Reports

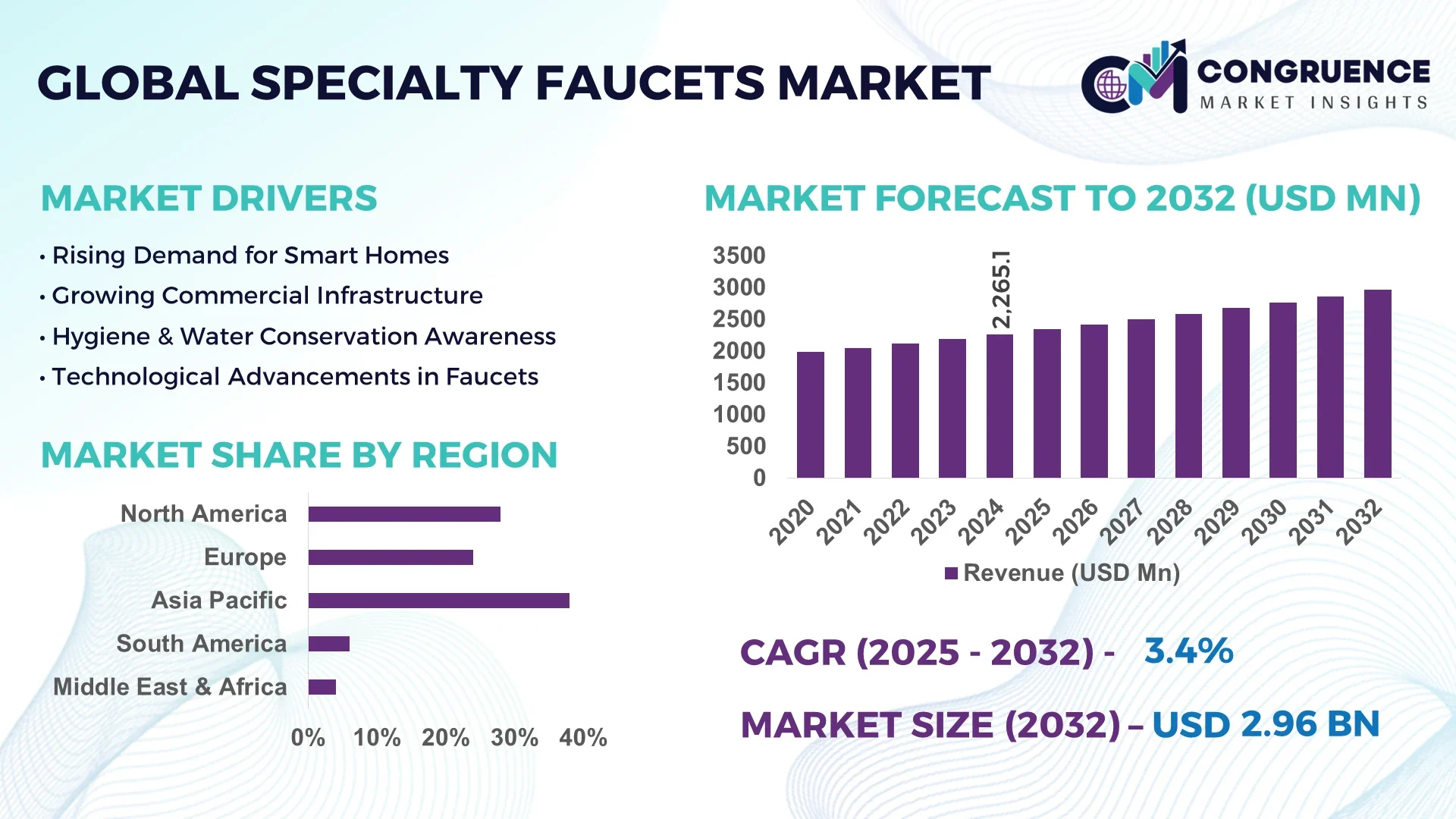

The Global Specialty Faucets Market was valued at USD 2,265.1 Million in 2024 and is anticipated to reach a value of USD 2,959.7 Million by 2032 expanding at a CAGR of 3.4% between 2025 and 2032.

