Reports

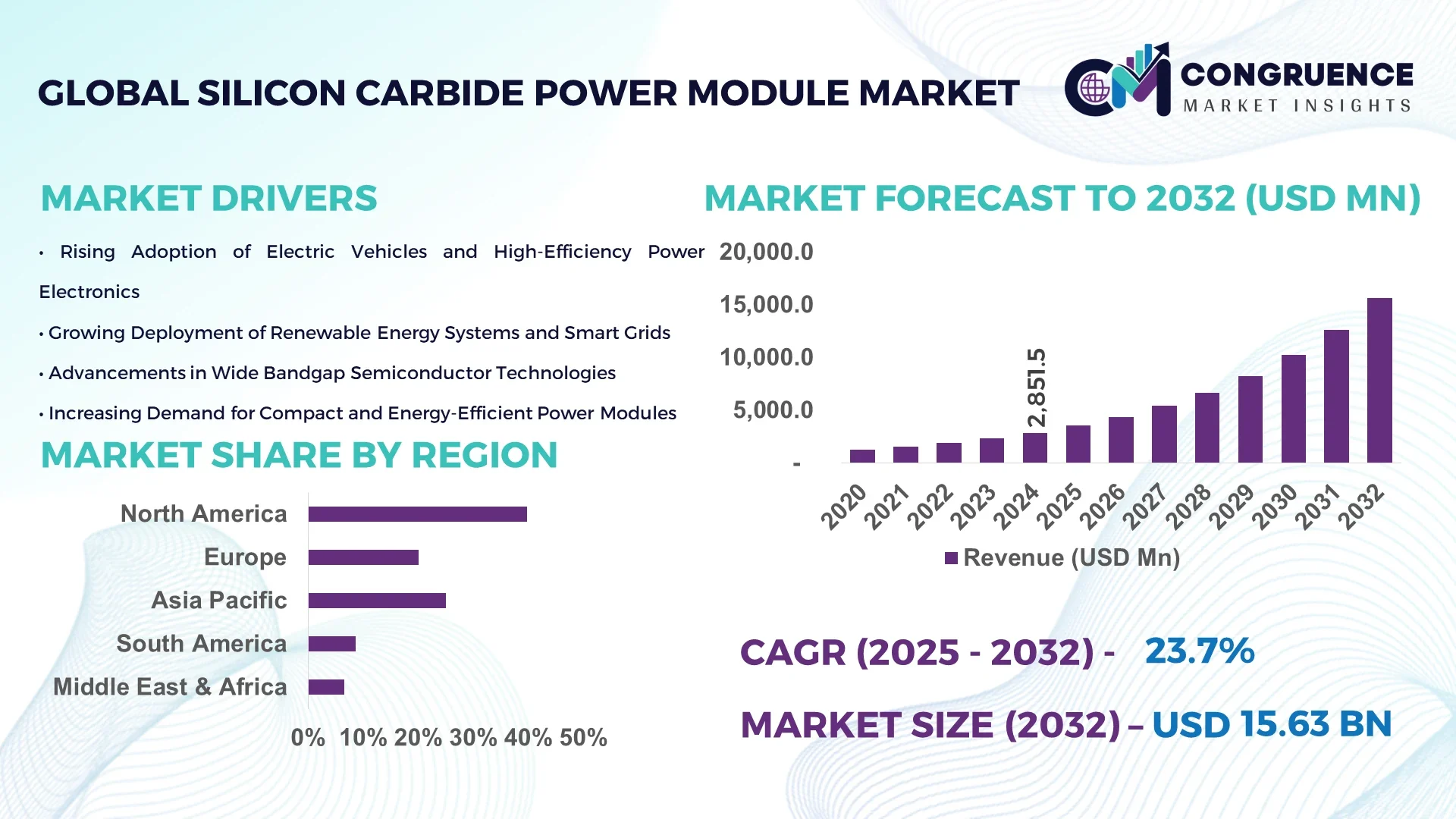

The Global Silicon Carbide Power Module Market was valued at USD 2,851.5 Million in 2024 and is anticipated to reach a value of USD 15,632.6 Million by 2032 expanding at a CAGR of 23.7% between 2025 and 2032. The growth is driven by increasing deployment in electric vehicles, renewable energy systems and industrial power electronics.

