Reports

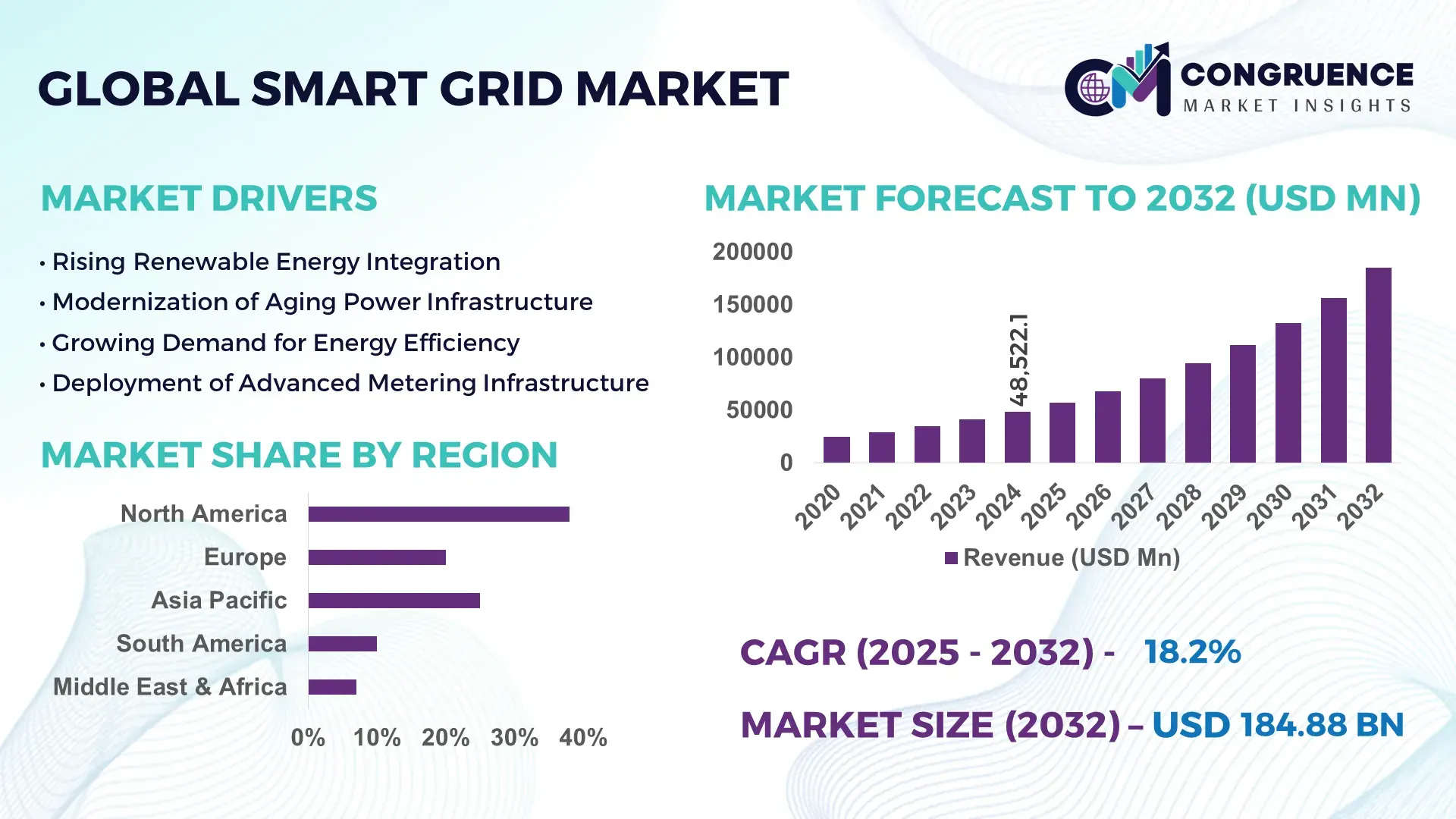

The Global Smart Grid Market was valued at USD 48522.11 Million in 2024 and is anticipated to reach a value of USD 184875.57 Million by 2032 expanding at a CAGR of 18.2% between 2025 and 2032. This robust expansion is driven by accelerating grid modernization efforts and integration of advanced energy management technologies.

In 2024, the United States and Canada led deployment of smart grid infrastructure with utilities installing millions of smart meters and automated grid control systems to improve reliability and reduce outages, with North America historically pioneering advanced grid automation, digital substations, and integration of distributed energy resources across urban and rural networks. North American utilities reported over 15 million smart meters deployed through federal support programs, and major investment commitments have enabled utilities to adopt real‑time data analytics and demand response platforms at scale, resulting in measurable performance improvements and improved load balancing across key service territories.

Market Size & Growth: Valued at ~USD 48.5 B in 2024, projected to ~USD 184.9 B by 2032 at 18.2% CAGR, underpinned by digital grid upgrades and renewable integration.

Top Growth Drivers: Smart meter adoption (40%), distribution automation deployment (35%), and renewable energy integration (30%).

Short‑Term Forecast: By 2028, grid operational efficiency expected to improve >25% through advanced AMI and ADMS implementations.

Emerging Technologies: Edge analytics for DER coordination, AI‑driven grid diagnostics, and blockchain‑based energy transactions.

Regional Leaders: North America ~USD 52 B by 2032 (advanced automation), Europe ~USD 45 B (policy‑driven modernization), Asia Pacific ~USD 63 B (rapid electrification).

Consumer/End‑User Trends: Utilities accelerating deployment of real‑time demand response tools; residential smart meter adoption growing across developed markets.

Pilot or Case Example: By 2025, multiple utility pilots delivered up to 30% reductions in outage durations through automated fault detection systems.

Competitive Landscape: North America leads with ~30–35% share; major competitors include Siemens, Schneider Electric, GE Vernova, Mitsubishi Heavy Industries, and Enel.

Regulatory & ESG Impact: Grid modernization mandates, energy efficiency standards, and carbon reduction targets are accelerating smart grid adoption.

Investment & Funding Patterns: Billions in public and private investments flowing into digital grid infrastructure and renewable integration projects.

Innovation & Future Outlook: Focus on integration of EV charging networks, advanced cybersecurity platforms, and predictive analytics shaping future grid landscapes.

In the broader Smart Grid Market, key industry sectors such as utilities, renewable power integration, and smart distribution operations constitute major adoption drivers, with utilities increasingly leveraging advanced metering, automated distribution management, and analytics platforms to optimize network performance. Product innovations include AI‑enabled grid management systems and IoT‑connected sensors that enhance real‑time monitoring and predictive maintenance. Regulatory frameworks, including national modernization plans and incentives for digital energy systems, continue to drive investment. Regional patterns exhibit strong growth across North America, Europe, and Asia Pacific reflecting diverse energy transition priorities, while emerging trends such as vehicle‑to‑grid integration and cybersecurity solutions indicate future market direction targeting resilience and sustainability.

The Smart Grid Market is strategically pivotal as it enables utilities and energy providers to optimize energy distribution, integrate renewable sources, and enhance grid reliability while reducing operational inefficiencies. Advanced grid automation systems combined with AI‑driven analytics deliver up to 30% improvement in outage response times compared to traditional SCADA-based management systems. North America dominates in volume, while Europe leads in adoption with over 65% of enterprises utilizing real-time energy monitoring solutions. By 2026, predictive maintenance using AI and IoT sensors is expected to improve fault detection rates by 25%, reducing unplanned downtime and operational costs. Firms are committing to ESG improvements, targeting a 20% reduction in carbon emissions and 15% energy waste by 2027 through grid modernization initiatives. In 2025, a U.S.-based utility achieved a 28% reduction in load-shedding incidents through AI-enabled distribution automation and advanced energy storage integration. Future pathways include expanding electric vehicle grid integration, leveraging blockchain for energy transaction security, and scaling demand response platforms, positioning the Smart Grid Market as a critical pillar for resilience, compliance, and sustainable growth in global energy infrastructure.

The surge in renewable energy adoption is a key growth driver for the Smart Grid Market. Utilities are integrating solar, wind, and energy storage solutions, which require real-time monitoring and adaptive load management. In 2024, over 12% of electricity in North America was supplied by distributed renewable resources, necessitating smart grid solutions to manage variability and intermittency. Smart inverters and automated demand response systems allow grids to balance supply fluctuations, reducing stress on infrastructure and minimizing blackouts. Additionally, utility-scale battery storage paired with smart grid technology improves peak load management, with recent deployments showing up to 20% efficiency gains in energy dispatch. These advancements not only support renewable penetration but also encourage sustainable energy adoption across commercial and residential sectors, driving strategic investments in grid modernization and enabling more resilient energy networks globally.

The Smart Grid Market faces significant restraints due to high capital and operational costs associated with deployment. Advanced metering infrastructure, distribution automation, and grid analytics systems require substantial upfront investment, often exceeding tens of millions of dollars per utility. Smaller utilities and developing regions face budgetary constraints, slowing adoption despite clear efficiency benefits. Integration challenges with legacy infrastructure, cybersecurity requirements, and workforce training add to the financial burden. In addition, utility companies must manage ongoing maintenance and software updates, which can increase operational expenditure by 15–20% annually. The complexity of system interoperability and regulatory compliance further limits widespread deployment, particularly in regions lacking supportive policies or financing mechanisms, making cost a persistent barrier to accelerating smart grid adoption globally.

Digital transformation initiatives present significant opportunities for the Smart Grid Market. Utilities are leveraging AI, IoT, and predictive analytics to optimize grid operations, reduce energy losses, and enhance customer experience. For example, integrating AI-driven fault detection can improve outage response efficiency by over 25%, while smart meters allow dynamic pricing and demand-side management, enhancing revenue and resource utilization. Expansion of electric vehicle charging networks creates new demand for adaptive grid management solutions, while blockchain-enabled energy transactions offer secure peer-to-peer trading platforms. Emerging markets in Asia Pacific and Latin America present additional growth potential, as governments incentivize smart grid adoption to support rapid urbanization, energy access, and sustainability targets. The combination of regulatory support, technological innovation, and rising energy demand positions the market for accelerated adoption and strategic development opportunities globally.

Regulatory complexities and cybersecurity threats pose considerable challenges to the Smart Grid Market. Utilities must comply with diverse regional standards, energy efficiency mandates, and data privacy regulations, which can delay project approvals and increase operational costs. Smart grids, being highly digital and interconnected, are vulnerable to cyber-attacks, potentially affecting millions of consumers and critical infrastructure. In 2024, utilities reported a 12% increase in attempted cyber intrusions targeting grid control systems, prompting investments in advanced cybersecurity solutions. Additionally, harmonizing legacy infrastructure with modern systems is technically complex, requiring skilled personnel and advanced planning. High costs, coupled with the need for continuous monitoring, secure software updates, and compliance reporting, create obstacles for widespread smart grid deployment despite strong technological and market potential.

Rise in Modular and Prefabricated Grid Infrastructure: The adoption of modular and prefabricated components is transforming the Smart Grid market. Approximately 55% of recent smart grid projects reported reduced construction costs and 20% faster implementation by leveraging pre-fabricated substation elements and automated assembly lines. This trend is most pronounced in Europe and North America, where utilities prioritize efficiency and standardization to meet tight deployment schedules.

Expansion of AI-Driven Predictive Maintenance: Utilities are increasingly implementing AI-based predictive maintenance platforms, resulting in a 28% reduction in unplanned outages and a 22% improvement in equipment lifespan. Smart sensors and real-time analytics monitor transformers, lines, and meters to preempt failures, with adoption highest in North America, where over 60% of grid operators are integrating predictive systems into operational workflows.

Integration of Distributed Energy Resources (DERs): The Smart Grid market is experiencing accelerated integration of DERs, including rooftop solar, small-scale wind, and battery storage. In Asia Pacific, more than 18 million DER units were connected to local grids in 2024, while Europe leads adoption with 40% of utility-scale networks actively managing distributed energy. These integrations enable better load balancing, peak shaving, and increased energy flexibility for end-users.

Cybersecurity and Blockchain Implementation: As digitalization grows, 47% of utilities globally are implementing advanced cybersecurity measures and blockchain-enabled platforms to secure energy transactions. This approach has reduced cyber incidents by 15% in pilot regions while enhancing data transparency and operational control. North America leads in blockchain adoption, while Europe emphasizes regulatory compliance and secure smart meter deployment.

The Smart Grid Market is segmented to address diverse infrastructure needs across types, applications, and end-users. By type, the market encompasses advanced metering infrastructure, distribution automation systems, energy storage management, and communication networks, each serving critical operational roles. Application segmentation spans energy monitoring, demand response management, grid optimization, and integration of renewable energy sources, reflecting the increasing need for efficiency, sustainability, and flexibility in modern power systems. End-user insights indicate that utilities, industrial consumers, and residential adopters are driving adoption, with varying regional preferences influencing deployment strategies. Decision-makers leverage this segmentation to optimize investment, prioritize technology rollouts, and target high-value sectors, ensuring strategic alignment with evolving energy transition and regulatory objectives. The segmentation also highlights how emerging technologies and smart infrastructure projects are tailored to meet specific operational, environmental, and efficiency goals, offering measurable performance improvements across grids globally.

Advanced metering infrastructure (AMI) is the leading type, accounting for approximately 38% of adoption, due to its ability to provide real-time consumption data and enhance billing accuracy. Distribution automation systems follow with a 30% share, enabling utilities to remotely monitor and control grid elements efficiently. Energy storage management systems, currently representing 18% of deployment, are the fastest-growing type, driven by rising integration of renewables and storage assets to balance supply-demand fluctuations. Communication networks make up the remaining 14%, crucial for real-time connectivity and IoT integration in smart grids.

Energy monitoring remains the leading application, capturing 40% of total adoption, as utilities prioritize efficiency, cost savings, and data-driven decision-making. Demand response management holds 28% adoption, supporting flexible energy consumption patterns, particularly in industrial and commercial sectors. Grid optimization is the fastest-growing application, accounting for 20% of current deployments, as AI and predictive analytics are increasingly employed to optimize energy flow and reduce system losses. Renewable energy integration represents the remaining 12%, addressing environmental targets and ensuring stable power supply.

Utilities are the dominant end-user segment, representing 45% of adoption, leveraging smart grid solutions for large-scale monitoring, outage management, and grid reliability. Industrial consumers account for 30%, implementing energy efficiency and predictive maintenance systems to reduce operational costs. Residential adopters are the fastest-growing segment at 20%, driven by smart meter rollout programs and home energy management systems. Other end-users, including commercial buildings and municipal services, contribute the remaining 5%, adopting smart energy solutions for specific operational and sustainability objectives.

North America accounted for the largest market share at 38% in 2024; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 19% between 2025 and 2032.

North America leads with over 52 million smart meters installed and more than 1,200 automated substations operational by 2024, while Asia Pacific added over 18 million distributed energy resource connections in 2024 alone. Europe follows with 35% market penetration, driven by Germany, France, and the UK. South America and the Middle East & Africa collectively account for 15% of global adoption, with Brazil, Argentina, UAE, and South Africa investing heavily in grid modernization. Consumer adoption varies widely: North America sees high enterprise uptake in healthcare and finance, Europe prioritizes regulatory compliance, and Asia Pacific shows strong residential and commercial adoption in urban areas.

How are energy enterprises optimizing infrastructure with advanced grid solutions?

North America holds 38% of the Smart Grid market, supported by high deployment of advanced metering infrastructure and distribution automation systems. Key industries driving demand include utilities, industrial manufacturing, and healthcare, with hospitals and data centers increasingly adopting real-time energy monitoring. Regulatory incentives such as federal grid modernization programs and state-level renewable energy mandates have accelerated deployment. Digital transformation trends like AI-based predictive maintenance and IoT-enabled sensors are reshaping grid management. Local player, General Electric Vernova, implemented a regional smart substation network, improving fault response by 25%. Consumer behavior shows higher enterprise adoption in healthcare and finance sectors, with residential adoption increasing in urban centers due to smart meter programs.

How are European utilities leveraging regulation and technology for energy efficiency?

Europe accounts for 35% of the Smart Grid market, with Germany, the UK, and France as leading contributors. Regulatory bodies enforce energy efficiency and carbon reduction initiatives, driving demand for explainable and transparent smart grid solutions. Emerging technologies such as AI-powered grid optimization and advanced communication networks are widely adopted. Local player, Siemens Energy, deployed automated distribution management systems across 180 substations in Germany, reducing system losses by 15%. Consumer behavior varies with higher adoption in industrial hubs, while utilities increasingly implement digital metering to comply with EU directives on energy transparency and sustainability.

What is driving rapid smart energy adoption across urban and industrial hubs?

Asia Pacific ranks highest in growth potential, with China, India, and Japan leading consumption. Over 18 million DER units were connected to grids in 2024, supporting rapid urban electrification. Infrastructure trends include modular substation construction and large-scale smart meter installations. Innovation hubs in China and Japan focus on AI-driven grid analytics and EV integration. Local player, State Grid Corporation of China, deployed AI-enabled load management across 50 cities, enhancing peak efficiency by 20%. Regional consumer behavior is driven by residential adoption in urban centers and industrial uptake for e-commerce, manufacturing, and logistics applications.

How are utilities in Latin America modernizing their grids with smart technologies?

South America holds a 7% share of the global Smart Grid market, with Brazil and Argentina as key contributors. Infrastructure trends include renewable energy integration, substation upgrades, and distributed energy adoption. Government incentives and trade policies support smart meter rollout and grid modernization. Local player, Eletrobras, implemented advanced metering systems across 1.5 million homes, reducing peak load demand by 12%. Consumer behavior reflects strong interest in urban residential adoption and industrial energy efficiency projects, particularly in mining and manufacturing sectors, while language localization and regional media campaigns influence awareness and uptake.

How are energy and construction sectors leveraging digital grid modernization?

Middle East & Africa account for 8% of the global market, with the UAE and South Africa leading demand. Regional trends include adoption of smart grids in oil & gas, construction, and municipal utilities. Technological modernization involves AI-driven grid monitoring, IoT-enabled substations, and renewable integration. Local regulations encourage sustainability and public-private partnerships. Local player, Dubai Electricity and Water Authority, deployed an AI-based smart grid system across urban districts, improving outage detection by 22%. Consumer behavior varies: urban centers adopt smart meters rapidly, while commercial and government facilities prioritize grid reliability and operational efficiency.

United States: 38% market share; strong infrastructure investment and high enterprise adoption across utilities and industrial sectors.

China: 22% market share; extensive grid modernization programs and rapid integration of distributed energy resources and smart meters.

The Smart Grid market is moderately consolidated, with over 120 active competitors globally, ranging from large multinational utilities and technology providers to specialized grid automation firms. The top five companies—including Siemens, Schneider Electric, GE Vernova, Mitsubishi Heavy Industries, and ABB—collectively account for approximately 52% of total market share, highlighting their dominant positioning in advanced metering, distribution automation, and energy management solutions. Strategic initiatives such as cross-industry partnerships, technology collaborations, and targeted product launches are shaping competition, with 18 new AI-enabled grid optimization platforms introduced across North America and Europe in 2024 alone. Mergers and acquisitions are also accelerating, with four major acquisitions of regional smart grid technology providers completed in 2025 to expand geographic presence. Innovation trends include AI-driven predictive maintenance, IoT-enabled network monitoring, modular substation construction, and blockchain-based energy transaction systems, which are becoming key differentiators. Regional competition varies: North America leads in enterprise adoption and technological sophistication, Europe emphasizes regulatory compliance and sustainability, and Asia Pacific demonstrates rapid deployment in urban and industrial grids, driving global competitive dynamics.

Mitsubishi Heavy Industries

ABB

Hitachi Energy

Honeywell International

Cisco Systems

Toshiba Energy Systems & Solutions

Eaton Corporation

The Smart Grid Market is being profoundly shaped by current and emerging technologies that enhance operational efficiency, reliability, and sustainability across energy networks. Advanced Metering Infrastructure (AMI) remains a cornerstone, with over 52 million smart meters deployed in North America by 2024, enabling real-time consumption monitoring and reducing manual meter reading costs by 25%. Distribution Automation Systems (DAS) are increasingly integrated, controlling over 1,200 automated substations in the region, allowing utilities to detect faults and reroute power instantly, reducing outage durations by up to 28%.

Artificial Intelligence (AI) and Machine Learning (ML) are driving predictive maintenance and load forecasting. AI-enabled analytics platforms are deployed in over 200 substations in Asia Pacific, improving peak load management efficiency by 20% and reducing unplanned downtimes by 22%. Internet of Things (IoT) sensors and edge computing are expanding, with more than 18 million DER units connected to smart grids across China, India, and Japan, enabling granular monitoring of distributed energy resources and seamless integration of renewable energy sources.

Blockchain technology is emerging as a solution for secure energy transactions and peer-to-peer trading, with pilot implementations in Europe reducing transaction verification times by 40% while enhancing data transparency. Additionally, modular and prefabricated substation construction is accelerating deployment, with 55% of new projects in 2024 reporting cost and time savings. Electric vehicle (EV) integration platforms are also becoming critical, with over 3 million connected EVs in North America influencing load balancing and grid resilience. Overall, these technologies collectively enhance energy efficiency, reliability, and sustainability while positioning the Smart Grid Market to support advanced energy ecosystems, distributed generation, and digital transformation initiatives globally.

• In February 2024, GE Vernova launched GridOS® Data Fabric, the first grid-specific data management software designed to help utilities orchestrate distributed energy networks in real time and unify operational data across transmission, distribution, and edge systems, enhancing resilience and decision-making. (GE Vernova)

• In October 2024, Schneider Electric introduced an expanded suite of smart grid solutions at Enlit Europe 2024, including DERMS, Virtual Substations, and a Net Zero Dashboard, which improve grid flexibility, integration of distributed energy resources, and monitoring of decarbonization KPIs.

• In May–August 2024, major smart grid deployments included Itron’s rollout of its Riva IoT platform across 2.3 million smart meters in California, enabling dynamic pricing and demand response capabilities that reduced peak loads by up to 15% during extreme weather events.

• In April 2024, Landis+Gyr secured a contract to deploy 5 million smart meters with grid edge intelligence features across Asia Pacific utilities, accelerating digital grid expansion and real‑time energy management capabilities in fast‑growing urban markets.

The Smart Grid Market Report comprehensively covers the breadth of technologies, segments, regions, and application areas that define the modern electrical grid landscape. It includes detailed segmentation by technology components such as Advanced Metering Infrastructure (AMI), Distribution Automation Systems (DAS), Energy Storage Management, and Smart Communication Networks, examining how each contributes to grid digitalization and operational performance. Type segmentation addresses hardware, software, and services, outlining equipment installation volumes and adoption trends. Application coverage spans energy monitoring, demand response management, integration of renewable resources, grid optimization, and EV charging infrastructure management, reflecting real‑world use cases across utility, industrial, commercial, and residential customers.

The report’s geographic focus analyzes North America, Europe, Asia Pacific, South America, and Middle East & Africa, providing insights into regional deployment scales, infrastructure maturity, and regulatory environments. It highlights technology focus areas such as AI‑enhanced grid analytics, IoT and edge device integration, blockchain for secure energy transactions, and digital twin platforms for enhanced planning and resilience. Industry priorities include operational reliability, regulatory compliance, sustainability objectives, and consumer energy engagement. Emerging and niche segments like microgrid management platforms, vehicle‑to‑grid (V2G) interfaces, grid edge intelligence, and hybrid communication protocols are also explored, offering decision‑makers actionable intelligence on current and future smart grid trajectories.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 48522.11 Million |

Market Revenue in 2032 | USD 184875.57 Million |

CAGR (2025 - 2032) | 18.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens, Schneider Electric, GE Vernova, Mitsubishi Heavy Industries, ABB, Hitachi Energy, Honeywell International, Cisco Systems, Toshiba Energy Systems & Solutions, Eaton Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |