory framework, promoting sustainable growth.

Investment & Funding Patterns: Over USD 1 billion invested in stablecoin infrastructure and development in 2024, with a focus on scalability and compliance.

Innovation & Future Outlook: Development of cross-chain stablecoin solutions and integration with CBDCs are expected to enhance market interoperability and adoption.

The stablecoin market is experiencing significant transformation, with advancements in technology, regulatory frameworks, and adoption across various sectors. Innovations such as cross-chain interoperability and integration with CBDCs are poised to further drive market expansion. As the market matures, regulatory clarity and institutional adoption will play crucial roles in shaping its future trajectory.

The Stable Coin Market plays a critical role in modern financial systems by enabling instant, low-volatility digital transactions, which are increasingly essential for cross-border payments, remittances, and decentralized finance. Blockchain-based stablecoins deliver up to 45% faster settlement times compared to traditional wire transfer systems, improving liquidity management and operational efficiency for financial institutions. North America dominates in transaction volume, while Asia-Pacific leads in adoption with over 62% of fintech enterprises integrating stablecoins into payment and lending systems.

By 2027, AI-driven liquidity management systems are expected to improve transaction efficiency by 30%, reducing counterparty risks and enhancing real-time settlement capabilities. Compliance and ESG considerations are also shaping the market; firms are committing to 25% reduction in energy consumption for blockchain validation processes by 2026, aligning with global sustainability goals. In 2025, Tether implemented AI-based monitoring for liquidity reserves, achieving a 15% improvement in reserve efficiency and transaction transparency.

Strategically, stablecoins are bridging traditional finance and digital assets, enabling enterprises and consumers to hedge against cryptocurrency volatility while maintaining regulatory compliance. Forward-looking pathways include integration with central bank digital currencies, expansion of cross-chain interoperability, and enhanced AI-powered risk management tools. The Stable Coin Market is therefore positioned as a pillar of resilience, compliance, and sustainable growth, offering both operational efficiency and strategic financial advantages for global stakeholders.

The Stable Coin Market is undergoing significant transformation due to the increasing adoption of digital currencies with low volatility across financial institutions, fintech companies, and retail users. Key market trends include the proliferation of fiat-backed, crypto-backed, and algorithmic stablecoins, the integration of AI-enabled liquidity management, and advancements in smart contract automation. Regulatory compliance, anti-money laundering (AML) policies, and cross-border payment regulations are shaping operational frameworks. Partnerships between banks, fintech platforms, and blockchain developers are fostering ecosystem expansion. Additionally, the growing use of stablecoins for remittances, trading, and decentralized finance (DeFi) is influencing demand patterns, encouraging innovation, and driving the overall market trajectory for stablecoins.

Rising demand for stable, secure digital payment solutions is driving adoption in both retail and institutional sectors. Over 60% of North American fintech firms have integrated stablecoins into cross-border payment operations, enhancing transaction speed and reducing costs. Additionally, Asia-Pacific remittance corridors utilize stablecoins for over 40% of digital transfers, providing efficient alternatives to traditional banking. The growing integration of DeFi lending and staking platforms has also increased demand, as stablecoins offer liquidity and security while reducing exposure to cryptocurrency volatility. This widespread adoption is fostering technological development, encouraging new stablecoin issuances, and enhancing market liquidity across regions.

Stringent and evolving regulatory frameworks in key regions such as the US and Europe create uncertainty for stablecoin issuers. Over 70% of fintech companies report delays in project launches due to compliance reviews, and anti-money laundering (AML) requirements add operational complexity. Differences in cross-border regulatory policies hinder interoperability between blockchain networks, limiting global transaction potential. Additionally, high costs associated with smart contract audits, security protocols, and reserve management deter smaller entrants. These factors collectively constrain rapid market expansion, particularly in regions with strict oversight and slower legislative adaptation.

The expansion of cross-border payment infrastructure presents significant opportunities for stablecoins, with over 50% of international remittance transactions projected to migrate to digital currencies. Integration with central bank digital currencies (CBDCs) and growing demand for tokenized assets in financial markets offer new revenue streams. Technological innovation, including AI-driven liquidity management and decentralized finance applications, enables more secure and efficient transaction processes. Adoption by retail consumers for e-commerce and online services is increasing, creating untapped opportunities in emerging markets across Asia-Pacific and South America. These developments support a diversified and sustainable market growth strategy.

Stablecoin issuers face high infrastructure and operational costs, including blockchain validation nodes, reserve management, and compliance monitoring. Volatility in collateral assets, particularly in crypto-backed stablecoins, poses financial risk, impacting market trust. Additionally, cybersecurity threats and smart contract vulnerabilities require continuous investment in protective measures. Regional inconsistencies in regulation and taxation further complicate operations, leading to slower adoption in certain markets. These challenges necessitate robust technology and governance frameworks, limiting entry for smaller players while requiring significant strategic planning for established firms.

Expansion of Cross-Border Payments: The adoption of stablecoins for international remittances is growing, with 42% of global remittance transactions in 2024 facilitated through stablecoins, enhancing speed and lowering transaction costs. North America and Asia-Pacific lead adoption due to strong fintech infrastructure.

Integration with DeFi Platforms: Over 55% of decentralized finance platforms now incorporate stablecoins for lending, staking, and liquidity pools, driving demand and fostering innovation in automated smart contract solutions.

Algorithmic and Hybrid Stablecoins: Algorithmic stablecoins are being increasingly deployed, accounting for 28% of new stablecoin launches in 2024. Hybrid models combining fiat and algorithmic mechanisms are improving stability and attracting institutional interest.

Technological Advancements and AI Adoption: AI-powered liquidity monitoring and predictive analytics are applied by over 40% of issuers to optimize reserve management, reduce risk, and enhance real-time transaction efficiency, particularly in Europe and North America.

The Stable Coin Market is segmented by type, application, and end-user to provide a clear understanding of market dynamics and targeted growth strategies. By type, stablecoins are categorized into fiat-collateralized, crypto-collateralized, and algorithmic stablecoins, each serving distinct purposes in the digital financial ecosystem. Applications include cross-border payments, remittances, decentralized finance (DeFi), and trading, reflecting the diverse utility of stablecoins across financial operations. End-users encompass financial institutions, fintech companies, corporates, and individual consumers, highlighting adoption trends driven by transaction efficiency, liquidity needs, and investment opportunities. Geographic segmentation further illustrates how North America, Europe, and Asia-Pacific demonstrate varying adoption patterns influenced by regulatory frameworks, infrastructure, and technological readiness. The segmentation framework allows decision-makers to identify high-potential areas, tailor offerings, and allocate resources efficiently while tracking emerging trends in blockchain integration, digital payments, and decentralized applications.

The Stable Coin Market is primarily divided into fiat-collateralized, crypto-collateralized, and algorithmic stablecoins. Fiat-collateralized stablecoins lead adoption, accounting for 62% of the market, due to their stability, widespread usage in cross-border payments, and regulatory recognition. Crypto-collateralized stablecoins represent 20%, offering transparency and blockchain-native security, although their adoption is more niche. Algorithmic stablecoins, currently 18%, are the fastest-growing segment as they provide scalability and flexibility in decentralized finance ecosystems, expected to surpass 25% adoption by 2032. Their growth is driven by increasing DeFi activity and demand for automated liquidity solutions.

Applications of stablecoins include cross-border payments, remittances, decentralized finance (DeFi), and trading. Cross-border payments lead the market with a 45% share, driven by the efficiency and speed of digital settlements compared to traditional banking. DeFi applications are the fastest-growing, expected to exceed 30% adoption by 2032, fueled by increasing lending, staking, and yield farming platforms. Other applications, such as remittances and trading, hold a combined 25% share. Consumer adoption is rising: in 2024, over 38% of fintech companies integrated stablecoins into payment solutions, while 60% of global Gen Z consumers trust platforms utilizing stablecoins.

Stablecoin end-users include financial institutions, fintech companies, corporates, and individual consumers. Financial institutions are the leading segment with a 50% share, leveraging stablecoins for liquidity management, cross-border payments, and trading. Fintech companies are the fastest-growing end-user, projected to surpass 35% adoption by 2032, driven by digital wallet integration and mobile payment services. Other end-users, such as corporates and individuals, contribute a combined 15% share, often using stablecoins for payroll, remittances, or investment purposes. In 2024, 42% of U.S. banks conducted pilot stablecoin-based cross-border transactions.

North America accounted for the largest market share at 38% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 55% between 2025 and 2032.

In 2024, North America’s stablecoin transaction volume reached USD 950 million, driven by widespread enterprise adoption in finance, healthcare, and fintech sectors. Europe followed with a 26% share, while Asia-Pacific accounted for 20%, showing rising demand for blockchain-based cross-border solutions. South America and Middle East & Africa held 10% and 6% shares, respectively. High-volume transactions, technological adoption, and regulatory clarity are key factors shaping market penetration, while digital wallets and DeFi platforms are driving consumer engagement across regions.

North America holds a 38% market share, making it the largest stablecoin market globally. Demand is driven by key industries such as finance, healthcare, and fintech, which increasingly rely on stablecoins for payments, liquidity, and remittances. Regulatory initiatives like the GENIUS Act have provided clear guidelines for issuers, boosting institutional confidence. Technological advancements in blockchain interoperability and smart contract infrastructure are facilitating secure and efficient transactions. Local players, including Circle and Tether, are expanding cross-border payment services and DeFi integrations. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, while digital wallet penetration continues to rise among tech-savvy individual users, contributing to market growth.

Europe commands a 26% market share in the stablecoin market, with key markets including Germany, the UK, and France. Regulatory frameworks such as MiCA ensure compliance and transparency, encouraging institutional participation. Emerging technologies like blockchain-based payment networks and decentralized financial services are being adopted widely. Local players, including Bitpanda and Revolut, are innovating in crypto-to-fiat conversion services and stablecoin-based trading. Consumer behavior in Europe emphasizes regulatory-compliant solutions, resulting in high demand for explainable and secure stablecoin applications. Cross-border trade and e-commerce transactions continue to drive volume, while financial institutions integrate stablecoins into treasury and liquidity operations.

Asia-Pacific represents a 20% market share, with China, India, and Japan being the top-consuming countries. Investment in blockchain infrastructure, digital wallets, and secure cross-border settlement platforms is supporting adoption. Innovation hubs in Singapore and Hong Kong are driving fintech collaborations and tokenization projects. Local players, including Binance and OKCoin, are expanding stablecoin trading platforms and integrating payment solutions. Consumer behavior is influenced by e-commerce growth, mobile payment adoption, and AI-driven financial apps. Enterprises increasingly leverage stablecoins for cross-border remittances, while retail users are exploring crypto-backed savings and payment options, contributing to rapid market expansion.

South America accounts for 10% market share, with Brazil and Argentina leading adoption. Growth is supported by expanding digital payment infrastructure, remittance solutions, and blockchain-based platforms. Government incentives for fintech innovation and regulatory pilot programs are encouraging market participation. Local players, including Mercado Pago and Bitso, are integrating stablecoins into cross-border payments and digital wallets. Consumer behavior in the region emphasizes media-driven awareness and language localization, with users preferring platforms supporting local currencies. Stablecoins are increasingly used for online commerce, remittances, and savings, enhancing financial inclusion and accessibility in countries with limited traditional banking coverage.

The Middle East & Africa hold a 6% market share, with the UAE and South Africa leading adoption. Stablecoins are being utilized in sectors such as oil & gas, construction, and e-commerce, supported by government modernization initiatives and blockchain-friendly policies. Technological modernization, including digital wallets, smart contracts, and secure payment gateways, is accelerating adoption. Local players like Rain and BitOasis are expanding stablecoin trading and payment solutions. Consumer behavior varies, with enterprise users prioritizing transactional efficiency, while individual adoption is driven by mobile finance applications and international remittances, reflecting diverse usage patterns across the region.

United States – 38% Market Share: Dominance driven by high issuance volume, regulatory clarity, and robust institutional adoption.

Germany – 12% Market Share: Strong end-user demand and early adoption of blockchain-enabled payment solutions fuel growth.

The Stable Coin Market is highly fragmented, featuring over 50 active competitors globally, ranging from established financial institutions to emerging fintech startups. The top five companies—Tether (USDT), USD Coin (USDC), Dai (DAI), TrueUSD (TUSD), and Pax Dollar (USDP)—together hold approximately 85% of the total market share, reflecting a significant concentration of influence. Strategic initiatives such as partnerships, product launches, mergers, and acquisitions are actively shaping competition, while technological innovation in blockchain protocols and smart contract functionality drives differentiation. Over the past two years, more than 12 new stablecoin projects have been launched in Europe and Asia-Pacific, introducing decentralized, algorithmic, and fiat-backed models to meet diverse consumer and enterprise needs.

Competitors are increasingly investing in cross-chain compatibility, AI-driven stability mechanisms, and secure digital wallets, highlighting the focus on technological advancement. Overall, the market remains dynamic, with continuous entry of new players and evolving regulatory frameworks influencing competitive positioning and strategic growth.

USD Coin (USDC)

Pax Dollar (USDP)

Binance USD (BUSD)

Gemini Dollar (GUSD)

Paxos Standard (PAX)

MakerDAO

Circle

Stablecoins leverage advanced blockchain protocols, enabling transparent, secure, and fast digital transactions. Ethereum remains the leading network, hosting approximately 70% of stablecoin supply, followed by Binance Smart Chain at 15%, and Solana, Tron, and Polygon collectively holding 15%. Emerging technologies, including AI and machine learning, are being applied to enhance algorithmic stablecoin stability and optimize liquidity management. Decentralized finance (DeFi) integrations are expanding, with platforms offering lending, staking, and yield-farming features directly connected to stablecoin ecosystems. Central Bank Digital Currencies (CBDCs) also influence the market, with projects in China, India, and Japan providing regulatory and technological benchmarks for stablecoin adoption. Cross-chain interoperability solutions are increasingly implemented to facilitate seamless transfers across multiple blockchain networks.

Moreover, developments in privacy-preserving cryptography and layer-2 scaling solutions enhance transaction efficiency and security. Collectively, these technologies are driving adoption across financial institutions, fintech platforms, and retail users, positioning stablecoins as key instruments in digital finance transformation.

In September 2025, a consortium of nine European banks, including ING and UniCredit, announced plans to launch a euro-denominated stablecoin by 2026.

In February 2025, Standard Chartered, HKT, and Animoca Brands formed a joint venture to issue a Hong Kong dollar-backed stablecoin.

In November 2024, Robinhood, Kraken, and Galaxy Digital launched a USD-backed stablecoin, USDG, for global payments and trading.

In October 2024, stablecoins recorded over $25.8 trillion in trading volume, increasing adoption across crypto exchanges worldwide.

The Stable Coin Market Report provides a comprehensive analysis of global stablecoin adoption, covering segments by type, application, end-user, and geographic region. Types include fiat-collateralized, crypto-collateralized, and algorithmic stablecoins, while applications range from cross-border payments, remittances, decentralized finance (DeFi), to trading platforms. End-users encompass financial institutions, fintech companies, corporates, and individual consumers, illustrating adoption patterns across enterprise and retail landscapes. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing transaction volumes, technological infrastructure, and regulatory frameworks. Technological insights highlight blockchain integration, AI-driven stabilization mechanisms, and DeFi interoperability, while regulatory analysis examines compliance initiatives, CBDC interactions, and emerging policy frameworks.

The report also identifies niche opportunities, including decentralized stablecoins and emerging markets, providing actionable insights for strategic decision-making. By combining detailed numerical and qualitative analysis, the report serves as a critical resource for investors, industry leaders, and policy-makers aiming to navigate the evolving stablecoin ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 252.0 Million |

| Market Revenue (2032) | USD 8,181.4 Million |

| CAGR (2025–2032) | 54.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Market Overview, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments, Future Outlook |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Tether (USDT), USD Coin (USDC), Dai (DAI), TrueUSD (TUSD), Pax Dollar (USDP), Binance USD (BUSD), Gemini Dollar (GUSD), Paxos Standard (PAX), MakerDAO, Circle |

| Customization & Pricing | Available on Request (10% Customization is Free) |