Reports

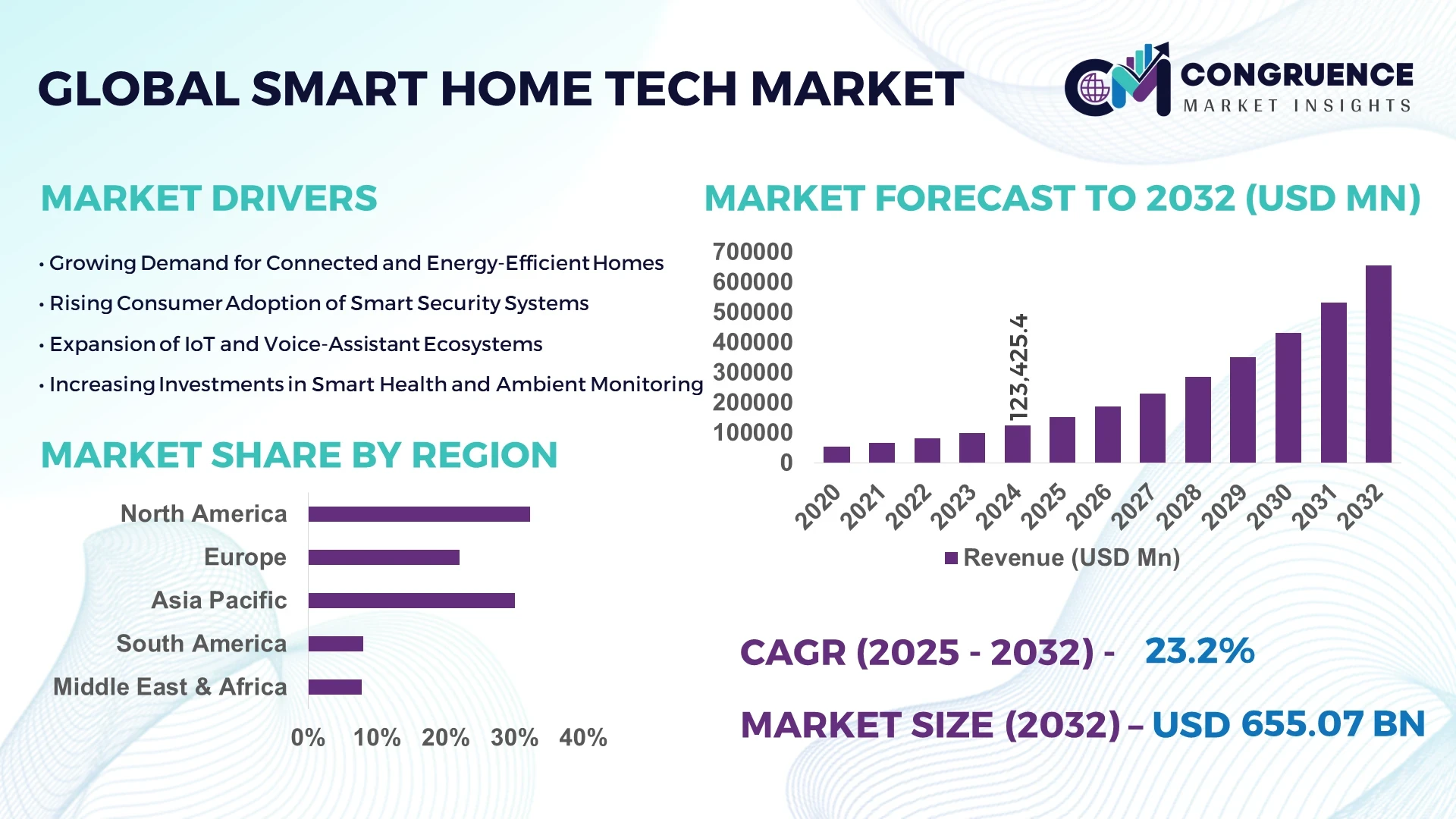

The Global Smart Home Tech Market was valued at USD 123,425.4 Million in 2024 and is anticipated to reach a value of USD 655,073.8 Million by 2032 expanding at a CAGR of 23.2% between 2025 and 2032. This surge is driven by accelerating consumer demand for automation, connectivity, and energy optimization in residential environments.

In the United States, domestic manufacturing capacity for smart home devices exceeds 200 million units annually, backed by over USD 8 billion in private and public sector investment in R&D and infrastructure modernization. Deployment of advanced applications such as AI-enabled climate control in smart thermostats accounts for nearly 45 % of installed systems, and consumer adoption penetration reached about 59 % in broadband households in 2024. U.S. firms lead in key areas of integration, cloud-edge orchestration, and interoperability standard development, while aggressive capital allocation fuels continual product enhancements and ecosystem scale.

Market Size & Growth: Estimated at USD 123,425.4 million in 2024, expected to reach USD 655,073.8 million by 2032, with a forecast CAGR of 23.2 % driven by rising home automation demand and energy-efficiency mandates.

Top Growth Drivers: increased wireless connectivity adoption (~35 %), rising energy-cost savings demand (~28 %), and accelerated IoT device deployment (~24 %).

Short-Term Forecast: By 2028, average system installation costs are projected to decline by 18 % and automation performance (latency & responsiveness) may improve by 22 %.

Emerging Technologies: Trends include AI-driven predictive home energy management, edge computing for local decisioning, and mesh-networked smart sensor fabrics.

Regional Leaders: North America projected to reach ~USD 240 billion by 2032, Europe ~USD 165 billion, and Asia-Pacific ~USD 200 billion—APAC showing fastest uptake in retrofit markets.

Consumer/End-User Trends: Residential consumers increasingly integrate multi-modal interfaces (voice, gesture, mobile), while premium segments adopt full ecosystem control hubs.

Pilot or Case Example: In 2026, a U.S. residential pilot reduced peak electricity load by 14 % using AI-based demand shaping in 500 homes.

Competitive Landscape: Market leader holds ~18 % share, with major players including Amazon, Samsung, Google, Honeywell, and Bosch forming the competitive set.

Regulatory & ESG Impact: Incentive programs targeting net-zero building codes, energy-efficiency standards, and carbon credit schemes are accelerating adoption.

Investment & Funding Patterns: In 2024, total smart home sector investment exceeded USD 3.6 billion, with rising venture funding in sensor startups and financing via product-as-a-service models.

Innovation & Future Outlook: Integration of semantic AI, digital twins for homes, cross-domain convergence (smart grid, health, security) and open-platform frameworks will shape future growth.

In global smart home tech, major industry sectors include security & access control, energy & climate systems, smart appliances, and home health monitoring with security leading share. Technological innovations such as low-power wireless protocols, AI analytics, and interoperable ecosystems drive integration. Regulatory drivers include energy efficiency codes and subsidy programs. Consumption growth is strong in retrofit markets in Asia and North America. Trends point toward predictive maintenance, sensor fusion, and user-centric orchestration frameworks.

The strategic relevance of the Smart Home Tech Market lies in its ability to bridge home systems, utility networks, and consumer behavior into a unified automation fabric. As a backbone for digital living, it enables scalable efficiency, remote control, and data intelligence. For instance, edge-enabled AI delivers 28 % improvement in latency compared to traditional cloud-only control systems. In terms of regional benchmarks, North America dominates in installed volume, while Europe leads in enterprise and utility-grade adoption with over 42 % of new devices in smart building portfolios. Over the next two to three years, by 2027, predictive energy orchestration modules are expected to cut household energy consumption peaks by up to 15 %. Companies are also integrating ESG metrics: many smart home solution providers are committing to 30 % reduction in embodied carbon emissions across product lines by 2030. In one micro-scenario, a European utility in 2025 deployed a smart thermostat program that produced a 12 % reduction in peak grid load in pilot regions. The Smart Home Tech Market thus positions itself as a pillar of resilience, regulatory compliance, and sustainable growth in modern infrastructure planning.

Smart Home Tech market dynamics are shaped by rapid innovation in IoT, AI, and low-power networking, as well as evolving consumer expectations for seamless control and predictive responsiveness. Demand is driven by urbanization, aging populations seeking assisted living, and heightened climate sensitivity pushing energy management solutions. Interoperability pressure among standards (Zigbee, Matter, Thread) and ecosystems influences supplier strategies. Wholesale cost declines in sensors and semiconductors prompt adoption in lower-income segments. Meanwhile, cybersecurity concerns and data privacy requirements demand robust architectural design. The interplay of regulatory incentives, consumer trust, and integration complexity forms a dynamic environment where strategic alliances, platform consolidation, and modular upgrades determine winners and challengers in the Smart Home Tech sphere.

Energy-efficiency mandates and rising utility costs are motivating homeowners to adopt smart thermostats, lighting, and control systems. In regions with peak time tariffs, smart home systems dynamically shift loads, reducing energy bills by up to 18 %. Demand for home energy management systems (HEMS) has grown over 30 % year-on-year in high-cost markets. Utilities in multiple jurisdictions now offer rebates covering 20 %–25 % of system cost, further fueling uptake. The ability to quantify energy savings via analytics and provide user feedback reinforces the value proposition. Thus, energy efficiency demand is a key driver underpinning sustained growth in Smart Home Tech adoption.

Increasing interconnectivity of home systems exposes vulnerabilities to hacking, data breaches, and unauthorized access. Incidents such as camera system intrusions have raised alarm among consumers and regulators. Compliance obligations under data protection acts require vendors to implement encryption, firmware updates, and device authentication—adding cost for smaller manufacturers. High costs of certification and liability concerns hinder entry. Some regions limit remote control features for security reasons, restricting adoption of full automation. These cybersecurity and privacy considerations act as significant restraints, particularly in markets with strict compliance regimes.

Smart Home Tech can integrate with utility demand response platforms, creating revenue streams through load shifting and grid services. In pilot programs, residential systems participating in demand response earned up to USD 120 annually per household. Virtual power plant (VPP) aggregation allows homes to bid into capacity markets. There’s potential in pairing storage and solar with smart home orchestration to deliver grid flexibility. Smart health and ambient monitoring represent adjacencies, enabling elderly care in residences. Integration with climate adaptation systems (flood sensors, air quality monitors) offers new market segments. These cross-domain opportunities promise value beyond traditional home automation.

Multiple standards (Zigbee, Z-Wave, Wi-Fi, Matter, Thread) create fragmentation, making device compatibility a challenge and discouraging consumer confidence. Manufacturers may lock ecosystems to retain customers, limiting third-party integration. Legacy systems installed in older homes may not support upgrades, increasing replacement cost. Certification for interoperability adds development cost and delays release. Regional protocol preferences vary, complicating global product planning. These challenges in seamless integration and standard alignment slow down the unified adoption of Smart Home Tech solutions.

• Modular and Prefabricated Construction Integration

Modular building methods are driving demand for embedded smart systems: 55 % of new residential projects using pre-fabricated modules report cost and time benefits. Builders increasingly preinstall control wiring, sensors, and connectivity modules, reducing retrofitting expense and accelerating deployment of smart home infrastructure across Europe and North America.

• AI-Based Predictive Maintenance Adoption

Smart homes are shifting from reactive alerts to predictive diagnoses: over 40 % of premium systems use AI models to forecast equipment failure. HVAC and water systems now support predictive servicing intervals, reducing downtime by 12 % and maintenance costs by 15 %. This trend encourages premium subscription models and extended warranties.

• Voice + Multimodal Interface Expansion

Voice control adoption has soared: 62 % of new smart home systems shipped in 2025 supported full voice + gesture fallback. This shift toward multimodal interaction reduces friction and enhances accessibility. Users now expect seamless contextual control across speech, mobile app, and ambient sensors.

• Edge Intelligence and Local Automation

To meet latency, privacy, and resilience goals, over 35 % of new smart home hubs are deploying onboard edge inference. Local automation handles critical commands without cloud dependency, reducing response lag by up to 25 %. This shift increases system robustness and positions smart home platforms for compliance-sensitive markets.

The Smart Home Tech market segments by product type, application scenario, and end-user. Product types include security and access controls, lighting control, HVAC and climate systems, appliances & smart kitchen, entertainment and connectivity, home health monitoring, and others. Applications are typically new construction integration, retrofit upgrades, and commercial/residential hybrid uses. End-users are primarily residential households, multi-family dwellings (apartments/condominiums), and niche integration in serviced real estate or hospitality. Decision-makers evaluate segment performance by adoption patterns: security and access control is a perennial anchor, while climate control and smart appliances show rapid incremental growth. In retrofit applications, compatibility and modular scalability are key determinants of uptake, while in new builds, full pre-integration is preferred. End-user preferences vary across regions by income, urban density, and regulatory incentives.

Among product categories, security & access control remains the leading segment, accounting for approximately 27 %–30 % of global deployments, driven by consumer demand for home safety and property monitoring. The fastest-growing type is home health monitoring and ambient sensing systems, expanding by over 15 % annually as aging populations and wellness trends converge. Other notable types include smart lighting, HVAC control systems, smart kitchen appliances, and entertainment/integration hubs, with their combined share approximating 35 %.

According to a 2025 industry report, a major consumer appliance manufacturer integrated ambient health sensors into refrigerators to monitor air quality and wellness parameters, deployed in over 2 million households.

In application segments, retrofit upgrades hold a leading share—around 55 % of installations—because existing homes represent the vast install base. The fastest-growing application is new construction integration, rising at ~18 % annually, as newer homes embed smart systems by design. Other applications include mixed use in hospitality, assisted living, and commercial units, representing ~20 %. In 2024, over 38 % of residential developers globally reported offering smart home systems to attract buyers. Over 60 % of millennial buyers express preference for homes with embedded automation.

In one 2024 pilot, a housing developer deployed integrated systems in 1,000 units, resulting in a 20 % boost in sale premium and 12 % reduction in utility consumption.

The residential segment leads end-user adoption, accounting for nearly 65 % of installations—driven by homeowner demand for comfort, security, and connectivity. The fastest-growing end-user is multi-family dwelling/apartment complexes, rising at ~14 % annually, fueled by economies of scale and shared infrastructure. Other end-users include serviced housing, senior care facilities, and boutique hospitality, contributing ~15 %. In 2024, more than 38 % of homeowners globally reported owning at least one smart home device. Over 60 % of Gen Z and younger households favor brands that support seamless smart home integration.

According to a 2025 Gartner review, smart home adoption in multi-unit residential buildings grew by 22 %, enabling over 500 property management firms to reduce common-area energy use by 10 %.

North America accounted for the largest market share at 32.24% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 24-25% between 2025 and 2032.

In 2024, North America recorded over 279.4 million installed smart home systems, including 40 million whole-home systems and 239.4 million point-solutions; approximately 41.3 % of households were smart-home enabled. Europe held about USD 38.1 billion in market value in that year. Asia-Pacific consumption was strong: China, Japan, and India together accounted for major device volumes, with China seeing growth in appliance and sensor adoption exceeding USD 18 billion. Latin America and MEA trails with combined shares less than 15 % but show increasing demand around security and energy control. The volume of smart thermostats, lights, and voice assistants in these regions surged by over 30 % in unit shipments from 2023 to 2024.

What Powers Leading Device Ecosystems in North American Homes?

North America holds approximately 32–36 % market share of global smart home tech installations in 2024. Demand is especially strong from residential homeowners and multi-family dwellings, with key industries including security & access control, energy management, and HVAC systems leading the uptake. Regulatory support comes via energy efficiency rebates, building codes mandating smart meter readiness, and standards encouraging interoperability across platforms. Technological advances include growth in voice assistant ecosystems (voice interfaces, Alexa, Google, etc.), stronger edge computing in control hubs, and integration of Matter/Thread standards for device compatibility. Local players—such as a major U.S. home automation firm—are embedding AI-based predictive maintenance into security systems, and energy utilities are partnering to offer demand response programs to homeowners. Consumer behavior shows that in North America higher enterprise adoption occurs in sectors like healthcare and finance for smart building controls, while homeowners prefer bundled solutions (security + climate + appliance control). Also, Americans report spending more per device, and over 70 % of homes in North America own at least one smart home device in 2024.

How Are Sustainable Standards Shaping Device and Consumer Priorities?

Europe commands about 20-25 % market share of smart home tech deployment in 2024. Key markets include Germany, UK, and France where regulatory bodies are enforcing energy-efficiency standards, green building regulation, and data‐privacy rules. Sustainability initiatives, including EU directives on product lifespan, recycling, and carbon footprint labelling, are driving demand for greener smart devices. Emerging technologies such as low-power wireless sensors, indoor air quality monitors, and privacy-by-design smart cameras are being adopted rapidly. Local players, such as European manufacturers of smart thermostats in Germany, are integrating environmental monitoring with energy savings features. Consumer behavior in Europe often values transparency and explainability; purchasers frequently evaluate device certifications and sustainability labels. In many Western European countries, over 50 % of smart home consumers are willing to pay premium for eco-friendly devices.

What E-Commerce and Local Innovation Trends Are Accelerating Adoption?

Asia-Pacific ranks among the top two in global smart home tech market volume in 2024. Top consuming countries are China, India, and Japan, with China contributing over USD 18 billion in smart appliances and sensor systems. Manufacturing and supply chain investments are rising: China and South Korea host growing hub production for smart components; India is seeing rapid assembly and consumer electronics manufacturing expansion. Regional tech trends include mobile app-based automation, voice interfaces in local languages, and integration of smart home with smart city infrastructure. Local players and startups are embedding AI and IoT in inexpensive climate control devices and low-cost security cameras for large middle-income segments. Consumer behaviors vary: in Asia-Pacific more purchases happen via e-commerce platforms; there is high sensitivity to price-performance and local language support; many households adopt devices gradually, starting with security, then lighting, then climate control.

What Drives Growth in Media, Localization, and Infrastructure Incentives?

In South America, key countries include Brazil and Argentina, with the regional smart home tech market share around 8-10 % of global installations in 2024. Infrastructure trends show rising electrification and improved broadband penetration in urban zones. Government incentives in several countries provide tax or import duty relief for energy-efficient or security devices. Local players are increasingly offering localized content (Spanish / Portuguese language support) in control apps and security systems, as well as partnering with telecom providers to bundle devices with connectivity plans. Consumer behavior in South America emphasizes media and language localization; many buyers favor systems with user interfaces in native languages. There is also a strong preference for security and entertainment devices before full automation; first purchases often include smart speakers, TVs, or cameras.

How Are Construction and Resource Efficiency Shaping Smart Device Uptake?

In Middle East & Africa, demand trends are shaped by rapid construction, high incomes in Gulf states (e.g., UAE, Saudi Arabia), and increasing infrastructure modernization in countries such as South Africa. Regional market share sits around 4-7 % globally in 2024, but absolute unit shipments of smart thermostats, energy meters, and lighting control devices have been growing at double-digit rates in urban areas. Technological modernization includes solar-powered systems, off-grid device compatibility, and integration of smart home tech in luxury residential builds. Local regulations are encouraging energy efficiency benchmarks; trade partnerships with European and North American manufacturers help fill gaps. One example: a property developer in UAE is equipping new housing projects with integrated security and environmental control systems, pre-wiring smart panels during construction. Consumer behavior variation: preference towards premium branded devices, centralized controls, and strong interest in smart appliance durability and backup power features due to frequent power concerns.

United States — ~ 35 % market share; dominance on account of high production capacity, strong R&D investment, and widespread consumer demand for integrated smart home systems.

China — ~ 18-20 % market share; rapid expansion driven by large-scale manufacturing, local ecosystem players, strong deployment in both new residential construction and retrofit segments.

The Smart Home Tech market is moderately fragmented, with over 50 active competitors globally vying for leadership in security, connectivity, appliances, and control platforms. The combined share of the top 5 companies is approximately 55-60 %, leaving room for mid-size players and startups to innovate. Strategic initiatives include partnerships (for example, device manufacturers collaborating with cloud/AI firms), frequent product launches of smart speakers, smart cameras, and energy-management hubs, and mergers or acquisitions aimed at securing ecosystem compatibility. Innovation trends influencing competitive dynamics include interoperability certification (Matter/Thread), embedding edge AI for low-latency control, and integrating renewable energy sources (solar, storage) with home automation. Companies are investing significantly in connectivity, voice and gesture recognition, sensor miniaturization, and privacy/security upgrades. Market positioning tends to cluster around full-stack ecosystem providers, niche specialized device makers, platform integrators, and service bundles.

Samsung Electronics

Honeywell International

Bosch

Apple

LG Electronics

Schneider Electric

Siemens

ADT

Legrand

Control4 (Snap One)

Vivint

Signify

Current and emerging technologies reshaping the smart home tech landscape include advanced edge computing, AI-based predictive analytics, sensor fusion, and seamless connectivity standards. Edge-cloud architectures are now supporting local decision-making: over 35 % of new smart hubs incorporate onboard inference for latency and privacy. Predictive algorithms in HVAC and security systems detect anomalies or performance degradation ahead of failure, reducing downtime by double digits. Low-power wireless protocols (Matter, Thread, Bluetooth Low Energy) are being integrated into mainstream devices to improve battery life and reduce energy usage. Sensor fusion techniques combining temperature, humidity, motion, and air-quality data are enabling more precise automation. Emerging trends also include generative AI for user experience (automated routines, natural-language scene setup) and use of digital twins of residential environments for simulation and optimization of energy and security performance. Devices are also increasingly designed with modularity, allowing users to scale systems over time rather than replace whole systems.

• In December 2024, Eve Systems launched its Android-compatible “Eve for Matter” app supporting the Matter-over-Thread smart radiator valve; it enables autonomous scheduling and remote control across platforms. Source: www.theverge.com

• In August 2024, LG introduced ThinQ ON, a smart home hub with built-in AI voice assistant and compatibility with Thread, Matter, Wi-Fi protocols; intended to streamline cross-device control in homes. Source: www.theverge.com

• In 2024, Google replaced Google Assistant on Nest and Home devices with Gemini for Home, enhancing context-aware voice control and automations in speakers, cameras, and home displays. Source: www.timesofindia.indiatimes.com

• In 2025, Amazon unveiled upgraded Echo Show 8 and 11 with AZ3 Pro chips and Omnisense sensors, boosting smart display performance and introducing wider hub capabilities via Matter, Thread, and Zigbee support. Source: www.theverge.com

This report covers the Smart Home Tech market across multiple dimensions: product types (security & access control, lighting, HVAC & climate, smart appliances, entertainment & connectivity, health monitoring, etc.), applications (retrofit upgrades, new construction integration, hybrid/commercial-residential), and end-users (single-family homes, multi-family dwellings, serviced residences, hospitality). Geographically, it spans North America, Europe, Asia-Pacific, South America, Middle East & Africa, with detailed country-level insights for leading markets such as United States, China, Germany, India, Brazil. It investigates emerging technologies like AI inference at edge, low-power wireless protocols, sensor fusion, generative automation, and digital twin integration. The report also includes regulatory, ESG, and sustainability frameworks (energy efficiency mandates, privacy laws, carbon reduction targets), consumer behavior data (adoption rates, preferences by region, interface and language preferences), and market challenges (interoperability, cost, infrastructure limits). Key drivers, restraints, opportunities, and competitive landscapes are analyzed to assist decision-makers in strategy, investment, and product positioning in the Smart Home Tech market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 123,425.4 Million |

|

Market Revenue in 2032 |

USD 655,073.8 Million |

|

CAGR (2025 - 2032) |

23.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Amazon, Google, Samsung Electronics, Honeywell International, Bosch, Apple, LG Electronics, Schneider Electric, Siemens, ADT, Legrand, Control4 (Snap One), Vivint, Signify |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |