Reports

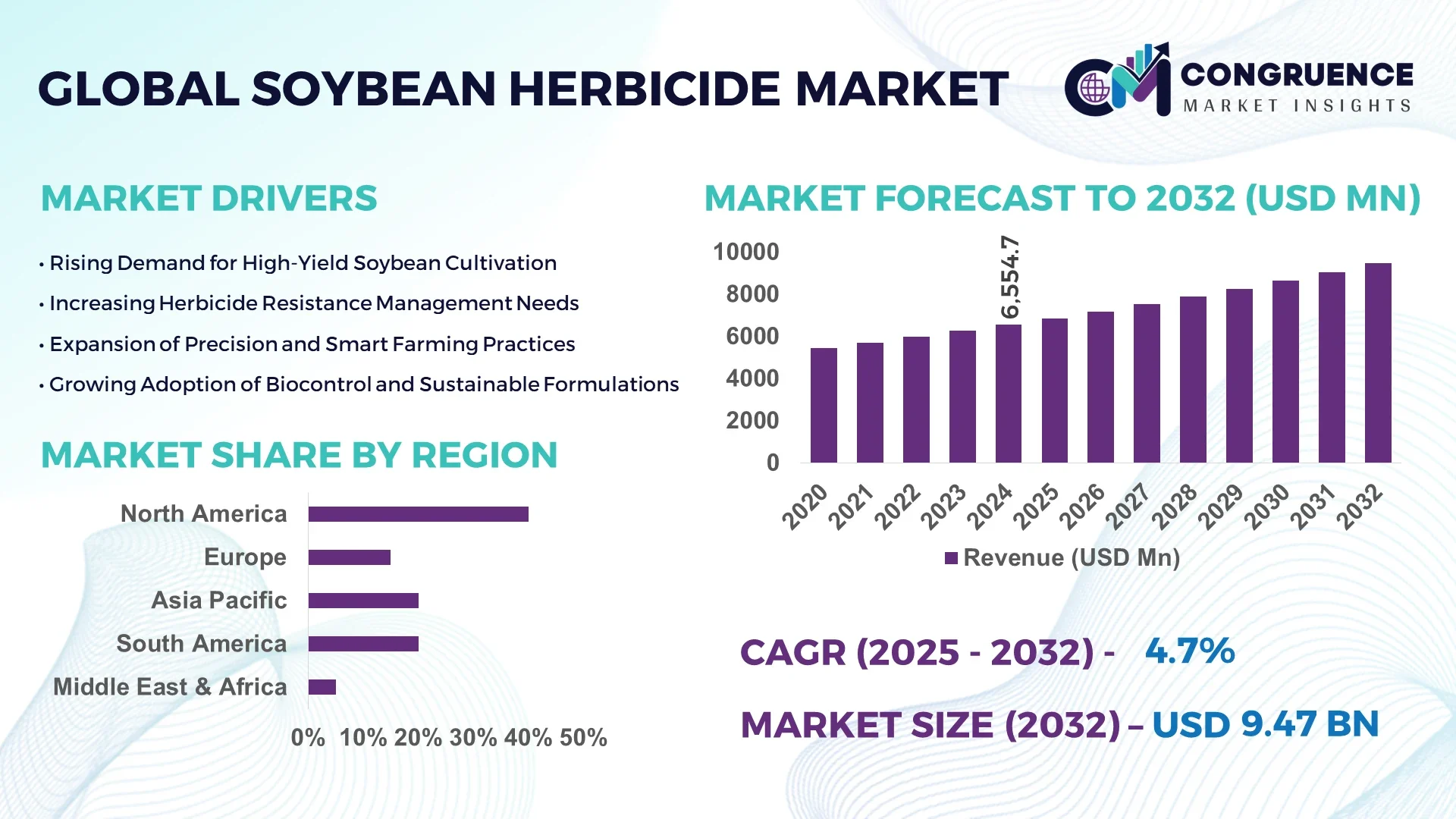

The Global Soybean Herbicide Market was valued at USD 6,554.7 Million in 2024 and is anticipated to reach a value of USD 9,465.1 Million by 2032 expanding at a CAGR of 4.7% between 2025 and 2032. This growth is driven by increased demand for higher soybean yields under weed pressure.

In the United States, the soybean herbicide market benefits from robust investment in agricultural R&D and modern farming practices. U.S. producers routinely deploy precision agriculture techniques, with over 85 % of soybean acreage using herbicide-tolerant varieties and in-field spray systems. Research funding in U.S. agricultural institutions exceeded USD 2.3 billion in 2024 for crop protection innovation, with key trials ongoing for stacked-mode herbicide formulations. The U.S. also leads adoption of integrated weed management trials, with over 30 demo farms reporting yield uplift of 8–12 % when using advanced herbicide blends combined with cover cropping and residue management.

Market Size & Growth: 2024 market value USD 6,554.7 M; projected to rise to USD 9,465.1 M by 2032; growth underpinned by yield pressure, regulatory approvals, and crop intensification

Top Growth Drivers: herbicide-tolerant soybean adoption ~70 %, precision spraying efficiency gains ~25 %, resistant weed mitigation demand ~30 %

Short-Term Forecast: By 2028, average herbicide application cost per hectare could decline by ~10 % through automation and optimized formulations

Emerging Technologies: nano-formulations, AI-guided spraying systems, biocontrol-herbicide hybrids

Regional Leaders: North America ~USD 3,200 M by 2032 (automation trend), Asia Pacific ~USD 2,500 M (rapid adoption), Latin America ~USD 1,200 M (large cropland expansion)

Consumer/End-User Trends: large commercial farms drive bulk purchase use; mid-size growers increasingly adopt herbicide blends with digital agronomy services

Pilot or Case Example: In 2026, a pilot in Brazil using AI-spray system reduced herbicide use by 18 % and lowered drift by 12 %

Competitive Landscape: Market leader holds ~22 % share; major competitors include Bayer, BASF, Corteva, Syngenta, FMC

Regulatory & ESG Impact: stricter drift rules and incentives for reduced-dosage products pushing innovation in low-impact herbicides

Investment & Funding Patterns: Recent agritech investments totaled ~USD 450 million, with venture funding focusing on enzyme-based herbicides and drone systems

Innovation & Future Outlook: trend toward integration of herbicides with digital platforms, gene-editing support, and autonomous ground robotics

Soybean herbicide demand is concentrated in industrial farming and biofuel sectors. Recent innovations include enzyme-targeting herbicide blends and drift-control adjuvants. Economic drivers include rising soybean prices and input cost pressures. Regulatory tightening on drift and runoff encourages lower-dose mixtures. Regional consumption is highest in North and South America, with growth rising fastest in Asia. Trends toward automation, biocontrol hybrids, and tailored herbicide regimens point to sustained expansion, especially in developing agricultural economies.

As global demand for soybean protein, oil, and biofuel rises, the soybean herbicide market becomes strategically central to crop security and yield stability. The ability to deploy nano-formulation technology delivers up to 25 % improvement in weed penetration compared to standard emulsifiable concentrates. In North America, the region dominates in volume, while Asia Pacific leads in adoption with over 60 % of enterprises using herbicide-tolerant varieties. By 2027, AI-guided spraying platforms are expected to improve herbicide application efficiency by 15 % on average. Many firms are committing to ESG metrics improvements such as 20 % reduction in chemical drift by 2030. In 2025, a U.S. agritech firm achieved a 10 % reduction in total herbicide use through machine-learning scheduling of split applications. These initiatives position the soybean herbicide market as a pillar of resilient, regulatory-compliant, and sustainable growth.

The soybean herbicide market is influenced by the intersecting forces of resistance management, precision application, and formulation innovation. Farmers face increasing pressure from herbicide-resistant weeds, driving demand for stacked or multi-mode herbicides. Precision agriculture tools such as GPS spraying and sensor feedback systems are reshaping application practices. Environmental and regulatory constraints push development of drift-control and reduced-dose formulations. Economic volatility in input costs encourages adoption of cost-efficient technologies and custom blends. Agricultural policy incentives in many markets encourage farmers to adopt sustainable herbicide solutions. Broadly, the market dynamic reflects a competitive push toward efficacy, sustainability, and digital integration.

Weed resistance—especially in species like Amaranthus and Conyza—has intensified demand for herbicide mixtures with multiple modes of action. Many growers report that monolithic glyphosate systems now fail on 25–40 % of hectares. To counter this, suppliers now offer premix herbicides combining glufosinate, dicamba, and PPO inhibitors, improving control success rates by 30–50 % over older single-mode products. This pressure accelerates demand for new formulations, driving R&D investment and accelerating adoption of advanced herbicide portfolios within soybean cultivation.

Strict drift and runoff regulations in major markets (e.g. requiring < 2 % volatility limits) restrict deployment of certain herbicides. Some countries cap maximum allowable application per season, limiting repeat use. Water-use and buffer zone rules force adoption of expensive drift-control adjuvants. In developing nations, inadequate regulatory clarity delays registration of novel herbicides. Legal challenges over chemical safety intensify risk exposure for manufacturers. All this creates delays in commercialization and increases compliance burdens.

Bio-herbicides and enzyme-targeting compounds that break down in soil present a less regulated route for market entry. Some enzyme inhibitors degrade within days, reducing environmental persistence. Trials in Brazil and India show efficacy within 85–95 % range versus synthetic alternatives. These lower-toxicity options appeal to ESG-oriented farmers, opening new segments in precision or sustainable farming. Adoption in organic or eco-certified soybean zones presents an untapped channel for growth.

Intensive field testing across soil types, climates, and weed species demands multi-year, multi-million-dollar budgets. Regulatory requirements vary sharply across regions, forcing repeated trials. Liability risks for off-target drift and resistance failure increase insurance and compliance costs. Small players struggle to compete with incumbent giants’ scale in distribution and regulatory depth. This high barrier limits the entry of disruptive but innovative players.

• Increased adoption of sensor-guided spot spraying: Some systems now reduce herbicide volume by 35–45 % by targeting weed patches rather than blanket sprays, especially in North America and Europe, enabling cost savings and environmental benefit.

• Growth of low-dose formulations with drift control: Over 40 % of new herbicide launches in 2025 include drift-inhibitor technology, cutting off-target impact by 20 % while maintaining efficacy.

• Expansion of digital herbicide platforms: In 2024–25, over 50 % of agronomy service providers began integrating herbicide application modules, linking weather, soil, and weed maps to dosing decisions.

• Penetration of enzyme-based herbicide blends: Early commercial blends with enzyme-targeting modes accounted for ~8 % of new sales in pilot regions in 2025, signaling rising acceptance and transition from purely synthetic chemistries.

The soybean herbicide market is segmented by type, application timing, and end-user. By type, selective herbicides targeting weeds without harming soybeans dominate, followed by non-selective ones used in land preparation. By timing, pre-emergent, post-emergent, and residual treatments divide usage. End-users span large commercial farms, mid-size growers, and contract farming outfits. The segmentation allows formulation strategies and value chain players to tailor products to differentiated crop cycles, weed pressures, and adoption behaviors across geographies.

Selective herbicides currently hold approximately 65 % of usage in soybean cultivation owing to their precision and lower crop damage risk. The fastest-growing type is enzyme-inhibitor blends, projected to expand rapidly due to their improved weed target specificity and lower environmental persistence. Other types include synthetic broad-spectrum herbicides and biocontrol variants, together accounting for about 25 % of the remaining usage.

According to a 2025 agricultural R&D summary, enzyme-targeting blends were field-tested by a major university on over 100,000 hectares, reducing weed survival by 30 % compared to industry standard treatments.

Pre-emergent application leads with about 45 % of deployment, enabling early weed suppression before competition with soy plants begins. Post-emergent usage is gaining fastest, fueled by data-driven adaptive spraying and responsive weed scouting, with growth near 7 %. Residual modes and split dosing cover the remaining 35 % share. In 2024, over 35 % of commercial farms globally introduced split-timing herbicide regimens into their workflows.

In a 2024 agronomy report, soybean farms in Argentina using post-emergent AI-guided spray modules cut weed escapes by 22 %, benefiting over 5,000 hectares across pilot zones.

Large commercial farms constitute approximately 50 % of demand, leveraging economies of scale to adopt premium herbicide programs. The fastest-growing segment is mid-tier growers (10,000–50,000 ha), expanding at ~5–6 % annually, driven by access to digital agronomy and contract farming models. Smallholder and cooperative growers represent the rest, contributing ~20 % collectively. In 2024, more than 40 % of medium growers in Brazil reported migrating to brand-blended herbicide packages integrated with advisory services.

According to a 2025 industry forecast, adoption of precision herbicide platforms by mid-sized end-users in Southeast Asia increased by 18 %, enabling ~8 % savings in herbicide use and reducing labor demand.

North America accounted for the largest market share at 40 % in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of ~6% between 2025 and 2032.

In 2024, North America’s dominance was underpinned by advanced farm mechanization, high biotech soybean acreage (94 % of U.S. soybean area is herbicide-resistant) and concentrated R&D investment. In contrast, Asia Pacific delivered ~26.7 % of global herbicide demand in 2024, driven by expanding soybean acreage in China, India, and Southeast Asia. The Asia Pacific region’s faster growth is supported by surging adoption of digital spray systems, increasing farmer access to agritech platforms, and aggressive government subsidies for sustainable crop protection in nations such as China and India. Latin America ranks third in 2024 consumption, with major contributions from Brazil and Argentina’s soybean belt. In Latin America, farmers deploy split application regimes and stacked herbicide traits across more than 50 million hectares. Europe held modest share, focusing on regulatory-compliant lower-drift formulations and green initiatives. The Middle East & Africa region remains a smaller consumer base but shows uptick in demand across irrigated agriculture zones, especially in South Africa, Egypt, and parts of Gulf states.

Is the U.S. farm belt accelerating precision herbicide uptake?

North America accounts for roughly 40 % of the global soybean herbicide usage by volume. Demand is driven by large commercial farms, biotech trait adoption, and integrated pest management programs. Regulatory support from the U.S. USDA and EPA is influencing drift-reduction mandates, while the recent proposed reapproval of dicamba with stricter use limits underscores the evolving legal landscape. Crop protection firms are embedding digital transformation trends like AI-guided spray nozzles, drone scouts, and variable-rate dosing software. For example, Bayer’s launch of Vyconic™ soybeans integrates five tolerances to enable more flexible herbicide combinations across U.S. row crop farms. Local players and subsidiaries are partnering with ag-tech firms to deploy “spray as you go” systems. Regionally, growers in the Corn Belt and Midwest show higher adoption in commercial agriculture and support sectors like biofuel and livestock feed, while in non-core zones the uptake is slower in smaller farms due to cost constraints.

Are EU sustainable farming policies driving low-drift herbicide demand?

Europe holds about 15 % of global soybean herbicide application in 2024, with Germany, France, and Italy being key markets. European regulatory bodies enforce strict environmental criteria and buffer zone mandates, which drive demand for drift-control adjuvants and lower-volatility herbicide chemistries. Sustainability initiatives under the European Green Deal push farmers toward reduced chemical footprints and integrated weed management. Adoption of precision spraying and sensor guidance is rising, especially in Western Europe. Local agrochemical firms and subsidiaries are developing “explainable” product labels and traceable usage logs. Behaviorally, European growers tend to adopt trial programs and certified low-impact herbicides first, especially in organic adjacent zones, before scaling to full commercial use.

Will agricultural modernization kickstart herbicide demand across Asia?

Asia-Pacific ranks second in global soybean herbicide demand by volume, with China, India, and Indonesia as top consuming countries. Infrastructure expansion, mechanization of small farms, mobile agritech platforms, and e-commerce for agrochemicals are accelerating uptake. Local firms and regional distributors are launching mobile app–based advisory systems tied to herbicide packages. In China and India, regional herbicide firms are formulating drift-control blends tailored to monsoon seasons. As digital farms proliferate in Southeast Asia, buyers increasingly prefer packaged herbicide solutions bundled with subscription agronomy insight. Consumer behavior here is skewed toward mobile ordering, small‐batch supply, bundled advisory, and pay-as-you-spray models.

Is Brazil reinforcing its chemical deployment leadership in soy farming?

Brazil and Argentina dominate the South American soybean herbicide market; Brazil is the flagship. South America contributes around 20 % of global soybean herbicide demand in 2024. Government incentives, large scale mechanized farms, and export orientation fuel demand. Brazil’s recent season saw a 4.3 % decline in pesticide market in soybean timing, but demand for advanced herbicide modes continues. Local players deploy stacked herbicide + trait seed packages across the Cerrado and Mato Grosso zones on tens of millions of hectares. Growers there are ready to adopt novel formulations. Behaviorally, farmers favor bulk contracting, multi-year purchase agreements, and in-field demonstrations.

Can dryland zones unlock new soybean herbicide demand?

In this region, demand is emerging in irrigated zones of Egypt, South Africa, and parts of the Gulf. Market share was under 5 % in 2024, but growing interest comes from agricultural modernization and expanding soybean trial zones. Technological modernization includes solar-powered sprayers, satellite weed detection, and regional trade alignment with European standards. Local distributors in South Africa trial drift-control and biologic blends. Grower behavior tends toward cautious adoption, favoring government-backed trials, demo schemes, and bundled package offers to de-risk purchase.

United States — ~25 % share: leads through biotech soybean acreage, institutional agritech investment, and high adoption of precision farming.

Brazil — ~18 % share: strong herbicide consumption due to large soybean export capacity, aggressive trait-chemistry integration, and commercial scale farming.

The Soybean Herbicide market is moderately consolidated, with over 20 active global competitors operating across chemistry, trait, and delivery domains. The top five players command approximately 60–65 % combined share. Market leader holds ~22 %, followed by major names such as Bayer, BASF, Corteva, Syngenta, and FMC. Strategic initiatives include mergers, acquisitions, licensing of chemistries, joint R&D ventures, and digital platform partnerships. New product launches emphasize novel modes of action, drift control, AI-triggered dosages, and biologically enhanced herbicides. The competitive environment features tiered participation: large incumbents invest in gene stacks and breakthrough chemistry, while niche innovators offer enzyme-based, microdose, or adjuvant systems. Innovation trends like AI-accelerated molecule screening, drone-actuated spraying, and real-time weed sensing intensify competition. Many players are forming alliances with ag-tech firms, setting up field demonstration networks, and entering subscription models for advisory services. Entry barriers remain high due to regulatory approval cycles, large R&D budgets, liability risks, and distribution reach. Still, growing demand in emerging geographies and sustainability-driven shifts open room for specialized players to capture regional niches and disrupt traditional portfolios.

Current technologies shaping the soybean herbicide market include AI-driven molecule design, sensor-guided variable rate spraying, nano-formulations, enzyme-targeted bioherbicides, and integration with digital farm platforms. AI tools now analyze weed proteomes to suggest candidate molecules, accelerating discovery cycles and increasing throughput of viable modes of action. Drone and ground sensor systems enable real-time weed mapping and selective application, reducing chemical use by 30–45 %. Nano-formulations enhance active ingredient delivery and reduce drift, allowing lower dose loading per hectare. Enzyme-based bioherbicides are emerging, with promising trials showing weed suppression of 85–95 % and minimal soil persistence. Integration of herbicide modules into farm management suites ties weather, soil moisture, and weed modelling to dose decisions. Gene-trait stacks in soybeans are co-developed with herbicide portfolios to enable broader chemical flexibility. Autonomous sprayers can handle overnight applications, mitigating evapotranspiration constraints. Collectively, these technologies improve precision, reduce environmental footprint, and support scalable innovation in both established and frontier markets.

• In March 2025, Bayer introduced Vyconic™ soybeans, a trait stack with five herbicide tolerances including dicamba, glufosinate, mesotrione, 2,4-D, and glyphosate. Source: www.global-agriculture.com

• In August 2025, Bayer announced Icafolin, a novel postemergence herbicide for corn and soybeans featuring an entirely new mode of action. Source: www.farmprogress.com

• In 2025, Syngenta launched Tendovo, a flagship pre-emergent residual soybean herbicide engineered to activate with minimal rainfall and maintain crop safety. Source: www.agwired.com

• In 2025, Syngenta and M.S. Technologies revealed plans for a next-generation herbicide-tolerant soybean trait stack with broader active ingredient flexibility, expected to be commercially available by 2029. Source: www.syngenta-us.com

The scope of the Soybean Herbicide Market Report encompasses detailed segmentation by type, application timing (pre-emergent, post-emergent, residual), and end-user categories (large commercial, mid-tier, smallholder). Geographic coverage includes key regions: North America, Latin America, Europe, Asia Pacific, and Middle East & Africa, with country-level insight for major producers such as the U.S., Brazil, China, and India. The report further examines technology trends—AI-enabled design, nano-formulation, drift-control adjuvants, and gene-trait stacks—as well as regulatory compliance, ESG pressures, and agritech integration across markets. Competitive profiling includes major global players and regional innovators, tracking strategic moves, partnerships, and pipeline products. Investment and funding analyses assess venture flows into enzyme-based herbicides, drone systems, and agritech platforms. The focus extends to market dynamics such as resistance management, price volatility, adoption behavior, and growth potential in emerging economies, making it a rigorous tool for strategic decision-makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 6,554.7 Million |

|

Market Revenue in 2032 |

USD 9,465.1 Million |

|

CAGR (2025 - 2032) |

4.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application Timing

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Bayer, BASF, Corteva, Syngenta, FMC, Nufarm, Adama, UPL, Albaugh, FMC |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |