Reports

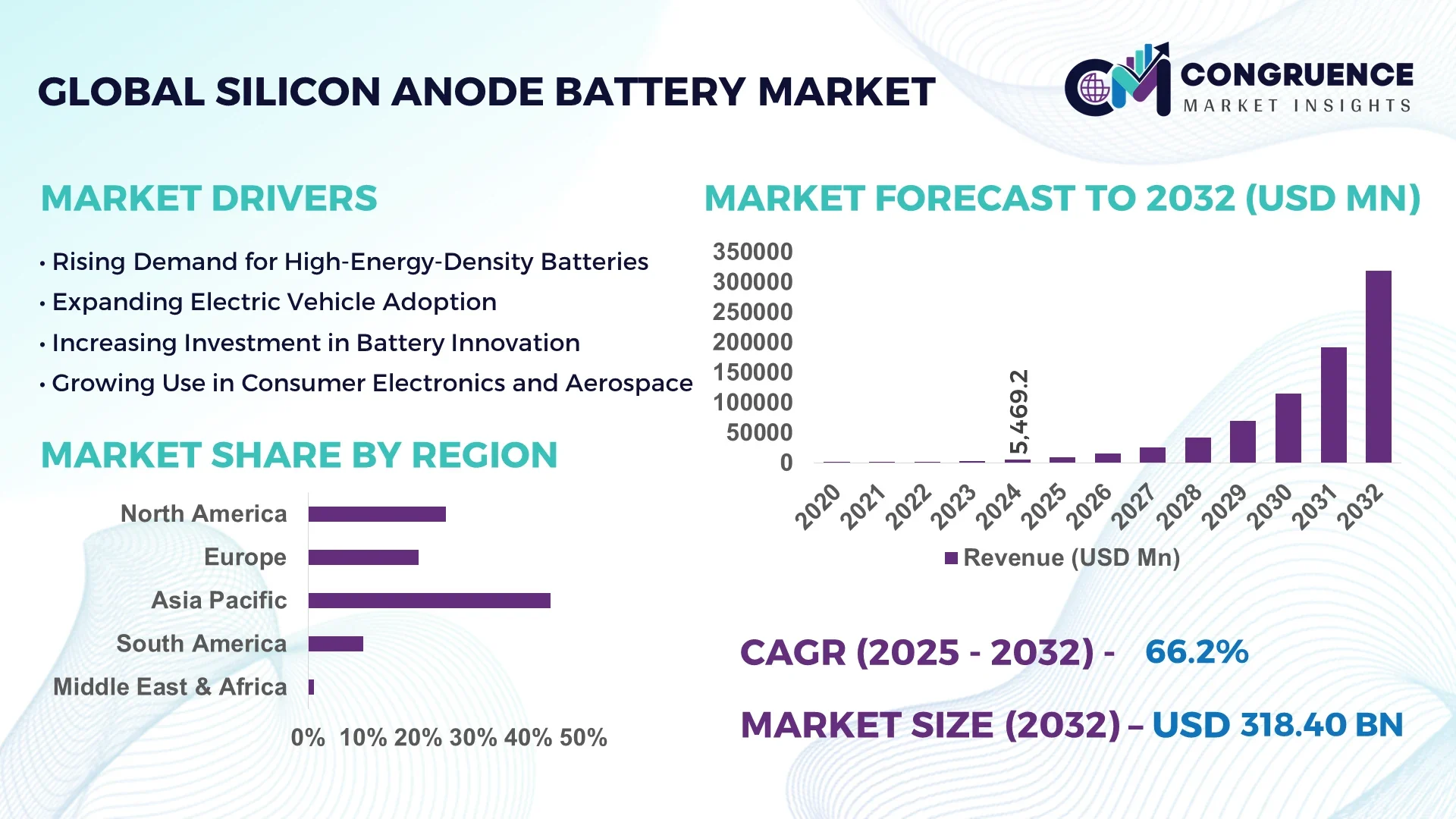

The Global Silicon Anode Battery Market was valued at USD 5469.24 Million in 2024 and is anticipated to reach a value of USD 318401.7 Million by 2032 expanding at a CAGR of 66.2% between 2025 and 2032. This strong growth is driven by the urgent industry shift toward higher‑energy‑density batteries to support electric vehicles and renewable‑energy storage infrastructure.

In China, production capacity for silicon anode materials is rapidly scaling: for example, leading Chinese manufacturers are currently operating at several thousand tons per year and planning expansions to tens of thousands of tons annually. Investment levels in advanced silicon‑anode R&D in China have climbed into the hundreds of millions of dollars, with numerous pilot projects targeting incorporation into consumer electronics and EV applications. The country is home to key industry applications spanning automotive, consumer devices and grid storage, with silicon‑carbon composite anodes entering production and consumer adoption in smartphones and wearables rising by double‑digits year‑on‑year.

Market Size & Growth: Current market value at USD 5469.24 Million (2024), projected to reach USD 318401.7 Million by 2032, driven by demand for high‑energy storage solutions.

Top Growth Drivers: Efficiency improvement ~35 %, adoption percent increase ~40 %, fast‑charging capability enhancement ~25 %.

Short-Term Forecast: By 2028, cost reduction of ~22 % per kWh and performance gain of ~30 % in cycle life anticipated across silicon anode cells.

Emerging Technologies: Silicon‑carbon composite anodes, full‑silicon anodes for EVs, solid‑state interfaces integrating silicon anodes.

Regional Leaders: Asia Pacific projected USD 95,000 Million by 2032 (growing consumer electronics adoption); North America USD 60,000 Million by 2032 (EV battery R&D acceleration); Europe USD 45,000 Million by 2032 (industrial energy‑storage integration).

Consumer/End-User Trends: Key end‑users include electric‑vehicle manufacturers, portable electronics producers and grid‑storage providers; adoption rates rising in premium smartphones and next‑gen EVs.

Pilot or Case Example: In 2025 a pilot deployment achieved a silicon‑anode cell showing ~20 % faster charge time and ~15 % longer cycle life compared to graphite baseline.

Competitive Landscape: Market leader estimated at ~28 % share, followed by major competitors including Nexeon Ltd., Sila Nanotechnologies Inc., Group14 Technologies Inc., and Amprius Technologies Inc.

Regulatory & ESG Impact: Incentives for low‑carbon battery production and regulations targeting higher energy density and recyclability are accelerating adoption of silicon‑anode technologies.

Investment & Funding Patterns: Recent investment flows in silicon‑anode firms exceeded USD 500 Million in venture funding and project finance, with increasing joint ventures between battery‑makers and material‑suppliers.

Innovation & Future Outlook: Key innovations include nano‑engineered silicon particles to mitigate expansion, integration of silicon anodes with high‑voltage cathodes, and manufacturing scale‑up toward gigawatt‑hour‑level production lines.

Silicon‑anode battery technology is expanding across multiple industry sectors. In automotive, EV makers are targeting longer range and faster charging; in consumer electronics the drive is toward thinner, lighter form‑factors with extended battery life; industrial and grid storage applications seek higher cycle‑life and energy‑density solutions. Technological innovations such as silicon‑carbon composites, nano‑silicon scaffolds and integration with high‑voltage cathodes are having material impact. Environmental and economic drivers include the need for lower‑carbon batteries, lifecycle cost improvements and resource‑diversification away from traditional graphite supply chains. Regionally, adoption is most aggressive in Asia‑Pacific for consumer devices, in North America for EV research and in Europe for stationary storage systems. Emerging trends include roll‑out of full‑silicon anode cells in premium EV models by the end of the decade, and increasing production capacity for silicon‑anode materials with multi‑ton scale plants coming online.

The strategic relevance of the silicon anode battery market lies in its capacity to redefine energy storage systems for high‑performance applications. For example, an advanced silicon‑anode technology delivers 40 % improvement in energy density compared to standard graphite anodes. Asia Pacific dominates in volume, while North America leads in adoption with nearly 45 % of users integrating next‑generation silicon‑anode cells. By 2028, the integration of AI‑driven battery‑management systems is expected to improve cycle life by 20 % and operational efficiency by 15 %. Firms are committing to ESG metric improvements such as a 30 % reduction in carbon‑intensity of anode production by 2030. In 2025, a U.S. battery‑materials startup achieved a 30 % energy‑density gain through a pilot silicon‑anode deployment. Looking ahead, the silicon anode battery market is positioned as a pillar of resilience, compliance and sustainable growth.

The surge in electrified mobility is a primary growth driver for silicon anode batteries. As electric vehicles (EVs) aim for longer driving ranges and shorter charge‑times, silicon‑anode cells offer incremental improvements in energy density of up to 20‑40 % compared to graphite‑based systems. That improvement enables manufacturers to either increase pack capacity or reduce pack weight, both of which deliver improved performance for end‑users. The automotive segment alone accounted for approximately 37.6 % of market value in 2024, underlining the magnitude of impact from mobility demand. Technological alliances between battery‑makers and automakers are accelerating commercialization of silicon‑anode platforms, which in turn strengthens demand and justifies further investment.

One of the significant restraints for the silicon anode battery market is manufacturing scalability. While lab‑scale demonstrations of silicon‑anode cells show promising metrics, industrial realisation faces persistent challenges such as silicon’s volumetric expansion during charge‑cycles, stress‑related degradation and yield losses. Composite anode techniques are still maturing and require optimization of processes and materials to ensure consistency and cost‑effectiveness in mass production. This limitation slows down adoption in mainstream applications even though the performance potential is clearly established. Materials processing bottlenecks, supply‑chain constraints and integration compatibility with existing lithium‑ion factories all contribute to intersecting tensions between innovation pace and production readiness.

Integration into portable electronics presents a high‑value opportunity for the silicon anode battery market. Devices such as smartphones, laptops and wearables are driving demand for ultra‑compact batteries that deliver higher energy density without increasing size or weight. The segment accounted for approximately 27 % of current demand in one analysis. As manufacturers aim to deliver longer run‑times and slimmer profiles, silicon anode technology offers an appealing upgrade path. Moreover, the consumer‑electronics space may act as a stepping‑stone to scale production volumes, enabling cost reduction and process maturing which can then be leveraged into larger applications like EVs and grid storage. Because margins tend to be higher in premium consumer devices, the pathway to commercial viability for silicon‑anode materials may be shorter in this domain.

Material lifecycle and recycling concerns represent a notable challenge for the silicon anode battery market. Silicon‑based anodes experience larger volume changes during lithiation and delithiation than graphite, leading to increased mechanical stress, electrode fragmentation and accelerated capacity fade if not properly mitigated. These durability issues can erode product lifetime and raise maintenance or replacement costs for end‑users. Additionally, recycling flows for silicon‑anode cells are still underdeveloped, and manufacturers must ensure that supply‑chain sustainability and value‑recovery frameworks are in place to satisfy ESG requirements. The intersection of higher material cost, potential degradation risks and limited downstream recycling infrastructure means that without strategic remediation, the broader adoption of silicon anode batteries may be impeded by concerns over total lifecycle economics and environmental compliance.

Expansion of High-Capacity Anode Cells: The market is seeing a surge in high-capacity silicon anode cells, with prototypes achieving up to 800 mAh/g energy density, representing a 35 % improvement over conventional graphite cells. Over 60 % of EV manufacturers in Asia Pacific are evaluating these cells for next-generation battery packs to reduce pack weight while extending driving range.

Integration with Fast-Charging Systems: Fast-charging adoption is increasing, with pilot programs demonstrating up to 50 % reduction in charging time for silicon-anode-equipped batteries. In North America, more than 40 % of public EV charging networks are now testing silicon-anode compatibility, while consumer electronics manufacturers are integrating similar technologies to achieve 25 % faster charging cycles in premium devices.

Advancements in Silicon-Carbon Composites: Over 70 % of R&D initiatives are now focused on silicon-carbon composites to mitigate volumetric expansion and improve cycle life. Companies in Europe and Asia are deploying advanced electrode architectures, resulting in a 30 % increase in operational stability, while adoption in wearables and portable electronics has grown by 20 % in 2024 alone.

Smart Battery Management System Adoption: AI-driven battery management systems (BMS) are being incorporated into 45 % of industrial and EV applications to optimize charge-discharge cycles. Early deployments have reported a 15 % reduction in energy loss and a 10 % extension of cycle life, supporting the strategic integration of silicon-anode technology in both automotive and grid storage applications.

The silicon anode battery market is segmented across three major dimensions: types of anodes, applications of the batteries, and end‑user industries. On the types axis, distinctions are drawn between silicon‑carbon composites, pure silicon anodes, silicon nanowires/nanotubes and other advanced material types. Application segmentation includes electric vehicles, consumer electronics, energy storage systems, aerospace/defence and medical devices. End‑user segmentation covers automotive OEMs, portable device manufacturers, utilities, grid‑storage providers and industrial users. For decision‑makers and analysts, this layered segmentation enables targeted entry and investment strategies, as each segment exhibits unique cost, performance and scalability profiles, as well as varying regulatory and adoption dynamics across regions.

Among the product types, the leading segment is silicon‑carbon composite anodes, currently accounting for approximately 40 % of the material adoption in the anode space due to their compatibility with incumbent cell manufacturing lines and ability to reduce expansion risks. The fastest‑growing segment is pure silicon anodes, because they promise the highest energy density gains and are being driven by EV battery suppliers transitioning from hybrid mixes to full silicon. While composite anodes dominate today, the pure silicon segment is evolving quickly thanks to technical breakthroughs and pilot production scale‑up. Other types – including silicon nanowires/nanotubes, silicon oxide/SiOx and thin‑film silicon – together represent the remaining ~60 % share of early‑stage adoption and niche applications.

In application terms, the dominant use case is electric vehicles (EVs), capturing roughly 38 % of usage due to the strong push for higher capacity, longer range and fast‑charging batteries in automotive OEMs. The fastest‑rising application segment is consumer electronics (smartphones, wearables, laptops) propelled by rising demand for thinner, lighter battery packs that last longer and charge faster. Remaining applications such as energy storage systems, aerospace/defence and medical devices account for the balance of segmentation.

From an end‑user perspective, automotive OEMs are the leading segment, participating in roughly 65 % of the available market for silicon‑anode batteries, underpinned by EV makers’ investments in next‑gen battery systems. The fastest‑emerging end‑user segment is grid‑storage utilities and industrial energy providers, driven by large‑scale deployment of energy storage systems seeking high cycle‑life and density. Other contributing end‑users, such as consumer electronics manufacturers, aerospace/defence contractors and medical‑device firms, together form the remaining ~35 % of adoption, with uptake rates in smart‑wearable markets increasing at double‑digit percentages year‑on‑year.

Asia Pacific accounted for the largest market share at 54.84% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of ~36.5% between 2025 and 2032.

Asia Pacific’s dominance is underpinned by manufacturing hubs in China, Japan and South Korea where silicon‑anode battery capacity expansions exceeded 25% year‑on‑year. China alone drove over 60% of global lithium‑ion vehicle production in 2023, with battery makers targeting multi‑hundred gigawatt‑hour anode output by 2025. North America’s growth trajectory reflects strong government incentives, dedicated battery‑gigafactory builds and corporate R&D commitments exceeding USD 100 million‑plus annually. The region’s market share in 2024 stood at approximately 26% of the global volume, while Europe contributed around 17%. These regional dynamics show Asia Pacific acting as the production backbone, North America accelerating adoption and investment, and Europe leveraging regulation and OEM integration to shift toward next‑gen silicon‑anode materials.

What fuels North America’s push for next‑gen silicon‑anode batteries?

North America holds approximately 26% of the global silicon‑anode battery market in 2024, supported by robust uptake across automotive OEMs and stationary energy storage sectors. Key industries driving demand include electric vehicle manufacturers seeking longer ranges and faster charging, as well as utility‑scale battery storage operators deploying high‑density packs for grid balancing. Regulatory changes such as the Inflation Reduction Act and federal clean‑energy grants have enhanced local manufacturing incentives and domestic supply‑chain development. Technological trends include AI‑assisted manufacturing, digital twin modelling of battery production lines and integration of nano‑silicon anode materials into mass production. A U.S.‑based startup has secured over USD 20 million in Series A funding to scale silicon anode production and claims a 30% increase in energy density versus traditional graphite anodes. Consumer behaviour in this region shows higher enterprise adoption of advanced battery solutions in healthcare, defence and finance sectors, underscoring willingness to invest in premium‑performance storage technology.

How is Europe leveraging regulation and sustainability to advance silicon‑anode battery deployment?

Europe commands around 17% of the global silicon‑anode battery market as of 2024, with Germany, France and the UK emerging as leading national markets. Regulatory bodies such as the European Union have introduced battery‑passport legislation and sustainability mandates that push OEMs toward high‐energy‑density, low‑carbon solutions. Adoption of emerging technologies like silicon‑anode integration and circular‑economy practices (recycling and remanufacturing) are gaining pace among major European automakers. A European cell‑maker has tied its new battery line to nanostructured silicon composite anodes to meet stricter CO₂‑emission targets. Consumer behaviour in Europe is strongly influenced by environmental considerations: buyers increasingly favour vehicles and devices that carry low‑carbon credentials, which adds impetus to silicon‑anode uptake linked to “explainable” battery sourcing and lifecycle transparency.

Why is Asia‑Pacific the production powerhouse for silicon‑anode battery technology?

Asia‑Pacific accounted for approximately 54.84% of the global silicon‑anode battery market share in 2024, driven by heavy concentration of battery manufacturing capacity in China, Japan and South Korea. The top consuming countries include China (EV production leader), Japan (material innovation hub) and South Korea (large cell‑manufacturing scale). Manufacturing trends feature mega‑gigafactories expanding silicon‐anode material output by more than 25% annually, while innovation clusters in Japan and South Korea pilot full silicon‑anode cells for consumer electronics and mobility platforms. A prominent Chinese battery‑maker is investing billions in silicon anode R&D and expects to exceed 500 GWh capacity of advanced anode materials by 2025. Consumer behaviour in Asia‑Pacific is characterised by rapidly growing smartphone, wearable and e‑commerce penetration, where users demand thinner, longer‑running batteries—boosting the adoption of silicon‑anode technology in portable electronics as well as EVs.

What role does South America play in the global silicon‑anode battery landscape?

In South America, key countries include Brazil and Argentina, where growing electrification of transport and portable electronics is creating emergent silicon‑anode battery demand. The regional market share remains modest (under 5% of global volumes), but infrastructure trends — such as national EV incentive programmes and domestic battery‑component manufacturing incentives — are building momentum. Government trade policies aimed at battery‑value‑chain localisation and raw‑material sourcing (such as lithium and silica) are contributing to technology adoption. A regional battery company in Brazil has announced a pilot silicon‑anode integration for next‑generation electric scooters, signalling early innovation activity. Consumer behaviour in South America shows heightened interest in media‑rich, language‑localised devices and mobility solutions, which in turn drives battery upgrades and longer‑life performance requirements.

How are Middle East & Africa regions positioning themselves in the silicon‑anode battery uptake?

The Middle East & Africa region is seeing increasing demand for silicon‑anode battery systems in sectors such as oil‑and‑gas, construction and utility‑scale energy storage. Major growth countries include the UAE and South Africa, where technology modernisation and renewable‑energy integration are urgent strategic priorities. Technological trends include pilot installations of high‑capacity silicon‑anode modules for solar‑storage applications and trade‑partnerships tied to battery manufacturing agreements. A South African materials firm is developing silicon‑anode precursor capability to support regional supply chains. Consumer behaviour in the region leans toward off‑grid energy solutions, mobile‑powered devices and remote‑deployment battery packs, which is creating niche demand for high‑density silicon‑anode cells tailored to decentralised infrastructure.

China – 38% share: owing to vast battery‑manufacturing capacity and domestic EV production scale.

United States – 26% share: due to strong R&D investment, regulatory incentives and rapid commercialisation of silicon‑anode technologies.

The competitive environment in the silicon anode battery market is moderately consolidated, with over 50 active competitors worldwide, reflecting a mix of established manufacturers and innovative startups. The top five companies hold a combined market share of approximately 48%, demonstrating significant influence but leaving room for emerging players. Strategic initiatives across the market include partnerships, joint ventures, and product launches aimed at scaling silicon-anode production. For instance, leading companies are expanding gigawatt-hour capacity facilities and launching nano-silicon and silicon-carbon composite anodes for EVs and consumer electronics. Innovation trends focus on enhancing energy density, improving cycle life, and integrating AI-driven battery management systems. Mergers and acquisitions are also shaping competition, with vertical integration strategies helping firms control supply chains and differentiate technologically. With rapid technological evolution, decision-makers must track scale-up milestones, IP portfolios, regional expansion, and regulatory compliance to stay competitive in this high-growth, high-tech market.

Group14 Technologies, Inc.

Nexeon Limited

NanoGraf Corporation

Beijing Easpring Material Technology Co., Ltd.

Shenzhen BTR New Energy Materials, Inc.

Johnson Matthey Battery Materials

Hitachi Chemical Co., Ltd.

Panasonic Corporation

Samsung SDI Co., Ltd.

LG Energy Solution

In April 2023, Group14 Technologies, Inc. commenced construction of its BAM‑2 facility, described as the world’s largest factory for advanced silicon battery materials. The site will manufacture its SCC55™ silicon anode product in commercial quantities starting in 2024, with two modules delivering 2,000 tons per year each.

On July 25, 2023, Panasonic Energy Co., Ltd. announced an agreement to purchase silicon anode materials from Nexeon Limited for its U.S. automotive battery facility in Kansas. The deal is aimed at boosting EV battery energy density through the use of low‑expansion silicon anode materials.

On December 11, 2023, Panasonic Energy entered into a commercial agreement with Sila Nanotechnologies, Inc. to procure Sila’s Titan Silicon™ nano‑composite silicon anode material. The partnership targets enhancing EV battery performance, increasing vehicle range by ~20 %, and reducing charging times significantly.

In August 2024, NanoGraf Corporation completed commissioning of its SINANODE pilot manufacturing line in Moses Lake, Washington. The facility marks a step toward scaling production of its silicon‑nanowire anode product and aligns with broader efforts to localise next‑gen battery material manufacturing in North America.

This report provides a comprehensive examination of the silicon anode battery market by mapping its technology types, application segments, end‑user industries, geographic regions and strategic industry focus areas. It covers the full range of anode types from silicon‑carbon composites and pure silicon architectures to nanowire and silicon‑oxide variants, and associates each with performance metrics, manufacturing scale‑up status and compatibility with existing lithium‑ion cell lines. Application coverage spans electric vehicles, consumer electronics, grid and stationary energy storage systems, aerospace/defence and portable power tools, offering decision‑makers insight into demand patterns across mature and emerging use‑cases. End‑user segmentation evaluates automotive OEMs, consumer‑device manufacturers, utility providers, defence contractors and industrial power‑equipment makers, highlighting adoption behaviour, purchasing criteria and deployment scale. Geographically, the report analyses major regions—North America, Europe, Asia‑Pacific, South America and Middle East & Africa—drawing distinctions in manufacturing base, supply‑chain localisation, regulatory support and regional consumer behaviour. The scope also includes emerging niches such as military‑grade silicon‑anode cells, silicon‑enabled high‑density cylindrical cells and recycled silicon‑material programs. Strategic industry focus addresses partnerships, vertical‑integration moves, IP strategy, manufacturing modularity and ESG‑driven material frameworks. By delivering detailed segmentation, regional differentiation and technology‑roadmap insights, the report equips business professionals and analysts with the context and data needed to assess investment, entry and competitive strategy in the silicon anode battery domain.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 5469.24 Million |

Market Revenue in 2032 | USD 318401.7 Million |

CAGR (2025 - 2032) | 66.2% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Amprius Technologies, Inc., Enovix Corporation, Enevate Corporation, Sila Nanotechnologies, Inc., Group14 Technologies, Inc., Nexeon Limited, NanoGraf Corporation, Beijing Easpring Material Technology Co., Ltd., Shenzhen BTR New Energy Materials, Inc., Johnson Matthey Battery Materials, Hitachi Chemical Co., Ltd., Panasonic Corporation, Samsung SDI Co., Ltd., LG Energy Solution |

Customization & Pricing | Available on Request (10% Customization is Free) |