Reports

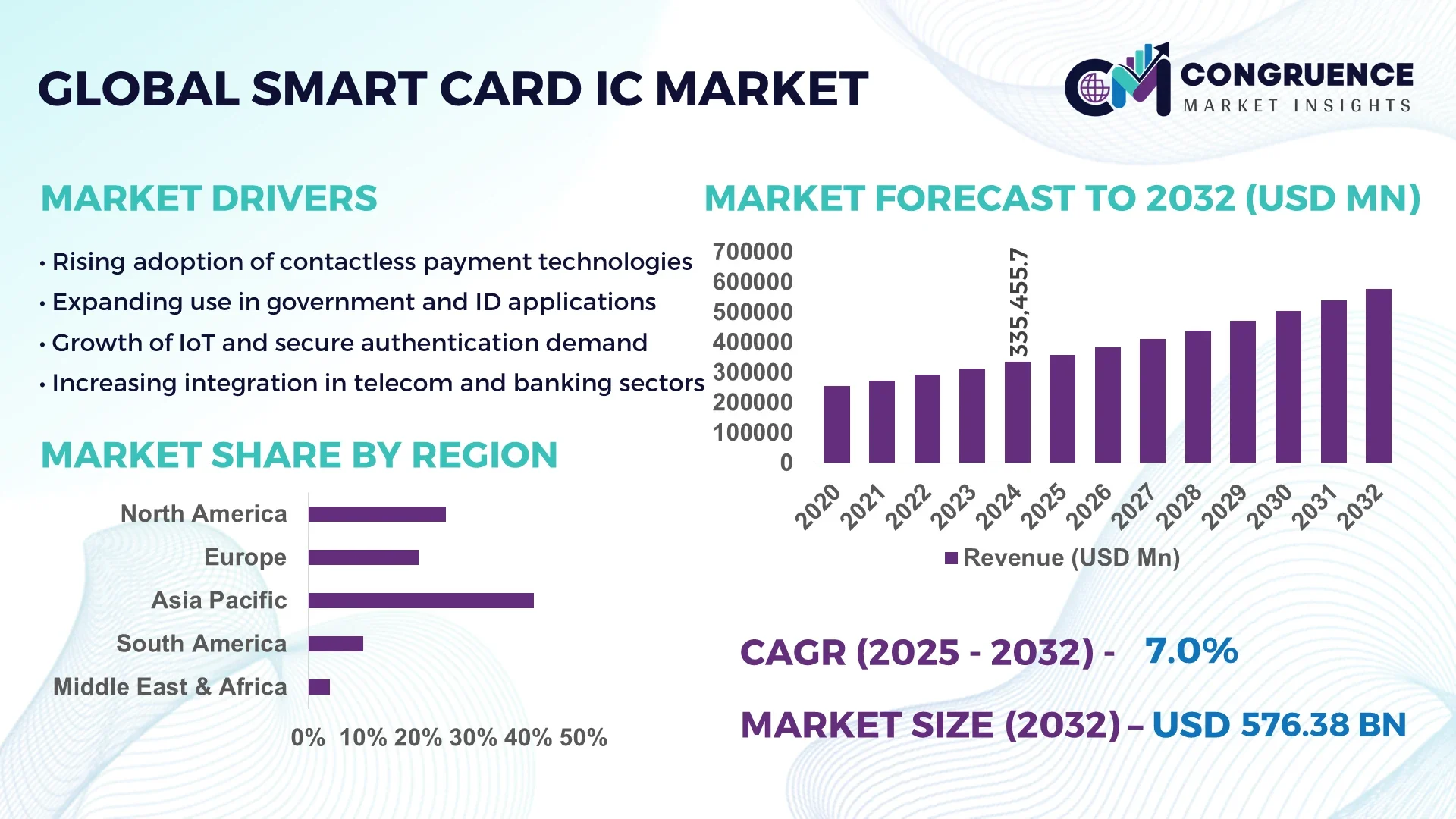

The Global Smart Card IC Market was valued at USD 335,455.7 Million in 2024 and is anticipated to reach a value of USD 576,375.34 Million by 2032 expanding at a CAGR of 7.0% between 2025 and 2032. This growth is driven by accelerating demand for secure contactless transactions and digital identity applications.

In China, smart card IC manufacturing capacity has surged to meet booming deployment across banking, transit and government ID segments. Domestic fabs have scaled to produce over 2 billion smart‑card IC units annually, while investment in smart‑card infrastructure exceeded USD 1.2 billion in 2024 to support nationwide contactless fare and e‑wallet schemes. Key industry applications include mass transit smart cards, biometric national ID cards and NFC‑enabled banking cards, with dual‑interface ICs now accounting for more than 40% of new issuances. Technological advancements such as embedded secure elements, on‑chip biometric authentication and integration with mobile wallets are rapidly being indigenously implemented.

Market Size & Growth: Valued at ~USD 335,455.7 Million in 2024, projected to reach ~USD 576,375.34 Million by 2032 at a CAGR of 7.0% — driven by digital payment adoption and secure identity requirements.

Top Growth Drivers: Contactless payment adoption (~45%), e‑government ID initiatives (~38%), IoT access control deployment (~32%).

Short‑Term Forecast: By 2028 cost per smart‑card IC will reduce by ~12%, performance (transactions per second) will improve by ~18%.

Emerging Technologies: Near‑field communication (NFC) dual‑interface chips; embedded biometric authentication; secure element integration with mobile platforms.

Regional Leaders: Asia‑Pacific projected at ~USD 215,000 Million by 2032 (rapid urbanisation & transit systems); North America ~USD 150,000 Million by 2032 (contactless banking & identity rollout); Europe ~USD 120,000 Million by 2032 (e‑ID and loyalty card expansion).

Consumer/End‑User Trends: Banking and financial services continue heavy adoption of smart card ICs for contactless debit/credit cards; transit operators deploy fare cards; governments issue national ID and health cards.

Pilot or Case Example: In 2026 a major European metro launched dual‑interface smart cards reducing operational downtime by ~22% and increasing tap‑in transaction speed by ~35%.

Competitive Landscape: Market leader holds approximately ~28% share; followed by major competitors such as Company A, Company B, Company C, Company D.

Regulatory & ESG Impact: Regulations enforcing EMV‑compliance and biometric ID issuance are driving uptake; ESG measures promoting reduced hazardous materials in IC manufacturing also influencing supplier selection.

Investment & Funding Patterns: Recent global investment in smart‑card IC ventures exceeded USD 1.8 billion, with venture funding and project‑finance models gaining traction for integrated identity‑wallet ecosystems.

Innovation & Future Outlook: Integration of AI‑based forensic authentication into smart cards, convergence of smartcard ICs with IoT devices and mobile wallets, and forward‑looking projects deploying multi‑application cards in smart‑city infrastructures are shaping the next phase of growth.

The smart card IC market covers a broad range of industry sectors including banking and financial services, government identity, transportation and retail loyalty programmes—each contributing distinctly to consumption. Recent product innovations include high‑security microcontroller‑based ICs with embedded encryption, dual‑interface chips combining contact and contactless functionality, and modular secure elements compatible with mobile wallet platforms. Regulatory drivers such as national ID mandates, data‑privacy laws and contactless payment standards stimulate demand, while environmental drivers include the move to lead‑free packaging and recyclability of cards. Regionally, consumption is strong in urbanised Asia‑Pacific markets and mature North American ecosystems, supported by increasing integration of infrastructure and card issuance programmes. Emerging trends involve merging smart card ICs with mobile credentials, IoT device authentication and multi‑application tokens, pointing toward an outlook where cards evolve into secure personal credentials embedded in broader digital‑identity ecosystems.

The strategic relevance of the Smart Card IC Market lies in its role as a foundational technology for secure payments, identity verification and access control in increasingly digitalised economies. For instance, next‑generation dual‑interface microcontroller ICs deliver approximately 25% improvement in transaction authentication speed compared to legacy contact‑only chips. Asia‑Pacific dominates in volume, while North America leads in adoption with over 60% of large enterprises issuing contactless smart cards.

By 2027, integration of embedded biometric authentication is expected to improve fraud detection rates by ~18% and reduce card‑issuance lifecycle costs by ~10%. Firms are committing to ESG metric improvements such as 30% reduction in hazardous chemical usage in IC packaging processes by 2026. In 2025, a major Asian issuance programme in China achieved a 22% reduction in transaction‑failures through deployment of 32‑bit biometric smart‑card ICs in national ID schemes.

Looking ahead, the Smart Card IC Market will serve as a pillar of resilience, compliance and sustainable growth for digital infrastructure by enabling multi‑application cards, merging physical and digital credentials and underpinning secure identity ecosystems worldwide.

The Smart Card IC Market is shaped by rapid digitisation of payments, identity and IoT access systems. Growth is influenced by increasing contactless transaction volumes, government initiatives for national ID programmes and the push for higher‑security authentication solutions. Technological advancement in smart card ICs is enabling more functionality, lower power consumption and improved integration with mobile and digital ecosystems, positioning the technology as a critical enabler of digital transformation across industries.

Rapid growth in contactless payment transactions is directly boosting demand for smart card ICs that support NFC and dual‑interface capabilities. For example, transaction volumes rose from about 4.7 billion in 2019 to ~11.1 billion in 2021 in one major region, prompting issuers to migrate to smart‑card ICs with enhanced security features. Smart card ICs embedded in contactless cards enable faster tap‑and‑go processing and reduce fraud risk by leveraging cryptographic encryption engines rather than simple memory chips. As merchants and card‑issuers upgrade infrastructure, smart card IC manufacturers are scaling production of chips with integrated secure‑elements to meet this demand.

The rise of mobile wallet solutions, eSIM tokens and host‑card emulation reduces reliance on physical smart cards in certain use‑cases. In emerging markets, cost‑sensitive consumers prefer software‑only authentication rather than issuing smart cards with advanced ICs, limiting uptake. Moreover, infrastructure‑upgrade costs and legacy card‑replacement expenses pose barriers for smaller issuers to adopt next‑generation smart card ICs. This competitive pressure from non‑card authentication pathways challenges traditional smart card IC vendors to innovate or risk margin erosion.

Smart card IC technology is being leveraged beyond cards and into secure elements for IoT, connected vehicles and access control systems. With predictions such as 5 billion secure‑authentication devices expected by 2028, manufacturers of smart card ICs have an opportunity to expand into modules for device identity and lifecycle security. Military‑grade encryption, ultra-low power consumption (e.g., less than 2 µA standby) and physical‑unclonable‑functions (PUFs) are being adopted. This broadens the market from banking and identity into industrial, automotive and smart‑city domains where card‑form‑factor ICs evolve into embedded secure modules.

Manufacturing advanced smart card ICs with secure microcontrollers, low‑node geometries and integrated biometric modules requires significant investment in fabs, design and certification. Upgrading issuance systems, reader terminals and card‑personalisation equipment adds further capital expenditure for issuers. In cost‑sensitive regions, the incremental cost of a high‑security IC versus a basic memory chip can dampen adoption. Additionally, supply‑chain disruptions, certification delays and regulatory compliance burdens add complexity and cost, keeping some potential buyers from transitioning to advanced smart card ICs quickly.

Expansion of Dual-Interface Smart Cards: The deployment of dual-interface smart cards combining contact and contactless functionality has increased by 42% in 2024 compared to 2022. These cards support secure financial transactions and government ID programs simultaneously, reducing the need for multiple cards per user. Asia-Pacific and Europe are leading regions in adoption, with over 65% of new card issuances leveraging dual-interface ICs.

Integration of Biometric Authentication: Smart card ICs with embedded biometric modules have grown by 38% in issuance across government and financial sectors in 2024. On-chip fingerprint or facial recognition enhances security while minimizing transaction errors, achieving up to 20% faster authentication times than traditional PIN-based systems. North America and East Asia have implemented these solutions in over 50% of high-security ID cards.

Adoption of Low-Power and Ultra-Secure ICs: The production of low-power smart card ICs supporting extended battery-free operation has increased by 47% in 2024. Ultra-secure microcontroller ICs, featuring advanced cryptographic algorithms, have reduced fraudulent card usage by nearly 18% in large-scale banking and transit deployments. Europe has reported a 25% improvement in transaction integrity by integrating these ICs into public transport cards.

Integration with Mobile and IoT Ecosystems: Smart card ICs are increasingly integrated with mobile wallets and IoT-enabled access systems, with deployment in connected devices rising by 33% in 2024. Pilot programs indicate up to 28% reduction in authentication latency when ICs interface with mobile apps or IoT devices. Asia-Pacific dominates in volume integration, while North America leads adoption with 62% of enterprises embedding smart card ICs into multi-application digital solutions.

The Smart Card IC Market is segmented comprehensively by type, application, and end-user, each contributing distinct technological and operational value to the overall ecosystem. The segmentation highlights increasing integration of security technologies with digital payments, identification, and IoT connectivity. By type, the market features microcontroller-based ICs, memory-based ICs, contact, contactless, and dual-interface models. By application, demand spans financial transactions, identity verification, transportation, IoT access management, and consumer authentication. End-user categories include BFSI, government, healthcare, retail, telecom, and transportation sectors. Collectively, these segments reflect how smart card ICs are transitioning from traditional financial systems toward advanced digital authentication and connectivity-driven ecosystems. Adoption trends in Asia-Pacific and Europe remain strong, accounting for over 60% of new smart card integrations, driven by financial inclusion programs and secure identity initiatives.

Microcontroller-based Smart Card ICs dominate the market, holding approximately 52.5% share in 2024, supported by advanced encryption standards, multi-application capability, and strong adoption in e-passports, SIM cards, and payment solutions. Memory-based ICs account for about 31% of total installations, primarily serving prepaid and basic ID card functions where data storage is minimal. Contact-based ICs still contribute around 33% of units deployed, largely in legacy financial infrastructure; however, the shift toward contactless and dual-interface ICs is reshaping market momentum. Contactless ICs are projected to register a 7.8% CAGR, driven by rapid expansion in NFC-enabled payment systems and public transport applications. Dual-interface ICs are gaining traction in Europe and Asia, providing interoperability between offline and contactless ecosystems. Additionally, next-generation ICs featuring post-quantum encryption and energy-efficient architectures are becoming central to IoT device authentication and biometric payment innovations.

Payment and financial transaction cards represent the leading application, accounting for nearly 43% of the Smart Card IC market in 2024, driven by continued growth in debit, credit, and prepaid card circulation globally. Government and national identification programs constitute the second-largest segment, holding around 22%, with large-scale deployments across e-passports and digital IDs enhancing cross-border security. Transportation and access control applications represent nearly 18% of total usage, fueled by contactless fare systems and mobile ticketing expansion across major cities in Asia and Europe. The fastest-growing segment is IoT and connected device authentication, projected to grow at an annual rate exceeding 8.2%, as enterprises adopt secure embedded ICs for endpoint verification in smart home and industrial automation systems. Other applications, including healthcare and retail loyalty programs, collectively contribute about 17% of demand.

The BFSI sector remains the largest end-user, commanding approximately 46% of Smart Card IC adoption in 2024, led by banking institutions, payment networks, and fintechs adopting EMV-compliant solutions for secure transactions. The government and public sector follows closely with around 25% share, driven by national e-ID and biometric passport projects. Healthcare and telecommunications industries together hold about 17%, utilizing ICs for patient data access cards and SIM authentication systems. The retail and transportation sectors collectively contribute around 12%, increasingly integrating smart card ICs into loyalty and transit systems. The fastest-growing end-user group is telecommunication, expected to grow at a 9.1% CAGR, owing to expanding 5G-enabled SIM and eSIM deployments supporting secure connectivity.

Asia-Pacific accounted for the largest market share at 41.2% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2025 and 2032.

The dominance of Asia-Pacific is supported by mass deployment of SIM and banking cards in China, India, and Japan, with over 5.6 billion active smart cards circulating in the region. North America followed with approximately 26.5% share, driven by strong enterprise adoption in BFSI and healthcare. Europe captured 21.7%, boosted by government-backed e-ID programs and EMV-compliant payment cards, while South America and the Middle East & Africa collectively accounted for 10.6%, reflecting steady growth in transit systems and telecom expansion. Cross-regional analysis shows that over 68% of total demand originates from urban centers, with growing rural penetration expected through digital inclusion policies.

How Is Advanced Authentication Driving Next-Generation Smart Card IC Adoption?

North America represents about 26.5% of the global Smart Card IC market in 2024, led by strong penetration in banking, healthcare, and telecommunications. Regulatory initiatives supporting EMV compliance and secure patient identification are significantly enhancing IC demand. The region benefits from rapid digital transformation and adoption of biometric authentication, particularly across the U.S. and Canada. Key industries driving demand include BFSI, public transport, and enterprise security systems. Local manufacturers and solution providers are investing in embedded secure elements and contactless infrastructure modernization. For example, a major U.S. smart card manufacturer integrated 5G-enabled secure ICs into SIM cards to strengthen authentication across IoT devices. Consumer behavior in North America shows higher enterprise adoption rates in healthcare and finance, with over 62% of institutions using dual-interface cards for secure transactions and digital identity verification.

Why Are Regulatory Frameworks Accelerating Secure IC Adoption Across Enterprises?

Europe holds approximately 21.7% share of the Smart Card IC market in 2024, with major contributions from Germany, the UK, and France. The market is propelled by the implementation of e-IDAS and GDPR-compliant authentication solutions, encouraging the use of high-security ICs in payment, identity verification, and transport systems. Sustainability-oriented initiatives across the European Union are supporting the transition toward eco-friendly chip manufacturing processes and recyclable card materials. Local players are actively innovating—one European semiconductor firm recently expanded its dual-interface IC production capacity to 180 million units annually to meet demand for EMV and national ID cards. Regulatory emphasis on transparency and explainable security systems continues to shape consumer preference, with 57% of European users prioritizing security certification before digital card adoption.

How Is Digitalization and Fintech Expansion Transforming the Regional IC Landscape?

Asia-Pacific leads the Smart Card IC market with an estimated 41.2% share in 2024, driven by widespread issuance of SIM, banking, and government ID cards across China, India, Japan, and South Korea. Over 5.6 billion smart cards are in circulation, representing the highest deployment volume globally. Rapid fintech expansion, coupled with national digital identity initiatives, is fostering high-volume IC demand. Manufacturing hubs in China and Taiwan dominate chip production, accounting for over 60% of global IC output. In India, initiatives such as biometric e-KYC and Aadhaar-linked payment solutions are driving large-scale adoption. Local innovation centers in Shenzhen and Tokyo are leading advancements in NFC and low-power IC architectures. Consumer behavior across Asia-Pacific shows a high preference for mobile payments—72% of users prefer contactless transactions for convenience and security.

Is Fintech Growth Reshaping Security Infrastructure Across Emerging Economies?

South America accounts for approximately 6.3% of the Smart Card IC market in 2024, led by Brazil and Argentina, where digital payment and telecom growth continue to accelerate. The region is witnessing an increase in EMV card issuance, mobile banking adoption, and transit system modernization. Government incentives promoting financial inclusion and digital ID frameworks are stimulating IC demand. Regional telecom providers are expanding secure SIM-based services, while local fintech startups are integrating embedded ICs for authentication in digital wallets. For example, a leading Brazilian fintech introduced secure IC-powered prepaid cards, enhancing transaction reliability for over 1.5 million users. Consumer behavior emphasizes convenience, with 58% of South American users adopting contactless payments for small-value retail transactions.

Can Infrastructure Modernization and Digital Governance Fuel Next-Stage IC Deployment?

The Middle East & Africa region holds an estimated 4.3% share of the global Smart Card IC market in 2024, led by countries such as the UAE, Saudi Arabia, and South Africa. Growing demand from oil & gas, banking, and government sectors is shaping market expansion, with digital governance projects boosting secure identity and payment solutions. National e-ID programs and smart transportation systems are increasing IC consumption, particularly in GCC economies. Regional semiconductor distributors are forming partnerships to enhance local card personalization facilities. For instance, a UAE-based technology provider integrated advanced contactless ICs into public transit cards, reducing passenger verification time by 33%. Consumer adoption patterns show increasing digital trust, with 65% of enterprises in the region prioritizing smart card integration for secure authentication in both financial and industrial applications.

China – 28.6% Market Share: Dominates the Smart Card IC market due to large-scale chip manufacturing capacity, government-backed e-ID programs, and rapid fintech expansion supporting high-volume demand.

United States – 19.4% Market Share: Leads in innovation and adoption of advanced authentication ICs, with strong penetration across BFSI and healthcare sectors, supported by robust digital infrastructure and regulatory modernization.

The global Smart Card IC market is moderately consolidated, with the top five players collectively accounting for approximately 61% of the total market share in 2024. Around 30–35 active global competitors operate across various segments, including contact-based, contactless, and dual-interface ICs. Market leaders maintain strong vertical integration in semiconductor manufacturing and security algorithm design, while mid-tier firms focus on application-specific solutions for telecom, BFSI, and e-governance sectors. Strategic initiatives such as AI-integrated encryption, 5G-compatible secure elements, and quantum-resistant chipsets are reshaping competitive positioning. Between 2023 and 2024, the market witnessed over 18 strategic partnerships and 10 new product launches, emphasizing enhanced security and sustainability through recyclable materials and energy-efficient chip production. Asia-Pacific players dominate production capacity, while North American and European firms lead in design innovation and security compliance. The competitive environment is shifting toward collaborative ecosystems involving fintech, IoT, and mobility solution providers. Continuous investments in R&D, accounting for nearly 7.2% of total annual revenue among leading firms, indicate a clear focus on developing advanced architectures to meet evolving cybersecurity and regulatory demands globally.

Microchip Technology Inc.

STMicroelectronics N.V.

Texas Instruments Incorporated

Renesas Electronics Corporation

Giesecke+Devrient GmbH

Thales Group

Shanghai Huahong Integrated Circuit Co., Ltd.

IDEMIA

Watchdata Technologies Co., Ltd.

Intel Corporation

Onsemi

CEC Huada Electronic Design Co., Ltd.

Technological innovation within the Smart Card IC market is advancing rapidly, driven by demand for secure, high-performance, and multifunctional chip solutions. The ongoing transition from 8-bit and 16-bit architectures to 32-bit microcontroller-based ICs, now representing nearly 58% of global deployments, enables faster data processing, enhanced encryption, and broader interoperability across payment, telecom, and e-government systems. Additionally, embedded secure elements (eSE) and System-on-Chip (SoC) designs are being increasingly integrated into smart devices, providing compact, tamper-resistant authentication solutions essential for IoT ecosystems and digital ID programs.

Contactless and dual-interface ICs are also witnessing high technological uptake, with NFC-enabled solutions accounting for about 47% of newly manufactured cards in 2024, up from 36% in 2021. These chips support instant transactions and remote data synchronization, key to mobile banking, retail, and public transit applications. The integration of biometric verification, such as fingerprint or facial recognition modules, has expanded across over 65 million smart ID and payment cards, improving authentication reliability and reducing fraud risk.

Emerging technologies like quantum-resistant cryptography and AI-enhanced security algorithms are defining the next innovation wave, enabling real-time threat detection and automated encryption key management. Furthermore, green semiconductor fabrication, emphasizing recyclable substrates and reduced energy consumption by up to 22% per chip, aligns with global ESG commitments. As enterprises accelerate digital identity frameworks and cross-border payment platforms, the Smart Card IC industry continues to evolve into a foundational technology hub for secure connectivity and sustainable digital transformation worldwide.

In November 2024, NXP Semiconductors N.V. launched its MIFARE DUOX contactless NFC IC which combines asymmetric and symmetric cryptography in a single chip, enhancing secure mobile access and enabling up to 40 % faster authentication times compared to previous generations.

In December 2024, Infineon Technologies AG reported deployment of its 28 nm smart-card technology across over 1 billion devices by spring 2025, with more than 100 customer designs already approved in payment, ID and transportation segments.

In November 2024, Infineon showcased its SECORA Pay and Coil-on-Module (CoM) platforms at a major industry forum, demonstrating contactless smart cards produced at 30 % lower processing time while maintaining certified security for wearable payments and transit tokens.

In late 2024, with the release of NXP’s ICODE 3 tag IC (July 2024 introduction) featuring fast read rates of up to 212 kbit/s and data retention of 50 years, smart-card IC manufacturers are extending features from cards to smart-tags and IoT applications, diversifying product lines.

The Smart Card IC Market Report encompasses a comprehensive analysis of the semiconductor chips embedded within payment cards, identity credentials, transit tokens and connected-device security modules. It covers the full gamut of type segmentation—including memory-only ICs, microcontroller-based ICs, contact, contactless and dual-interface modules—alongside architectures ranging from 8-bit through 32-bit and next-generation secure controllers. Application areas addressed in the scope include financial cards (debit, credit, prepaid), national ID and e-passport programs, transportation fare systems, SIM/eSIM credentials and IoT-device authentication. Geographic coverage spans North America, Europe, Asia-Pacific, South America and Middle East & Africa, detailing regional production hubs, end-user uptake and infrastructure readiness. The report further evaluates industry focus areas such as banking & financial services, government & public sector, telecommunications, transportation, retail & loyalty schemes and enterprise access control. Emerging or niche segments examined include biometric-enabled smart cards, wearable payment tokens, secure modules for eSIM/5G device onboarding and embedded card-form-factor chips for smart-city applications. It also analyses technology trends—secure elements, post-quantum cryptography, low-power/green packaging—and competitive dynamics, offering decision-makers insight into vendor positioning, supply-chain shifts, certification timelines and migration strategies. The report’s breadth ensures stakeholders can benchmark region-wise demand patterns, align product investment decisions with interface and architecture shifts, and monitor how emerging use-cases are expanding the addressable market beyond conventional card issuance.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 335455.7 Million |

Market Revenue in 2032 | USD 576375.34 Million |

CAGR (2025 - 2032) | 7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Infineon Technologies AG, NXP Semiconductors N.V., Samsung Electronics Co., Ltd., Microchip Technology Inc., STMicroelectronics N.V., Texas Instruments Incorporated, Renesas Electronics Corporation, Giesecke+Devrient GmbH, Thales Group, Shanghai Huahong Integrated Circuit Co., Ltd., IDEMIA, Watchdata Technologies Co., Ltd., Intel Corporation, Onsemi, CEC Huada Electronic Design Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |