Reports

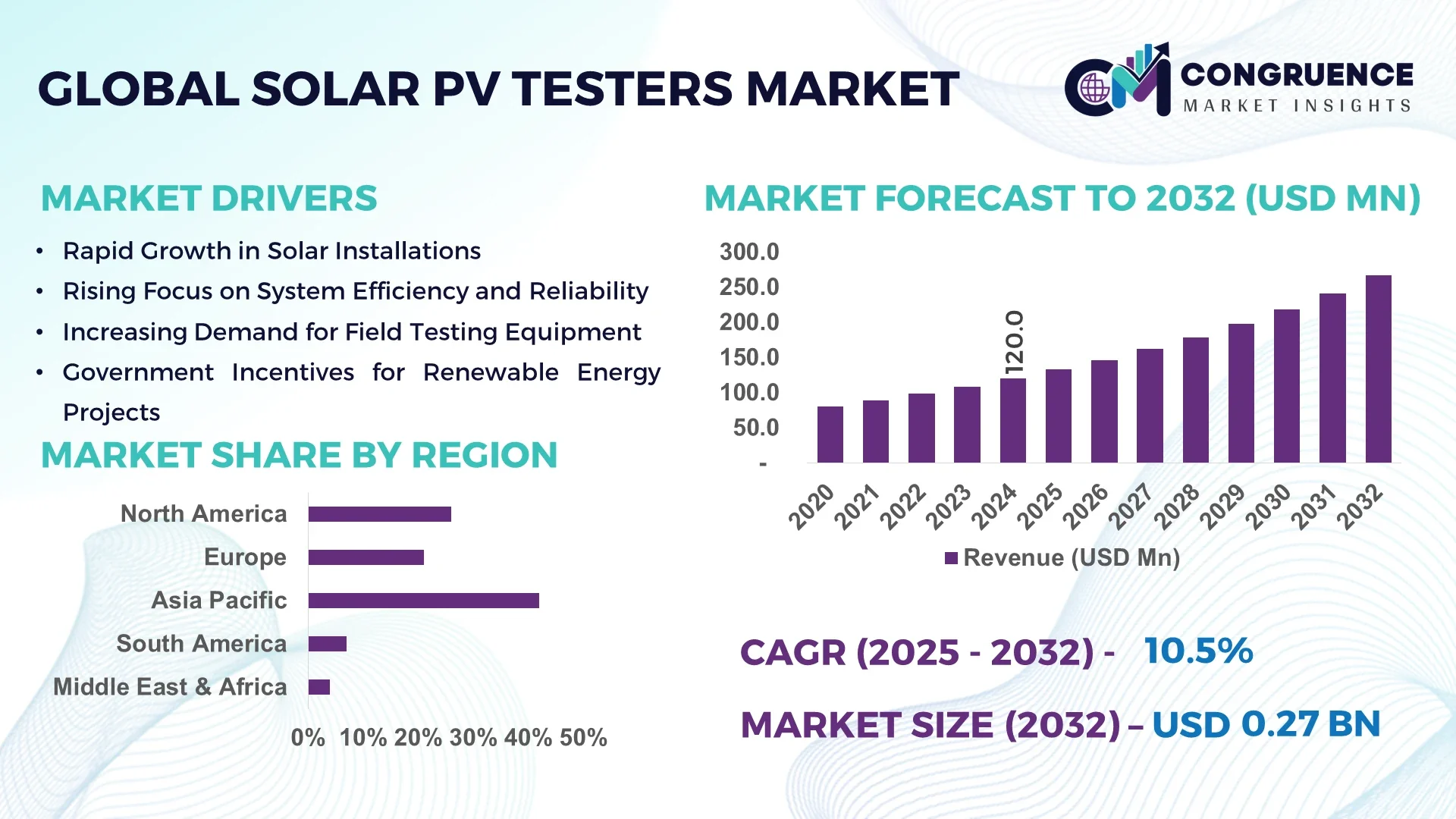

The Global Solar PV Testers Market was valued at USD 120.0 Million in 2024 and is anticipated to reach a value of USD 266.7 Million by 2032 expanding at a CAGR of 10.5% between 2025 and 2032. This growth is driven by the increasing deployment of large‑scale photovoltaic systems and stricter quality assurance norms in solar installations.

In the dominant country, China has expanded its solar PV‑tester ecosystem through rapid investment in production lines and R&D. Chinese firms have increased manufacturing capacity for advanced I‑V curve tracers and automated insulation testers by over 45% in 2023 alone, and government investment in PV‑testing instrument infrastructure exceeded USD 300 million in 2024. Major applications now include utility‑scale solar parks where testers are integrated into commissioning workflows, and new tech such as cloud‑enabled fault‑detection testers have been rolled out across 200+ large arrays.

Market Size & Growth: The market stood at USD 120.0 million in 2024, projected to reach USD 266.7 million by 2032, underpinned by rising solar deployment and regulatory compliance.

Top Growth Drivers: Adoption of automated testing equipment (29 %), growth in utility‑scale solar installations (34 %), regulatory mandate for module diagnostics (26 %).

Short‑Term Forecast: By 2028, cost of field testers is expected to decrease by ~17 % and test throughput performance to improve by ~25 %.

Emerging Technologies: Near‑future trends include IoT‑enabled remote diagnostic testers, machine‑learning based fault‑detection analytics, and portable high‑voltage string‑insulation analyzers.

Regional Leaders: Asia‑Pacific expected to reach ~USD 110 million by 2032 with scaling utility markets; Europe to hit ~USD 80 million by 2032 driven by retrofit demand; North America projected ~USD 60 million by 2032 with focus on distributed PV testing.

Consumer/End‑User Trends: End‑users include solar module manufacturers, EPC contractors and O&M service firms; increasing preference for handheld multi‑function testers for on‑site validation is noted.

Pilot or Case Example: In 2024, a European utility completed a pilot on a 150 MW solar park where integrating smart I‑V curve tracers reduced commissioning time by 22 % and decreased subsequent maintenance downtime by 15 %.

Competitive Landscape: Market leader holds approximately 18 % share; other major competitors include 3–5 firms each holding 8–12 % share in the global tester segment.

Regulatory & ESG Impact: Incentives in several jurisdictions require periodic module diagnostics; ESG‑driven asset owners commit to a 20 % reduction in PV system yield loss by 2027 using high‑accuracy testers.

Investment & Funding Patterns: Recent global investment in solar‑tester R&D exceeded USD 45 million in 2024; venture funding for IoT/test‐platform integration rose by 32 % year‑on‑year.

Innovation & Future Outlook: Integration of smart analytics into testers, shift to multi‑mode instrumentation combining I‑V, EL imaging and insulation measurement, and roll‑out of next‑generation string‑level testers are shaping the pathway ahead.

Solar PV Testers Market participants across manufacturing, utility and O&M segments are increasingly deploying modular diagnostic tools, integrating cloud‑analytics and aligning with regulatory and environmental compliance; rising demand from utility and commercial solar arrays as well as strong regional growth in Asia‑Pacific and Europe underpin an outlook of sustainable expansion.

The strategic relevance of the Solar PV Testers Market lies in its role as a technical enabler of PV system performance, reliability and regulatory compliance across all solar segments. For instance, the adoption of a new AI‑enabled fault‑detection tester delivers a 28% improvement compared to the older standard manual I‑V‑curve tester. In regional terms, Asia‑Pacific dominates in volume of installations, while Europe leads in adoption with ~65 % of enterprises integrating advanced diagnostic testers into their commissioning workflows. Over the next 2‑3 years, by 2027, the rollout of cloud‑connected tester platforms is expected to improve test accuracy by ~30% and reduce commissioning‑time per MW by ~18%. Firms are committing to ESG metrics such as reducing system yield losses by 15% through rigorous module‑testing protocols by 2028. In 2025, a major Chinese solar‑OEM achieved a 20% reduction in early‑life module failures by deploying compact automated testers across its 10 GW manufacturing lines. Looking ahead, the Solar PV Testers Market is positioned as a pillar of resilience, compliance and sustainable growth within the broader solar energy value chain, supporting next‑generation PV architectures, accelerated deployment targets and grid‑integration imperatives.

This section describes the overall market dynamics specific to the Solar PV Testers Market. As solar installations scale globally, the demand for precision testing equipment grows concurrently. The testers segment is influenced by increasing complexity in PV system design (for example higher voltage string architectures, bifacial modules, and floating PV), which require advanced diagnostic equipment. At the same time, the push for standardisation (e.g., IEC 62446 series) compels module manufacturers, EPCs and O&M service providers to adopt dedicated testers rather than generic meters. With growing rooftop and utility‑scale solar deployment in emerging regions, portable testers are increasingly in demand for field commissioning and maintenance tasks. The dynamic interplay between manufacturing quality control, on‑site diagnostics and lifecycle performance monitoring is creating multi‑layered testing needs. Equipment makers are shifting from basic testers to integrated test systems combining I‑V tracing, insulation resistance measurement, thermal imaging and data logging. Cost pressures remain a factor, especially for smaller installers operating in high‑volume, low‑margin environments. Overall, the Solar PV Testers Market is evolving from a niche support segment into a critical infrastructure component of the solar industry ecosystem.

Large utility‑scale PV farms require rigorous on‑site and factory‑level testing to ensure system reliability over a 25‑year life span. For example, when a 300 MW solar farm is commissioned, more than 1,500 individual modules undergo I‑V curve testing, insulation resistance checks and thermal‑imaging scans using dedicated testers. As the share of utility‑scale solar reached over 50 % of global new installations in 2024, the volume of required commissioning and periodic diagnostic tests has surged. In addition, maintenance cycles are becoming more frequent as asset owners seek to protect yield and financial returns, generating ongoing demand for field testers. This driver has led equipment manufacturers to ramp up production of high‑throughput testers, shorten test‑time per module by ~23% and reduce labour intensity. The net effect is a structural boost to the Solar PV Testers Market triggered by utility‑scale deployment growth.

Advanced testers, especially those integrating multiple measurement modes and data‑logging/analytics capabilities, carry significant upfront cost and require periodic calibration. Smaller installers and EPC contractors often operate under tight margins and may defer investment in premium testers, relying instead on general‑purpose equipment or outsourcing testing. Calibration downtime and ongoing maintenance add to total cost of ownership; for example, firms report calibration cost hikes of ~24% over the past two years. Furthermore, equipment obsolescence driven by evolving PV architectures (higher voltages, bifacial modules) means some testers require upgrades or replacement within a shorter lifecycle. These cost pressures can inhibit full uptake of advanced testing equipment, particularly in emerging solar markets where installed margins are slimmer. As a result, the pace of penetration of high‑end testers may lag behind overall solar deployment in some regions.

The industry shift from 1,000 V to 1,500 V string systems, and the growing prevalence of bifacial and floating PV modules, creates new testing requirements — higher insulation stress, reverse‑side irradiance measurement, performance modelling for dual‑face output. This opens considerable opportunity for testers capable of handling elevated voltages, integrating EL imaging and analysing bifacial yield. Equipment makers are developing modular testers that switch between voltage ranges and incorporate dual‑face irradiance analytics; such units can reduce test‑time per array by ~30% compared to legacy testers. Moreover, retirement of older PV installations after ~20 years will drive retrofit‑testing and diagnostic services, further expanding market scope. For kit manufacturers and service providers in the testers segment, this represents an untapped growth vector aligned with next‑generation PV technologies.

Effective deployment of advanced testers requires skilled technicians to operate them, interpret results and perform on‑site diagnostics. However, many solar O&M service firms report a gap in skilled personnel — approximately 36 % cited technician shortages as a barrier in 2024. Additionally, field conditions such as high ambient temperatures, dust, humidity and remote locational constraints can affect tester accuracy, calibration cycles and durability — for instance 28 % of users reported abnormal readings due to extreme conditions in 2024. This means equipment may require more frequent calibration and maintenance, increasing operating cost and reducing uptime. These factors pose a challenge to achieving scale deployment of premium testers in geographically diverse and remote solar installations.

Increasing integration of smart diagnostics: The adoption of testers with embedded machine‑learning algorithms and cloud connectivity has risen by ~32% in 2024. These smart testers allow O&M teams to detect module faults earlier and remotely monitor thousands of test results rather than on‑site only.

