Reports

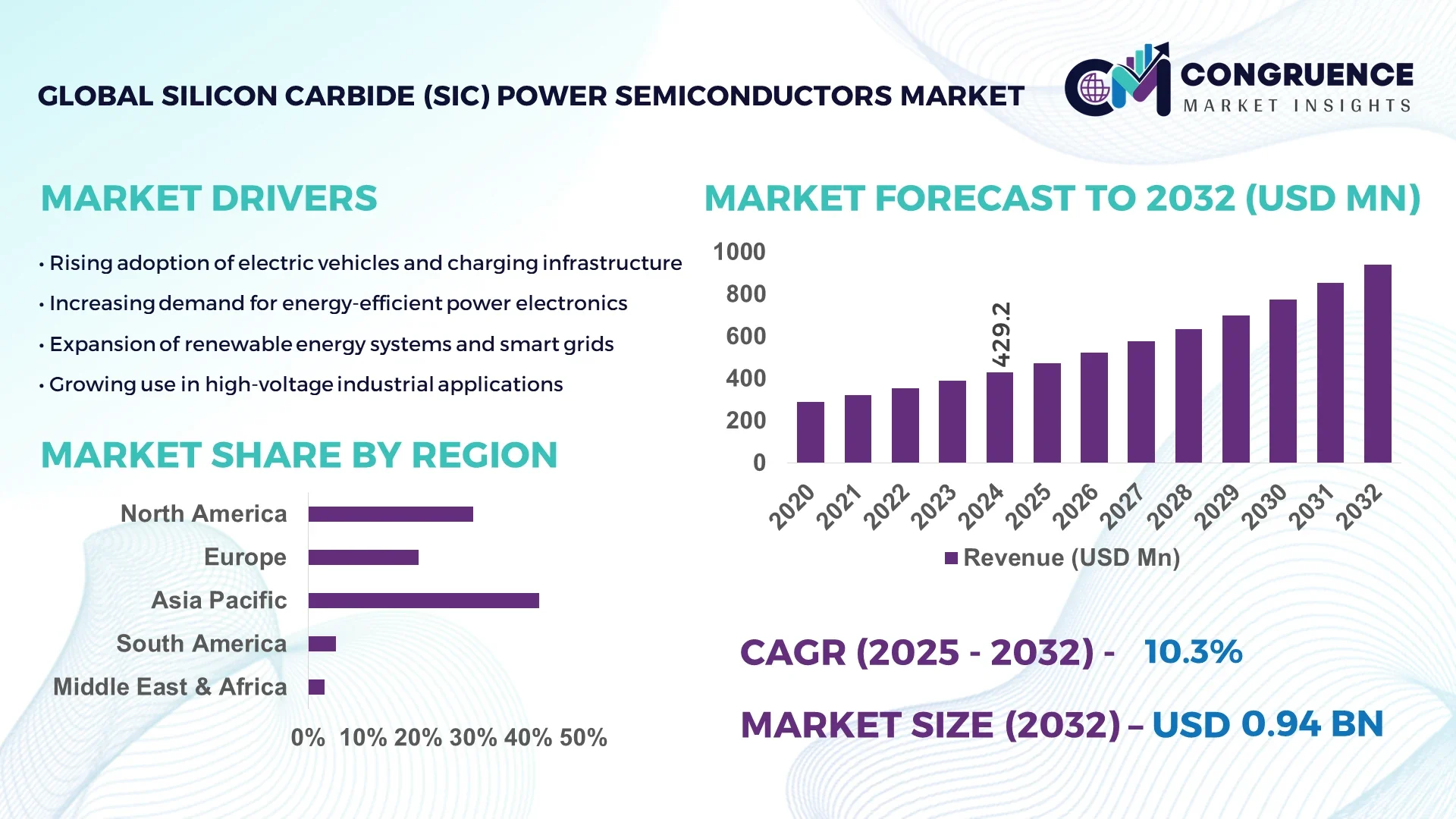

The Global Silicon Carbide (SIC) Power Semiconductors Market was valued at USD 429.17 Million in 2024 and is anticipated to reach a value of USD 940.24 Million by 2032 expanding at a CAGR of CAGR of 10.3% between 2025 and 2032.

In Europe, Italy plays a leading role with significant technological strides in silicon carbide (SiC) capabilities. The STMicroelectronics facility in Catania, Sicily, employs advanced energy-efficient SiC chip production tailored for electric vehicle power systems, renewable energy interfaces and automotive-grade semiconductors, showcasing elevated investment in wafer-scale manufacturing and integration of high-voltage SiC microchip technologies.

Key industry sectors such as electric vehicles, renewable energy, industrial automation, and high-performance data center infrastructure drive demand. Advances include new 650 V and 1200 V MOSFETs rising by over 27% year on year, next generation diode series with 18% lower switching losses, and trench MOSFETs delivering 20% lower conduction losses. Customized SiC modules for high temperature and high frequency use surged by 23%. Regulatory momentum and environmental mandates favor high efficiency wide bandgap semiconductor adoption, while economic incentives and the drive for energy efficient electrification accelerate regional consumption. Emerging trends include miniaturized, high power density modules tailored for aerospace, defense, and electric drivetrain applications. The outlook indicates sustained growth, propelled by innovations in thermal performance, efficiency enhancements, and integration across new verticals in infrastructure and transportation.

Artificial intelligence is playing an increasingly strategic role in enhancing the capabilities and efficiency of the Silicon Carbide (SIC) Power Semiconductors Market. AI driven manufacturing and design techniques are enabling smarter process control, predictive defect detection, and real time optimization in SiC wafer production and device fabrication. In semiconductor manufacturing, AI models are being deployed to analyze process variations and improve yield quality, reducing wafer defects and lowering cost per unit. AI algorithms enhance recipe tuning in plasma etching and epitaxial layer growth, accelerating time to target in production workflows. Simulation tools infused with machine learning help engineers predict device behavior under dynamic thermal and electrical stress, aiding the development of next generation SiC MOSFETs and power modules for electric vehicles and energy storage. These capabilities streamline R&D and shorten iteration cycles, empowering companies to bring efficient, robust SiC solutions to market more quickly. In AI focused data centers, AI optimized power conversion architectures incorporating SiC achieve higher efficiency and thermal management, directly influencing the market adoption of SiC power devices. As AI continues advancing across manufacturing, design automation, and system integration, its contributions reinforce competitiveness and innovation within the Silicon Carbide (SIC) Power Semiconductors Market, enabling cost effective scalability, superior performance, and rapid deployment in fast evolving, high power sectors.

“2024 Few Shot Test Time Optimization Without Retraining for Semiconductor Recipe Generation and Beyond” introduces a Model Feedback Learning (MFL) framework that optimizes semiconductor manufacturing recipes such as plasma etching and chemical vapor deposition, achieving target recipe generation in just five iterations, outperforming both Bayesian optimization and manual tuning by experts.

The Silicon Carbide (SIC) Power Semiconductors market is evolving rapidly, driven by the rising adoption of energy efficient technologies across multiple industries. Increasing electrification of vehicles, expanding renewable energy infrastructure, and advancements in high voltage applications are reshaping demand patterns. The ability of SiC devices to deliver higher power density, lower switching losses, and better thermal performance compared to traditional silicon-based semiconductors positions them as a critical enabler of next-generation power electronics. Regional demand is further influenced by supportive government policies, strategic investments in wafer fabrication facilities, and technological innovations in SiC MOSFETs and Schottky diodes. These dynamics highlight a robust growth trajectory underpinned by both technological advantages and market diversification.

The rapid global expansion of electric vehicles and the supporting charging ecosystem is a primary growth driver for the Silicon Carbide (SIC) Power Semiconductors market. SiC power devices are increasingly preferred in traction inverters, onboard chargers, and fast charging stations due to their ability to handle high voltages and reduce power losses by up to 50% compared to silicon components. Automotive manufacturers are incorporating SiC-based MOSFETs to improve range efficiency and support ultra-fast charging, with adoption rates in EV powertrains projected to rise significantly by 2030. Additionally, global investments in EV charging networks exceeding 2 million installations in 2024 are further amplifying the demand for high efficiency SiC devices, cementing their role in the future of sustainable mobility.

A major restraint for the Silicon Carbide (SIC) Power Semiconductors market is the high cost associated with wafer production and fabrication complexity. SiC substrates are difficult to grow and require specialized equipment for cutting, polishing, and epitaxial growth, leading to production costs that are substantially higher than traditional silicon wafers. Manufacturing yields remain lower due to defect densities, limiting economies of scale and slowing widespread adoption in cost-sensitive industries. The price gap between SiC wafers and conventional silicon remains nearly three to four times higher, posing a barrier for applications where performance gains may not justify added costs. These manufacturing challenges hinder faster market penetration, especially in regions with limited advanced fabrication infrastructure.

The global transition toward renewable energy presents significant opportunities for the Silicon Carbide (SIC) Power Semiconductors market. SiC devices are crucial in solar inverters, wind turbines, and energy storage systems, where their superior efficiency improves energy conversion and reduces overall system costs. With global renewable energy capacity additions exceeding 500 GW in 2024, demand for SiC-based power electronics is set to rise sharply. Smart grid modernization and distributed energy systems further increase the need for reliable high voltage and high frequency devices, areas where SiC excels. This creates substantial opportunities for market players to supply advanced SiC solutions that optimize renewable integration, improve grid stability, and accelerate the adoption of sustainable energy systems worldwide.

One of the critical challenges facing the Silicon Carbide (SIC) Power Semiconductors market is the constrained availability of high quality raw materials and supply chain bottlenecks. The production of SiC requires pure silicon and carbon sources, and the growth of defect free wafers is a complex, time intensive process. Global supply has struggled to keep pace with surging demand, leading to extended lead times for wafer deliveries, often exceeding six months. Limited supplier bases and concentration of production capacity in specific regions increase the risk of disruptions. These factors contribute to uncertainty for manufacturers and delay large scale adoption, particularly in rapidly growing sectors such as electric vehicles and renewable power generation.

• Expansion of high voltage MOSFET and diode portfolios: The Silicon Carbide (SIC) Power Semiconductors market is experiencing a surge in the development of advanced MOSFETs and diodes, particularly in voltage classes above 1200 V. New generations of trench MOSFETs have achieved 20% lower conduction losses, while Schottky barrier diodes have shown a 15% improvement in switching efficiency. These innovations are enabling more compact, energy efficient converters and inverters used in electric vehicles, renewable energy systems, and aerospace power modules.

• Increased integration in data center power architectures: Data centers are driving a measurable trend toward SiC adoption, as power consumption from global hyperscale facilities continues to grow by over 10% annually. SiC based power modules are being integrated into server power supplies and uninterruptible power systems, delivering efficiency gains of up to 3% compared to silicon alternatives. This translates into significant reductions in cooling requirements and operational costs, supporting the market shift toward sustainable and high performance data infrastructure.

• Growth of wafer capacity expansions and foundry partnerships: To meet accelerating demand, leading manufacturers are expanding 200 mm SiC wafer production capacity. Multiple fabrication plants have reported scaling their output by more than 35% year over year, with new partnerships between foundries and integrated device manufacturers ensuring supply continuity. This expansion addresses supply chain bottlenecks and is critical for enabling mass adoption of SiC devices in automotive, industrial, and renewable applications.

• Adoption in aerospace and defense power systems: SiC power semiconductors are increasingly used in next generation aerospace and defense programs, where weight reduction and power efficiency are key. SiC modules are delivering up to 25% higher power density in aircraft electric propulsion systems and advanced radar applications. This trend demonstrates the strategic relevance of SiC technology in high reliability and mission critical environments, reinforcing its role in specialized high performance markets.

The Silicon Carbide (SIC) Power Semiconductors market is segmented by type, application, and end user, each contributing uniquely to its expansion. By type, the market encompasses MOSFETs, diodes, and modules, with MOSFETs currently leading due to their efficiency in high voltage switching. By application, electric vehicles dominate, while renewable energy systems and industrial automation are witnessing significant growth. End user insights highlight automotive as the primary consumer segment, while energy and utilities, data centers, and aerospace sectors are expanding adoption. Each segment is influenced by technological innovation, government incentives, and shifting industrial priorities, shaping a dynamic competitive environment.

The Silicon Carbide (SIC) Power Semiconductors market includes MOSFETs, diodes, and power modules, each fulfilling different roles in high power electronics. MOSFETs dominate the type segment, as they are widely deployed in electric vehicles, charging stations, and renewable power inverters. Their ability to handle higher switching frequencies and minimize power losses has positioned them as the preferred component for high efficiency designs. Diodes, particularly Schottky barrier diodes, are essential for fast switching and reduced reverse recovery losses, making them indispensable in power supply and motor drive applications. Modules represent the fastest growing type, with demand rising for compact, integrated solutions that combine multiple SiC devices into a single package. These modules are increasingly applied in aerospace and heavy industrial systems where high reliability and reduced size are critical. Together, these types form the backbone of SiC technology adoption, each serving specialized performance and operational needs across industries.

Electric vehicles represent the leading application for Silicon Carbide (SIC) Power Semiconductors, driven by their role in traction inverters, onboard chargers, and fast charging infrastructure. SiC enables EVs to achieve longer driving ranges and supports ultra fast charging, making it the most impactful application area. Renewable energy is the fastest growing application, with SiC devices integrated into solar inverters, wind turbine systems, and energy storage, ensuring improved efficiency and stability in renewable grids. Industrial automation also plays a crucial role, where SiC enhances efficiency in motor drives, robotics, and factory power management. Aerospace and defense applications are more niche but growing steadily, as SiC supports high power density needs in electric propulsion and advanced radar systems. Data centers add another layer of opportunity by adopting SiC modules for efficient power conversion and thermal management. Collectively, these applications highlight the widespread integration of SiC across industries undergoing electrification and digital transformation.

Automotive stands as the leading end-user of Silicon Carbide (SIC) Power Semiconductors, fueled by the global shift to electric mobility. Automakers are adopting SiC devices in drivetrains and fast charging platforms, reinforcing their dominant share. The fastest growing end-user is the energy and utility sector, as SiC plays a critical role in renewable energy systems and smart grid integration. Rising installation of solar and wind power facilities is creating demand for highly efficient inverters and converters, directly boosting adoption. Industrial manufacturing is also a strong contributor, utilizing SiC devices in high precision machinery, robotics, and automation solutions. Aerospace and defense remain specialized but strategic, where SiC technologies enable advancements in compact, reliable, and lightweight power electronics. Data centers are another emerging end-user segment, leveraging SiC for reducing energy consumption in power supply units. These varied end-users collectively reflect the versatile application potential of SiC across both mainstream and specialized markets.

Asia-Pacific accounted for the largest market share at 42% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 11.5% between 2025 and 2032.

Asia-Pacific’s lead is supported by strong semiconductor manufacturing bases, rapid electrification in China and India, and investments in renewable energy. Europe follows closely with a 28% market share, driven by sustainability policies and EV adoption in Germany and France. North America, with a 19% share, benefits from cutting-edge research, regulatory backing, and electric mobility expansion. South America and the Middle East & Africa collectively account for 11%, reflecting growing renewable energy deployments, industrial modernization, and rising infrastructure projects.

High efficiency power electronics adoption shaping industrial transformation

North America held a 19% share of the Silicon Carbide (SIC) Power Semiconductors market in 2024, reflecting strong uptake across electric vehicles, aerospace, and industrial sectors. Automakers and energy firms are accelerating SiC adoption in drivetrains and grid infrastructure, while aerospace companies deploy SiC modules for lightweight, efficient systems. Regulatory policies supporting zero emission vehicles and federal incentives for clean energy transition further stimulate demand. Technological advancements include widespread integration of 200 mm SiC wafer technologies and AI driven manufacturing analytics that improve yield and performance. The region is also witnessing digital transformation in semiconductor supply chains, optimizing production and addressing growing demand for high efficiency, reliable power devices.

Next generation semiconductor solutions driving sustainability adoption

Europe accounted for 28% of the Silicon Carbide (SIC) Power Semiconductors market in 2024, led by Germany, the UK, and France. Germany’s automotive sector continues to lead in adopting SiC for electric drivetrains, while France strengthens renewable integration through advanced SiC inverter systems. The European Union’s sustainability initiatives, including stricter carbon reduction targets and mandatory energy efficiency standards, are accelerating adoption across industries. Regulatory bodies actively promote wide bandgap semiconductor deployment in renewable grids and transportation electrification. Advances in high voltage MOSFETs and expansion of local fabrication facilities are fostering innovation, positioning Europe as a leader in sustainable semiconductor technologies.

Rising semiconductor capacity and electrification initiatives fueling adoption

Asia-Pacific represented the largest regional market in 2024 with 42% share, anchored by China, Japan, and India. China leads with high-volume SiC wafer production and EV infrastructure deployment, while Japan emphasizes precision manufacturing and energy efficiency. India’s rapid expansion of renewable energy and EV charging infrastructure further boosts demand for SiC technologies. Regional governments are investing heavily in semiconductor manufacturing hubs, driving innovation clusters in power electronics. Advancements in 200 mm wafer fabs and integration of SiC into smart grid modernization projects are enhancing reliability and efficiency. This dynamic mix of production scale, innovation, and infrastructure growth secures Asia-Pacific’s position as the dominant global hub.

Infrastructure modernization and renewable push enabling semiconductor demand

South America accounted for 6% of the Silicon Carbide (SIC) Power Semiconductors market in 2024, with Brazil and Argentina emerging as the key contributors. Brazil’s large-scale renewable projects in wind and solar are driving demand for SiC inverters and grid stability solutions. Argentina’s industrial modernization efforts are expanding opportunities for SiC in automation and energy storage systems. Regional governments are introducing tax incentives for clean energy investments and upgrading transmission networks to meet rising energy demand. These policies, combined with steady automotive electrification efforts, are shaping the region’s SiC semiconductor adoption, particularly within renewable energy and infrastructure development sectors.

Energy diversification and industrial electrification boosting semiconductor adoption

The Middle East & Africa represented 5% of the Silicon Carbide (SIC) Power Semiconductors market in 2024, with the UAE and South Africa leading adoption. Demand is rising in oil and gas electrification, renewable energy integration, and construction modernization. The UAE is investing heavily in solar power and grid infrastructure, creating strong demand for SiC-based high efficiency inverters. South Africa is advancing industrial electrification projects and modernizing mining operations with SiC solutions. Regional trade partnerships and government initiatives supporting energy diversification are fueling uptake. Technological modernization, particularly in smart grids and advanced industrial equipment, is accelerating SiC adoption across the region.

China: 26% market share | Dominance driven by large-scale wafer production capacity and extensive EV infrastructure deployment.

Germany: 15% market share | Strong demand supported by advanced automotive manufacturing and rapid electrification of transportation systems.

The Silicon Carbide (SIC) Power Semiconductors market is characterized by an intensely competitive environment, with over 25 active global manufacturers and suppliers engaged in the development, production, and commercialization of SiC devices. Competition is driven by advancements in wafer size transition from 150 mm to 200 mm, innovation in trench MOSFET architectures, and the expansion of integrated SiC power modules targeting automotive, renewable, and industrial applications. Leading companies are strengthening their market positioning through strategic mergers, long-term supply agreements with automotive OEMs, and partnerships with energy companies to secure large-scale adoption. In 2024, multiple players announced the commissioning of new fabs to address capacity shortages, with some facilities capable of producing more than 1 million SiC wafers annually. Product launches focused on high voltage diodes and next-generation MOSFETs with reduced switching losses underscore the pace of innovation. Additionally, collaboration between foundries and system integrators is accelerating the integration of SiC into fast-growing markets such as electric mobility, aerospace, and smart grids. This competitive landscape reflects a balance of established multinational corporations and emerging specialized players, both of which are influencing pricing, technology roadmaps, and global supply chains.

ON Semiconductor

ROHM Semiconductor

Mitsubishi Electric Corporation

Toshiba Corporation

Littelfuse, Inc.

Microchip Technology Inc.

GeneSiC Semiconductor Inc.

Technological advancements in the Silicon Carbide (SIC) Power Semiconductors market are reshaping high-power electronics, particularly in applications requiring efficiency, reliability, and compact designs. The transition from 150 mm to 200 mm SiC wafers is one of the most significant innovations, allowing higher output capacity and reduced per-unit production costs. In 2024, multiple manufacturers successfully scaled wafer production by more than 35%, meeting the rising demand from automotive and renewable sectors. Trench MOSFET technology continues to advance, delivering up to 20% lower conduction losses and improved thermal performance, making them essential for next-generation traction inverters and high-frequency converters.

Integration of SiC in power modules is another technological leap. Compact modules combining MOSFETs and Schottky barrier diodes are being deployed in electric drivetrains, aerospace power systems, and industrial motor drives. The development of ultra-low defect density substrates has further improved yields, with defect levels reduced by nearly 40% over the past two years. Enhanced epitaxial growth processes and AI-based quality control systems are enabling consistent device performance across large-scale production.

In addition, innovations in packaging, such as double-sided cooling and silver sintering, are enhancing thermal conductivity and reliability. Emerging applications in 5G base stations, smart grids, and fast-charging stations highlight the versatility of SiC technology. Collectively, these advancements are strengthening the market by driving down costs, boosting performance, and widening the scope of adoption across industries.

• In January 2023, Wolfspeed inaugurated its 200 mm silicon carbide wafer fabrication facility in New York, significantly increasing global capacity for high-efficiency power devices, with production capability exceeding one million SiC wafers annually.

• In September 2023, Infineon Technologies launched a new 650 V CoolSiC MOSFET family designed for data center and renewable applications, achieving efficiency gains of 2–3% in server power supplies and solar inverters.

• In April 2024, ROHM Semiconductor introduced its fourth-generation trench gate SiC MOSFETs, offering 40% lower switching losses compared to previous models, tailored for automotive traction inverters and industrial converters.

• In July 2024, STMicroelectronics expanded its Catania SiC facility in Italy, doubling production capacity with a new automated line focused on automotive-grade MOSFETs and diodes to meet accelerating EV demand in Europe.

The scope of the Silicon Carbide (SIC) Power Semiconductors Market Report encompasses a comprehensive analysis of technologies, applications, regional dynamics, and industry segments shaping the global market landscape. The report evaluates major product types including MOSFETs, diodes, and integrated power modules, highlighting their adoption across diverse end-user industries. Applications examined range from electric vehicles and renewable energy to industrial automation, aerospace, data centers, and grid infrastructure. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing consumption patterns, industrial growth drivers, and regional policy influences. Asia-Pacific, holding over 40% of the share in 2024, is covered in detail, alongside insights into Europe’s sustainability-led adoption and North America’s advanced research-driven growth trajectory.

Technological dimensions include wafer size evolution, trench MOSFET advancements, Schottky barrier diode innovation, and packaging technologies such as silver sintering and double-sided cooling. The report also explores AI integration in manufacturing, supply chain dynamics, and emerging 200 mm wafer capacity expansions. Additionally, niche segments such as aerospace electrification, 5G infrastructure, and smart grid modernization are analyzed to provide insight into emerging opportunities. The breadth of coverage ensures decision-makers understand both established growth areas and potential untapped markets where SiC technologies are poised to gain traction.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD V2025 Million |

Market Revenue in 2033 | USD V2033 Million |

CAGR (2026 - 2033) | 22.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Wolfspeed, Infineon Technologies AG, STMicroelectronics, onsemi, ROHM Semiconductor, Mitsubishi Electric Corporation, Fuji Electric Co., Ltd., Toshiba Electronic Devices & Storage, Bosch Semiconductor, Renesas Electronics Corporation |

Customization & Pricing | Available on Request (10% Customization is Free) |