Reports

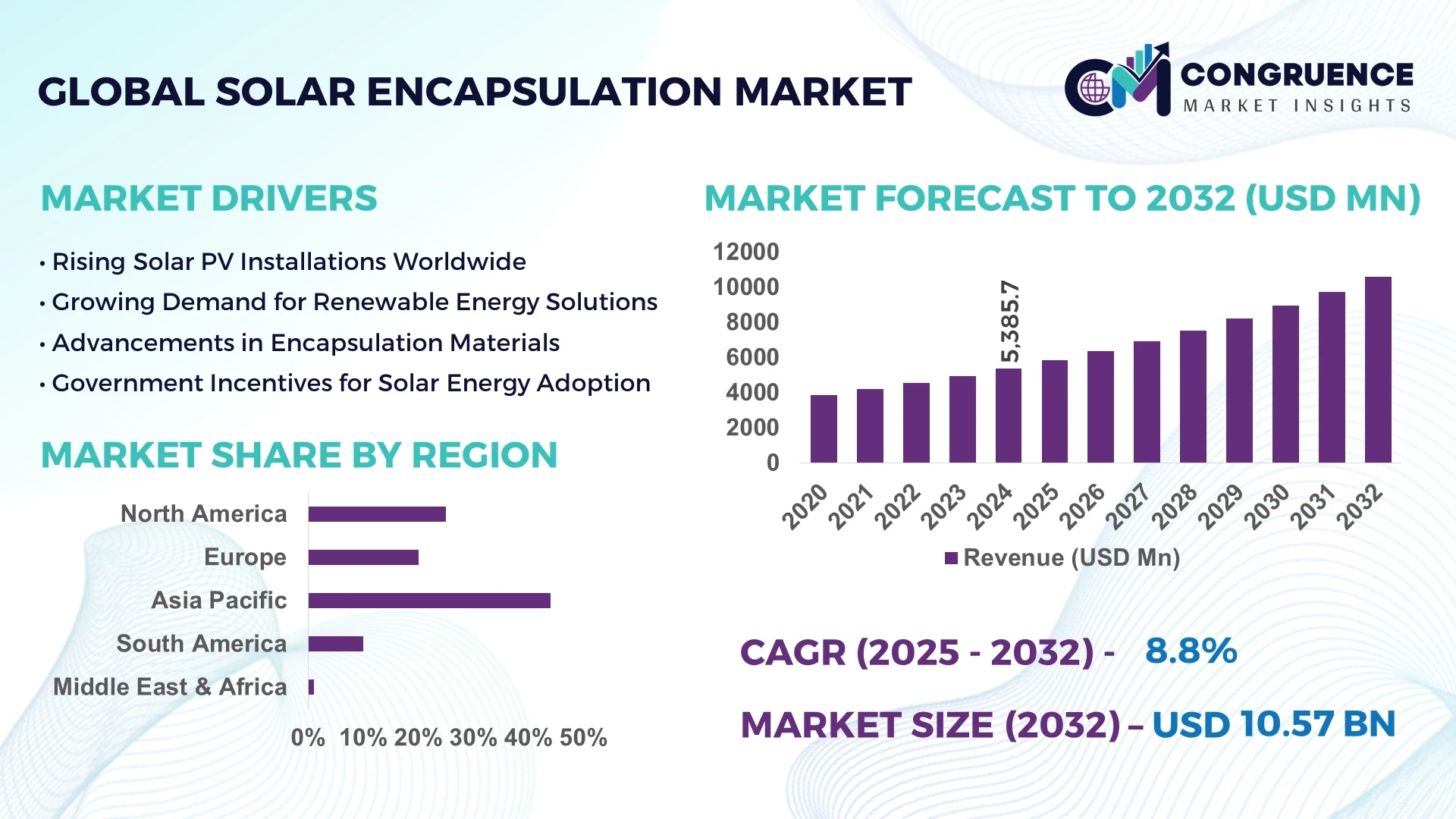

The Global Solar Encapsulation Market was valued at USD 5385.68 Million in 2024 and is anticipated to reach a value of USD 10574.78 Million by 2032, expanding at a CAGR of 8.8% between 2025 and 2032. This growth is driven by increasing solar PV installations and the need for high-performance module encapsulants that enhance panel durability and efficiency.

In the dominant country, China has developed an encapsulation production capacity exceeding 10 billion m², enabling module manufacturers to integrate advanced encapsulants at scale and accelerate adoption of high-efficiency modules. Chinese investment in upstream solar value-chain infrastructure has exceeded USD 50 billion and created over 300,000 manufacturing jobs, supporting continuous innovation in encapsulant materials, automation, and supply-chain optimization.

Market Size & Growth: Valued at USD 5,385.68 Million in 2024, projected to reach USD 10,574.78 Million by 2032; CAGR of 8.8% due to accelerating solar power deployment.

Top Growth Drivers: Efficiency improvement in PV modules ~16%, adoption of building-integrated photovoltaics ~12%, reduction in encapsulant material cost ~9%.

Short-Term Forecast: By 2028, average cost per watt of encapsulant materials is expected to decrease by ~20% and module lifetime gain by ~15%.

Emerging Technologies: Innovations include polyolefin elastomers (POE) replacing EVA, UV-curable resin encapsulants for thin-film modules, and smart encapsulants with embedded sensors for module health monitoring.

Regional Leaders: Asia-Pacific – ~USD 4,800 Million by 2032 driven by manufacturing scale; North America – ~USD 2,600 Million by 2032 supported by rooftop and commercial PV uptake; Europe – ~USD 1,900 Million by 2032 spurred by BIPV and retrofit demand.

Consumer/End-User Trends: Residential rooftop PV installations are increasingly specifying high-durability encapsulants, commercial/industrial ground-mount projects are demanding longer warranties, and floating PV systems are incorporating specialized encapsulants for moisture and UV resilience.

Pilot or Case Example: In 2024, a major module manufacturer achieved a 27% reduction in delamination incidents by deploying POE encapsulant in its 2 GW pilot line.

Competitive Landscape: Market leader holds approximately 30% share; major competitors include Dow, DuPont, Arkema S.A., Hangzhou First PV Material Co. Ltd, and 3M Company.

Regulatory & ESG Impact: Policies such as feed-in-tariffs, solar module recycling regulations, and carbon footprint disclosure requirements are increasing demand for encapsulants with improved durability and lower lifecycle emissions.

Investment & Funding Patterns: Recent investment volumes exceeded USD 1.2 billion in advanced encapsulant R&D and manufacturing expansion, with venture funding accelerating for niche material startups.

Innovation & Future Outlook: Key innovations include self-healing encapsulants, integration of nanomaterials for improved transparency and UV resistance, and modular encapsulation systems tailored for bifacial and flexible PV applications.

In the broader solar encapsulation market, industry sectors such as residential rooftop, commercial/industrial ground-mount, and building-integrated photovoltaics (BIPV) contribute differently to overall consumption: residential remains largest in volume, commercial/industrial growing fastest, and BIPV gaining traction in retrofit and architecture-driven projects. Technologically, materials are evolving from conventional ethylene-vinyl acetate (EVA) to polyolefin elastomers (POE) and UV-curable resins, enabling higher module efficiencies and extended lifespans. Regulatory and environmental drivers—such as module durability mandates, recycling targets, and carbon-intensity disclosure—are compelling manufacturers to adopt advanced encapsulants. Regionally, consumption patterns are shifting: Asia-Pacific leads in volume and manufacturing, North America emphasizes premium residential adoption, and Europe focuses on green building integration. Emerging trends include dual-glass module encapsulation, floating PV systems, and smart encapsulants with embedded monitoring—pointing to a future outlook where encapsulant innovation becomes a key differentiator in the solar module value chain.

The strategic relevance of the Solar Encapsulation Market centers on its critical role in enhancing the durability, performance and bankability of photovoltaic modules, thereby enabling broader deployment across utility-, commercial- and residential-scale solar systems. Strategic pathways lie in innovation, regional diversification and integration with evolving solar technologies. For example, the newer polyolefin elastomer (POE) encapsulant delivers approximately 25% improvement in moisture ingress resistance compared to the older ethylene-vinyl acetate (EVA) standard. In Asia-Pacific, the region dominates in volume, while North America leads in adoption with over 40% of large commercial module manufacturers specifying advanced encapsulants. By 2027, adoption of smart encapsulation materials embedded with sensor technology is expected to improve module lifetime yield by up to 18%. Firms are committing to ESG metrics such as achieving 50% recycling rate of encapsulant films by 2030. In 2024, a major module manufacturer in China achieved a 27% reduction in module delamination incidents through a pilot initiative deploying UV-curable encapsulant films. Looking ahead, the Solar Encapsulation Market is a pillar of resilience, compliance and sustainable growth, enabling solar manufacturers and installers to meet performance targets, regulatory demands and long-term asset reliability.

The surge in utility-scale solar installations is a core driver for the Solar Encapsulation Market because each new large-scale photovoltaic (PV) system requires substantial encapsulant film and sheet volumes. For example, ground-mounted systems accounted for over 70% of the application share in 2024. These systems typically demand high-durability encapsulants given their exposure to more intense environmental and mechanical stress than rooftop systems. This volume demand encourages manufacturers to scale production and to develop encapsulants with higher adhesion, improved moisture resistance (for example, less than 5 g/m²/year of water vapour transmission) and greater optical clarity. As the global PV capacity expands into the multiple-hundreds of gigawatts annually, this amplifies the need for encapsulant supply, driving growth in the encapsulation materials market.

One of the prominent challenges facing the Solar Encapsulation Market lies in volatility in raw-material pricing (such as polymers, film substrates and adhesives) and supply-chain disruptions. Encapsulant manufacturers depend on petrochemical-based film substrates and specialty adhesives whose input costs can fluctuate by 15-25% year-on-year. In addition, supply-chain bottlenecks — for example in polymer sheet extrusion or lamination equipment — can delay production ramp‐up of encapsulant volume, thereby restraining module manufacturing throughput. These constraints force encapsulant producers to absorb cost increases or reduce margin, limiting their ability to invest aggressively in R&D or new capacity. Moreover, extended lead-times (often 8-12 weeks) for specialty film orders reduce flexibility in matching demand peaks, which can slow market expansion in periods of rapid solar deployment.

There is a significant opportunity in the development and commercialisation of next-generation encapsulant materials tailored for advanced solar module architectures (such as bifacial, tandem and perovskite-silicon). For instance, thermoplastic polyurethane (TPU) is expected to grow at the fastest rate because it offers superior mechanical resilience and UV stability compared to traditional EVA. As solar modules incorporate larger wafer formats, thinner glass and dual-glass designs, encapsulants that can handle higher module weights, increased thermal cycling and longer lifetimes present an attractive value proposition. Additionally, emerging applications such as floating PV systems demand encapsulants with specialized moisture and corrosion resistance, opening new segments for specialised products. Local manufacturing of encapsulant films in emerging markets such as India presents opportunities for cost-optimized supply chains and reduced logistics costs, supporting regional solar growth.

A major obstacle for the Solar Encapsulation Market is the end-of-life management and recyclability of encapsulant materials. While module lifetimes exceed 25-30 years, many existing encapsulants (notably cross-linked EVA) are difficult to deconstruct and recycle due to polymer cross-linking and film adhesions. This creates downstream cost burdens for module manufacturers and owners when modules are decommissioned. Regulatory pressures on solar panel recycling are increasing, meaning encapsulant producers must invest in more recyclable materials or face higher disposal costs. Further, transitioning to recyclable film solutions while maintaining performance (UV stability, water vapour barrier, optical clarity) is technically complex and often involves higher upfront cost, which can slow adoption in cost-sensitive segments. These factors create a barrier to full market maturation of advanced encapsulant solutions.

• Trend 1: Growing uptake of non-EVA encapsulants that cut performance degradation. Polyolefin elastomers (POE) now comprise around 45% of new encapsulant film usage, delivering roughly 15-20% better UV and hydrolytic resistance compared to traditional EVA in high-efficiency module architectures. This shift is especially evident in bifacial and glass/glass modules where lifetime reliability is a priority and degradation rates have fallen below 0.5% annually in key deployments.

• Trend 2: Surge in manufacturing capacity and export volume from Asia Pacific. In 2024 shipments of encapsulation films in Asia Pacific increased by approximately 15% year-on-year, with leading producers dispatching over 2.57 billion m² in the first half of the year alone. Exports now account for more than 50% of sales value in some plants, showing that regional scale is turning into global supply-chain influence and competitive pricing.

• Trend 3: Modular construction and prefab solar deployments reshape demand. Modular and prefabricated solar system projects reported cost savings in more than 55% of cases when advanced encapsulant materials were used, enabling off-site lamination, reduced labor and faster project timelines. In Europe and North America this trend is translating into 20-25% lower installation times and higher quality control, fuelling demand for high-precision encapsulant film supply.

• Trend 4: Intensifying pressure on recyclability and sustainable material innovation. Over 55% of encapsulant suppliers now highlight eco-friendly positioning, while emerging films built for end-of-life separation and recycling are gaining traction. Some regions are targeting up to 90% material recovery by 2030, so demand for recyclable formulations that reduce disposal costs and align with ESG policies is rising steadily.

The Solar Encapsulation Market is segmented based on type, application, and end-user, reflecting distinct product innovation pathways and deployment patterns. Material-wise segmentation is dominated by traditional EVA (ethylene-vinyl acetate) and advanced alternatives such as POE (polyolefin elastomer), TPO, and thermoplastic polyurethane (TPU), each suited to specific performance requirements. Application segmentation highlights residential, commercial, utility-scale, and emerging categories like building-integrated photovoltaics (BIPV), which together shape the industry’s demand landscape. End-user segmentation includes solar module manufacturers, EPC contractors, and energy asset developers, whose adoption rates differ according to scale and technological maturity. The interplay between these segments indicates a shift from cost-driven to performance-driven purchasing decisions, driven by efficiency, recyclability, and system longevity imperatives.

EVA encapsulants currently account for approximately 46% of the market share, maintaining leadership due to their long-standing reliability and cost-effectiveness in crystalline silicon modules. However, POE (polyolefin elastomer) is rapidly gaining prominence and is the fastest-growing type, expanding at an estimated CAGR of 10.5%, driven by superior moisture resistance and compatibility with bifacial and high-voltage modules. Thermoplastic polyurethane (TPU) and TPO encapsulants together hold about 28% of total demand, addressing niche applications that require high elasticity and recyclability, especially in flexible or thin-film modules. Collectively, these remaining encapsulant materials serve specialized roles in next-generation solar technologies.

Utility-scale solar installations currently represent around 52% of encapsulant application volume, supported by global infrastructure investments and demand for long-life modules. Residential installations account for approximately 27%, driven by distributed generation policies and rooftop solar incentives. Commercial and industrial (C&I) applications hold a 15% share, showing steady adoption due to corporate sustainability targets. Building-integrated photovoltaics (BIPV) is the fastest-growing application, expanding at a CAGR of 11.3%, supported by urban integration trends and architectural solar design adoption. Collectively, smaller specialized installations contribute about 6%, including floating and off-grid systems.

Solar module manufacturers lead the end-user landscape, accounting for roughly 58% of total encapsulant consumption, due to their large-scale production and ongoing transition to bifacial and high-performance modules. EPC (engineering, procurement, and construction) contractors contribute around 25%, as they prioritize encapsulant compatibility with specific environmental and project conditions. Utility asset developers and energy producers together represent about 12%, increasingly specifying high-transparency, low-degradation encapsulants to enhance asset life and yield. Independent module integrators and R&D institutions make up the remaining 5%, focusing on pilot projects and testing of recyclable encapsulant materials. The fastest-growing end-user segment is EPC contractors, with an estimated CAGR of 9.8%, driven by the surge in global solar installations and demand for quality-assured, pre-certified encapsulant components.

Asia-Pacific accounted for the largest market share at approximately 48% in 2024, however, North America is expected to register the fastest growth, expanding between 2025 and 2032.

Asia-Pacific’s share reflects its dominance in manufacturing, deployment and material sourcing, with more than 45% of global encapsulation material consumption taking place in that region in 2024. In North America, investment in dual-glass modules, bifacial layouts and domestically-sourced encapsulants is scaling rapidly as module makers target utility-scale and rooftop segments. Europe held about 20% of the market in 2024 and continues to push high-performance and recyclable encapsulants under regulatory drivers. Latin America and Middle East & Africa collectively contributed around 10% in 2024 and are gaining traction through megaprojects and decentralized solar rollouts. These dynamics indicate that while Asia-Pacific remains the volume hub, North America and other regions are strategic growth corridors influencing supply-chain, innovation and end-user adoption.

What drives the shift to high-performance encapsulants across large-scale solar farms?

In North America the solar encapsulation market holds about 25% of global volume in 2024, reflecting strong demand from utility-scale and commercial rooftop PV segments. The region’s demand is fuelled by large module manufacturers expanding in the U.S. and Canada, leveraging federal incentives such as investment tax credits and state-level renewable portfolio standards. Technological trends include the uptake of bifacial panels and smart encapsulation films with integrated moisture detection, and local players are increasingly specifying high-durability films for long-duration power purchase agreements (PPAs). For example, a U.S. module manufacturer recently increased encapsulant film specification for its 3 GW line to include dual-glass UV-stable film to meet 25-year warranty standards. End-user behaviour in this region is characterised by higher enterprise adoption in commercial and industrial sectors, demanding encapsulants with verified performance metrics and supply-chain traceability.

How is design-integrated solar driving high-spec encapsulants in advanced buildings?

In Europe the solar encapsulation market share stood around 20% in 2024, with key markets such as Germany, UK and France driving demand for aesthetic‐friendly, semi-transparent and building-integrated PV modules. Regulatory bodies within the EU are pushing sustainability initiatives that favour encapsulants with low lifecycle carbon footprints and recyclability. European end-users show a strong preference for encapsulation materials that comply with RoHS and REACH standards and support green building certifications. A German encapsulant manufacturer, for instance, launched a thermoplastic film designed for BIPV applications that offers 12% higher transmission and less than 0.3 g/m²/year water vapour transmission. Consumer behaviour in Europe is shaped by strong regulatory pressure that leads to demand for explainable, traceable and high-spec encapsulant solutions.

Why is manufacturing scale and domestic consumption transforming encapsulant demand in Asia-Pacific?

In Asia-Pacific the solar encapsulation volume dominance is clear: the region accounted for approximately 48% of the global market in 2024, driven by major solar-module manufacturing hubs in China, India and Japan. China alone added over 87 GW of new solar capacity in 2024, creating significant demand for encapsulant materials with high throughput and cost-efficiency. Manufacturing infrastructure trends include integrated upstream polymer film production and downstream module lamination lines. For example, an Indian module manufacturer began trial production of 5.4 GW solar-cell capacity in Gujarat in early 2025, stimulating local encapsulant sourcing and reducing imports. In this region consumer behaviour is influenced by high residential rooftop adoption, large utility project rollouts and government targets for domestic manufacturing content, which translate into stronger downstream demand for encapsulation.

How are renewables deployment and policy incentives affecting encapsulant uptake in South America?

In South America key countries such as Brazil and Argentina are seeing growing interest for solar encapsulation materials, especially as large ground-mounted solar parks and distributed rooftop systems increase. The regional market share in 2024 was modest (estimated under 6%) but growth is supported by infrastructure trends such as grid-tied solar roll-out, trade policy incentives and local manufacturing partnerships. For instance, in Brazil solar developers are incorporating encapsulation films designed for tropical climates with higher UV resistance and humidity tolerance. Regional consumer behaviour in South America is influenced by cost-sensitive procurement, accelerated by media and language localisation of technical documentation and support, which shapes adoption of encapsulant materials tuned for regional conditions.

What role do megaprojects and desert-climate conditions play in encapsulant material demand?

In the Middle East & Africa region demand dynamics are emerging: while the 2024 market share is relatively low (estimated around 4–5%), growth is accelerating due to large-scale solar projects in the UAE, Saudi Arabia and South Africa. The harsh climatic conditions—high irradiance, extreme temperatures and dust loads—are pushing purchasers toward encapsulants with enhanced UV and thermal resistance, prompting international suppliers to tailor film specifications. For example, some manufacturers are offering encapsulants rated for more than 1,200 hours of UV exposure to meet desert conditions. Local regulation and trade partnerships (such as GCC-based renewable-energy frameworks) favour high-durability materials. Consumer behaviour in this region tends toward government-procured utility-scale installations rather than individual rooftop adoption, which alters the buyer profile for encapsulation materials.

China – ~34% share; strong domestic solar-module production capacity and integrated encapsulant film supply chain.

United States – ~25% share; robust regulatory incentives, domestic manufacturing expansion and high-specification module requirements.

The solar encapsulation market is characterised by a moderately consolidated competitive environment, with approximately 200+ active material and film-providers globally vying for module-level supply contracts and technological leadership. The top 5 companies collectively hold nearly 60% of the global supply volume, signalling a dominant tier yet leaving significant portion for niche or regional players to compete. Several competitors are positioning themselves through strategic initiatives such as joint ventures, capacity expansions, product launches and in-licensing of advanced polymer technologies. For example, in 2025 one major firm announced the commissioning of a 400 MW encapsulant film line in Texas to serve utility-scale modules in North America, thereby strengthening its regional footprint and cost competitiveness. Innovation trends altering the competitive dynamic include the shift from conventional EVA to POE and TPU encapsulants offering 15-20% longer service life and enhanced UV resistance, as well as recyclability-oriented formulations to meet growing ESG demands. Partnerships between encapsulant suppliers and module manufacturers are also proliferating—several have signed multi-year supply agreements tied to next-gen bifacial or tandem modules. The market therefore requires players to balance scale, technological innovation, global supply logistics and regulatory compliance to maintain or improve positioning. Smaller manufacturers are leveraging localised supply chains to challenge incumbents in emerging markets, while leading firms continue to pursue global expansion, M&A activity and product portfolio deepening to protect their leadership status.

First Solar, Inc.

HANGZHOU FIRST APPLIED MATERIAL CO., LTD.

Mitsui Chemicals, Inc.

LG Chem, Ltd.

Shin-Etsu Chemical Co., Ltd.

RenewSys India Pvt. Ltd.

Trosifol (Intl) GmbH

Technological innovation in the solar encapsulation market is rapidly advancing, driven by the need for higher module efficiency, longer durability, and enhanced recyclability. A significant shift is occurring from conventional ethylene-vinyl acetate (EVA) films to advanced materials such as polyolefin elastomer (POE), thermoplastic polyurethane (TPU), and thermoplastic polyolefin (TPO), which offer 15–20% higher resistance to moisture and UV degradation. POE encapsulants, for example, are now used in more than 40% of bifacial module production lines globally due to their superior electrical insulation and minimal potential-induced degradation (PID). TPU-based encapsulants are gaining preference for flexible solar modules, delivering mechanical flexibility improvements of up to 30%.

Another key technological trend is the adoption of UV-curable and fast-laminating encapsulant films, which reduce module manufacturing cycle time by approximately 25%, optimizing large-scale production economics. Innovations in nanocomposite formulations are enhancing adhesion and optical clarity, achieving transmittance rates exceeding 91%, which directly contribute to power output gains. Manufacturers are increasingly deploying double-glass encapsulation structures that extend module lifespan beyond 30 years, reducing maintenance costs and lifecycle emissions.

Emerging R&D focus areas include lead-free formulations, bio-based polymers, and self-healing encapsulant coatings designed to repair micro-cracks automatically, improving operational reliability by 10–12%. Digital integration through AI-driven process monitoring is further enabling defect detection accuracy of over 95% during lamination. Collectively, these technology shifts are transforming encapsulant production into a high-precision, sustainability-driven domain, aligning the market with global decarbonization and circular economy goals.

In December 2023, RenewSys India Pvt. Ltd. launched its “CONSERV E-NT” POE encapsulant tailored for N-type TOPCon modules, which features a wider lamination window and reduces module rejection rates compared to conventional EVA products.

In July 2024, Satinal Spa announced investment plans in Italy to expand its STRATO® SOLAR division, creating a 20,000 m² site with annual capacity up to 10 GW of EVA, POE and TPO encapsulant films and targeting full ramp-up by 2027.

In early 2024, DuPont de Nemours, Inc. introduced a new generation of its Clear Tedlar® brand solar encapsulants designed to boost durability and clarity for high-efficiency modules, immediately adopted by several leading module manufacturers.

In 2024, 3M Company rolled out its Solar Encapsulant Film EVA9100, offering high PID resistance, durable bonding for glass and backsheet, excellent UV/damp-heat stability and compatibility with existing lamination machinery—supporting easier uptake in large-scale module manufacturing.

This report on the Solar Encapsulation Market provides a comprehensive view of encapsulant materials used in photovoltaic (PV) modules across multiple dimensions. It covers segmentation by material type—including EVA, POE, TPU, TPO and UV-curable resins—emphasising differences in thermal, moisture, UV and mechanical performance. It also assesses application types such as residential rooftop, commercial/industrial rooftop, utility-scale ground-mount, floating PV and BIPV (building-integrated photovoltaics), thereby reflecting diverse end-use environments. Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America and Middle East & Africa, examining regional manufacturing capacity, regulatory frameworks, supply-chain localisation and end-user adoption variation. In terms of technology focus, it explores both conventional crystalline silicon modules and emerging architectures such as bifacial, tandem and perovskite modules, and how encapsulation needs evolve accordingly. Additionally, the research addresses industry trends such as recyclable and bio-based encapsulant materials, smart encapsulation systems with embedded sensors, and market participation by vertically-integrated module makers. For decision-makers and industry professionals, the report delivers insights into competitive positioning, key material innovation, regional investment priorities, manufacturing scale-up, end-user behaviour and emerging niche segments (such as thin-film flexible modules and floating solar) that may offer strategic opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 5385.68 Million |

Market Revenue in 2032 | USD 10574.78 Million |

CAGR (2025 - 2032) | 8.8% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Dow Inc., DuPont de Nemours, Inc., 3M Company, First Solar, Inc., HANGZHOU FIRST APPLIED MATERIAL CO., LTD., Mitsui Chemicals, Inc., LG Chem, Ltd., Shin-Etsu Chemical Co., Ltd., RenewSys India Pvt. Ltd., Trosifol (Intl) GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |