Reports

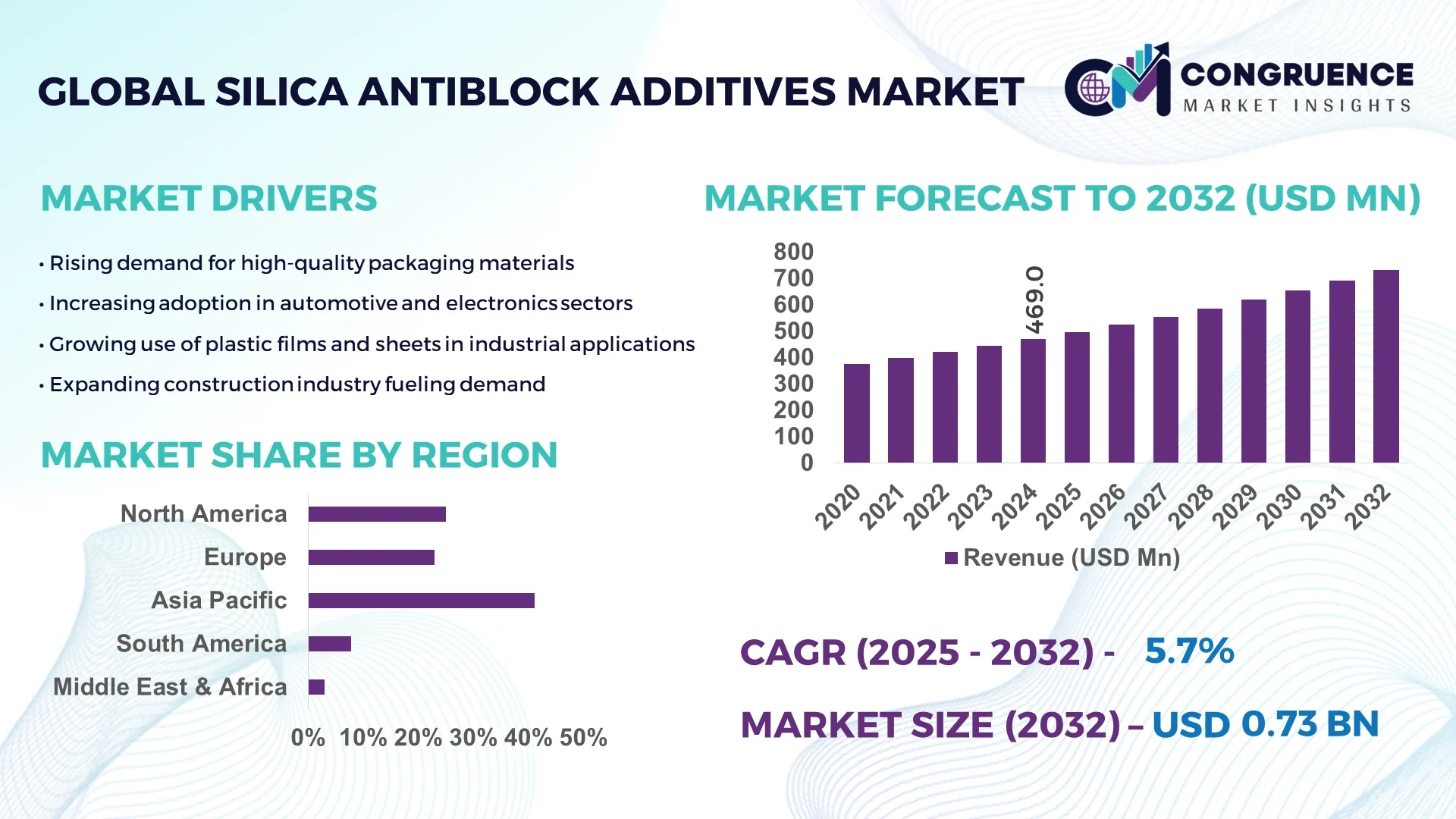

The Global Silica Antiblock Additives Market was valued at USD 469 Million in 2024 and is anticipated to reach a value of USD 730.8 Million by 2032 expanding at a CAGR of 5.7% between 2025 and 2032.

China continues to play a pivotal role in the Silica Antiblock Additives Market, with production facilities capable of processing over 150,000 metric tons annually. Significant capital investments—totaling more than USD 50 million in modernization and capacity expansion—are underway, especially in high-end packaging applications. Recent innovations include surface-treated synthetic silica grades optimized for ultra-thin PE films, enhancing free-flow and anti-caking performance.

The Silica Antiblock Additives Market serves a diverse set of industry sectors, including food packaging (with polyethylene films constituting over 70% of current application), pharmaceutical blister packaging, agricultural films, and specialty medical-grade packaging requiring USP-compliant purity. Technological breakthroughs have introduced fumed and precipitated silica with tailored surface treatments and controlled particle size, enabling superior clarity and reduced haze. Environmental regulations targeting microplastic contamination and recyclability in packaging have generated demand for inert, inorganic antiblock solutions. Economic drivers such as rising urbanization and supply chain automation amplify this demand in Asia-Pacific and Latin America. Emerging trends point toward hybrid formulations combining silica with organo-waxes to enhance sustainability and performance, while future developments may include nanocoated silica to further reduce additive loading and costs.

The integration of artificial intelligence into the Silica Antiblock Additives Market is reshaping process optimization and quality control across production and formulation stages. AI-powered particle morphology analysis enables real-time tuning of spray-drying parameters, improving particle size distribution consistency by up to 12%. Automated blending systems, guided by machine learning models, can adjust natural-synthetic silica ratios based on recipe performance metrics, ensuring consistent free-flow characteristics under variable humidity conditions.

In manufacturing plants, predictive maintenance algorithms monitor throughput and nozzle performance, reducing downtime by approximately 15%. AI-enhanced optical inspection systems evaluate film haze and clarity post-incorporation of silica additives, triggering corrective adjustments promptly. Packaging lines now feature AI-based feedback loops that calibrate additive touchpoint levels to maintain slip and antiblock performance without manual intervention, boosting overall output quality reliability. Digital twin models of compounding systems enable virtual experimentation with additive formulations, cutting trial-and-error cycles and expediting product rollouts.

By integrating AI across formulation, production, and quality assurance, the Silica Antiblock Additives Market is achieving higher throughput, improved consistency, and faster innovation cycles—transforming traditional additive workflows into digitally adaptive and data-driven operations.

“In 2024, a major silica additive producer deployed an AI-powered spray-drying control system that adjusted inlet temperature and spray pressure in real-time, resulting in a 10 % narrower particle size distribution and a 7 % reduction in production scrap.”

The Silica Antiblock Additives Market dynamics are shaped by evolving packaging requirements, supply chain efficiencies, and regulatory pressures. Increasing demand for high-clarity films in food and pharmaceutical packaging drives focus on ultra-fine silica grades. Agricultural film expansion, particularly in greenhouse and mulch applications, is amplifying volume demand. Regulatory emphasis on recyclability encourages shift toward inorganic additives that remain inert in recycling streams. Meanwhile, rising raw material costs and supply chain disruptions challenge cost management strategies. Adoption of environmental standards in developed regions compels producers to reformulate antiblock systems with reduced additive loadings. In emerging economies, rising urbanization and packaging modernization fuel uptake. Ultimately, the Silica Antiblock Additives Market is influenced by a mix of technological refinement, regulatory adaptation, and shifting end-use demands.

The food packaging sector prioritizes product visibility and hygiene, making high-clarity PE films essential. Silica antiblock additives are critical in maintaining slip and free-flow without compromising transparency. Recent formulations using sub-3 µm precipitated silica have improved film clarity by 15 %, ensuring consumer appeal. The surge in demand for ready-to-eat and fresh-food packaging amplifies this trend. Additive manufacturers are tailoring silica surfaces to minimize haze while preserving anti-block performance, reinforcing this driver’s importance in the market.

Silica prices fluctuate with changes in feedstock (e.g., quartz and sand) markets and energy costs. In 2024, production cost spikes of over 8 % were observed due to raw material shortages in key mining regions. These cost pressures squeeze margins, especially for mid-tier producers. The need to maintain price stability while managing operational cost escalations imposes pricing and profitability constraints across the Silica Antiblock Additives Market.

The sustainability trend has led to the emergence of hybrid products that blend silica with bio-based waxes or starch derivatives. These hybrids allow reduction in mineral loading by up to 30 %, while enabling enhanced recyclability. Food packaging lines adopting these formulations report smoother lamination and lower film abrasion. With growing circular economy commitments, such innovations represent a significant growth frontier in the Silica Antiblock Additives Market.

Crystalline silica concerns have prompted regulatory bodies—especially in Europe—to investigate stricter exposure limits in manufacturing plants. Compliance with occupational safety standards may require additional engineering controls and increased testing protocols. Upgrading facilities to mitigate dust emissions and monitor airborne silica levels imposes capital and operational burdens, creating entry barriers for smaller producers within the Silica Antiblock Additives Market.

Rise of Hybrid Formulations with Bio-Based Additives: Many manufacturers are now offering silica-wax hybrid antiblock blends that reduce mineral load by approximately 30%, enhancing recyclability while maintaining performance in film clarity and slip.

Adoption of Sub-3 µm Precipitated Silica for Ultra-Clear Films: Formulators increasingly use sub-3 µm silica grades, which improve film optical transparency by nearly 15%, aligning with intensifying clarity requirements in premium packaging.

Deployment of AI-Driven Spray-Drying Controls: Production facilities integrating AI-based control systems report a 10 % tighter particle size distribution, enabling better batch consistency and reducing scrap rates in silica additive compounding.

Expansion of Agricultural Film Applications: Use of silica antiblock additives in agricultural films—especially greenhouse and mulch sectors—has risen significantly due to government subsidies, enhancing demand for dust-resistant, UV-stable formulations.

The Global Silica Antiblock Additives Market is segmented into three primary dimensions: by type, by application, and by end-user. Each segment reveals unique dynamics influencing demand patterns and innovation strategies. By type, the market is characterized by natural silica and synthetic silica, each offering distinct advantages in terms of cost efficiency, purity, and performance. Applications span across packaging films, agricultural films, and industrial products, reflecting the wide utility of antiblock additives in ensuring film clarity and handling efficiency. End-user analysis highlights key adoption across industries such as food and beverage packaging, pharmaceuticals, agriculture, and industrial sectors. Among these, food packaging emerges as the most dominant consumer, while agricultural applications demonstrate rapid expansion driven by rising sustainability needs. This segmentation underscores the market’s adaptability to diverse industry demands, technological refinements in particle size engineering, and increasing regulatory emphasis on sustainable packaging practices that shape product innovation and end-user adoption.

The Silica Antiblock Additives Market comprises natural silica and synthetic silica as its main product types. Natural silica, derived from abundant raw materials, remains widely used due to its cost-effectiveness and broad availability. It continues to dominate lower-margin applications where price sensitivity is critical, particularly in general-purpose packaging films. However, synthetic silica has emerged as the leading type, primarily because of its higher purity levels, finer particle control, and superior performance in high-clarity packaging films. It is especially favored in pharmaceutical and food-grade applications where maintaining product visibility and compliance with strict safety standards is essential. Within this segment, precipitated silica is experiencing the fastest growth, as it offers excellent antiblock performance while maintaining film transparency, making it suitable for ultra-thin and multilayer films. Fumed silica also holds a niche role, particularly in specialty applications requiring high-performance films with reduced haze. Overall, synthetic silica’s precision-engineered characteristics are positioning it as the preferred type in advanced packaging markets.

Applications of silica antiblock additives are primarily segmented into packaging films, agricultural films, and industrial products. Packaging films dominate the market, accounting for the majority of usage, particularly in the food and beverage sector. The widespread demand is driven by the need for high-clarity, anti-blocking properties that ensure consumer appeal and efficient packaging line operations. Pharmaceutical blister packs and medical-grade films also contribute significantly within this category, given their stringent quality standards. The fastest-growing application is agricultural films, fueled by the global push for food security and sustainability. Rising adoption of greenhouse and mulch films requires durable, UV-stable antiblock solutions that can withstand harsh conditions while maintaining flexibility. Industrial products, such as laminates and protective films, play a smaller yet important role, particularly in construction and electronics packaging where mechanical strength and anti-block properties are critical. Together, these application areas highlight how silica antiblock additives enhance both functional performance and consumer-facing attributes across industries.

The Silica Antiblock Additives Market serves diverse end-users including food and beverage packaging, pharmaceuticals, agriculture, and industrial sectors. Food and beverage packaging stands as the leading end-user segment, supported by rising demand for flexible packaging solutions that provide product visibility, safety, and extended shelf life. The growing consumption of ready-to-eat foods and packaged fresh produce has amplified the adoption of high-clarity films enhanced with silica antiblock additives. The fastest-growing end-user is the agricultural sector, driven by increased deployment of greenhouse films and mulch films to boost crop yield efficiency. Government-backed initiatives promoting modern farming practices further strengthen this demand. The pharmaceutical industry is another significant end-user, requiring USP-compliant packaging films that safeguard drug stability and visibility. Meanwhile, industrial users employ silica antiblock additives in specialized films for construction materials, protective laminates, and electronics packaging. Collectively, these end-user groups reflect the wide applicability of silica antiblock additives, ranging from daily consumer goods to specialized industrial applications.

Asia-Pacific accounted for the largest market share at 41.2% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2025 and 2032.

The dominance of Asia-Pacific is attributed to its strong manufacturing base, large-scale packaging production, and extensive agricultural film usage in countries like China, India, and Japan. Meanwhile, North America is witnessing a surge in adoption, supported by technological advancements in packaging films, high demand from the food and beverage sector, and increasing sustainability initiatives. Europe continues to play a key role, driven by stringent regulatory frameworks, while South America and the Middle East & Africa are gradually emerging as promising regions, supported by infrastructure development and diversification of industrial applications. Overall, regional dynamics reflect the balance between established demand in Asia-Pacific and growing opportunities in technologically advanced markets such as North America and Europe.

North America held a significant share of 24.5% of the global silica antiblock additives market in 2024. The region’s strong demand is primarily fueled by the food and beverage packaging industry, supported by the rising preference for high-clarity films in consumer packaging. Pharmaceuticals also contribute substantially, given the region’s advanced healthcare infrastructure. Regulatory changes emphasizing sustainable packaging and reduced plastic waste have accelerated the use of high-performance silica additives. The United States dominates regional demand, followed by Canada, owing to strong manufacturing and R&D investments. Furthermore, digital transformation in manufacturing processes and increasing adoption of nanotechnology-based additives are reshaping the North American market landscape.

Europe accounted for 20.8% of the global silica antiblock additives market in 2024, with Germany, the United Kingdom, and France being the largest contributors. The European market is shaped by strong environmental regulations and sustainability initiatives, encouraging the use of recyclable packaging films enhanced with antiblock solutions. Regulatory bodies such as the European Chemicals Agency (ECHA) continue to influence product formulations, ensuring compliance with safety and sustainability requirements. Germany leads the market with a well-established industrial base, while the UK and France are experiencing increasing adoption in flexible packaging and pharmaceutical sectors. Moreover, Europe’s emphasis on circular economy principles and the rapid adoption of advanced production technologies support steady growth in the silica antiblock additives market.

Asia-Pacific accounted for the largest market share of 41.2% in 2024, cementing its position as the leading regional market. China dominates consumption, followed by India and Japan, due to extensive packaging film production and large-scale deployment of agricultural films. The region benefits from low-cost raw material availability, rapid industrialization, and government-backed initiatives to boost advanced manufacturing infrastructure. Additionally, the expansion of food packaging and pharmaceutical industries continues to fuel demand for high-purity silica antiblock additives. Innovation hubs in Japan and South Korea are contributing to material advancements, focusing on improved particle engineering and nanostructures. This combination of scale, cost efficiency, and innovation reinforces Asia-Pacific as the center of global silica antiblock additive consumption.

South America held an estimated 7.5% share of the global silica antiblock additives market in 2024. Brazil leads the region, followed by Argentina, driven by growing demand in food packaging and agricultural applications. Greenhouse films and protective packaging materials are key contributors, as the agricultural sector increasingly embraces modernized farming practices. Infrastructure development and expanding industrial activities are also fostering demand for advanced films with improved antiblock performance. Supportive government trade policies and foreign investments in packaging industries are opening new opportunities. The region’s rising consumer demand for packaged food and beverage products is further strengthening the market outlook for silica antiblock additives.

The Middle East & Africa accounted for 6.0% of the global silica antiblock additives market in 2024. Countries such as the United Arab Emirates and South Africa are at the forefront of adoption, driven by growing demand in construction, packaging, and oil & gas-related applications. The regional market benefits from modernization in manufacturing processes and increased focus on sustainable packaging materials. Trade partnerships and government-backed diversification strategies, particularly in the Gulf Cooperation Council (GCC) countries, are encouraging the use of advanced film materials. South Africa’s industrial and agricultural sectors further enhance the need for antiblock solutions in flexible films. With infrastructure growth and a shift toward innovative industrial practices, the Middle East & Africa is gradually positioning itself as a promising growth market.

The Silica Antiblock Additives Market is characterized by moderate to high competition, with more than 25 globally active players operating across diversified geographies. The competitive environment is defined by companies pursuing strategies such as product innovation, acquisitions, and expansion into high-growth regions. Leading players focus on producing high-performance silica antiblock additives that improve film quality, reduce haze, and provide better processing efficiency. Partnerships with packaging manufacturers and resin producers are increasingly shaping the competitive dynamics, as companies strive to integrate additive technologies directly into film production lines. Innovation trends such as nanoporous silica particles and eco-friendly formulations are gaining traction, as sustainability and regulatory compliance remain critical differentiators. Additionally, the market is witnessing heightened R&D activity aimed at optimizing particle size distribution and surface chemistry, enabling better compatibility with diverse polymers. With multiple small and mid-sized firms competing alongside established chemical giants, differentiation based on technology, product consistency, and cost-effectiveness is becoming increasingly significant in defining long-term market positioning.

Evonik Industries AG

W.R. Grace & Co.

PQ Corporation

Tosoh Silica Corporation

Madhu Silica Pvt. Ltd.

Solvay S.A.

Huber Engineered Materials

Fubao Group Co., Ltd.

PPG Industries, Inc.

Nissan Chemical Corporation

Technological advancements in the Silica Antiblock Additives Market are reshaping how additives are formulated and applied in polymer films and packaging materials. One of the most significant developments is the engineering of ultra-fine and nanoporous silica particles that enhance optical clarity while minimizing film blocking without compromising mechanical strength. These advanced grades allow manufacturers to achieve better dispersion, improved slip properties, and higher thermal stability in polyethylene and polypropylene films.

Surface modification technologies have also gained momentum, enabling the tailoring of silica’s chemical properties to improve compatibility with specific polymer systems. For instance, hydrophobic surface treatments reduce moisture absorption and improve dispersion in high-humidity environments, which is crucial for food and pharmaceutical packaging. Automation and digitalization in additive dosing systems are further optimizing production efficiency by ensuring precise control over additive concentrations, reducing waste, and maintaining product uniformity.

Sustainability-focused innovations are another prominent area of focus. Companies are developing eco-friendly silica additives derived from renewable sources or incorporating recyclable carrier materials to align with global regulations on plastic reduction. Additionally, hybrid silica solutions combining antiblock with UV resistance, antistatic, or antimicrobial functionalities are gaining traction, offering multifunctional benefits to end-users. These innovations underscore a broader industry shift toward performance-driven and environmentally responsible additive solutions, providing a competitive edge to players investing in advanced R&D.

• In February 2023, Evonik expanded its production capacity for precipitated silica to meet growing demand from the packaging and polymer film sectors, introducing new grades optimized for transparency and processability.

• In July 2023, PQ Corporation launched a high-dispersion silica antiblock additive designed to enhance optical clarity in thin-gauge polyethylene films used in food and consumer packaging.

• In April 2024, Tosoh Silica Corporation announced advancements in nanoporous silica additives that provide superior antiblocking performance while reducing haze levels, catering to premium packaging applications.

• In May 2024, Madhu Silica Pvt. Ltd. introduced sustainable silica antiblock solutions developed from renewable feedstocks, aligning with global sustainability goals in polymer film manufacturing.

The scope of the Silica Antiblock Additives Market Report covers a comprehensive analysis of the industry’s key drivers, market dynamics, and strategic opportunities across global and regional markets. This report provides detailed insights into segmentation by type, including natural silica and synthetic silica, each playing a distinct role in enhancing polymer film performance. It also examines applications across packaging, agriculture, electronics, and other end-use industries, highlighting how demand patterns vary with evolving consumer preferences and technological innovation.

Geographically, the report encompasses major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with each region analyzed for demand trends, industrial adoption, and regulatory frameworks. The report also focuses on industry-specific growth drivers such as the packaging industry’s shift toward high-clarity and recyclable films, along with the agricultural sector’s rising adoption of advanced polyethylene films for greenhouse and mulching applications.

Additionally, the scope highlights technological transformations influencing the market, including nanotechnology, surface modification processes, and multifunctional additive development. Emerging trends such as eco-friendly silica formulations, smart packaging, and regional supply chain optimization are also addressed. By combining insights on product innovation, regional developments, and end-user adoption, this report offers a holistic overview tailored to business leaders and decision-makers seeking to navigate the evolving competitive and technological landscape of the silica antiblock additives industry.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 469 Million |

| Market Revenue (2032) | USD 730.8 Million |

| CAGR (2025–2032) | 5.7% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Evonik Industries AG, W.R. Grace & Co., PQ Corporation, Tosoh Silica Corporation, Madhu Silica Pvt. Ltd., Solvay S.A., Huber Engineered Materials, Fubao Group Co., Ltd., PPG Industries, Inc., Nissan Chemical Corporation |

| Customization & Pricing | Available on Request (10% Customization is Free) |