In China, which dominates the Specialty Faucets Market, manufacturers have invested heavily in advanced production capacity, including precision casting facilities and smart-factory automation lines capable of output exceeding several million specialty faucet units per year. The country has allocated substantial capital toward R&D in sensor-based and smart faucets, integrating technologies like infrared motion detection and touchless control systems. Large firms have also collaborated with universities and institutes to pioneer antimicrobial coatings, ceramic disc mechanisms, and voice-activated interfaces. Major infrastructure projects in China regularly demand specialty faucets with enhanced durability, corrosion resistance, and water-efficient features, prompting manufacturers to scale up both domestic supply chains and export-oriented capacity.

The Specialty Faucets Market today is shaped by several key sectors, technological innovations, regulatory influences, and regional growth patterns. In terms of application, residential remodeling and premium home construction contribute significantly, especially in bathroom and kitchen fixtures where aesthetic design, finish, and feature integration (e.g. touchless, adjustable spray, filtration) are valued. Commercial sectors (hotels, hospitals, office buildings) also represent important demand centers, especially for hygienic, easy-to-maintain specialty faucets. On the technology front, innovations include sensor and automatic activation, voice control, advanced materials (e.g. ceramic disc valves, PVD finishes, antimicrobial surfaces), as well as IoT connectivity enabling predictive maintenance, flow-monitoring, and user behavior analytics. Regulatory and environmental drivers are becoming more influential: water-efficiency standards, lead-free materials, certifications like NSF, ISO, CE, and local environmental codes are pushing manufacturers to meet stricter performance and safety criteria. Regionally, growth is strong in Asia Pacific (China, India, Southeast Asia), driven by rising incomes, urbanization, and housing investment, while mature markets in North America and Europe emphasize smart features, sustainability, and premium finishes. Emerging trends include mass customization of finishes and features, modular faucet design for easy installation/repair, and integrations with smart home ecosystems. The future outlook points to increasing integration of digital controls, touchless interfaces, and sustainability-oriented features, with demand rising in both new construction and renovation as buyers demand higher hygiene, convenience, and environmental responsibility.

Artificial intelligence is making inroads throughout the Specialty Faucets Market by enabling smarter, more efficient, and adaptive product behavior, as well as optimizing operations for manufacturers and users alike. For manufacturers, AI-based process control systems are improving precision in processes like valve machining, finishing, and leak-testing. For example, computer vision powered by deep learning helps inspect components for micro-defects, leading to lower reject rates and improved yield. In product design and user interaction, AI is enabling faucets to learn usage patterns—such as how often, when, and how long water flows—and adjust behaviors accordingly (e.g. to minimize wastage or to deliver preset temperature or spray patterns under varying pressure conditions). Within facilities (commercial spaces, hospitals, hotels), AI-enabled specialty faucets with sensors and connected systems can detect anomalies (leaks, pressure fluctuations) and trigger alerts, reducing maintenance costs and downtime. Operational performance in water usage is improved via AI algorithms that modulate flow in response to real-time feedback, such as usage frequency or environmental conditions (temperature, demand). Generative design tools, combined with AI simulation, are helping faucet manufacturers to refine body shapes, material thicknesses, and flow path designs to reduce material usage while maintaining strength and functionality. Altogether, the Specialty Faucets Market is being transformed not only in terms of the product features but also in manufacturing efficiency, product reliability, reduced waste, and enhanced user experiences.

“In 2024, a leading faucet brand unveiled a new voice-activated smart faucet model that uses embedded AI to adjust water flow temperature within ±1 °C based on prior user preferences and automatically shuts off flow after detecting no hand motion for more than 20 seconds—this innovation reportedly reduced water usage by 18% in test installations.”

The Specialty Faucets Market Dynamics section outlines the underlying forces, trends, and influences shaping developments across innovation, regulation, competition, and consumption in the Specialty Faucets Market. Decision-makers in manufacturing, distribution, and product development can monitor shifts in materials, technology adoption, regulatory standards, and consumer preferences to anticipate changes. Key influences include the evolving expectations for hygiene and water efficiency, increasing importance of design aesthetics (finish, form, touch), cost pressures in raw materials, and growing demand for smart and touchless functionalities. Geographically, the interplay of mature markets (which value premium feature sets) and rapidly growing emerging economies (which emphasize affordability and durability) is impacting supply chain, manufacturing localization, and strategic investment. Regulatory bodies are imposing stricter standards for lead content, water flow rates, and energy efficiency, which forces companies to invest in development and certification. Environmental concerns—such as water scarcity, sustainability, and waste reduction—are also influencing product design and corporate strategy. Competitive pressures are intensifying as smaller players innovate and large incumbents scale up smart and sensor-based offerings.

The push for hygiene-centric and touchless faucet technologies has directly impacted the Specialty Faucets Market. In healthcare, food service, and public restrooms, touchless interfaces and sensor-based faucets have become preferred because they reduce contact points and risk of pathogen spread. In 2024, a number of large commercial projects—including hospitals and international hotels—specified automatic or touchless specialty faucets, sometimes paying a premium of 15-30% above standard manual faucets, reflecting the functional value in these settings. Manufacturers report that sensor modules, motion detectors, and infrared activation hardware have become standard offerings in new specialty faucet product lines. This driver is accelerating R&D investment into sensor durability and battery-free (or low-maintenance power) designs, and supporting integration with building management systems for centralized control of water fixtures.

Meeting regulatory, environmental, and safety standards presents a restraint for the Specialty Faucets Market. Factories producing specialty faucets must comply with numerous certification regimes (e.g. NSF, ISO, CE, lead-free alloys, water-efficiency, anti-microbial finish standards) which require rigorous testing and audits. These certification processes often take several months and necessitate expensive lab facilities or contracted third-party verification. Additionally, integrating advanced features (sensors, AI, special finishes) increases material and component costs; in many regions, import tariffs and local regulations add further burdens. For smaller manufacturers, these costs can erode margins – the added cost of compliance (materials, testing, documentation) can amount to 5-10% of production cost or more depending on the market. Also, supply chain disruptions in specialized components (sensor chips, special alloys, finishes) further complicate consistent compliance and timely delivery.

An important opportunity lies in replacing or upgrading existing faucet installations in older buildings, commercial establishments, and public infrastructure. Many legacy faucets lack touchless activation, antimicrobial surfaces, or smart flow control, and retrofitting is a growing demand. Urban public buildings, transport terminals, and educational institutions are starting to adopt retrofit programs to improve hygiene and reduce water wastage. In 2024, some retrofit contracts in North America and Europe showed projected cost savings of up to 25% in water usage through replacing conventional faucets with touchless specialty faucets. Also, surge in subsidy programs for water efficiency and sustainability in various jurisdictions is incentivizing retrofits of plumbing fixtures. This opportunity allows manufacturers to broaden product lines geared toward retrofit ease, modular upgrades, and aftermarket support.

Securing reliable sources for sensor modules, infrared/optical detection systems, antimicrobial coatings, and high-precision valve mechanisms is a significant challenge. Lead times for some sensor chips can extend to 16-20 weeks, especially when semiconductors are in high demand elsewhere (e.g. in consumer electronics). Specialized finishes such as PVD coatings or anti-microbial surfaces often require clean-room conditions and strict process control which many smaller manufacturing plants lack. Additionally, volatility in raw material prices (brass, stainless steel, rare alloys, electronic components) adds cost uncertainty. Manufacturers aiming to scale up specialty faucet production must invest in quality control, supplier development, and sometimes in-house component fabrication to mitigate these challenges.

Increased adoption of smart and sensor-based faucets in public and commercial infrastructure: There has been a measurable surge in specification of sensor-based specialty faucets in healthcare facilities and hotels in Europe and North America throughout 2024, with some new hospital projects specifying that 80-90% of washbasin fixtures be touchless or sensor-activated. This shift reflects heightened hygiene and maintenance efficiency priorities.

Growing preference for premium finishes and materials: Consumers are selecting finishes such as matte black, brushed gold, and PVD coatings paired with ceramic or composite materials—orders with premium finishes now account for nearly 30-35% of specialty faucet purchases in upscale residential projects in regions like North America and Western Europe.

Retrofit and upgrade programs rise across mature markets: Older commercial buildings in North America and Europe are increasingly retrofitting existing plumbing fixtures; in some cities, municipal incentive schemes cover up to 40% of the cost for upgrading to touchless or water-efficient faucets, leading to accelerated replacement cycles.

Integration with home automation and voice-control systems: Models that connect to voice assistants, or smartphones for scheduling or remote control, are increasingly being included in new residential developments; in some affluent suburbs, more than 25% of new specialty faucet installations in 2024 included some form of smart/voice control feature.

The Specialty Faucets Market is segmented by type, application, and end-user, each contributing uniquely to the industry’s overall dynamics. Product types include touchless faucets, sensor-based faucets, and specialty utility faucets designed for niche functions. Applications span across residential, commercial, and institutional use cases, with residential installations holding the highest adoption due to increasing home renovation trends and consumer preference for premium fittings. Commercial applications, however, are expanding rapidly, particularly in hospitality and healthcare, where hygiene and efficiency are critical. End-users range from homeowners to businesses and public institutions, with businesses driving strong adoption in sectors such as hospitality and retail. Understanding these segments provides insights into evolving consumer needs, innovation patterns, and competitive strategies within the market.

Within the Specialty Faucets Market, touchless faucets stand as the leading type, driven by heightened hygiene awareness and the growing preference for hands-free solutions in both residential and commercial environments. Their widespread adoption in healthcare and hospitality has reinforced their market dominance, making them a standard in new infrastructure projects. Sensor-based faucets are emerging as the fastest-growing type, benefitting from continuous technological innovation, improved energy efficiency, and integration with smart home ecosystems. This growth is further supported by the rise of smart city developments, particularly in Asia-Pacific. Specialty utility faucets, though a smaller category, play a significant role in industrial and laboratory settings, offering durability and precision where specialized use is required. Designer and luxury faucets also contribute to niche demand, catering to premium residential projects where aesthetics and customization are key. The interplay among these types demonstrates a balance between functional demand and lifestyle-driven preferences across global markets.

Residential applications dominate the Specialty Faucets Market, fueled by rising consumer expenditure on home renovation and remodeling, along with the popularity of modern kitchens and bathrooms featuring advanced fixtures. Homeowners are increasingly adopting water-efficient and smart faucets, aligning with both lifestyle aspirations and sustainability goals. Commercial applications, however, are expanding at the fastest pace, especially within the hospitality and healthcare sectors. Hotels, restaurants, and hospitals prioritize touchless and sensor-based faucets to enhance hygiene, meet regulatory requirements, and deliver superior user experiences. Institutional applications, including schools, public restrooms, and government facilities, contribute consistently to overall demand, driven by large-scale infrastructure modernization. While residential remains the largest application area, commercial projects are shaping innovation and accelerating adoption of advanced technologies. The steady growth across applications underscores the market’s adaptability to diverse environments and its alignment with evolving global infrastructure priorities.

Homeowners represent the leading end-user segment in the Specialty Faucets Market, supported by rising disposable incomes, a growing preference for home automation, and the emphasis on modern, stylish fixtures that enhance property value. This segment benefits from rapid adoption of premium and designer faucets, particularly in urban centers where lifestyle upgrades are more prevalent. The commercial sector is emerging as the fastest-growing end-user, driven by strong demand in hospitality, healthcare, and retail spaces. Businesses are increasingly prioritizing advanced faucets that combine hygiene, energy efficiency, and design aesthetics to meet customer and operational needs. Public and institutional end-users, including educational facilities and government infrastructure projects, also contribute to market expansion, especially as large-scale programs adopt water-efficient and smart solutions to align with sustainability targets. Together, these end-user dynamics reflect a balanced mix of individual consumer demand and organizational investments, shaping the future trajectory of the specialty faucets industry.

Asia-Pacific accounted for the largest market share at 38% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

The Asia-Pacific region benefits from its strong manufacturing base, high-volume residential and commercial construction activities, and rapid adoption of smart home technologies, particularly in China, India, and Japan. North America, on the other hand, is witnessing accelerated adoption of advanced water-saving and touchless technologies, driven by regulatory frameworks and growing consumer preference for premium, sustainable bathroom and kitchen fittings.

North America held approximately 28% share of the Specialty Faucets Market in 2024, reflecting the region’s strong demand across residential remodeling and commercial construction projects. Key industries driving adoption include healthcare, hospitality, and premium residential developments, where hygiene-focused and luxury fittings are prioritized. Regulatory changes such as state-level water efficiency mandates and the expansion of EPA’s WaterSense program have further fueled demand for compliant specialty faucets. Technological advancements are shaping the market through AI-enabled monitoring systems, integration with home automation platforms, and voice-controlled faucets. Digital transformation in plumbing distribution networks has also streamlined supply chains, accelerating product adoption across the United States and Canada.

Europe represented nearly 24% of the Specialty Faucets Market in 2024, led by major economies such as Germany, the UK, and France. European Union regulations on water conservation and sustainable materials have played a crucial role in shaping product design and innovation. Governments and organizations are promoting eco-labels and stricter lead-free standards, compelling manufacturers to innovate in finishes, materials, and efficient flow technologies. Technological adoption is rising, particularly in smart faucets with digital temperature control and IoT integration. Consumer preference in Europe also leans toward premium aesthetics and designer fittings, with Italy and Germany acting as key hubs for high-end manufacturing and product innovation.

Asia-Pacific accounted for the largest volume of the Specialty Faucets Market in 2024, with China, India, and Japan being the top consuming nations. Rapid urbanization, strong government-backed housing initiatives, and large-scale infrastructure projects continue to drive demand. China is recognized as the global manufacturing hub for specialty faucets, with large production facilities and high R&D investment in sensor-based and AI-enabled technologies. India’s smart city projects are stimulating installation of water-efficient, touchless faucets across public and private infrastructure. Japan is pushing technological boundaries with IoT-enabled faucets designed for compact urban living. Innovation hubs across Asia are enhancing production efficiency and enabling rapid scaling to meet both domestic and export demand.

South America accounted for nearly 6% of the Specialty Faucets Market in 2024, with Brazil and Argentina being the primary contributors. Rapid expansion of urban infrastructure and hotel development in Brazil has spurred adoption of durable, water-efficient specialty faucets. Argentina has seen growing demand in healthcare and educational institutions, driving upgrades to hygienic, touchless fixtures. Regional trade agreements and supportive government incentives in Brazil have lowered import barriers for advanced faucet technologies, creating opportunities for global brands to establish stronger presence. Infrastructure modernization programs across the region are expected to boost demand for premium and functional faucet solutions over the forecast period.

The Middle East & Africa accounted for approximately 4% of the Specialty Faucets Market in 2024, with the UAE and South Africa as leading growth countries. Demand is driven by mega construction projects, tourism-focused developments, and oil-funded infrastructure expansion. In the UAE, luxury hotels and premium residential complexes increasingly specify touchless and sensor-based faucets to align with hygiene and sustainability standards. South Africa is witnessing gradual modernization of public facilities, with government-led housing projects integrating water-efficient specialty faucets. Regional trade partnerships and regulatory efforts aimed at water conservation are accelerating adoption of advanced technologies, particularly in Gulf Cooperation Council countries.

The Specialty Faucets Market is characterized by a moderately fragmented competitive landscape with over 40 active global and regional manufacturers. Leading players are positioned strongly through diversified portfolios spanning touchless, sensor-based, and designer faucet categories, catering to residential, commercial, and institutional demand. Strategic initiatives such as cross-border partnerships, acquisitions, and investments in research and development are driving competition as companies aim to strengthen product differentiation. In 2024, several market participants launched advanced models integrating AI-enabled water flow control and IoT-based monitoring, reflecting a shift toward digitalization and smart technologies. Competitive intensity is further influenced by sustainability trends, with firms investing in eco-friendly manufacturing processes and water-efficient product lines. Emerging regional manufacturers, particularly in Asia-Pacific, are adding price competitiveness, while established brands maintain their edge through strong distribution networks and brand equity. The landscape is increasingly shaped by innovation, regulatory compliance, and customer preference for high-performance, sustainable, and technologically advanced faucets.

Kohler Co.

Moen Incorporated

Grohe AG

Delta Faucet Company

American Standard Brands

Roca Sanitario S.A.

Hansgrohe SE

TOTO Ltd.

Jaquar Group

Franke Holding AG

The Specialty Faucets Market is witnessing rapid technological advancement, reshaping product design, functionality, and performance standards. Sensor-based technology continues to dominate, with infrared and capacitive sensors enabling precise touchless operation, reducing water wastage by up to 30% in commercial and residential installations. AI-driven flow regulation is gaining traction, allowing faucets to automatically adjust water pressure and temperature based on usage patterns, improving both efficiency and user comfort. Integration of IoT platforms enables real-time monitoring, predictive maintenance, and connectivity with smart home ecosystems, with adoption rates particularly strong in North America and Asia-Pacific.

Material innovation is also a significant factor, with manufacturers adopting lead-free alloys, antimicrobial coatings, and corrosion-resistant finishes to enhance durability and meet stringent safety standards. Energy-efficient components, such as aerators and flow restrictors, are being refined with nanotechnology, delivering measurable reductions in water and energy consumption. Cloud-enabled faucet management systems are increasingly utilized in commercial facilities, offering centralized data collection and control. Emerging innovations such as voice-controlled faucets and integration with AI-powered assistants are expected to expand adoption across premium residential and high-end hospitality sectors. Collectively, these advancements position technology as the central driver of competitiveness, efficiency, and customer value within the Specialty Faucets Market.

• In February 2024, Kohler unveiled a new line of smart kitchen faucets with integrated voice and gesture controls, designed to enhance convenience and water efficiency in residential spaces. The models include real-time water usage monitoring.

• In May 2024, Grohe launched its updated sensor faucet range featuring antimicrobial surface coatings, targeting healthcare facilities where hygiene standards demand durable and easy-to-sanitize fixtures.

• In September 2023, TOTO introduced a next-generation commercial faucet with AI-assisted flow regulation, capable of reducing water consumption by 25% compared to conventional sensor faucets.

• In November 2023, Hansgrohe expanded its luxury faucet segment by introducing customizable smart faucets with app-based control, allowing users to personalize water temperature and pressure settings.

The Specialty Faucets Market Report provides a comprehensive examination of the industry, covering a wide array of product types, applications, regional insights, and emerging technologies. Segmentation includes touchless faucets, sensor-based faucets, utility faucets, and designer faucets, with detailed analysis of their roles across residential, commercial, and institutional applications. End-user coverage spans homeowners, businesses, and public institutions, highlighting adoption patterns across both established and emerging economies.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional consumption, industrial adoption, and infrastructure growth trends. Each regional section emphasizes demand drivers such as construction activity, technological modernization, and regulatory compliance.

From a technology perspective, the report explores sensor innovation, AI integration, IoT connectivity, and material science advancements shaping product development. It also assesses the role of sustainability through eco-friendly materials and water-efficient design enhancements.

The scope extends to competitive intelligence, profiling leading global manufacturers and evaluating strategies such as partnerships, product launches, and R&D investments. Niche segments, including luxury faucets and specialized utility models, are also addressed, providing a complete view of industry opportunities. By synthesizing these elements, the report offers decision-makers actionable insights into current dynamics and future opportunities in the Specialty Faucets Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 2,265.1 Million |

| Market Revenue (2032) | USD 2,959.7 Million |

| CAGR (2025–2032) | 3.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Kohler Co., Moen Incorporated, Grohe AG, Delta Faucet Company, American Standard Brands, Roca Sanitario S.A., Hansgrohe SE, TOTO Ltd., Jaquar Group, Franke Holding AG |

| Customization & Pricing | Available on Request (10% Customization is Free) |