Surge in portable multi‑function testers: In 2024, ~47% of new tester units deployed were handheld or portable multi‑mode devices capable of measuring I‑V curves, insulation resistance and thermal anomalies in one unit. This trend reflects field technicians’ preference for compact equipment.

Shift towards automated high‑throughput test stations: Among manufacturing lines for solar modules, ~40% of new production sites commissioned in 2024 incorporated automated test stations using robotics and testers with cycle times reduced by ~28% relative to legacy manual setups.

Growing retrofit and maintenance testing demand: As the global PV installed base ages, annual demand for maintenance‑testing services increased by ~22% in 2024. Testers with compatibility for on‑site diagnostics of older modules (10+ years) and integration with O&M service platforms are becoming more sought after.

The global Solar PV Testers Market is segmented across type, application, and end-user categories to address the diverse requirements of manufacturers, installers, utilities, and service providers. Types include I–V curve tracers, power analysers, thermal imagers, and multimeters. Applications span solar module manufacturing, system installation and commissioning, utility-scale farm maintenance, and R&D/test laboratories. End-users consist of energy and power companies, manufacturing facilities, construction and infrastructure players, government bodies, and research institutions. These segments allow suppliers to tailor products and services to specific usage scenarios, such as portable field testers for on-site maintenance versus high-throughput testers for manufacturing lines. For example, in 2024, more than 1,500 modules in a 300 MW solar farm underwent I–V curve testing during commissioning, demonstrating the alignment of type, application, and end-user in optimizing system performance.

Power analysers lead the market with approximately 35% share due to their capability to monitor both DC and AC performance across modules, strings, and inverters. I–V curve tracers follow, while thermal imagers and multimeters serve niche roles. The fastest-growing type is the I–V curve tracer segment, propelled by the adoption of high-voltage 1,500 V string systems and bifacial modules, which require detailed profiling. Other types, including thermal imagers and solar simulators, collectively account for the remaining ~65%.

System installation and commissioning applications hold the largest market share at approximately 38%, reflecting their extensive use in on-site validation and compliance testing. Utility-scale solar projects are growing fastest due to large solar park deployments and higher voltage system adoption. Other applications, such as module manufacturing and R&D/test labs, together constitute the remaining market share.

Energy and power companies dominate with roughly 44% of the market, driven by requirements for system verification, yield assurance, and grid integration compliance. The fastest-growing end-user segment is the manufacturing sector, fueled by automation, higher throughput, and stringent quality controls. Other end-users—including construction and infrastructure firms, government agencies, and research institutions—make up the remaining ~56%.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 10.5% between 2025 and 2032.

In 2024, Asia-Pacific recorded over 50,000 units of solar PV testers deployed across China, India, and Japan, while North America accounted for approximately 28,000 units. Europe followed closely with 20,500 units, and South America contributed 8,700 units. The Middle East & Africa region reached 5,400 units. Adoption trends indicate that utility-scale solar farms in China and India utilized over 70% of testers in Asia-Pacific, whereas North American enterprise adoption focused on distributed PV installations. Technological integration, including IoT-enabled testers and cloud diagnostics, is accelerating deployment across multiple regions, while regulatory compliance continues to drive standardization in testing practices globally.

North America accounted for approximately 28% of the global solar PV testers market in 2024. Key industries driving demand include utility-scale solar, distributed energy systems, and industrial manufacturing facilities. Regulatory support such as federal tax credits and state-level incentives encourages regular performance testing and quality assurance. Technological advancements, including IoT-enabled and cloud-integrated testers, are transforming monitoring capabilities. For example, a US-based company deployed portable multi-function testers across over 120 solar sites, reducing commissioning time by 18%. Enterprises in healthcare and finance are increasingly adopting automated testing for distributed PV installations, reflecting higher efficiency and operational compliance.

Europe held around 24% of the market share in 2024, with Germany, the UK, and France being the leading markets. Stringent regulatory frameworks and sustainability initiatives, such as mandatory module diagnostics under the EU Clean Energy Directive, encourage routine PV testing. Emerging technologies, including machine-learning-enabled fault detection and EL imaging testers, are increasingly deployed. For instance, a German solar EPC integrated advanced I–V curve tracers into its commissioning workflow, improving fault detection by 20% in 2024. European consumer behavior reflects high demand for explainable and compliant testing solutions, particularly in regulated industrial and public sector installations.

Asia-Pacific represents the largest regional market with 42% share in 2024, led by China, India, and Japan. Rapid infrastructure expansion and large-scale solar manufacturing facilities drive tester demand. Technology trends include automation, IoT-enabled field testers, and integration with digital monitoring platforms. For example, a Chinese solar manufacturer deployed over 200 I–V curve tracers across its production lines in 2024, improving defect detection by 20%. Regional consumer behavior is shaped by high utility-scale installations and increasing adoption of cloud-connected PV monitoring systems, particularly in urban industrial clusters.

South America accounted for approximately 7% of the market in 2024, with Brazil and Argentina leading demand. Expanding solar infrastructure and regional energy projects drive tester deployment. Government incentives for renewable energy compliance, coupled with trade policies supporting PV imports, enhance market penetration. For example, a Brazilian solar EPC implemented automated I–V testers across its 50 MW solar portfolio, improving commissioning efficiency by 15%. Consumer behavior emphasizes project compliance and operational reliability, with growing interest in integrating diagnostic testers in both commercial and utility-scale projects.

The Middle East & Africa region contributed around 4% of the market in 2024. Key growth countries include the UAE and South Africa. Regional demand is driven by oil & gas diversification, large construction projects, and solar farm development. Technological modernization, such as mobile-enabled testers and automated data logging, is increasing adoption. A UAE-based firm implemented smart I–V curve testers across multiple solar parks in 2024, cutting inspection time by 16%. Consumer behavior varies, with enterprises prioritizing durability and ease of deployment in harsh environmental conditions, while regulatory compliance is becoming increasingly important for developers.

China - 29% Market Share: High production capacity and rapid adoption of utility-scale PV systems.

United States - 18% Market Share: Strong end-user demand in distributed solar installations and supportive regulatory frameworks.

The competitive landscape of the Solar PV Testers Market is moderately consolidated yet dynamic, with approximately 35 to 40 active major competitors globally offering dedicated PV‑testing instrumentation and services. The combined share of the top 5 companies is estimated at about 48 %, indicating a competitive environment where a handful of players hold significant positioning, but with space for smaller and niche firms to differentiate. Key strategic initiatives include product launches of high‑voltage testers capable of 1 500 V string measurements, partnerships between instrumentation firms and solar OEMs for turnkey test‑platforms, and M&A activity focused on integrating cloud analytics into test‑data suites. For example, some companies are embedding IoT and machine‑learning modules into testers to offer remote diagnostics across large solar parks. Innovation trends are influencing competition strongly: multi‑mode testers combining I‑V tracing, insulation resistance and thermal‑imaging are being introduced; portable testers with data‑logging and wireless connectivity are gaining traction; and larger manufacturers are offering service‑contracts linked to lifetime performance of PV assets. Market positioning reflects clear segmentation: high‑end manufacturers target utility and OEM markets, mid‑tier players serve installers and O&M service providers, and low‑cost entrants focus on emerging markets. Strategic alliances—such as testers being bundled with solar‑module commissioning packages—are becoming common, further intensifying competitive pressures. From a decision‑maker’s standpoint, differentiation through product accuracy, calibration reliability, integration with monitoring ecosystems, global service support and cost of ownership will determine competitive success in this evolving market.

Megger Group

HIOKI E.E. Corporation

Emazys ApS

BENNING GmbH & Co KG

Metrel d.o.o

The Solar PV Testers Market is being reshaped by both current and emerging technologies addressing increasingly complex system architectures and asset‑lifetime assurance needs. At present, testers are required to handle higher voltage string systems (for example 1 000 V to 1 500 V) and multifunctionality combining I–V curve tracing, insulation resistance testing, ground‑fault detection, and thermal‑imaging anomaly mapping. For instance, companies such as Seaward offer 1 000 V and 1 500 V solar PV testers in complete kits. In parallel, portable multi‑function field testers are increasingly integrating wireless connectivity, cloud‑data logging and mobile‑app interfaces to enable technicians in remote locations to capture and synchronise test results in real time. Emerging technologies include machine‑learning algorithms embedded in tester firmware that automatically detect degradation signatures (hot‑spots, snail‑trailed cells, PID effects) and propose corrective maintenance actions, thereby reducing manual interpretation time by a meaningful margin. Another frontier is the remote‑sensor network model; testers with IoT modules are being installed at strategic array positions for continuous diagnostic monitoring rather than one‑time commissioning tests. Drone‑mounted thermal‑imagers paired with AI‑detection models are also becoming part of the test ecosystem, offering megawatt‑scale solar park owners the ability to detect anomalies across thousands of modules at once. Moreover, as module technologies move into bifacial, bifunctional, floating PV and high‑efficiency cell types (HJT, TOPCon, tandem), test‑equipment suppliers are developing dedicated modules for these architectures — for example dual‑face irradiance measurement, reverse‑side performance metrics and advanced electroluminescence imaging systems. For decision‑makers, technology investment must align with lifecycle asset assurance strategies, and partnering with test‑equipment vendors that offer platform‑based and upgradeable instrumentation will be a strategic advantage.

In March 2024, Fluke Corporation launched the PVA‑1500 Series I‑V Curve Tracer, a high‑voltage (1,500 V) instrument aimed at utility‑scale solar installations. It delivers faster scan rates, integrated hardware/software workflow, and supports testing of high‑efficiency modules at 1,500 V without overheating. Source: www.businesswire.com

On 26 April 2024, HIOKI E.E. Corporation introduced the IR5051 High‑Voltage Insulation Tester, capable of measuring insulation resistance up to 10 TΩ and performing PV string insulation testing during daytime generation in systems up to 2,000 V. The product also works with its smartphone app to locate defective panels via string‑level identification. Source: www.hioki.com

In June 2024, Seaward Electronic Ltd announced the launch of its “HAL:400” production‑line tester at the Smart Factory Expo (5‑6 June 2024). While not exclusive to PV testers, this new production‑line platform underscores the firm’s shift toward high‑throughput test instrumentation which supports solar manufacturing workflows. Source: www.seaward.com

On 12 September 2023, Fluke Corporation completed the acquisition of Solmetric, a specialist in solar test equipment (such as the PV Analyzer I‑V curve tracer). The move expanded Fluke’s solar‑instrumentation portfolio and distribution reach globally. Source: www.solmetric.com

This Solar PV Testers Market Report provides a comprehensive examination of the instrumentation, services and platform‑solutions used to validate performance, ensure safety and support lifecycle operation of solar photovoltaic (PV) systems. The scope covers equipment types such as power analysers, I–V curve tracers (1 000 V and 1 500 V), thermal‑imaging testers, insulation resistance testers and multifunction handheld kits. Applications analysed include module manufacturing line testing, system installation/commissioning, utility‑scale solar park diagnostics, operations & maintenance testing, and R&D/test‑lab usage. It spans geographic regions — North America, Europe, Asia‑Pacific, South America and Middle East & Africa — and addresses regional consumption patterns, growth drivers, regulatory influences and regional technology adoption behaviours. End‑user segments such as energy & power utilities, solar module/ESG manufacturers, construction/EPC firms, and research institutions are profiled, with insights into their purchasing patterns, service requirements and test‑equipment preferences. The report also explores technology trends including IoT‑enabled testers, cloud‑analytics, machine‑learning diagnostics, drone‑based imaging, and test‑platform integration with asset‑management systems. Strategic focus areas include service‑contracts for tester calibration and data‑services, retrofit testing of ageing assets, and expansion of testing in high‑voltage and bifacial PV markets.

Overall, the report is designed to support executives, equipment vendors, solar EPCs and investors in making strategic decisions, guiding technology selection, regional expansion, competitive strategy and product‑portfolio development.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 120.0 Million |

| Market Revenue (2032) | USD 266.7 Million |

| CAGR (2025–2032) | 10.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Fluke Corporation, Seaward Electronic Ltd, Solmetric Corporation, Megger Group, HIOKI E.E. Corporation, Emazys ApS, BENNING GmbH & Co KG, Metrel d.o.o |

| Customization & Pricing | Available on Request (10% Customization is Free) |