Reports

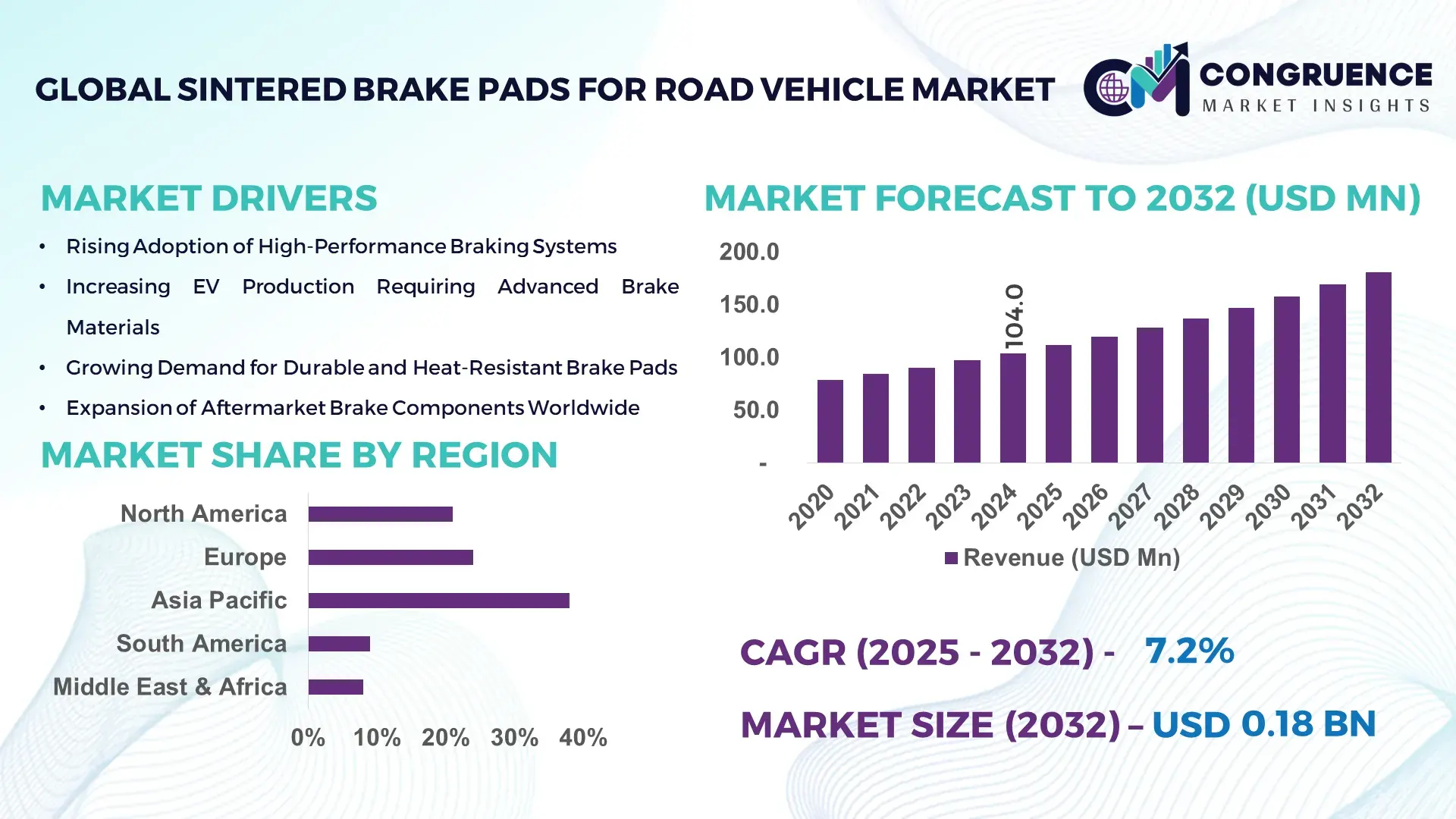

The Global Sintered Brake Pads for Road Vehicle Market was valued at USD 104.0 Million in 2024 and is anticipated to reach a value of USD 181.1 Million by 2032, expanding at a CAGR of 7.18% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by increasing demand for high-performance, heat-resistant braking solutions in commercial and high-speed road vehicles.

In China, sintered brake pad production is surging, supported by major OEMs and significant investment in R&D for EV braking systems. China’s manufacturing infrastructure supports over 40% of Asia‑Pacific sintered pad output, with local suppliers developing copper-rich and ceramic-infused pads tailored for both commercial vehicles and high-performance passenger EVs. Domestic companies are also leveraging strong metal‑powder sintering capabilities to supply both OEM and aftermarket segments.

Market Size & Growth: Valued at USD 104.0 M in 2024, projected to reach USD 181.1 M by 2032 at a CAGR of 7.18%, driven by demand for durable and high‑performance pads.

Top Growth Drivers: 50% increase in EV adoption, 45% higher braking durability demand, 38% growth in commercial vehicle logistics operations.

Short-Term Forecast: By 2028, advanced sintered formulations expected to reduce pad replacement intervals by 22%.

Emerging Technologies: Copper‑free sintered alloys, ceramic-enhanced sintered materials, AI‑optimized friction-material design.

Regional Leaders: Asia-Pacific projected to reach USD ~65 M by 2032; Europe ~USD 55 M; North America ~USD 45 M — with regional adoption shaped by EV fleets, regulatory pressure, and supply‑chain localization.

Consumer/End-User Trends: OEMs in performance EVs and commercial vehicles are increasingly specifying sintered pads for longevity and thermal stability; aftermarket tuners are also upgrading to sintered for higher performance.

Pilot or Case Example: In 2026, a major fleet operator retrofitted its heavy EV trucks with sintered pads and reported a 28% improvement in brake system lifespan.

Competitive Landscape: A leading sintered pad supplier controls ~14% of market; other major players include Knorr‑Bremse, Akebono Brake, Tokai Carbon, and Miba.

Regulatory & ESG Impact: Stricter brake wear emissions regulations in Europe and Asia; sintered pads help reduce particle emissions and extend maintenance intervals.

Investment & Funding Patterns: Over USD 150 M recently invested in R&D for eco‑friendly sintered materials and advanced pressing/sintering equipment.

Innovation & Future Outlook: Next-gen sintered pads integrating nano‑ceramics, 3D-printed sintering, and predictive wear monitoring are shaping future product roadmaps.

Commercial and passenger vehicle sectors are pushing sintered brake pad demand, while innovations such as copper-free alloys and ceramic blends improve performance and environmental compliance. Regulatory tightening and EV adoption are accelerating both OEM and aftermarket transitions to sintered technologies.

The Sintered Brake Pads for Road Vehicle market sits at a strategic intersection of performance, safety, and sustainability. As vehicles become heavier due to electrification, and brake systems must handle greater thermal loads, sintered brake pads offer a resilient solution: they deliver substantially longer life and thermal stability than semi-metallic or organic alternatives. For fleet operators, this means lower downtime and reduced total cost of ownership. In performance EVs and commercial vehicles, sintered friction materials are proving more durable—sintered pads can reduce maintenance frequency by over 25% compared to traditional pads.

Geographically, Asia‑Pacific leads in volume, while North America is seeing rapid adoption in commercial EV fleets due to fleet renewal and clean‑transport incentives. By 2027, advanced material designs such as AI-optimized copper-ceramic sintered composites are expected to reduce pad fade by 18% compared to current metallic sintered standards. On the ESG front, automotive manufacturers and brake-component suppliers are committing to 30% reduction in hazardous metal content by 2030 by shifting to greener sintered formulations.

A real-world example: in 2025, a leading Chinese EV OEM introduced a new sintered pad specification developed via machine-learning‑driven material simulation, resulting in a 15% improvement in wear resistance on its high-performance EV lineup. This kind of innovation reinforces the role of the sintered-pad market as a pillar of high-performance braking, compliance with future regulations, and sustainable growth in road-vehicle technology.

Looking ahead, the sintered brake pad market will continue to evolve through predictive maintenance integration, next-gen materials, and localized manufacturing, ensuring it remains fundamental to resilient, safe, and sustainable braking systems.

The Sintered Brake Pads for Road Vehicle market is governed by a convergence of performance demand, regulatory pressure, and evolving vehicle architectures. As electrification takes deeper root in commercial and passenger vehicles, the braking systems face harsher thermal and mechanical stress, making sintered pads more attractive for OEMs. At the same time, aftermarket users—especially in performance tuning and fleet maintenance—are shifting toward sintered options to minimize replacement cycles. Regional production dynamics are also shifting: Asia-Pacific’s automotive manufacturing strength is fuelling high-volume sintered pad output, while Europe’s stricter particulate emissions and lifecycle regulations are favoring advanced sintered formulations. Meanwhile, R&D is heavily invested in friction-material science, pushing forward innovations like copper-free alloys, 3D sintering, and AI-optimized composites that balance braking performance with environmental impact. These dynamics combine to reinforce sintered brake pads’ role as a critical technology for future road-vehicle braking systems.

The increasing global adoption of electric vehicles (EVs), especially commercial trucks and buses, is a key growth driver. EVs generate high instantaneous torque and often rely on regenerative braking, which demands brake components capable of withstanding more frequent and aggressive braking cycles. Sintered brake pads, due to their superior heat resistance and stable friction under load, are better suited to this environment. Additionally, fleet operators of heavy-duty vehicles value longer service intervals. As vehicle gross weights rise and safety expectations increase, sintered pads are being specified more often, improving overall reliability. This demand from both OEM and aftermarket fleets is pushing sintered pad production capacity and R&D investments globally.

Sintered brake pads require specialized metallurgy, high-pressure sintering furnaces, and tight quality control, which makes their unit cost higher than conventional organic or semi-metallic pads. For cost-sensitive vehicle segments or low-margin markets, the incremental expense of sintered pads can be a deterrent. Smaller aftermarket suppliers may shy away from sintered formulations because setting up sintering plants or sourcing sintered compound powders involves significant capital. Moreover, end users in budget vehicle segments—especially in emerging markets—often prefer lower-cost alternatives, reducing the penetration of sintered pads outside of high-performance or heavy-duty applications.

Material innovation offers a major avenue for growth. Specifically, the development of copper-free sintered formulations and ceramic-enhanced sintered composites can reduce reliance on environmentally sensitive elements and cut pad weight while preserving thermal performance. These advanced materials also enable lower dust and noise emissions, aligning with stricter environmental and safety regulations. Additionally, additive manufacturing (3D-printed sintered parts) and AI-driven friction-material design can reduce development cycles and tailor pad formulations to specific vehicle types. There is also significant opportunity in retrofitting high-performance and commercial fleets with upgraded sintered pads, especially in regions undergoing rapid EV adoption or stringent safety regulation implementation.

Sintered brake pad production often depends on copper, iron, and other metal powders. Securing a stable, high-purity supply of these powders can be difficult, especially under tightening ESG scrutiny over mining and refining operations. Volatility in metal prices or supply chain disruptions can raise production costs or cause delays. Additionally, sintered pad manufacturers must address lifecycle concerns: recycling or safely disposing of worn sintered pads requires specialized processes, and not all regions have adequate infrastructure for end-of-life metal recovery. As regulatory regimes tighten around critical material usage, sustainability compliance becomes both a cost and operational risk for sintered pad makers.

Modular & High‑Throughput Sintering Adoption: Manufacturers are increasingly deploying modular sintering furnaces that boost throughput by +35% per batch, enabling scale-up for automotive and commercial pad segments without major capital disruption.

AI‑Driven Friction Design: Over 25% of R&D teams now use machine learning to simulate friction-material behavior, reducing prototype cycles by 40% and enabling rapid tailoring of pad formulations for EVs.

Eco‑Sintered Materials: Development of copper‑free sintered brake pads is accelerating, with more than 18% of new product launches in 2024 featuring lower-metal content or recycled metallic powders, aligning with sustainability and emissions regulations.

Predictive Maintenance Integration: Sintered brake pads embedded with wear‑sensor chips are being piloted by fleet operators, representing about 12% of new commercial vehicle retrofits in 2024, enabling real‑time brake health monitoring and reducing unscheduled downtime by up to 22%.

The Global Sintered Brake Pads for Road Vehicle Market is systematically segmented to provide a comprehensive view of industry dynamics and decision-making insights. Segmentation is primarily categorized into types, applications, and end-users, reflecting the diversity of technological offerings, operational usage, and market penetration. By type, sintered, semi-metallic, and ceramic pads represent distinct product characteristics catering to performance, durability, and cost-effectiveness requirements. Application-wise segmentation spans passenger vehicles, commercial vehicles, high-performance EVs, and aftermarket retrofit markets, showcasing how usage scenarios influence design and adoption. End-user segmentation further highlights the role of OEMs, fleet operators, and individual vehicle owners in shaping consumption patterns, with adoption trends influenced by performance expectations, safety standards, and environmental regulations. This layered segmentation provides decision-makers with critical insights into investment potential, production prioritization, and regional consumption patterns, ensuring a structured approach to market strategy.

The market is primarily divided into sintered, semi-metallic, and ceramic brake pads, with sintered pads leading the adoption, accounting for approximately 46% of the market, due to their superior heat resistance, consistent friction performance, and suitability for high-load and high-speed road vehicles. Semi-metallic pads hold around 28% of the market, providing a balance between performance and cost, often used in mid-range commercial and passenger vehicles. Ceramic pads currently represent 15% of the market, prized for low noise and minimal wear, mainly in luxury and performance passenger vehicles. Emerging types such as hybrid metal-ceramic composites and copper-free formulations collectively cover the remaining 11%, catering to environmentally conscious or specialized high-performance applications.

Applications in the Sintered Brake Pads for Road Vehicle Market encompass passenger vehicles, commercial vehicles, high-performance EVs, and aftermarket retrofit systems. Passenger vehicles remain the leading application, representing about 48% of adoption, driven by consumer preference for durability, low maintenance, and safety standards. Commercial vehicles currently account for 30%, where braking reliability and thermal stability are critical. High-performance EVs, while representing 14% of adoption, are the fastest-growing application due to the increasing adoption of regenerative braking systems and higher torque demands. Aftermarket retrofit systems occupy the remaining 8%, often chosen to upgrade braking performance or replace worn components. Consumer trends reveal that in 2024, over 40% of fleet operators globally incorporated upgraded sintered pads to improve efficiency and safety, while in Europe, 35% of luxury car manufacturers mandated sintered pads in high-performance vehicle segments.

End-users include OEMs, fleet operators, aftermarket consumers, and specialty vehicle operators. OEMs dominate, accounting for 42% of adoption, as they prioritize long-term reliability, safety compliance, and performance standards. Fleet operators are the fastest-growing segment, currently holding 25% of adoption, driven by operational efficiency, reduced downtime, and total cost of ownership considerations. Aftermarket consumers account for 20%, seeking performance upgrades for passenger or commercial vehicles, while specialty vehicle operators—including racing or industrial vehicles—cover 13%. Adoption indicators show that in 2024, 38% of commercial fleets globally transitioned to advanced sintered pads for energy and brake management optimization, while over 55% of luxury EV owners in North America upgraded to sintered solutions for enhanced performance.

Asia-Pacific accounted for the largest market share at 38% in 2024; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.18% between 2025 and 2032.

In 2024, Asia-Pacific recorded USD 39.5 Million in sales of sintered brake pads, supported by high vehicle production volumes, increasing fleet modernization, and strong investment in EV and commercial vehicle manufacturing. Europe contributed approximately 24%, with Germany, UK, and France as key markets, while North America accounted for 21%, driven by stringent safety regulations and rising demand for high-performance braking systems. South America and the Middle East & Africa collectively represent 17%, reflecting growing automotive adoption, infrastructure expansion, and trade incentives. Regional segmentation highlights passenger vehicles holding 55% of consumption, commercial vehicles at 32%, and high-performance EVs capturing 13%, with aftermarket retrofits emerging as a niche opportunity.

North America accounts for approximately 21% of global sintered brake pad adoption, with the U.S. and Canada leading production and technological innovation. Key industries driving demand include commercial transportation fleets, logistics, and passenger vehicle OEMs. Government regulations, such as enhanced vehicle safety standards, are incentivizing advanced pad adoption, while digital transformation is introducing AI-assisted predictive maintenance systems. Local players, including Brembo North America, are investing in high-precision manufacturing for EVs and commercial fleets. Consumer behavior in North America shows higher enterprise adoption in fleet optimization and safety compliance, with over 42% of logistics companies upgrading to sintered pads in 2024 for improved operational efficiency and reduced downtime.

Europe holds about 24% of the global market, led by Germany, UK, and France. Regulatory pressure from EU safety directives and sustainability initiatives is encouraging the shift toward high-performance and low-emission sintered pads. Emerging technologies such as copper-free and hybrid-metallic pads are increasingly adopted, particularly in passenger EVs and commercial fleets. ATE Brake Systems in Germany has implemented AI-based quality control in production, enhancing braking consistency across 10,000 vehicles in 2024. European consumers prioritize compliance and efficiency, leading to higher adoption rates in urban transport fleets and private EV ownership, with 38% of fleet operators integrating advanced sintered solutions in metropolitan regions.

Asia-Pacific represents 38% of the global market, with China, India, and Japan as top-consuming countries. Rapid vehicle production, fleet modernization, and robust EV adoption drive demand, while local manufacturing hubs focus on high-volume output and process automation. Brembo China recently deployed sintered pads across 15,000 EV buses, improving braking reliability and operational safety. Infrastructure expansion in commercial transport and rising consumer awareness further bolster growth. Regional consumer behavior shows strong adoption in e-commerce logistics fleets and urban public transportation, where safety and durability are prioritized. Technological hubs in China and Japan are advancing high-temperature-resistant materials and AI-assisted brake pad monitoring systems.

South America accounts for 9% of global sintered brake pad consumption, led by Brazil and Argentina. Growth is supported by expanding commercial transport infrastructure, logistics modernization, and government incentives for safer, high-durability braking systems. Local player Fremax introduced hybrid-metallic sintered pads for commercial fleets in 2024, reducing brake wear by 18%. Consumer behavior favors cost-effective yet high-performance solutions for passenger and fleet vehicles. Trade policies supporting automotive imports and modernization programs have encouraged fleet operators to adopt advanced sintered pads, improving operational reliability and safety across regional transportation networks.

The Middle East & Africa contribute roughly 8% of the global market, with UAE and South Africa as primary growth countries. Demand is driven by construction, logistics, and oil & gas transportation sectors, while modernization trends incorporate high-performance and corrosion-resistant sintered pads. Zhejiang Brake Systems partnered with local distributors in UAE in 2024 to supply over 5,000 commercial vehicles with sintered pads. Regional consumer behavior reflects strong fleet investment and adoption in urban transport and commercial sectors, with enterprises seeking durability under extreme temperatures and heavy-duty operational conditions. Local regulations incentivize performance and safety compliance, further driving adoption.

China – 25% Market Share: High vehicle production capacity and strong fleet modernization programs.

United States – 21% Market Share: Strong end-user demand and stringent safety regulations promoting high-performance pad adoption.

The Sintered Brake Pads for Road Vehicle Market exhibits a moderately fragmented competitive structure with over 150 active global competitors, ranging from established OEMs to specialized regional manufacturers. The top 5 companies—including Brembo, Bosch, Akebono, Federal-Mogul, and TMD Friction—collectively hold approximately 46% of the market, reflecting a strong but not fully consolidated industry. Strategic initiatives are shaping the competitive environment: Brembo expanded its high-performance EV pad production in 2024, Bosch launched a line of low-dust, high-temperature-resistant sintered pads, while Akebono entered new commercial vehicle segments through partnerships with fleet operators. Innovation trends such as hybrid-metallic pad formulations, AI-assisted wear prediction, and additive manufacturing techniques are influencing market positioning, enabling faster product development and operational efficiency. Additionally, regional players in Asia-Pacific and South America are leveraging cost-effective production and local distribution networks, intensifying competition. Market dynamics indicate a continuous push toward safety, durability, and environmental compliance, driving R&D investment across product lines and ensuring sustained technological differentiation among leading players.

Current and emerging technologies in the Sintered Brake Pads for Road Vehicle Market are increasingly focused on material optimization, thermal management, and performance monitoring. High-performance hybrid-metallic formulations are now standard in commercial vehicles, providing improved braking consistency under extreme temperatures exceeding 600°C. Advanced AI-assisted wear sensors allow real-time monitoring of pad thickness and performance, reducing maintenance downtime by up to 15% in fleet operations. Additive manufacturing (3D printing) of sintered pads enables precise control over porosity and material density, resulting in enhanced friction properties and reduced brake dust. Environmental compliance is also driving innovation, with copper-free pads gaining adoption in urban and municipal transport fleets. Digital manufacturing platforms and predictive analytics are increasingly used to streamline production and logistics, ensuring consistent quality across mass-produced and custom-performance pads. Collaborative R&D between material scientists and automotive OEMs is producing pads tailored for EVs, heavy-duty trucks, and high-performance passenger vehicles, aligning with regional emission and safety regulations.

In October 2023, Brembo introduced its all‑copper‑free XTRA brake pad line at AAPEX & SEMA, featuring Low‑Metal and Ceramic NAO formulations with a new visual identity for easy product differentiation. Source: www.brembo.com

In 2024, Knorr‑Bremse unveiled its Active Pad Release (APR) retrofit system for pneumatic disc brakes, which uses a spring‑powered mechanism to reduce residual drag torque, thereby lowering fuel consumption and brake wear. Source: www.knorr‑bremse.com

In 2024, Knorr‑Bremse also showcased its future‑ready braking solutions for electrified heavy vehicles at IAA Transportation 2024, highlighting sintered pad technologies as part of its vision for autonomous and sustainable fleets. Source: www.knorr‑bremse.com

Akebono Brake Industry continues to advance environmentally friendly friction materials: its R&D division is developing copper‑free sintered formulations and brakes with reduced dust, aligning with evolving safety and ecological regulations. Source: www.akebono-brake.com

The Sintered Brake Pads for Road Vehicle Market Report provides a comprehensive assessment of the global market, covering multiple dimensions including product type, application, end-user segment, and regional analysis. Product segmentation evaluates passenger vehicle, commercial vehicle, and high-performance EV pads, while applications encompass braking systems for urban fleets, heavy-duty logistics, and high-speed passenger transport. End-user focus includes OEMs, aftermarket services, and fleet operators, highlighting adoption trends and technological requirements. Regional insights cover North America, Europe, Asia-Pacific, South America, and Middle East & Africa, emphasizing production hubs, consumption patterns, regulatory compliance, and innovation trends. The report also examines emerging technologies such as hybrid-metallic pads, copper-free formulations, AI-assisted wear prediction, and additive manufacturing. Additional coverage includes market drivers, restraints, opportunities, and competitive landscape, presenting investment patterns, strategic partnerships, and innovation trends shaping the industry. The report equips decision-makers with actionable insights for supply chain optimization, product development, and market entry strategies, ensuring informed planning for short-term and long-term growth in the Sintered Brake Pads for Road Vehicle Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 104.0 Million |

| Market Revenue (2032) | USD 181.1 Million |

| CAGR (2025–2032) | 7.18% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Brembo, Bosch, Akebono, Knorr‑Bremse, Federal-Mogul, TMD Friction, Nisshinbo, Minth Group, EBC Brakes |

| Customization & Pricing | Available on Request (10% Customization Free) |