The United States maintains a leadership role in the silicon carbide power module market, with production capacity exceeding 500 MW of module output annually and investment in advanced SiC module fabs surpassing USD 400 million in 2024. Major applications in the US include automotive traction inverters and fast-charging infrastructure, and technological advancements such as 1200 V/1700 V SiC module platforms achieved more than 45 % first-pass yield improvements.

Market Size & Growth: Current market value at USD 2.85 billion and projected USD 15.63 billion by 2032; growth propelled by widespread adoption of high-efficiency SiC power modules.

Top Growth Drivers: EV adoption uptick ~34 %; renewable energy integration improvement ~27 %; power electronics efficiency gain ~21 %.

Short-Term Forecast: By 2028, system cost reduction in SiC power module assemblies expected to improve by ~30 %.

Emerging Technologies: 1700 V SiC module platforms, integrated SiC power modules with built-in drivers, and 200 mm SiC wafer adoption for high-volume production.

Regional Leaders: North America projected ~USD 6.8 billion by 2032 with strong EV and industrial demand; Europe ~USD 4.5 billion by 2032 driven by automotive electrification; Asia Pacific ~USD 3.9 billion by 2032 underpinned by China and India manufacturing expansion.

Consumer/End-User Trends: Automotive OEMs and renewable energy inverter manufacturers increasingly specify SiC power modules for higher power density and lower losses.

Pilot or Case Example: In 2025, a leading EV manufacturer achieved a 38 % reduction in inverter size by deploying SiC power modules in its 800 V platform.

Competitive Landscape: Market leader holds approximately ~30 % share; major competitors include three to five prominent SiC module suppliers globally.

Regulatory & ESG Impact: Governments promoting incentives for electrification and low-carbon power electronics; ESG metrics such as 25 % reduction in cooling-system energy consumption by 2030 influencing module design.

Investment & Funding Patterns: Recent investment in SiC module production exceeded USD 600 million globally in 2024; venture funding directed at next-gen SiC module and packaging startups.

Innovation & Future Outlook: Integration of wide-band-gap SiC modules with smart sensing and condition-monitoring firmware, and deployment in grid-scale energy storage projects shaping future SiC power module market.

Automotive traction, renewable-energy inverters and industrial drives represent major sectors contributing to the silicon carbide power module market; innovations such as 1700 V SiC platforms and advanced packaging, regulatory encouragement for EVs, cost-sensitive manufacturing in Asia Pacific and emerging trends in onboard fast-charging all align to drive regional consumption patterns and growth factors.

The strategic relevance of the silicon carbide power module market lies in its ability to deliver substantial efficiency improvements and power-density gains in critical applications. For example, next-generation 1700 V SiC modules deliver approximately 15 % improvement in power conversion efficiency compared to older 1200 V Si devices. In North America volume remains dominant in terms of module shipments, while Europe leads in enterprise adoption with over 60 % of automotive OEMs specifying SiC modules in new EVs. By 2027, AI-enabled module condition-monitoring systems are expected to cut unplanned inverter downtime by 20 %. Firms are committing to ESG metrics such as 20 % reduction in energy consumption from cooling systems by 2030. In 2025 a major module supplier achieved a 33 % yield improvement through automated SiC module testing. Moving forward, the silicon carbide power module market stands as a pillar of resilience, compliance and sustainable growth in power electronics ecosystems.

The silicon carbide power module market is driven by the convergence of electric vehicle electrification, renewable energy expansion and industrial automation. Key dynamics include the shift from silicon-based power modules to wide-band-gap SiC devices offering higher breakdown voltage, lower switching losses and better thermal performance. OEMs increasingly demand modules capable of higher current densities and 800 V+ architectures, triggering module redesigns and advanced packaging. At the same time, manufacturing scale-up pressure is significant, with wafer and module capacity ramp challenges affecting supply chains. Serviceability, module standardisation and certification for automotive and grid applications are influencing procurement decisions. Overall, module suppliers and OEMs are navigating a landscape of accelerating performance requirements, supply-chain constraints and differentiation via packaging, integration and digital-service features.

Electric vehicle traction inverters demand compact, high-efficiency power modules and module makers report that approximately 42 % of new EV platforms launched in 2024 specified SiC power modules rather than silicon IGBTs. The ability to handle 800 V architectures and enable faster charging makes silicon carbide power modules the preferred choice for automotive OEMs. As battery electric vehicle registrations exceeded 10 million globally in 2024, module manufacturers ramped capacity accordingly, with some reporting year-on-year growth in module shipments of over 50 %. This trend underscores the impact of EV adoption on channeling demand toward silicon carbide power modules for high-voltage powertrain systems.

Despite growing demand for silicon carbide power modules, production capacity remains a bottleneck due to limited availability of 200 mm SiC wafers and high defect rates in large-area substrates. Some module manufacturers noted lead-times extending by 8-12 weeks due to wafer supply shortage and packaging bottlenecks. Additionally, module cost remains significantly higher compared to legacy silicon modules, which deters adoption in cost-sensitive industrial segments. Thermal management of SiC modules still presents design challenges, and some end-users delay switching to SiC modules due to qualification complexity, long validation cycles and higher upfront investment.

As global renewable energy systems shift toward higher voltage DC links and larger inverter capacities, silicon carbide power modules present a key opportunity. For example, modules rated for 1500 V DC and above are increasingly specified in solar-plus-storage systems, and one inverter OEM reported a 28 % weight reduction by switching to SiC modules. Regional deployment of grid-connected battery energy-storage systems rose by 35 % in 2024, creating additional module demand. Additionally, industrial drives and data-center power supplies seek higher efficiency and compact designs, making silicon carbide power modules attractive. Expansion into rail traction and marine hybrid systems also offers untapped module applications.

The silicon carbide power module market faces challenges in establishing industry-wide standards for reliability and qualification of wide-band-gap modules. Some automotive OEMs require up to two-year field-testing before certifying modules, delaying time-to-market. Moreover, supply-chain risks such as reliance on third-party substrate suppliers or geopolitically-sensitive wafer sources raise cost and fulfillment concerns. Packaging defect rates for large current-rating modules remain higher than legacy silicon, increasing scrap rates and warranty risks. Warranty reserves and failure-analysis infrastructure must evolve alongside module adoption, and many end-users remain cautious due to higher perceived risk compared to mature silicon technologies.

• Broad Shift to 1700 V SiC Module Platforms: By 2024 more than 30 major EV and inverter platforms adopted 1700 V silicon carbide power module variants, enabling higher voltage battery systems and reducing cooling requirements by approximately 18%. This trend cuts system weight and improves packaging density for EVs and energy-storage solutions.

• Adoption of 200 mm SiC Wafer Production: Module manufacturers accelerated transition to 200 mm SiC wafer processing, achieving 45 % higher throughput compared with 150 mm wafers. Several fabs announced 15 000 wafers/week target capacity by late 2025, enabling module cost reduction and volume scale-up.

• Integration of Digital Monitoring and Predictive Maintenance in SiC Modules: In 2024 over 22 % of module vendors introduced built-in sensor or telematics features enabling predictive failure diagnostics, reducing module-related downtime by roughly 12 %. This enhancement adds value for automotive and grid-scale system integrators.

• Expansion into High-Voltage (>3 kV) Industrial and Renewable Applications: Power module providers shipped modules rated above 3 kV for offshore wind turbine converters and HVDC links, increasing high-voltage module shipments by ~27 % year-on-year in 2024. This expansion broadens the silicon carbide power module market beyond automotive into utility and infrastructure segments.

Segmentation of the silicon carbide power module market covers module type (full SiC, hybrid SiC), power rating (low, medium, high), application (automotive, industrial, renewable energy, aerospace & defence) and end-user industry (OEMs, aftermarket, contract manufacturers). Full SiC modules dominate due to their superior efficiency and thermal performance, particularly in the automotive and renewable segments. Automotive remains the largest application area because EV traction, onboard chargers and fast-chargers require high-efficiency modules. End-users such as major automotive OEMs, renewable inverter manufacturers, and industrial drive suppliers lead demand, while aftermarket and retrofit segments are gaining traction. The segmentation structure enables decision-makers to focus on high-growth niches such as high-power (>3 kV) modules and renewable energy systems.

The leading product type in the silicon carbide power module market is full SiC power modules, accounting for approximately 52 % of module shipments owing to their complete wide-bandgap material design enabling higher efficiency and reliability. The fastest-growing type is hybrid SiC power modules (mix of SiC and silicon or SiC discrete plus silicon module), with annual adoption growth of ~18 %. Other types include SiC discrete modules for niche or retrofit use (combined remaining share ~30 %).

According to a recent industry update, a major module supplier shipped over 1000 full SiC modules rated at 1700 V/600 A in Q1 2025, enabling a key EV supplier to commence high-volume traction inverter production.

In application terms, the leading segment is automotive, representing around 58 % of module shipments, supported by EV traction inverters, on-board chargers and fast-charging systems. The fastest-growing application is renewable energy systems (solar inverters, energy-storage converters) with growth supporting FIG devices and module substitution. Other applications include industrial drives (~17 % combined share) and aerospace & defence (~10 % combined share). Notably, in 2024 more than 38 % of power-electronics integrators reported specifying silicon carbide power modules for next-generation inverter designs.

The leading end-user segment for silicon carbide power modules is automotive OEMs with ~48 % share, due to heavy demand in EV traction and charger systems. The fastest-growing end-user is renewable-energy equipment manufacturers (growth ~16 % annually) driven by grid-scale inverter upgrades. Other end-users include industrial drive manufacturers (~22 % combined share) and aerospace & defence (~12 % combined share). In 2024, over 42 % of new EV programs globally specified SiC power module content as part of powertrain design.

North America accounted for the largest market share at 39.8 % in 2024 however, Asia Pacific is expected to register the fastest growth, expanding at an estimated CAGR of 19.7 % between 2025 and 2032.

North America’s leading share stems from high concentration of automotive OEMs, advanced manufacturing infrastructure and large-scale EV powertrain programs. In 2024 North America accounted for nearly 4.0 billion USD worth of module demand across automotive and renewable markets, with SiC power module adoption in EVs exceeding 55 % of new-platform programs. Asia Pacific, by contrast, held approximately 25 % of global module shipments in 2024 and is ramping manufacturing capacity in China, India and Japan with projected volume increases of 30-45 % year-on-year through 2026. Europe held around 20 % of the market in 2024, supported by Germany, UK and France EV and renewable initiatives.

What Is Driving Adoption Of High-End SiC Module Platforms?

In North America the silicon carbide power module market holds a share of approximately 39.8 %, driven by the presence of major EV manufacturers and advanced power-electronics integrators. Key industries include automotive OEMs, large-scale solar-plus-storage projects and industrial automation. Government support such as EV tax credits and clean-energy incentives have spurred module adoption and manufacturing investment. Technological advances in the region include 1700 V/1200 A SiC module platforms, digital manufacturing and automated module testing systems. One US-based module supplier announced ramp-up of 600 MW annual capacity, reducing cost per module by approximately 20 %. Consumer behaviour in North America reflects higher enterprise adoption in automotive and renewable sectors, with OEMs specifying SiC modules as standard for next-generation traction inverters rather than niche options.

How Are Regulatory And Innovation Frameworks Shaping The SiC Module Market?

In Europe the silicon carbide power module market constitutes around 20 % of global shipments, with Germany, United Kingdom and France as leading sub-markets. Regulatory bodies and sustainability initiatives are influential: EU emission standards and electrification mandates push module suppliers to meet stringent performance and lifecycle requirements. Adoption of emerging technologies such as sintered packaging and press-fit SiC modules is advancing. One European module manufacturer introduced a 1700 V full SiC power module capable of automotive qualification up to 150 °C junction temperature, enabling premium EV applications. Regional consumer behaviour in Europe places premium value on explainable, certified module solutions and lifecycle sustainability, with OEMs increasingly requesting traceability and recycled-material content in module packaging.

Which Factors Are Accelerating SiC Module Deployment In High-Growth Markets?

In Asia-Pacific the silicon carbide power module market volume places the region among the top three, with circa 25 % of global shipments in 2024. Key consuming countries include China, India and Japan. Manufacturing infrastructure is expanding rapidly with new SiC module assembly lines and localised packaging hubs. Regional tech trends feature 200 mm SiC wafer integration and smartphone-style cloud ordering for SiC modules in China. For example, a Chinese module provider announced delivery of 5 000 1700 V SiC modules per month in 2024, cutting delivery lead-time to five days. Consumer behaviour in Asia-Pacific is cost-sensitive and volume-driven, with OEMs increasingly outsourcing SiC module manufacturing to regional low-cost providers and favouring modular, scalable module designs.

What Emerging Service And Manufacturing Nodes Are Accelerating SiC Module Growth?

In South America major countries such as Brazil and Argentina are emerging in the silicon carbide power module market, with a regional share currently in the low single digits but growth running double digits. Infrastructure and energy-sector trends show increasing investment in solar-plus-storage and electric-mobility charging systems. For example, a Brazilian service facility launched assembly of SiC power modules targeting local OEMs and research institutes, reducing import-lead-times by 30 %. Government incentives for renewable-energy equipment manufacturing and trade policies favouring regional export of modules bolster growth. Regional consumer behaviour emphasises localised support, language interfaces and shorter logistics for module procurement rather than global supply chains.

How Are Research Initiatives And Strategic Partnerships Supporting SiC Module Uptake?

In Middle East & Africa the silicon carbide power module market remains nascent, with demand trends tied to oil & gas electrification, data-centre power upgrades and smart-grid projects in UAE, Saudi Arabia and South Africa. Major growth countries are establishing research hubs and partnerships with module suppliers to support regional production and service ecosystems. For example, a South African institute partnered with a SiC module vendor to set up a local assembly line for power-electronics modules aimed at renewable and hybrid-marine applications. Local regulations increasingly focus on localisation and content-tracking, and consumer behaviour reflects preference for turnkey service-provider models rather than self-integration of SiC modules.

United States: ~55 % share — extensive EV and renewable-energy module demand, high production capacity and large-scale SiC module fabs.

China: ~8 % share — rapid expansion of domestic manufacturing, aggressive investment in SiC module plants and growing export volumes.

The silicon carbide power module market features over 40 active competitors globally, ranging from integrated device manufacturers to specialised module assemblers and packaging service providers. The market structure is moderately consolidated, with the top five companies capturing approximately ~62 % of module shipment volume. Strategic initiatives include joint ventures between SiC wafer manufacturers and module assemblers, launch of 1700 V/1200 A SiC module product lines, acquisitions of packaging technology firms and partnerships with automotive OEMs for inverter-system qualification. Innovation trends centre on integrating sensors for predictive maintenance, modular scalable module form-factors, sintered and press-fit packaging for automotive and industrial environments, and transition to 200 mm wafer sources to reduce cost. For decision-makers, vendor evaluation emphasises geographic capacity, integration level (wafer to module), lead-time performance, automotive qualification, and supply-chain resilience. The competitive landscape is evolving rapidly as SiC module demand grows and new entrants target niche high-voltage industrial and renewable segments.

Infineon Technologies

Mitsubishi Electric

Toshiba

Fuji Electric

ROHM Semiconductor

Semikron Danfoss

Microchip Technology

The silicon carbide power module market is underpinned by a wave of technology advancements tailored for next-generation power electronics. Key enablers include 1700 V and 1200 V SiC module platforms designed for high-voltage traction inverters and utility-scale converters, enabling up to 15 % higher system efficiency and 20 % smaller footprint compared with legacy silicon modules. Manufacturers are ramping adoption of 200 mm SiC wafer technology, which delivers up to 45 % higher throughput and lower per-unit cost compared with 150 mm wafers. Packaging innovations such as sintered copper baseplates, press-fit interconnects and integrated current-sensing modules reduce thermal resistance and improve reliability under 150 °C junction conditions. Digital transformation trends include cloud-based module ordering portals, built-in telemetry in modules tracking real-time temperature and current, and AI-driven predictive analytics reducing module failure risk by ~12 %. Automotive qualification standards (AEC-Q101/102) now apply to SiC modules, pushing development of automotive grade designs with lifetime targets beyond 10 years or 1.5 million km. The shift to >3 kV SiC modules for HVDC and renewable energy conversion expands the silicon carbide power module market beyond previous domains. Industrial and utility integrators are increasingly specifying modules with lifecycle traceability, recycled-material components and lower embodied energy, aligning module development with ESG compliance. Decision-makers must evaluate module technology readiness (wafer source, packaging technology, thermal management, digital features) as well as alignment with evolving system architectures such as 800 V EVs, 1500 V solar inverters and modular grid converters.

• In April 2024, Wolfspeed announced shipment of its first full SiC power module rated at 1700 V/600 A to a major EV OEM, enabling improved battery pack size by ~10%. Source: www.wolfspeed.com

• In October 2023, Infineon introduced a new SiC power module family with integrated gate driver and current sensing, targeting fast-charging infrastructure applications with up to 30% faster switching. Source: www.infineon.com

• In July 2024, STMicroelectronics launched an automotive-qualified 1200 V full SiC power module platform rated for 800 A continuous, aimed at next-generation EVs and energy storage systems. Source: www.st.com

• In December 2023, ON Semiconductor opened a new SiC module production line in North America with a capacity of 200 MW annually, reducing regional lead-time for module supply by approximately 25%. Source: www.onsemi.com

The scope of this market report spans global silicon carbide power module devices, covering product types (hybrid SiC modules, full SiC modules), power-rating categories (low-power, medium-power, high-power >3 kV), applications (automotive, industrial drives, renewable energy, aerospace & defence) and end-user industries (OEMs, aftermarket, system integrators). Geographic coverage includes regions such as North America, Europe, Asia-Pacific, South America and Middle East & Africa, with detailed country-level profiles for key markets including United States, China, Germany, India and Brazil. The report analyses technology segments (200 mm wafer SiC, sintered packaging, press-fit and digital-monitoring modules), manufacturing capacity trends, supply-chain dynamics and module qualification standards. Strategic focus areas include EV traction systems, 1500 V/1700 V module platforms, renewable-energy inverter upgrades and grid-scale power-conversion modules. Additionally, the study examines emerging niche segments such as SiC power modules for marine hybrid propulsion, DC-fast-charging stations, and decentralised data-centre power systems, along with invest-ment and funding patterns, competitive benchmarking, vendor evaluations and growth-opportunity mapping for decision-makers in module manufacturing, system integration and end-user procurement.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 2,851.5 Million |

|

Market Revenue in 2032 |

USD 15,632.6 Million |

|

CAGR (2025 - 2032) |

23.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

STMicroelectronics, Wolfspeed, ON Semiconductor, Infineon Technologies, Mitsubishi Electric, Toshiba, Fuji Electric, ROHM Semiconductor, Semikron Danfoss, Microchip Technology |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |