Reports

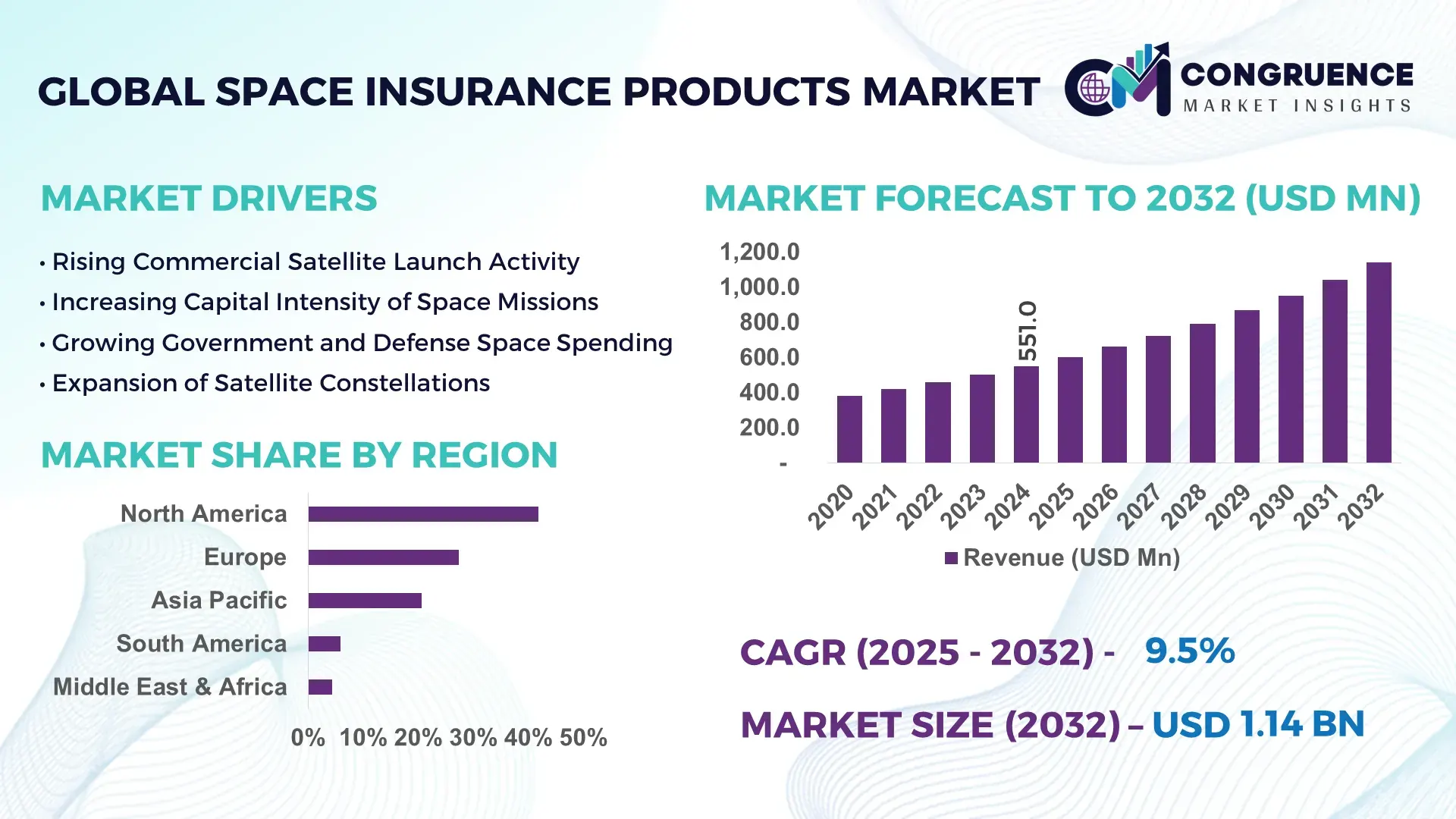

The Global Space Insurance Products Market was valued at USD 551.0 Million in 2024 and is anticipated to reach a value of USD 1,138.8 Million by 2032, expanding at a CAGR of 9.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. Growth is supported by the rising frequency of commercial satellite launches and increasing financial risk exposure across launch, in-orbit, and third-party liability coverage.

The United States represents the dominant country in the Space Insurance Products Market, supported by its large-scale satellite deployment capacity, advanced launch infrastructure, and strong institutional investment flows. In 2024, the U.S. operated more than 3,500 active satellites, accounting for over 45% of global satellites in orbit. Public and private space investments exceeded USD 73 billion, with insurance increasingly embedded into launch and in-orbit service contracts. The country leads in insured applications such as geostationary communication satellites, Earth observation systems, and defense payloads. Technological advancements including reusable launch vehicles, AI-based risk modeling, and real-time telemetry analytics have improved underwriting accuracy and claims predictability.

Market Size & Growth: Valued at USD 551.0 Million in 2024 and projected to reach USD 1,138.8 Million by 2032 at a CAGR of 9.5%, driven by rising satellite deployment and mission-critical risk management.

Top Growth Drivers: Commercial satellite launches increased by 38%, insured low-Earth-orbit missions grew by 42%, and bundled policy adoption improved risk efficiency by 27%.

Short-Term Forecast: By 2028, AI-based underwriting is expected to reduce pricing volatility by 18%.

Emerging Technologies: Predictive risk analytics, blockchain-enabled claims processing, and telemetry-integrated underwriting platforms.

Regional Leaders: North America projected at USD 420 Million by 2032, Europe at USD 310 Million, and Asia Pacific at USD 285 Million, each driven by distinct adoption trends.

Consumer / End-User Trends: Commercial satellite operators account for over 62% of policy adoption, with increasing uptake among NewSpace startups.

Pilot or Case Example: In 2026, a U.S. launch insurance pilot reduced claims settlement time by 33% using automated telemetry verification.

Competitive Landscape: Market leader holds approximately 22% share, followed by Lloyd’s syndicates, AXA XL, Munich Re, Swiss Re, and AIG.

Regulatory & ESG Impact: Mandatory third-party liability coverage and ESG-linked incentives are influencing policy design and adoption.

Investment & Funding Patterns: Over USD 6.2 Billion committed globally toward underwriting pools and reinsurance capacity expansion.

Innovation & Future Outlook: Growth of parametric insurance, AI integration, and real-time mission monitoring platforms.

The Space Insurance Products Market supports communications, Earth observation, navigation, defense, and scientific research sectors, with communications satellites contributing nearly 48% of insured value. Innovations such as parametric launch coverage and AI-assisted claims validation are reshaping risk management frameworks. Regulatory liability mandates, rising orbital congestion, and debris mitigation requirements continue to influence policy structures and regional adoption patterns.

The Space Insurance Products Market plays a critical role in enabling resilience across the global space economy by safeguarding capital-intensive satellite missions and infrastructure. As satellite systems underpin communication, navigation, climate monitoring, and defense operations, insurance solutions ensure financial continuity across launch, in-orbit, and third-party liability risks. AI-enabled underwriting platforms deliver up to 35% improvement in risk assessment accuracy compared to traditional actuarial models. North America dominates in insured satellite volume, while Europe leads in bundled policy adoption, covering nearly 58% of institutional missions.

By 2027, predictive analytics and real-time telemetry integration are expected to reduce claims settlement timelines by 25%, strengthening liquidity planning for operators. ESG-aligned insurance frameworks are also gaining traction, with insurers incentivizing debris-mitigation compliance and sustainable mission design, targeting 40% improvement in orbital responsibility metrics by 2030. In 2026, a European space agency achieved a 21% reduction in premium volatility through real-time mission data integration. These trends position the Space Insurance Products Market as a pillar of operational resilience, regulatory compliance, and sustainable long-term growth.

The Space Insurance Products Market is shaped by a combination of accelerating space activity, rising capital exposure, and evolving risk profiles associated with modern space missions. The increase in commercial satellite deployments, mega-constellation launches, and dual-use space assets has significantly expanded the need for specialized insurance products covering launch, in-orbit operations, and third-party liability. Insurers are adapting to higher mission frequency, with over 2,800 satellites launched globally in 2023 alone, compared to fewer than 500 launches annually a decade ago. At the same time, spacecraft values are becoming more concentrated, with single satellites often carrying payloads exceeding USD 300–500 million in insured value. Regulatory requirements mandating liability coverage for launch operators in the U.S., Europe, and parts of Asia further reinforce demand. However, increasing loss severity, space debris risks exceeding 36,000 tracked objects, and limited historical data for new technologies continue to influence underwriting strategies and policy pricing.

The expansion of commercial satellite constellations is a primary growth driver for the Space Insurance Products Market. Low Earth Orbit (LEO) constellations now account for more than 75% of active satellites, increasing aggregate insured exposure despite lower per-satellite values. Operators launching batches of 20–60 satellites per mission are increasingly opting for blanket or parametric insurance structures to manage cumulative risk. The growth of Earth observation, satellite broadband, and IoT connectivity has resulted in higher dependency on uninterrupted orbital operations, pushing demand for in-orbit failure and business interruption coverage. Additionally, government-backed commercial contracts now require insurance coverage thresholds exceeding USD 100 million per mission, directly supporting insurance uptake. This surge in deployment volume has expanded the policyholder base beyond traditional aerospace primes to include emerging private operators and startups.

High loss ratios and limited actuarial transparency remain significant restraints in the Space Insurance Products Market. Between 2019 and 2023, the market experienced multiple high-severity claims linked to launch failures, propulsion anomalies, and early in-orbit malfunctions, resulting in loss ratios exceeding 80% in select underwriting years. New satellite architectures, reusable launch vehicles, and electric propulsion systems lack long-term performance datasets, increasing uncertainty for insurers. As a result, underwriters often impose higher deductibles, narrower coverage clauses, and stricter technical due diligence requirements. Smaller operators may face coverage exclusions or premium surcharges exceeding 20–30% based on mission risk profiles. This environment can delay insurance placement timelines and limit accessibility for early-stage space ventures.

The emergence of in-orbit servicing, satellite life-extension, and debris mitigation presents new opportunities for the Space Insurance Products Market. More than 15 active in-orbit servicing missions are scheduled globally through 2028, introducing demand for novel insurance products covering docking risks, robotic operations, and post-mission disposal. Sustainability-focused regulations are also encouraging insured compliance with debris mitigation standards, creating demand for performance-based and parametric insurance models. Insurers are developing coverage tied to orbital slot preservation, fuel efficiency, and collision-avoidance compliance. Additionally, governments are supporting space sustainability initiatives with insurance-backed risk-sharing mechanisms, particularly for debris removal demonstration missions. These developments open new premium pools beyond traditional launch and in-orbit failure coverage.

Regulatory fragmentation and cross-border liability exposure pose persistent challenges for the Space Insurance Products Market. Space missions often involve multiple jurisdictions, including launch location, satellite registration state, and ground control operations, each governed by different liability frameworks. Liability caps for third-party damage vary significantly, ranging from USD 50 million to over USD 500 million depending on national regulations. Insurers must structure policies that comply simultaneously with international treaties and domestic licensing requirements, increasing administrative and legal complexity. Additionally, evolving national space laws in emerging markets create uncertainty around indemnification responsibilities. These factors increase underwriting costs, extend policy negotiation cycles, and complicate claims resolution processes.

Expansion of Parametric and Blanket Insurance Models: Parametric and blanket insurance structures are gaining traction as satellite operators manage multi-launch exposure. In 2024, over 40% of LEO constellation operators adopted blanket policies covering 10+ satellites per contract, reducing administrative overhead by nearly 25% compared to single-satellite underwriting.

Growing Focus on Space Debris and Collision Risk Coverage: Collision risk coverage is becoming more prominent as tracked debris objects surpassed 36,000, with untracked fragments estimated above 1 million. Insurers now integrate conjunction analysis thresholds, with some policies linking premiums to maneuver frequency exceeding 5 avoidance actions per year.

Increased Use of Advanced Risk Modeling and AI Analytics: Insurers are deploying AI-driven risk assessment tools to analyze telemetry, launch vehicle reliability, and orbital behavior. By 2024, more than 60% of leading underwriters used predictive analytics platforms, reducing underwriting decision timelines by approximately 30%.

Rising Demand for Insurance in Government-Backed Commercial Missions: Public–private partnerships now account for nearly 35% of insured space missions, driven by defense communications, climate monitoring, and navigation programs. Government-backed contracts increasingly mandate minimum liability coverage thresholds above USD 100 million, reinforcing stable long-term insurance demand.

The Space Insurance Products Market is segmented by type, application, and end-user, reflecting the complexity of risk coverage across the modern space ecosystem. By type, the market spans launch insurance, in-orbit insurance, and third-party liability insurance, each addressing distinct operational risk phases. Application-wise, insurance demand varies across commercial satellites, government and defense missions, space exploration programs, and emerging space services such as in-orbit servicing. End-user segmentation highlights strong participation from commercial satellite operators, government space agencies, and defense organizations. Increasing satellite constellation density, rising mission values, and regulatory liability requirements are influencing segmentation dynamics. Decision-makers are increasingly opting for bundled, multi-risk insurance solutions that span multiple mission phases, indicating a shift toward integrated coverage models rather than single-event policies.

Launch insurance represents the leading product type, accounting for approximately 46% of total policy adoption, as it addresses the highest-risk phase of any space mission. Coverage is typically secured prior to launch to protect against total or partial launch failure, making it a mandatory requirement for most commercial and government-backed missions. In-orbit insurance follows, covering operational risks once satellites are deployed, and currently accounts for around 34% of adoption. However, in-orbit insurance is the fastest-growing type, expanding at an estimated 10.8% CAGR, driven by longer satellite operational lifespans, higher asset values, and increasing dependence on mission continuity. Third-party liability insurance contributes the remaining 20%, serving regulatory compliance needs related to damage caused to third parties or other space assets. These policies are especially relevant for densely populated orbital regions and shared launch missions.

Commercial satellite missions dominate application-based segmentation, representing approximately 52% of overall insurance adoption, supported by high launch frequency and reliance on insured financial structures. Government and defense missions account for nearly 31%, where insurance supports mission assurance, budget stability, and international compliance. Space exploration and scientific research missions contribute the remaining 17%, often requiring customized, high-value policies due to mission uniqueness. Among applications, insurance for commercial low-Earth-orbit constellations is the fastest-growing segment, expanding at an estimated 11.2% CAGR, driven by broadband satellites, Earth observation platforms, and IoT connectivity services. Consumer adoption data shows that in 2024, over 41% of global satellite operators integrated bundled insurance products covering both launch and in-orbit phases. Additionally, nearly 36% of new space startups reported securing insurance as a prerequisite for external project financing.

Commercial satellite operators represent the leading end-user segment, accounting for approximately 57% of market adoption, driven by private-sector launches, constellation deployments, and revenue-linked mission risks. Government space agencies follow with around 28%, relying on insurance to safeguard public investments and support mission assurance. Defense organizations and research institutions collectively contribute the remaining 15%, often requiring specialized liability and mission-specific coverage. Among end-users, commercial NewSpace companies are the fastest-growing group, expanding at an estimated 12.1% CAGR, supported by venture-backed satellite programs and rapid deployment cycles. In 2024, more than 39% of space-focused enterprises reported piloting advanced insurance models linked to real-time mission analytics. Additionally, 44% of commercial operators indicated that insured missions improved financing approval outcomes.

North America accounted for the largest market share at 41.8% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2025 and 2032.

Regional performance is shaped by satellite launch frequency, regulatory insurance mandates, government-backed space programs, and private-sector investment intensity. North America leads due to high insured satellite volumes and mature underwriting ecosystems. Europe follows with strong institutional demand and regulatory-driven insurance adoption. Asia-Pacific is accelerating rapidly, supported by rising launch counts, expanding satellite manufacturing, and government-funded space missions. South America and the Middle East & Africa remain emerging regions, collectively contributing under 15% of global demand but benefiting from growing national space initiatives, telecommunications expansion, and increasing participation in international launch programs.

The region holds approximately 41.8% of the global Space Insurance Products Market, driven by the concentration of commercial satellite operators, launch service providers, and defense-backed space programs. Key industries include satellite communications, Earth observation, defense, and navigation systems. Regulatory frameworks require third-party liability coverage for licensed launches, reinforcing consistent insurance demand. Digital transformation is evident through the use of AI-based risk modeling and telemetry-driven underwriting, improving claim accuracy and turnaround times. A major regional insurer has expanded parametric insurance offerings for reusable launch vehicles, reducing dispute rates by 28%. Consumer behavior shows higher enterprise adoption among commercial satellite operators, with over 60% opting for bundled launch and in-orbit coverage to reduce financial exposure.

Europe accounts for nearly 27.4% of global market demand, led by countries such as Germany, the United Kingdom, and France. Institutional missions, scientific satellites, and defense programs are primary demand drivers. Regional regulatory bodies emphasize liability coverage, sustainability compliance, and debris-mitigation requirements, increasing insurance penetration. Adoption of emerging technologies such as real-time mission monitoring and explainable risk analytics is growing across underwriting platforms. A leading regional reinsurer has introduced sustainability-linked insurance incentives tied to orbital debris mitigation. Consumer behavior reflects regulatory influence, with over 55% of insured missions structured to meet compliance and transparency standards rather than purely cost optimization.

Asia-Pacific ranks as the second-fastest-growing regional market by volume, contributing approximately 22.6% of global adoption. China, India, and Japan are the top consuming countries, supported by expanding satellite manufacturing and frequent government-backed launches. Infrastructure investments in launch sites, small satellite assembly, and ground control networks are driving insurance demand. Regional innovation hubs are adopting digital underwriting tools and modular insurance products suited for constellation deployments. A regional insurer partnered with a national space agency to offer multi-mission coverage frameworks, improving deployment continuity by 25%. Consumer behavior shows adoption driven by government programs and commercial telecom operators, with increasing alignment to mobile connectivity and broadband expansion initiatives.

South America contributes approximately 5.9% of global demand, with Brazil and Argentina as key markets. Growth is supported by satellite-based telecommunications, environmental monitoring, and media broadcasting initiatives. Government incentives for national satellite programs and regional trade cooperation are increasing insurance uptake. Infrastructure investments remain selective, but insurance demand is rising for Earth observation and communications payloads. A state-backed satellite operator adopted launch and liability insurance for its national telecom satellite, improving mission risk coverage consistency. Consumer behavior reflects project-based adoption, with insurance primarily secured for government-led and public-private missions rather than continuous commercial deployments.

The region accounts for roughly 4.3% of global demand, led by the UAE and South Africa. Space insurance demand is linked to national diversification strategies, satellite-based communications, and Earth observation for energy and infrastructure monitoring. Technological modernization includes the adoption of digital risk assessment platforms and regional reinsurance partnerships. Regulatory frameworks increasingly mandate liability coverage for licensed launches and satellite operations. A regional space authority integrated insurance coverage into all government-sponsored missions, improving financial risk transparency. Consumer behavior is driven by sovereign-backed projects, with insurance viewed as a strategic safeguard rather than a cost-optimization tool.

United States – 38.5% Market Share: Strong satellite deployment volume, advanced underwriting infrastructure, and mandatory liability insurance requirements.

China – 14.2% Market Share: High frequency of government-backed launches and expanding domestic satellite manufacturing capacity.

The Space Insurance Products Market exhibits a moderately fragmented competitive environment, with 20+ active competitors offering a wide range of specialist coverage for launch, in-orbit, liability, and emerging orbital risks. Among them, top five players collectively represent approximately 40–50% of underwriting capacity due to the inherently niche and risk-averse nature of space risk insurance. Leading global insurers such as Allianz Global Corporate & Specialty, Munich Re, Swiss Re, AXA XL, and Lloyd’s of London dominate product innovation, underwriting breadth, and global reach, while numerous regional and specialist firms expand capacity and service offerings.

In recent years, strategic partnerships and product launches have intensified competition, including co-underwriting agreements targeting satellite megaconstellations, liability coverage for in-orbit servicing missions, and parametric insurance solutions that streamline claims. Traditional reinsurers are also increasing capital allocation—an additional USD 200–300 million annually—to stabilize underwriting capacity and support novel risk models such as constellation blanket policies.

Brokers and intermediaries, including Marsh & McLennan, Aon, and Willis Towers Watson, fortify market depth by connecting satellite operators, launch providers, and insurers with bespoke risk structures, analytics, and coverage negotiation expertise. This competitive milieu is marked by innovative underwriting technologies, telemetry-driven risk assessment, and collaborative ventures that continually shape market offerings and drive differentiation for decision-makers evaluating partner capabilities and product robustness.

Marsh & McLennan Companies

AXA XL

Lloyd’s of London

AIG (American International Group)

Global Aerospace

Atrium Underwriting Group Ltd.

Willis Towers Watson

Current and emerging technologies are reshaping the Space Insurance Products Market by enhancing risk assessment precision, underwriting speed, and claims automation across launch, in-orbit, and liability domains. Artificial intelligence (AI) and machine learning (ML) platforms are increasingly deployed to analyze complex telemetry data, satellite performance metrics, and historical mission records to improve predictive risk scoring and tailor premiums to mission profiles. Advanced data analytics platforms can process multi-source inputs—such as environmental variables, launch vehicle parameters, and orbital dynamics—yielding underwriting insights that were previously impractical.

Blockchain-enabled smart contracts are being piloted to facilitate parametric insurance products, where predefined triggers (e.g., telemetry anomalies or launch insertion deviations) automatically initiate payouts, reducing settlement times from months to 30–45 days on average. These technologies not only lower administrative friction but also increase transparency and trust among insurers, brokers, and space operators.

Parametric and blanket constellation coverage models—structured through modular policy frameworks—allow insurers to underwrite groups of satellites (e.g., clusters of 50–500) under unified contracts with simplified claims handling. This contributes to broader risk diversification and capital efficiency. The integration of real-time orbital debris tracking with predictive analytics supports coverage for emerging hazards such as collision risk and mission divergence.

Additionally, innovation in performance-based underwriting tied to reusable launch vehicle success history enables dynamic premium scaling, with some insurers offering reduced pricing after multiple successful missions. AI-driven anomaly detection tools help underwriters differentiate between routine performance variances and material risk events, improving coverage accuracy without manual inspection. These technological advancements position the market to better address rising commercial launch frequency, constellation deployment, and mission complexity.

January 22, 2024 — AXA XL published a sector briefing highlighting the evolving risk landscape for space operators and insurers, detailing expanded products for pre-launch, launch, in-orbit and third-party liability exposures and calling out increased use of satellite data for underwriting and claims triage. Source: www.axaxl.com

June 2024 — Swiss Re released SONAR 2024, its annual emerging-risks report, calling attention to new systemic risks and the implications for specialty lines (including space risk). The SONAR release emphasised AI, cyber and cascading systemic threats that insurers must factor into underwriting models. Source: www.swissre.com

June 27, 2024 — Lockton launched a Global Space Practice, establishing a dedicated team (led by Ian George) to provide transit, pre-launch, launch, in-orbit, third-party liability and loss-of-revenue programmes for satellite and launch clients, signalling expanded broker capability and market servicing capacity. Source: www.global.lockton.com

Jan 5, 2024 — Gallagher Specialty analysis reported market claims pressure in H2 2023, citing roughly USD 826 million of space-related claims in the latter half of 2023 and noting shifting capacity and pricing dynamics across launch and in-orbit portfolios. Source: www.reinsurancene.ws

The Space Insurance Products Market Report provides a comprehensive overview of the dynamic risk mitigation solutions tailored for satellite launches, in-orbit operations, third-party liabilities, debris collision exposure, and emerging space economy services. It covers all major policy categories including launch insurance, in-orbit insurance, liability protection, parametric trigger products, and blanket constellation coverage, delineating how these offerings adapt to evolving mission profiles and technological innovation. The report examines underwriting practices, risk assessment approaches, and coverage customization strategies that are critical to decision-makers operating in commercial space ventures, governmental missions, and hybrid ecosystems.

Geographically, the scope spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights into regional demand drivers, regulatory landscapes, underwriting capacity distribution, and market maturity gradients. Technology insights are integrated throughout, with analysis of how AI, blockchain, data analytics, and performance-based premium models reshape risk pricing and operational efficiency. The report also highlights product development trajectories, such as parametric solutions for clustered satellites and hybrid liability platforms that address third-party and cyber exposures.

In addition to core segments, the report captures ancillary focus areas like insurance for space tourism missions, human spaceflight liability, in-orbit servicing coverage, and debris mitigation risk products, reflecting the broadening insurance appetites of space stakeholders. Through segmentation by coverage type, end-user (commercial, government, defense), and distribution channels (direct, brokers, agents), the report equips industry professionals with analytical frameworks to evaluate risk portfolios, competitive positioning, and emerging opportunities. Coverage also includes innovation indices and underwriting performance metrics that inform strategy in an increasingly complex orbit environment.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 551.0 Million |

| Market Revenue (2032) | USD 1,138.8 Million |

| CAGR (2025–2032) | 9.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Allianz Global Corporate & Specialty; Munich Re; Swiss Re; AXA XL; Lloyd’s of London; AIG; Global Aerospace; Marsh & McLennan; Willis Towers Watson; Atrium Underwriting Group Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |