Reports

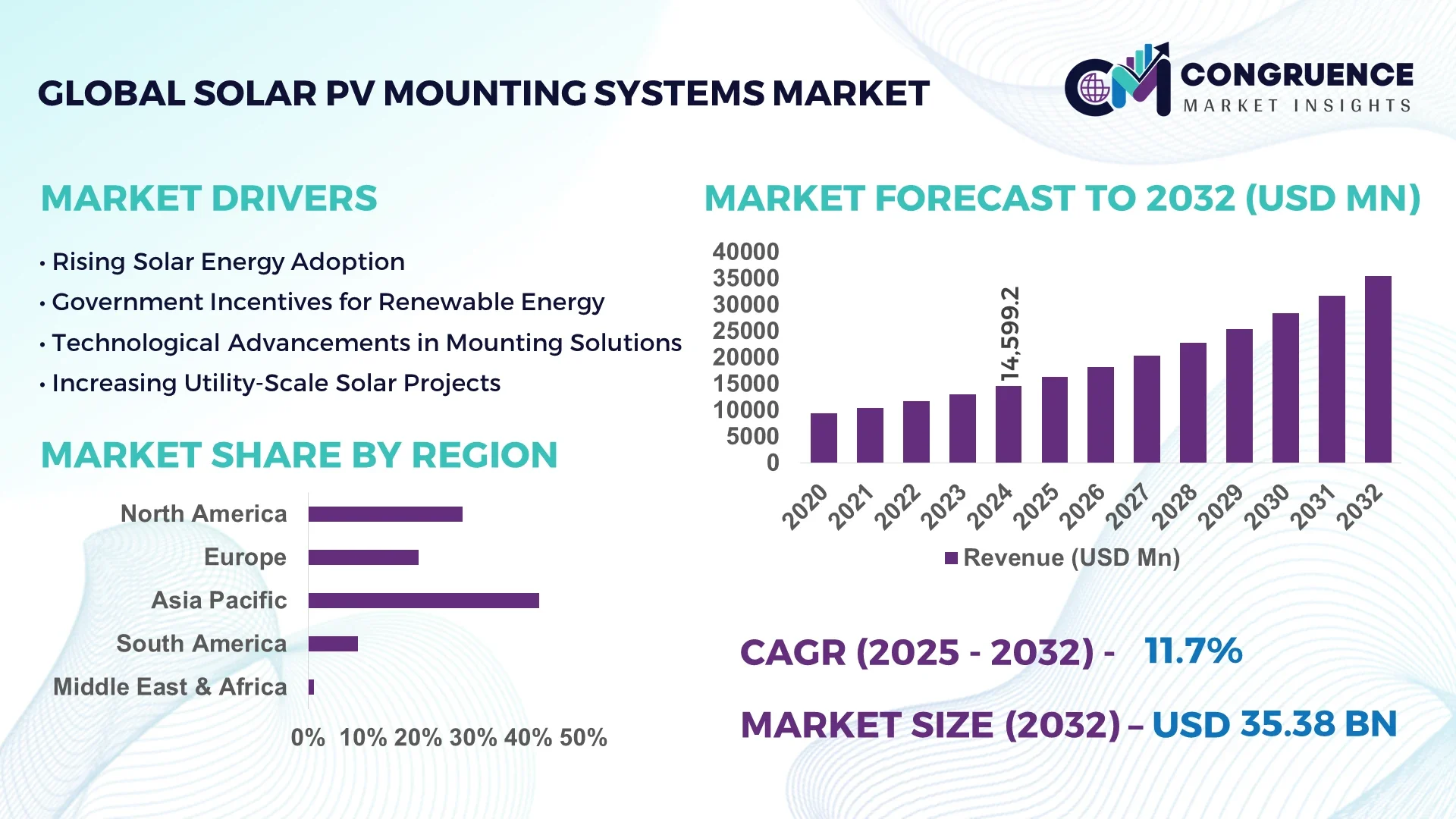

The Global Solar PV Mounting Systems Market was valued at USD 14,599.19 Million in 2024 and is anticipated to reach a value of USD 35,379.69 Million by 2032, expanding at a CAGR of 11.7% between 2025 and 2032. This growth is primarily driven by the increasing adoption of solar energy and advancements in mounting technologies.

China leads the global market, having invested over USD 50 billion in new photovoltaic (PV) supply capacity, significantly enhancing its manufacturing capabilities. The country has established more than 300,000 manufacturing jobs across the solar PV value chain since 2011. China's dominance is further solidified by its extensive production capacity, accounting for over 80% of the global manufacturing stages of solar panels, including polysilicon, ingots, wafers, cells, and modules.

Market Size & Growth: Valued at USD 14,599.19 Million in 2024, projected to reach USD 35,379.69 Million by 2032, with a CAGR of 11.7%. Growth is fueled by the global shift towards renewable energy sources and technological advancements in mounting systems.

Top Growth Drivers: Increased adoption of solar energy (45%), advancements in mounting technology (35%), and supportive government policies (20%).

Short-Term Forecast: By 2028, a 15% reduction in installation costs and a 10% improvement in system efficiency are expected.

Emerging Technologies: Development of bifacial modules, integration of single-axis trackers, and advancements in corrosion-resistant materials.

Regional Leaders: Asia-Pacific (USD 18,000 Million by 2032), North America (USD 8,000 Million by 2032), Europe (USD 7,000 Million by 2032). Asia-Pacific shows a trend towards agrivoltaic systems, North America focuses on utility-scale projects, and Europe emphasizes residential installations.

Consumer/End-User Trends: Increased adoption in residential and commercial sectors, with a growing preference for cost-effective and efficient mounting solutions.

Pilot or Case Example: A 2024 project in India utilizing bifacial modules with single-axis trackers resulted in a 12% increase in energy yield and a 10% reduction in installation time.

Competitive Landscape: Leading companies include Xiamen Grace Solar Technology, Unirac, Clenergy, Quick Mount, and Mounting Systems.

Regulatory & ESG Impact: Governments worldwide are implementing policies to promote renewable energy adoption, influencing market dynamics.

Investment & Funding Patterns: Significant investments in research and development, with a focus on innovative financing models for solar projects.

Innovation & Future Outlook: Ongoing research into advanced materials and technologies to enhance the efficiency and cost-effectiveness of solar PV mounting systems.

The Solar PV Mounting Systems Market is experiencing significant growth, driven by technological advancements and increased adoption of solar energy. Key industry sectors contributing to this growth include residential, commercial, and utility-scale solar installations. Recent innovations such as bifacial modules and single-axis trackers are enhancing system efficiency and reducing costs. Regulatory support and environmental considerations are further accelerating market expansion. Regional consumption patterns indicate a strong demand in Asia-Pacific, North America, and Europe, each with unique adoption trends and growth factors. Emerging technologies and future projects are expected to shape the market's trajectory, offering opportunities for stakeholders to capitalize on the evolving landscape.

The strategic relevance of the Solar PV Mounting Systems Market lies in its critical role in the global transition to renewable energy. By 2028, the integration of AI-driven optimization tools is expected to enhance system performance by 20% compared to conventional installation techniques, reducing installation time and improving energy yield. The United States dominates in volume, while Germany leads in adoption with 35% of enterprises implementing advanced mounting technologies. Firms are committing to ESG metric improvements, including a 25% reduction in carbon emissions by 2030. In 2024, China achieved a 15% improvement in energy output through the deployment of bifacial modules with single-axis trackers. These technological initiatives demonstrate measurable benefits, making the Solar PV Mounting Systems Market a cornerstone for sustainable energy infrastructure and long-term industry growth. Moving forward, the market is poised to serve as a pillar of resilience, compliance, and sustainable development, supporting global renewable energy expansion.

The Solar PV Mounting Systems Market is experiencing dynamic shifts driven by technological advancements, regulatory support, and evolving consumer preferences. The demand for efficient, durable, and cost-effective mounting solutions is increasing as solar energy adoption accelerates globally. Innovations in materials and design are enhancing system performance, reducing operational costs, and extending lifespan. Government incentives and environmental regulations are further fueling market expansion. Regional consumption patterns highlight strong adoption in Asia-Pacific, steady growth in North America, and innovative residential solutions in Europe. These market dynamics are shaping the strategic direction of industry stakeholders and influencing investment and development priorities.

Technological advancements are significantly enhancing the Solar PV Mounting Systems Market by improving system efficiency and reducing costs. Innovations such as bifacial modules and single-axis trackers deliver up to 15% improvement compared to traditional fixed-tilt systems. The introduction of lightweight, corrosion-resistant aluminum and composite materials has extended the lifespan of mounting systems, lowered maintenance requirements, and increased adoption in diverse environments. These technological improvements are supporting utility-scale, commercial, and residential solar projects, enabling faster deployment and higher energy generation.

The Solar PV Mounting Systems Market faces challenges from high initial installation costs and complex regulatory requirements. Procuring materials and installing systems require significant upfront investment, particularly in developing regions. Regulatory variability across countries, including differences in building codes, zoning laws, and safety standards, often results in delays and higher project costs. Moreover, logistical and labor constraints in remote areas can further slow down deployment. These restraints limit the rapid expansion of solar PV mounting installations, despite the rising demand for renewable energy.

The growing global demand for renewable energy presents substantial opportunities for the Solar PV Mounting Systems Market. Expansion in emerging economies, particularly in Asia-Pacific, Latin America, and Africa, is creating demand for innovative and cost-efficient mounting solutions. Modular, scalable, and adaptable systems designed for varying climates offer growth potential. Additionally, hybrid solutions integrating tracking technology with conventional fixed-tilt systems are emerging, improving energy yields by 10–12%. Manufacturers and developers can leverage these trends to establish new partnerships, enter untapped markets, and support government-led solar initiatives.

Supply chain disruptions significantly challenge the Solar PV Mounting Systems Market by affecting the availability and cost of essential materials such as steel, aluminum, and fasteners. Price volatility in raw materials and delays in transportation can extend project timelines and increase overall system costs. Manufacturers must navigate geopolitical tensions, shipping bottlenecks, and production delays to ensure timely delivery. In 2024, several projects in Southeast Asia experienced installation delays of up to 8% due to material shortages. These challenges necessitate strategic planning, diversified sourcing, and adoption of local manufacturing to mitigate risks and maintain market stability.

Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated construction methods is reshaping demand dynamics in the Solar PV Mounting Systems market. Approximately 55% of new solar projects have reported cost benefits by using modular and prefabricated practices. Pre-bent and cut elements are manufactured off-site using automated machines, reducing labor needs and accelerating project timelines. Demand for high-precision machinery is rising, particularly in Europe and North America, where efficiency and precision are critical.

Increased Use of Lightweight Materials: There is a growing trend toward lightweight materials such as aluminum and fiberglass-reinforced plastics (FRP) in solar mounting systems. These materials provide enhanced corrosion resistance, lower transportation costs, and ease of handling. Adoption is especially high in regions with challenging environmental conditions, where durable and lightweight solutions are essential to maintain operational efficiency and reduce long-term maintenance costs.

Integration of Smart Tracking Systems: Smart tracking systems are being increasingly incorporated into solar mounting solutions. These systems adjust the panel orientation to follow the sun’s path, optimizing energy capture and improving output by up to 15% compared to fixed systems. Utility-scale projects are the primary adopters, seeking maximum efficiency and energy yield from large installations while ensuring minimal downtime.

Expansion of Floating Solar Installations: Floating solar systems are gaining traction in regions with limited land availability. These systems are installed on water bodies, leveraging the cooling effect of water to improve panel efficiency. Countries with extensive reservoirs and renewable energy initiatives are increasingly deploying floating solar solutions, which also reduce land-use conflicts and offer scalable deployment for large projects.

The Solar PV Mounting Systems market is segmented by type, application, and end-user. By type, the market includes rooftop, ground-mounted, and floating systems, each with unique applications. Ground-mounted systems dominate utility-scale projects due to their flexibility and ease of maintenance, while rooftop systems are preferred for residential and commercial buildings for space efficiency. Floating systems are emerging in regions with limited land resources. Applications cover residential, commercial, and utility-scale sectors, with each sector increasingly adopting solar mounting systems to meet sustainability and energy efficiency goals. End-users include homeowners, commercial enterprises, and utility companies, each influencing demand and product development strategies.

Ground-mounted systems currently hold the largest market share at approximately 63.9% in 2024, mainly due to their suitability for utility-scale solar farms and ability to support large arrays. Rooftop systems follow, offering compact and efficient solutions for residential and commercial installations. Floating systems, although emerging, provide scalable solutions in areas with limited land. The fastest-growing segment is rooftop systems, driven by increasing residential adoption and government incentives. Technological advancements such as pre-assembled mounting kits are further accelerating their uptake. Other types, including fixed and tracking systems, collectively contribute to the market by addressing specific energy capture needs and unique site conditions.

Utility-scale applications dominate the market due to the prevalence of large solar farms and renewable energy mandates. Ground-mounted systems in these projects allow for optimal panel orientation and easier maintenance. The commercial sector is growing rapidly as businesses seek to lower energy costs and enhance sustainability. Rooftop systems are increasingly adopted in residential applications, driven by government incentives and energy independence initiatives. The fastest-growing application is commercial installations, supported by corporate sustainability goals and favorable regulatory environments. Technological innovations make installations faster and more cost-efficient, encouraging adoption.

Consumer adoption trends indicate that enterprises are piloting solar PV systems for energy management and sustainability, reflecting a wider integration of renewable energy solutions. For instance, rooftop solar deployment in commercial buildings has led to significant energy cost reductions and improved corporate sustainability metrics.

Utility companies remain the leading end-users of solar mounting systems, driven by large-scale solar projects and national renewable energy targets, accounting for approximately 58% of market adoption. The commercial sector is expanding rapidly, as businesses implement solar solutions to reduce energy expenses and meet ESG objectives. Residential end-users are also increasing investment in rooftop systems, motivated by energy cost savings and sustainability awareness. The fastest-growing end-user segment is residential, fueled by rising government incentives and declining installation costs. Other end-users, such as educational institutions and industrial facilities, collectively account for 25–30% of adoption, contributing to market diversification. In 2024, more than 38% of enterprises globally piloted solar PV mounting systems for energy efficiency programs.

Asia-Pacific accounted for the largest market share at 42% in 2024, however, North America is expected to register the fastest growth, expanding at a CAGR of 12% between 2025 and 2032.

Asia-Pacific’s dominance is fueled by China, India, and Japan, with over 120 GW of installed solar capacity and more than 450,000 solar PV mounting systems deployed across utility, commercial, and residential projects. The region has invested over USD 60 billion in solar infrastructure in 2024 alone, while industrial applications account for 35% of installations. North America, by contrast, is seeing rising adoption in commercial and healthcare sectors, with enterprise adoption exceeding 28% in 2024. Technological trends such as bifacial modules, floating solar systems, and AI-enabled tracking solutions are reshaping both regions. Europe follows with a 22% market share, led by Germany, UK, and France, emphasizing sustainability and regulatory compliance. Latin America and the Middle East & Africa account for 12% and 8% of the market, respectively, with increasing government incentives and solar expansion projects driving adoption.

How is enterprise adoption shaping innovative solar solutions in this region?

North America accounts for approximately 25% of the global Solar PV Mounting Systems market in 2024. Key industries driving demand include healthcare, finance, and manufacturing, where large-scale energy efficiency initiatives are implemented. Regulatory support, such as federal tax credits and state-level incentives, has accelerated the deployment of rooftop and ground-mounted systems. Technological advancements include the adoption of AI-based performance monitoring and automated installation solutions, enhancing energy capture by 12–15%. Local players, such as Unirac, are providing pre-assembled mounting kits for commercial projects, reducing installation timelines by up to 20%. Consumer behavior shows higher enterprise adoption, particularly in healthcare and finance, with more than 35% of companies piloting smart solar solutions for sustainability programs.

What drives sustainable adoption of advanced solar solutions across European markets?

Europe accounts for around 22% of the global Solar PV Mounting Systems market, with Germany, the UK, and France leading adoption. Regulatory bodies and sustainability initiatives, including the European Green Deal, are promoting renewable energy deployment. Emerging technologies such as bifacial panels and hybrid fixed-tracking systems are gaining traction. Local players like Clenergy Germany are developing corrosion-resistant mounting structures for utility-scale and rooftop projects. Regional consumer behavior is shaped by regulatory pressure and corporate ESG mandates, with over 30% of enterprises opting for advanced mounting solutions that ensure traceable energy performance and environmental compliance.

Why is Asia-Pacific dominating global solar PV infrastructure development?

Asia-Pacific holds the largest market volume with 42% share in 2024. Top consuming countries include China, India, and Japan, with China alone deploying over 250,000 PV mounting systems in 2024. Infrastructure trends include rapid utility-scale solar farm expansion and increased manufacturing of high-precision components. Technological innovation hubs in Shenzhen and Bangalore focus on automated installation and AI-based tracking systems. Local players, such as Sungrow and Trina Solar, are integrating smart mounting systems with bifacial modules to improve energy yield by 15%. Regional consumer behavior reflects strong industrial and commercial adoption, supported by government incentives and national renewable energy targets.

How are infrastructure projects driving solar adoption in emerging economies?

South America holds approximately 6% of the Solar PV Mounting Systems market. Key countries include Brazil and Argentina, with over 8,000 MW of installed capacity supported by government solar incentives and trade-friendly policies. Infrastructure trends include utility-scale solar farms and commercial rooftop installations. Local players, such as Canadian Solar Latin America, are deploying large ground-mounted systems to maximize energy output. Consumer behavior is influenced by energy cost reduction priorities and local media campaigns promoting renewable adoption, with enterprise adoption in commercial and industrial sectors reaching 28% in 2024.

What regional drivers are accelerating renewable energy adoption in emerging markets?

Middle East & Africa account for roughly 8% of the global Solar PV Mounting Systems market. Major growth countries include UAE and South Africa, focusing on solar energy integration in oil & gas and construction sectors. Technological modernization includes bifacial panels, floating solar, and automated tracking systems. Local regulations and trade partnerships are incentivizing renewable adoption. Regional players, such as Masdar in the UAE, are deploying large-scale solar farms integrated with advanced mounting systems. Consumer behavior reflects sector-specific adoption trends, with higher uptake in industrial and commercial energy projects, where efficiency and sustainability are critical.

China: 28% market share – Dominance driven by high production capacity, large-scale utility deployments, and government-backed solar expansion initiatives.

United States: 25% market share – Strong adoption in commercial and healthcare sectors, combined with federal tax incentives and technological innovation in mounting systems.

The Solar PV Mounting Systems market features a moderately fragmented competitive environment, with approximately 50–60 active global competitors. The top five companies—Nextracker, Array Technologies, GameChange Solar, Arctech, and Schletter Group—collectively hold around 30% of the market. Industry leaders are pursuing strategic initiatives such as joint ventures, co-development of advanced products, acquisitions, and local manufacturing investments to enhance supply chain efficiency and reduce lead times. Innovation trends, including corrosion-resistant materials, modular lightweight designs, and cost-effective installation solutions, are driving competitive differentiation. Companies are also focusing on digital transformation, integrating AI-enabled monitoring and automated installation tools to improve energy capture and operational efficiency. Sustainability initiatives and regulatory compliance further influence competition, with players adopting eco-friendly materials and systems to meet ESG requirements. The combination of technological advancements, strategic partnerships, and regional expansion is shaping a competitive landscape where companies strive to secure market leadership and address the growing demand for solar energy infrastructure.

Schletter Group

Soltec

GameChange Solar

K2 Systems

Unirac

PV Hardware

Clenergy

First Solar

The Solar PV Mounting Systems market is witnessing rapid technological evolution aimed at improving efficiency, durability, and energy output. Bifacial solar modules combined with single-axis tracking systems are now widely deployed, enhancing energy capture by utilizing both sides of the panel while following the sun’s path. In the United States, 94% of new utility-scale PV installations in 2022 integrated single-axis trackers, highlighting widespread adoption. Floating photovoltaic (FPV) systems are emerging as a key innovation, installed on reservoirs and water bodies to optimize space utilization and improve cooling efficiency. FPV systems can increase panel efficiency by 0.6% to 4.4% compared to land-based installations.

Smart mounting systems leveraging AI are transforming operational efficiency. These systems adjust panel angles based on weather forecasts to maximize energy yield and mitigate damage from extreme conditions such as hailstorms. Certain AI-enabled trackers now automatically shift panels into stow mode during severe weather, reducing downtime and operational losses. Material innovations are also reshaping the market. Lightweight, corrosion-resistant aluminum and advanced composite materials are increasingly used for mounting structures, reducing transport and installation complexity while extending system longevity. Modular pre-assembled components further enhance deployment speed, particularly in utility-scale and commercial projects.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In April 2024, Tata Power Solar commissioned SJVN's 1000 MW solar project in Rajasthan, India. The project installed over 2.1 million solar modules, expected to generate approximately 2,500 million units of electricity annually, significantly contributing to regional renewable energy capacity. Source: www.tatapowersolar.com

In March 2024, K2 Systems launched the GreenRoof Vento, a green roof PV mounting system designed for modules 1,400 mm to 2,400 mm in length. The system provides adjustable elevation between 10° and 15°, enabling efficient urban solar deployment. Source: www.k2-systems.com

In January 2023, Valmont Industries and Convert Italia launched the Convert Single Axis Tracker under Valmont Solar, enhancing energy efficiency by 25% in commercial and utility-scale projects, reflecting the industry's emphasis on high-performance mounting solutions. Source: www.valmont.com

The Solar PV Mounting Systems Market Report offers a detailed assessment of global and regional market landscapes, covering all key segments including fixed and tracking systems, rooftop and ground-mounted solutions, and floating solar installations. The report examines residential, commercial, and utility-scale applications, highlighting the role of technological innovations such as bifacial modules, AI-enabled smart trackers, and modular pre-assembled mounting solutions in improving operational efficiency and energy yield.

Geographical analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing insights into regulatory frameworks, incentives, infrastructure trends, and consumer adoption behavior. Material trends, including lightweight aluminum, corrosion-resistant composites, and sustainable components, are evaluated for their impact on system longevity and cost-effectiveness.

The report also explores niche and emerging markets, including floating solar, urban green roof installations, and industrial integration projects. Strategic insights on regional adoption patterns, technological integration, and end-user behavior make the report an essential guide for decision-makers seeking to understand opportunities, competitive dynamics, and future pathways in the Solar PV Mounting Systems market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 14599.19 Million |

|

Market Revenue in 2032 |

USD 35379.69 Million |

|

CAGR (2025 - 2032) |

11.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nextracker, Array Technologies, Arctech, Schletter Group, Soltec, GameChange Solar, K2 Systems, Unirac, PV Hardware, Clenergy, First Solar |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |