Reports

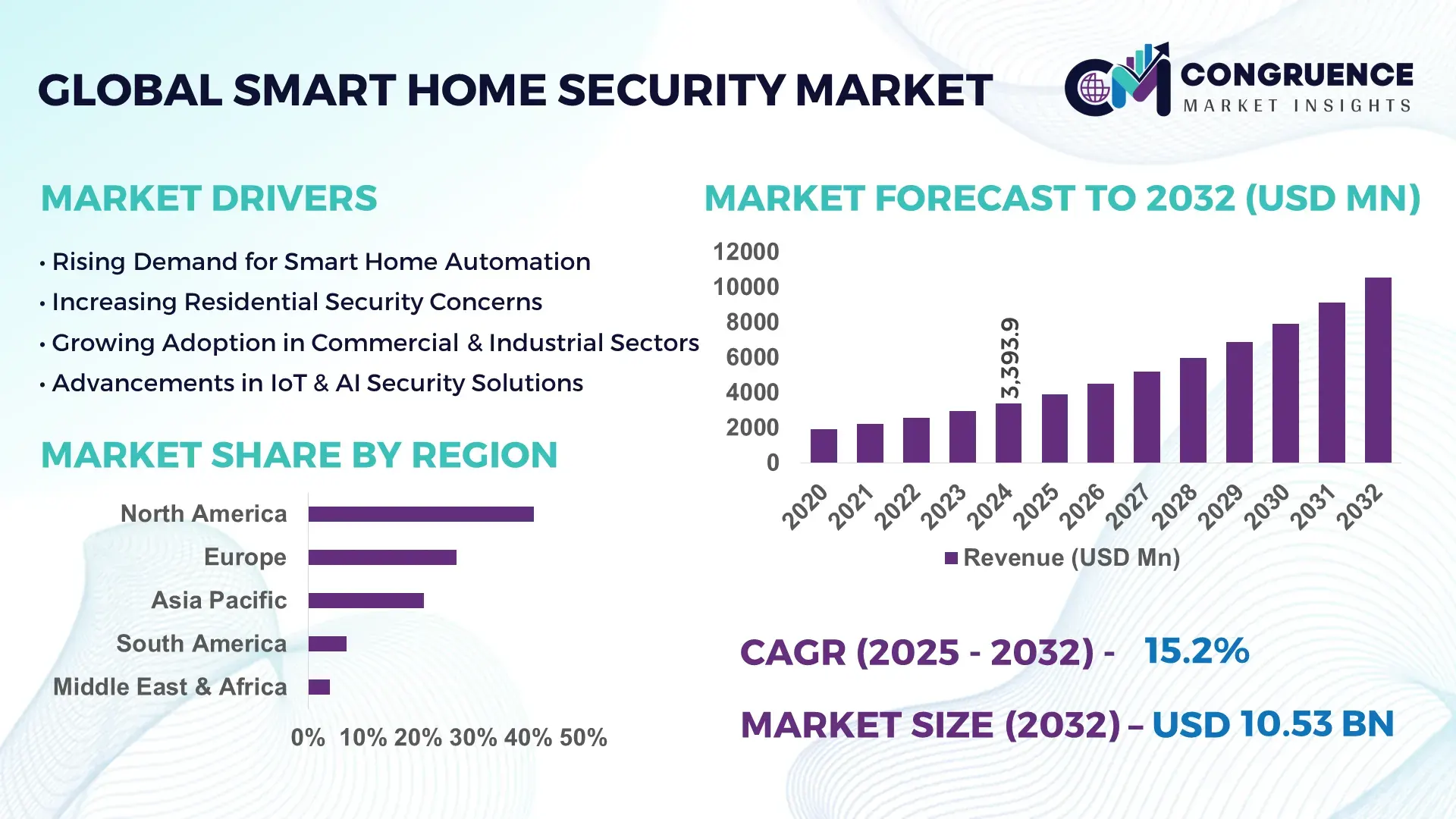

The Global Smart Home Security Market was valued at USD 3,393.9 Million in 2024 and is anticipated to reach a value of USD 10,527.3 Million by 2032, expanding at a CAGR of 15.2% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by the increasing adoption of connected devices and rising consumer awareness of home safety.

The United States leads the Smart Home Security Market, with substantial investments in IoT-enabled security systems and advanced surveillance technologies. The country’s production capacity exceeds 2.5 million smart security devices annually, supported by an investment of over USD 1.2 billion in R&D facilities. Key applications span residential, commercial, and industrial sectors, with consumer adoption rates of 48% for smart alarms and 42% for video surveillance systems. The U.S. market is also witnessing rapid integration of AI-driven analytics and cloud-based monitoring, with over 65% of new installations leveraging these technologies for predictive security measures.

Market Size & Growth: The market value reached USD 3,393.9 Million in 2024 and is projected to hit USD 10,527.3 Million by 2032. Growth is fueled by widespread adoption of IoT-enabled smart devices and enhanced consumer awareness about home safety.

Top Growth Drivers: Rising adoption of AI-enabled security solutions (62%), increasing smart home penetration (55%), and enhanced networked surveillance capabilities (48%).

Short-Term Forecast: By 2028, system integration and cloud-based monitoring are expected to reduce incident response times by 30% across residential installations.

Emerging Technologies: AI-driven video analytics, biometric authentication, and cloud-based smart monitoring platforms are redefining system capabilities.

Regional Leaders: North America projected at USD 4,200 Million by 2032 with advanced adoption; Europe at USD 3,100 Million with smart building integration; Asia Pacific at USD 2,800 Million focusing on IoT-enabled residential solutions.

Consumer/End-User Trends: Residential users increasingly favor multi-device systems; commercial establishments implement automated access control for efficiency.

Pilot or Case Example: In 2025, a pilot deployment in New York improved residential response times by 28% using AI-enabled smart sensors.

Competitive Landscape: Market leader: ADT Inc. (~18%), followed by Honeywell, Vivint Smart Home, Ring, and SimpliSafe.

Regulatory & ESG Impact: Incentives for energy-efficient security systems and compliance with privacy regulations are shaping adoption.

Investment & Funding Patterns: USD 1.2 Billion in recent smart security projects, with venture capital increasing investments in AI and IoT innovations.

Innovation & Future Outlook: Expansion of AI-powered analytics, predictive monitoring, and integration with smart home ecosystems to enhance operational efficiency.

The Smart Home Security Market is witnessing adoption across residential, commercial, and industrial sectors, driven by advances in AI surveillance, cloud monitoring, and integrated alarm systems. Regulatory measures promoting energy efficiency and regional preferences for IoT-enabled devices are shaping deployment patterns, while emerging technologies like facial recognition and predictive analytics are redefining market expectations.

The strategic relevance of the Smart Home Security Market lies in its ability to combine safety, automation, and operational efficiency. AI-powered video analytics deliver a 35% improvement in threat detection compared to conventional CCTV systems. North America dominates in installation volume, while Europe leads in adoption among commercial enterprises with over 40% integration in corporate facilities. By 2026, cloud-based monitoring platforms are expected to reduce false alarms by 25% and improve system response times. Firms are committing to ESG improvements, including a 20% reduction in energy consumption through IoT-enabled devices by 2027. In 2025, ADT Inc. achieved a 30% decrease in downtime for residential monitoring through AI-enabled sensor deployment. Looking forward, the Smart Home Security Market is poised to be a cornerstone for resilient, compliant, and sustainable home and commercial security solutions globally, driven by technology integration and advanced analytics.

The Smart Home Security Market is shaped by technological innovation, rising urbanization, and increased consumer awareness of safety. Advancements in IoT devices, AI surveillance, and cloud-based monitoring systems are enabling smarter, faster, and more integrated security solutions. Demand is also influenced by government regulations, incentives for energy-efficient systems, and a growing trend toward smart homes and automated building management. Key market players are investing heavily in R&D to enhance system capabilities, improve reliability, and expand product offerings across residential, commercial, and industrial sectors, ensuring robust adoption across diverse geographies.

The integration of AI and IoT technologies is enabling smart homes to monitor, detect, and respond to threats in real-time. AI-driven analytics can identify unusual behavior patterns and alert homeowners or authorities, while IoT connectivity allows seamless integration with multiple devices. In 2024, over 48% of new smart security installations in the U.S. employed AI-enabled sensors, significantly improving operational efficiency and reducing false alerts. Commercial and industrial facilities are also leveraging predictive analytics to optimize security patrol schedules, enhance surveillance coverage, and improve response times by up to 30%, demonstrating tangible operational benefits.

The initial investment in AI-driven and IoT-enabled smart security systems remains high, deterring small residential and commercial users. Installation complexity, including network configuration, device calibration, and system integration, adds to operational overheads. In 2024, 22% of potential adopters cited system complexity as a primary barrier, while maintenance and software updates contribute to ongoing costs. Additionally, compatibility issues with legacy devices limit adoption in older buildings. Such factors slow down the pace of market penetration despite the technological advantages offered by advanced smart security solutions.

AI-driven predictive security systems offer significant untapped potential by enabling proactive threat detection, reducing false alarms, and optimizing response times. In commercial sectors, predictive analytics have reduced security incidents by 18%, while residential pilot programs report a 25% improvement in system reliability. Integration with smart home ecosystems allows seamless device communication, enhancing convenience and safety. As AI algorithms become more sophisticated, there is potential to expand adoption in multi-unit residential complexes, smart offices, and industrial facilities, providing measurable improvements in safety outcomes.

Smart home security systems connected via IoT networks are vulnerable to cyberattacks, raising privacy and data security concerns. Compliance with regional regulations such as GDPR in Europe requires robust encryption and secure data handling practices. In 2024, 15% of security breaches were linked to weak device security protocols. Moreover, ensuring compatibility with evolving standards and maintaining firmware updates across multiple devices pose operational challenges. These factors create hurdles for manufacturers and service providers in delivering reliable, secure, and compliant solutions to end-users.

AI-Enabled Surveillance Integration: AI-powered video analytics are increasingly deployed, with 55% of new commercial installations in 2024 leveraging facial recognition and behavioral analysis, improving threat detection accuracy by 28%.

Cloud-Based Monitoring Adoption: Cloud integration for residential and commercial properties rose by 48% in 2024, enhancing system uptime, real-time alerts, and remote access capabilities while reducing operational downtime by 22%.

Consumer Preference for Multi-Device Platforms: 60% of homeowners now prefer integrated platforms combining smart alarms, cameras, and door locks, driven by convenience and unified app control, improving system responsiveness by 35%.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Smart Home Security Market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

The Smart Home Security Market is structured around key segments that include product types, applications, and end-user categories, providing a comprehensive framework for industry stakeholders. By type, the market is driven by devices such as smart cameras, alarms, access control systems, and sensors, each designed to address varying security needs. Applications range from residential monitoring to commercial surveillance and industrial safety, reflecting diverse deployment scenarios. End-user insights reveal that homeowners, small-to-medium enterprises, and large industrial facilities increasingly adopt integrated smart security solutions. Consumer adoption trends highlight preferences for systems combining video surveillance, motion detection, and mobile monitoring capabilities, with adoption rates exceeding 45% in urban households. Regional segmentation also shows differing usage patterns, with North America and Europe leading in technology integration, while Asia Pacific demonstrates rapid growth in sensor and alarm deployments. These segmentation insights allow decision-makers to tailor strategies across products, applications, and end-users.

Smart cameras currently lead the Smart Home Security Market, accounting for approximately 42% of adoption, due to their high-resolution monitoring, AI-driven analytics, and remote accessibility. Alarms and access control systems follow with a combined share of 33%, providing essential intrusion detection and user authentication functions. Sensors, including motion and window/door detectors, make up the remaining 25%, serving niche applications such as perimeter monitoring and smart home automation. Video cameras are experiencing the fastest adoption growth, fueled by advances in AI-powered facial recognition, cloud-based storage, and integration with mobile platforms.

Residential monitoring dominates the application segment, accounting for 48% of adoption, driven by increasing consumer awareness of home security and smart device integration. Commercial surveillance holds 32% of the market, focused on office buildings, retail outlets, and logistics centers that rely on AI-enabled monitoring for risk mitigation. Industrial safety and critical infrastructure applications contribute the remaining 20%, incorporating automated monitoring for operational continuity. Video surveillance adoption is rising fastest, supported by trends in AI-based analytics, cloud integration, and mobile accessibility. In 2024, over 38% of enterprises globally reported piloting smart security systems for office premises to improve asset protection and operational oversight.

Homeowners represent the leading end-user segment with a 45% adoption rate, primarily driven by the integration of smart cameras, alarms, and mobile monitoring applications. Small-to-medium enterprises are emerging rapidly as the fastest-growing end-user segment, fueled by the need for affordable, scalable security systems; adoption is projected to surpass 30% by 2032. Large industrial and critical infrastructure facilities account for 25% of adoption, using advanced AI-driven monitoring and access control solutions. In 2024, more than 60% of urban households in North America adopted multi-device smart security platforms, reflecting heightened consumer safety awareness. Over 40% of SMEs in Europe implemented integrated access control and surveillance systems for workforce and asset protection.

North America accounted for the largest market share at 41% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 16.8% between 2025 and 2032.

In 2024, North America installed over 5.2 million smart home security devices, driven by high consumer adoption of AI-enabled surveillance, cloud monitoring, and integrated access control. Europe followed with 3.1 million units, while Asia Pacific deployed 2.8 million units. Urban households in North America showed adoption rates of 48%, with SMEs contributing an additional 22% of total deployments. Investments in R&D for AI-powered sensors exceeded USD 1.2 billion in 2024, supporting advanced device production. Smart cameras, alarms, and access control systems accounted for 68% of total devices installed across all regions, highlighting type-specific dominance and consumer preference trends.

North America holds approximately 41% of the global smart home security market by volume, driven by residential and commercial demand. Healthcare and financial sectors are leading adopters, leveraging AI-driven video analytics and cloud-based monitoring. Recent regulatory initiatives encourage energy-efficient and connected security installations, promoting both compliance and innovation. Technological advancements include integration of biometric authentication, predictive AI monitoring, and multi-device control platforms. ADT Inc., a key player, recently launched an AI-enabled residential monitoring program covering over 1.5 million homes, enhancing real-time threat detection. Consumer behavior varies with higher enterprise adoption in healthcare and finance, while residential users prefer mobile-enabled monitoring systems. North America’s focus on digital transformation supports broader uptake of advanced smart security technologies.

Europe accounts for around 27% of the global smart home security market, with Germany, the UK, and France being the top contributors. Regulatory requirements and sustainability initiatives, such as energy efficiency certifications and privacy compliance standards, influence adoption patterns. Emerging technologies, including AI-based facial recognition and cloud monitoring, are widely integrated into residential and commercial projects. Local players, such as Bosch Security Systems, are advancing AI-enabled camera solutions to enhance predictive monitoring. Consumer behavior reflects regulatory-driven demand, with urban households prioritizing explainable and compliant solutions. Industrial sectors, including logistics and energy, also drive adoption, leveraging integrated alarm and access control systems to protect assets.

Asia-Pacific represents approximately 21% of global installations, with China, India, and Japan leading adoption. The region emphasizes mobile AI applications and e-commerce integration, supporting residential and small business uptake. Infrastructure development, including smart city initiatives and automated commercial complexes, drives volume growth. Regional innovation hubs focus on AI-based video analytics and cloud connectivity. Hikvision, a key regional player, expanded its AI camera installations to over 1.2 million units in 2024, enhancing monitoring efficiency. Consumer preferences favor mobile-controlled, multi-device platforms. Urbanized populations increasingly demand integrated smart home security systems to improve convenience, safety, and energy efficiency.

South America accounts for approximately 7% of the global smart home security market, led by Brazil and Argentina. Adoption is influenced by energy sector investments and modernized infrastructure projects. Government incentives for connected security systems encourage SME and residential uptake. Local players, such as Positivo Tecnologia, have expanded smart alarm and access control solutions in metropolitan areas, improving consumer safety. Regional consumer behavior is influenced by language localization, mobile integration, and media-driven awareness campaigns. Urban households increasingly adopt AI-enabled cameras and alarms, while commercial establishments implement automated monitoring for risk mitigation.

The Middle East & Africa region represents roughly 4% of global installations, with major growth in the UAE and South Africa. Demand is driven by the oil & gas, construction, and commercial sectors, emphasizing high-security standards. Technological modernization trends include AI surveillance, biometric access, and cloud-based monitoring. Government regulations and trade partnerships support adoption, including security mandates in commercial complexes. Local players, such as G4S Middle East, are deploying integrated monitoring systems for large facilities, enhancing real-time surveillance capabilities. Regional consumer behavior reflects preference for advanced systems in urban centers, with higher enterprise adoption in energy and commercial infrastructure projects.

United States – 41% Market Share: Strong production capacity, advanced AI surveillance adoption, and regulatory support for connected security devices.

Germany – 12% Market Share: High consumer adoption of integrated security systems and strict regulatory compliance driving demand for advanced smart home solutions.

The Smart Home Security Market is moderately fragmented, with over 120 active competitors operating globally. The competitive environment is characterized by strategic product innovations, technology-driven differentiation, and regional expansion initiatives. The top five companies collectively account for approximately 55% of the market, indicating a strong presence but allowing ample opportunities for emerging players. Leading firms are actively engaging in partnerships and mergers to expand technology offerings and geographic coverage, while continuous product launches focus on AI-enabled surveillance, cloud monitoring, and multi-device integration. Innovation trends include advanced biometric authentication, predictive threat analytics, and edge computing-enabled devices. Companies are increasingly leveraging IoT connectivity and mobile application integration to enhance user convenience and system interoperability. Regional competition is also intensifying, with North America emphasizing enterprise adoption in healthcare and finance, Europe focusing on regulatory-compliant solutions, and Asia-Pacific accelerating AI-driven residential deployments. Market participants are strategically investing in R&D facilities, piloting smart security solutions, and developing energy-efficient, connected devices to strengthen market positioning and maintain a competitive edge.

Vivint Smart Home

SimpliSafe Inc.

Bosch Security Systems

Hikvision Digital Technology

G4S plc

The Smart Home Security Market is being shaped by both current and emerging technologies that enhance operational efficiency, predictive monitoring, and user experience. AI-powered video analytics are now standard in over 50% of smart cameras installed in residential and commercial properties, enabling real-time threat detection and automated anomaly alerts. Cloud-based monitoring platforms allow seamless remote access and integration with multiple devices, improving system uptime by approximately 22%. Biometric authentication technologies, including facial recognition and fingerprint sensors, are being deployed in access control systems to enhance security reliability. Edge computing is increasingly incorporated in smart security devices to process data locally, reducing latency and improving response times by up to 30%. Additionally, IoT integration ensures interoperability between cameras, alarms, sensors, and mobile applications, creating unified smart home ecosystems. Companies are also exploring energy-efficient hardware and AI-enabled predictive algorithms to optimize performance while reducing operational costs. Robotics-assisted surveillance and drone-based monitoring are emerging in high-security industrial and commercial applications, demonstrating the trend toward automated and intelligent security solutions. These technological advancements are driving differentiated offerings and influencing purchasing decisions across residential, commercial, and industrial end-users.

In 2024, ADT officially launched its next-generation ADT+ platform, integrating its proprietary hardware with Google Nest devices, adding AI-powered insights and real-time alerts for improved customer control and monitoring. Source: www.adt.com

Also in 2024, ADT introduced the “Trusted Neighbor™” feature via the ADT+ app, allowing homeowners to grant secure, event- or time-based access to trusted individuals using Yale smart locks and Nest cameras. Source: www.adt.com

In October 2024, ADT disclosed a cybersecurity incident: an unauthorized actor accessed certain internal systems using third‑party credentials. While no customer security systems were compromised, the company reinforced cybersecurity controls and engaged external experts. Source: www.adt.com

In March 2024, Hikvision launched its AX HOME Series wireless alarm system, certified to European EN Grade 2 intruder alarm standards. The system is energy-efficient (consumes as little as 0.05 kWh/day), supports Open Things Access Protocol (OTAP) for third-party device integration, and offers plug-and-play setup via the Hik‑Connect app. Source: www.hikvision.com

The Smart Home Security Market Report provides a comprehensive analysis of global trends, technologies, product types, applications, and end-user segments across major geographic regions. The report covers detailed segmentation including smart cameras, alarms, access control systems, sensors, and integrated platforms, highlighting their deployment across residential, commercial, and industrial sectors. Geographic coverage encompasses North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing insights into regional adoption patterns, regulatory landscapes, and technological innovations. Key industry focus areas include AI-driven analytics, IoT-enabled monitoring, cloud-based solutions, biometric access, and predictive threat management. Emerging segments such as modular security devices, drone-assisted monitoring, and robotics-integrated systems are also included, reflecting evolving market dynamics. Additionally, the report examines consumer behavior trends, enterprise adoption rates, and technological advancements shaping future investments. Strategic insights into competitive activities, R&D initiatives, and pilot programs offer decision-makers actionable intelligence to optimize market positioning. The report emphasizes the interconnection between technology, regulations, and end-user requirements, providing a holistic understanding of opportunities and challenges across global markets.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 3,393.9 Million |

| Market Revenue (2032) | USD 10,527.3 Million |

| CAGR (2025–2032) | 15.2% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | ADT Inc., Honeywell International Inc., Ring LLC, Vivint Smart Home, SimpliSafe Inc., Bosch Security Systems, Hikvision Digital Technology, G4S plc |

| Customization & Pricing | Available on Request (10% Customization Free) |