Reports

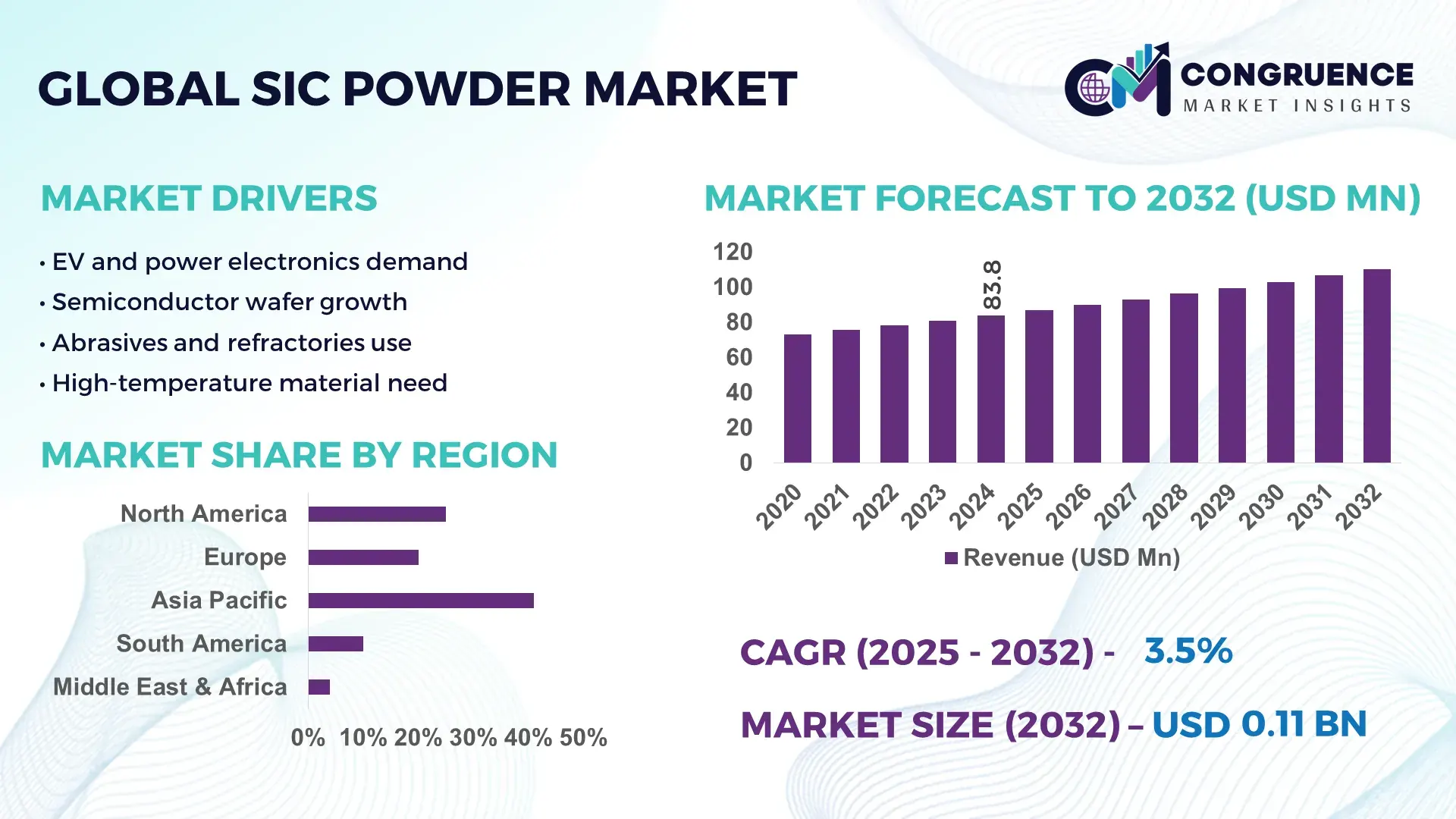

The Global SiC Powder Market was valued at USD 83.83 Million in 2024 and is anticipated to reach a value of USD 110.39 Million by 2032 expanding at a CAGR of 3.5% between 2025 and 2032. This growth is supported by rising demand for high-performance ceramic materials in power electronics, electric vehicles, renewable energy systems, and advanced industrial manufacturing.

China represents the most significant national market for SiC powder, supported by large-scale industrial production capacity, vertically integrated supply chains, and sustained investment in advanced materials. The country operates multiple SiC manufacturing clusters with combined output capacity estimated at over 70,000 metric tons per year across industrial-grade and high-purity segments. More than 40% of domestic SiC powder consumption is linked to electronics, semiconductors, and EV power modules, reflecting strong downstream integration. Public and private investment programs focused on wide-bandgap semiconductor development and energy-efficient manufacturing continue to drive technology upgrades in purification, particle size control, and high-purity processing, strengthening China’s industrial position in both volume and quality output.

• Market Size & Growth: USD 83.83 Million in 2024, projected to reach USD 110.39 Million by 2032 at a CAGR of 3.5%, driven by expanding use in EV power electronics, industrial ceramics, and semiconductor manufacturing.

• Top Growth Drivers: EV component adoption (45%), semiconductor integration (38%), industrial manufacturing upgrades (29%).

• Short-Term Forecast: By 2028, manufacturers are expected to achieve up to 22% cost efficiency improvements through process optimization and higher yield purification technologies.

• Emerging Technologies: Nano-scale SiC powders, ultra-high-purity refining (>99.9%), and additive manufacturing feedstock development.

• Regional Leaders: Asia Pacific projected at ~USD 48 Million by 2032 with strong electronics demand, North America at ~USD 34 Million driven by aerospace and power devices, Europe at ~USD 28 Million supported by renewable energy and automotive electrification.

• Consumer/End-User Trends: Semiconductor fabs and EV manufacturers increasingly specify fine and ultra-fine powders for thermal management and power conversion efficiency.

• Pilot or Case Example: A 2025 EV inverter pilot project using ultra-fine SiC powders achieved an 18% efficiency improvement and 12% thermal loss reduction.

• Competitive Landscape: A market leader with ~14% share, followed by Saint-Gobain, ESD-SIC, Ningxia Tianyuan, Wolfspeed, and Shin-Etsu Chemical.

• Regulatory & ESG Impact: Energy-efficiency regulations and decarbonization targets are accelerating adoption of SiC-based power devices and materials.

• Investment & Funding Patterns: Recent industry investments exceed USD 500 Million globally, focused on capacity expansion, purification technologies, and semiconductor-grade material development.

• Innovation & Future Outlook: Integration with wide-bandgap semiconductor platforms, growth in aerospace and hydrogen energy applications, and increasing demand for high-thermal-conductivity materials will shape future market evolution.

The SiC powder market is primarily driven by electronics and semiconductors (around 38% of demand), automotive and EV power systems (about 27%), and industrial ceramics and abrasives (roughly 22%), with smaller shares in aerospace, energy, and metallurgy. Recent innovations include ultra-fine and nano-grade powders for precision electronics, higher purity refining processes to support semiconductor fabrication, and tailored particle morphologies for additive manufacturing. Regulatory pressure to improve energy efficiency and reduce emissions is accelerating adoption in power electronics and renewable energy systems, particularly in Asia Pacific and Europe. Regional consumption growth is strongest in Asia Pacific due to electronics manufacturing expansion, while North America focuses on aerospace and advanced power systems, and Europe emphasizes automotive electrification and renewable integration. Emerging trends include increased use of SiC in hydrogen energy infrastructure, solid-state power devices, and next-generation mobility platforms, positioning the market for steady, technology-driven expansion over the coming decade.

The strategic relevance of the SiC Powder Market lies in its role as a foundational input for wide-bandgap semiconductors, high-temperature ceramics, advanced abrasives, and energy-efficient power electronics. SiC-based power devices enable higher switching frequencies, lower conduction losses, and superior thermal performance compared to silicon, directly influencing energy efficiency, system miniaturization, and reliability across automotive, renewable energy, and industrial automation sectors. For example, silicon carbide power devices deliver approximately 40% lower switching losses compared to conventional silicon IGBTs, allowing OEMs to reduce cooling system size, weight, and total system energy losses. This performance advantage positions SiC powder as a strategic enabler for electrification and decarbonization strategies globally.

Asia Pacific dominates SiC powder production volume due to its large electronics and materials manufacturing base, while North America leads in advanced adoption, with roughly 55% of power electronics manufacturers actively transitioning to SiC-based device architectures. This regional differentiation reflects a dual strategy: capacity-driven supply in Asia and technology-driven demand in developed markets. By 2028, AI-driven process control and digital twins in powder synthesis and purification are expected to reduce defect rates and scrap levels by approximately 20%, improving yield consistency and lowering operational risk for producers.

From a compliance and ESG perspective, manufacturers are committing to sustainability metrics such as 25% reductions in energy consumption and 30% increases in material recycling rates by 2030 through improved furnace efficiency, waste heat recovery, and closed-loop processing. In 2024, a major Japanese materials producer achieved an estimated 18% reduction in energy usage per kilogram of SiC powder by deploying AI-based furnace optimization and real-time quality monitoring systems.

Collectively, these trends position the SiC Powder Market as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term competitiveness across electrification, clean energy, and advanced manufacturing value chains.

The transition toward electric vehicles, renewable energy, and energy-efficient industrial systems is a primary driver of the SiC Powder Market. SiC-based power electronics enable higher efficiency in inverters, chargers, and grid equipment, reducing energy losses and improving thermal stability. Electric vehicle powertrains using SiC devices can achieve up to 5–10% higher overall efficiency, extending driving range and reducing battery size requirements. Renewable energy inverters based on SiC can operate at higher switching frequencies, improving power conversion efficiency and reducing system size. These performance gains translate into lower lifecycle costs and improved sustainability, making SiC powder a preferred input for manufacturers seeking to meet efficiency standards and decarbonization targets. As governments and corporations commit to net-zero and energy transition goals, demand for SiC-enabled technologies continues to rise, directly supporting growth in SiC powder consumption.

The production of SiC powder is energy-intensive, requiring extremely high temperatures and precise process control, which increases operational costs and carbon footprint. Electricity and energy costs can account for a substantial portion of total manufacturing expenses, making producers sensitive to energy price volatility. In addition, high-purity grades needed for semiconductor applications require multiple purification and classification steps, increasing capital and operating expenditures. Smaller producers may face difficulty scaling production while meeting quality and environmental standards, limiting market entry and competition. Regulatory pressure to reduce industrial emissions further increases compliance costs, as firms must invest in cleaner energy sources, emissions control systems, and waste management infrastructure, which can constrain short-term profitability and expansion.

Emerging applications in additive manufacturing, aerospace, hydrogen energy systems, and next-generation power electronics present significant opportunities for the SiC Powder Market. Additive manufacturing is enabling the production of complex SiC components for high-temperature and high-stress environments, opening new design possibilities in aerospace and industrial equipment. Hydrogen electrolyzers and fuel cell systems increasingly require materials with high thermal and chemical stability, supporting SiC adoption. Furthermore, the shift toward solid-state power devices and ultra-fast charging infrastructure creates demand for higher purity and more precisely engineered powders. These new use cases expand the addressable market beyond traditional abrasives and refractories into high-value, technology-driven segments, encouraging investment in innovation and specialized production capabilities.

The SiC Powder Market faces challenges from supply chain concentration, long lead times for capacity expansion, and tightening regulatory requirements. Production depends on access to high-quality carbon and silicon feedstocks, specialized furnace equipment, and skilled technical labor, all of which can be subject to geopolitical, logistical, or economic disruption. At the same time, environmental regulations governing emissions, energy use, and industrial waste are becoming more stringent, particularly in developed markets. Compliance requires continuous monitoring, reporting, and investment in cleaner technologies, increasing operational complexity. These factors can slow expansion, increase risk, and require producers to balance cost competitiveness with resilience and regulatory adherence in an increasingly demanding business environment.

• High-Purity SiC Adoption in Power Electronics Manufacturing: Semiconductor and power device manufacturers are rapidly shifting toward ≥99.9% purity SiC powders for MOSFETs and Schottky diodes, with over 48% of new power module production lines now specifying ultra-high-purity grades. Device yields have improved by approximately 15%, while defect densities have fallen by nearly 20%, supporting higher reliability requirements in EV inverters and fast-charging systems.

• Rise in Modular and Prefabricated Construction Applications: The adoption of modular construction is reshaping demand dynamics in the SiC Powder market, particularly for cutting, grinding, and precision shaping tools. Around 55% of new modular projects report cost benefits through prefabrication, while automated pre-bending and cutting systems have reduced on-site labor needs by nearly 30% and shortened construction timelines by 20%, increasing demand for SiC-based tooling.

• Expansion of SiC Use in Renewable Energy and Grid Infrastructure: Approximately 42% of new solar and wind power installations now incorporate SiC-based power conversion systems, enabling up to 8% higher conversion efficiency and 25% reductions in thermal losses. This trend is driving higher consumption of fine and ultra-fine SiC powders for advanced power electronics used in inverters, transformers, and energy storage interfaces.

• Process Digitalization and Yield Optimization in SiC Production: Around 35% of large SiC powder manufacturers have implemented AI-enabled furnace control and digital quality monitoring, achieving scrap reductions of 18% and energy-use efficiency improvements of 12%. These digital upgrades are enabling tighter particle size distribution control and faster scale-up of high-grade powder production to meet rising industrial and electronics demand.

The SiC Powder market is segmented by type, application, and end-user, reflecting the material’s wide industrial relevance and increasing specialization. By type, the market is divided into standard industrial-grade, high-purity semiconductor-grade, and ultra-fine or nano SiC powders, each serving distinct performance and quality requirements. Applications range from abrasives and refractories to power electronics, renewable energy systems, automotive components, and aerospace materials, with electronics-driven demand gaining structural importance. End-user segmentation shows strong concentration in semiconductor manufacturers, automotive OEMs, and industrial equipment producers, while construction, energy utilities, and aerospace companies represent secondary but growing demand centers. This segmentation structure highlights a gradual shift away from commodity uses toward higher-value, technology-intensive applications where performance, purity, and reliability are critical decision criteria.

The largest share of the SiC Powder market is currently held by standard industrial-grade SiC powder, which accounts for approximately 46% of total volume, primarily due to its widespread use in abrasives, cutting tools, and refractory products. High-purity semiconductor-grade SiC powders represent about 32% of adoption, driven by demand from power electronics, EV inverters, and fast-charging infrastructure. However, ultra-fine and nano-sized SiC powders are the fastest-growing type, expanding at an estimated 9.2% annually, supported by increasing use in advanced ceramics, additive manufacturing, and next-generation semiconductor processes where precise particle size and morphology are critical. The remaining specialty and composite grades together contribute roughly 22% of demand, serving niche applications such as aerospace coatings, biomedical components, and hydrogen energy systems.

Abrasives and refractory materials remain the leading application segment, accounting for approximately 39% of SiC powder usage, supported by steady demand from metalworking, construction, and heavy industry. Power electronics and semiconductor applications follow closely with about 34% adoption, reflecting the growing importance of SiC in EVs, renewable energy inverters, and data center power systems. However, power electronics is the fastest-growing application area, with usage expanding at an estimated 10.1% annually as manufacturers transition from silicon to wide-bandgap materials. Other applications, including aerospace, energy storage, and additive manufacturing, together represent around 27% of demand and are gaining relevance due to performance and weight-reduction requirements.

Semiconductor and power device manufacturers form the largest end-user group, accounting for approximately 41% of total SiC powder demand, followed by automotive OEMs at about 28%, reflecting strong electrification trends. Industrial equipment and construction firms together contribute roughly 21%, while aerospace, energy utilities, and research institutions make up the remaining 10%. Automotive and mobility-related users are the fastest-growing end-user segment, expanding at an estimated 11.3% annually as EV platforms increasingly integrate SiC-based power modules to improve efficiency and reduce system weight. Adoption rates among automotive Tier-1 suppliers now exceed 60% for new EV powertrain designs.

Asia-Pacific accounted for the largest market share at 48% in 2024 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2025 and 2032.

Asia-Pacific’s leadership is driven by high-volume manufacturing in China, Japan, and South Korea, which together account for more than 65% of global SiC powder production capacity. China alone contributes approximately 38% of total consumption due to strong demand from electronics, EV power modules, and industrial abrasives. Europe represents around 26% of the market, supported by automotive electrification and renewable energy expansion, while North America holds roughly 19%, driven by aerospace, power electronics, and semiconductor investments. South America and the Middle East & Africa together account for about 7%, reflecting emerging adoption in infrastructure, energy, and industrial processing. Regional differences in regulatory intensity, manufacturing scale, and technology adoption rates shape distinct demand patterns and investment priorities across the global SiC Powder Market.

North America accounts for approximately 19% of the global SiC Powder Market, with demand concentrated in the United States and Canada. Key industries include semiconductors, electric vehicles, aerospace, and renewable energy infrastructure, where high thermal stability and efficiency are critical. Government incentives for domestic semiconductor manufacturing and clean energy deployment are accelerating adoption of SiC-based components. Over 60% of new EV powertrain designs in the region now integrate SiC power devices. Local players are expanding capacity for high-purity and ultra-fine grades to support power electronics and defense applications. Digital manufacturing and AI-driven quality control systems are increasingly used to improve yield and consistency. Regional consumer behavior shows higher enterprise adoption in automotive, energy, and high-performance computing, where reliability and efficiency gains directly impact operating costs and sustainability targets.

Europe represents about 26% of the SiC Powder Market, led by Germany, France, and the UK. Automotive electrification, renewable energy systems, and industrial automation are the primary demand drivers. Regulatory bodies enforcing carbon reduction and energy efficiency targets are pushing manufacturers to adopt SiC-based power electronics and high-performance ceramics. Around 52% of new industrial power systems in the region now specify SiC components for higher efficiency and lower losses. Local manufacturers are investing in low-emission production methods and recyclable materials to align with sustainability initiatives. European consumers and enterprises exhibit strong preference for energy-efficient, compliant technologies, making regulatory alignment a key purchasing criterion.

Asia-Pacific is the largest market with approximately 48% share, dominated by China, Japan, and South Korea. The region benefits from large-scale electronics manufacturing, automotive production, and advanced materials clusters. China alone accounts for roughly 38% of global SiC powder consumption, driven by semiconductors, EVs, and industrial abrasives. Regional innovation hubs are advancing purification and nano-particle processing technologies to support next-generation electronics. Local players are scaling high-purity capacity and integrating AI-based process optimization. Consumer behavior reflects strong industrial demand linked to electronics exports, infrastructure expansion, and electrified mobility.

South America accounts for approximately 4% of the global market, led by Brazil and Argentina. Demand is tied to industrial processing, energy infrastructure, and mining equipment, where SiC is used for wear resistance and thermal stability. Government programs supporting renewable energy and industrial modernization are stimulating adoption. Brazil is investing in grid upgrades and EV infrastructure, increasing demand for SiC-based power electronics. Regional buyers prioritize cost-effective, durable materials, with adoption often driven by lifecycle cost reduction and improved equipment reliability.

The Middle East & Africa represent around 3% of global demand, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Oil and gas, construction, and renewable energy projects are the main drivers, where SiC is valued for high-temperature and corrosive environments. Governments are promoting industrial diversification and clean energy, supporting adoption in power conversion and industrial equipment. Local players focus on importing high-quality powders for specialized applications. Buyers in the region emphasize durability, thermal performance, and long-term reliability due to harsh operating conditions.

• China SiC Powder Market: 38% share — driven by large-scale manufacturing capacity and strong demand from electronics, EV, and industrial sectors.

• Japan SiC Powder Market: 14% share — supported by advanced semiconductor fabrication, materials innovation, and high adoption in power electronics.

The SiC Powder market is moderately fragmented, with more than 40 active commercial producers globally, ranging from large multinational materials companies to specialized high-purity powder manufacturers. The top five companies collectively account for approximately 52% of total global supply, indicating moderate consolidation with ongoing competitive pressure from regional and niche suppliers. Competition is primarily driven by product purity, particle size control, supply reliability, and the ability to support high-volume industrial and semiconductor-grade requirements. Around 58% of leading suppliers have launched new high-purity or ultra-fine powder grades over the past three years, reflecting a strong innovation focus. Strategic partnerships between powder producers and semiconductor or EV manufacturers have increased by roughly 35%, aimed at securing long-term supply agreements and co-developing application-specific materials. Capacity expansion remains a key strategy, with over 30% of major players announcing new furnaces, purification lines, or digital quality systems to improve yield and consistency. Mergers and minority stake investments are being used selectively to access regional markets and specialized technologies, particularly in Asia-Pacific and Europe. Overall, the competitive environment is shaped by a balance between scale advantages, technological differentiation, and the ability to meet increasingly stringent quality and sustainability expectations.

Saint-Gobain

Shin-Etsu Chemical Co., Ltd.

Wolfspeed, Inc.

Showa Denko Materials Co., Ltd.

ESD-SIC

Ningxia Tianyuan Manganese Industry Group

Washington Mills

Tokai Carbon Co., Ltd.

Technological advancements are reshaping the SiC Powder Market, particularly in high-purity production, particle size control, and application-specific customization. High-purity SiC powders with ≥99.9% purity are increasingly used in power electronics, EV inverters, and semiconductor fabrication, improving device reliability and reducing defect densities by approximately 12–18% during production. Ultra-fine and nano-sized powders are emerging as critical inputs for additive manufacturing and advanced ceramics, enabling precision components with tighter tolerances and enhanced thermal and mechanical properties. Particle size distribution and morphology optimization have improved surface area control by nearly 20%, supporting applications in high-performance abrasives and specialty coatings.

Digitalization and AI-driven process control are transforming production efficiency. About 35% of leading SiC powder manufacturers have implemented AI-enabled furnace control and real-time quality monitoring, achieving scrap reduction of 15–18% and energy consumption improvements of 10–12%. Advanced purification techniques, including chemical vapor deposition and carbothermal reduction, are enhancing consistency in impurity levels and supporting scalable industrial production.

Emerging technologies such as hybrid SiC composite powders, surface-coated particles, and additive manufacturing feedstocks are extending market applications to aerospace, hydrogen energy systems, and next-generation electronics. Innovations in automated classification and grading systems now allow manufacturers to produce powders with consistent particle shapes, sizes, and surface characteristics, improving integration into high-value applications. These technological trends collectively enhance performance, reduce operational inefficiencies, and position SiC powders as a critical material for industrial, automotive, and semiconductor sectors, supporting long-term competitiveness and strategic adoption.

• In March 2024, Wolfspeed extended a long‑term supply contract worth approximately USD 275 million with a major global semiconductor business to deliver 150 mm silicon carbide wafers, reinforcing its role as a key materials supplier and expanding market presence in high‑performance SiC materials.

• In 2023–2024, multiple Chinese SiC powder manufacturers collectively increased production capacity by around 25% to support surging electric vehicle and power electronics demand, reflecting regional scaling efforts to meet industrial consumption growth.

• During 2024, Saint‑Gobain announced expansion of its SiC powder production capabilities to serve the semiconductor and advanced materials segments, aligning capacity with rising requirements from EV, renewable energy, and industrial applications.

• In 2023, Fiven launched its new SIKA® TECH silicon carbide product line designed for advanced technical ceramics, improving performance characteristics and broadening the application scope of SiC powders in high‑temperature and structural material markets.

The SiC Powder Market Report provides a comprehensive evaluation of the global silicon carbide powder landscape, covering detailed segmentation by product type, particle size, purity grade, application area, and end‑user industry. The report examines granular distinctions between industrial‑grade, high‑purity, and nano/ultra‑fine SiC powders and their respective performance attributes, particle uniformity specifications, and morphological differences. Geographic scope includes regional analysis of North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with quantitative insights on volume production, consumption trends, and regional infrastructure forces shaping SiC demand patterns. Application coverage spans abrasives and refractories, power electronics and semiconductors, automotive powertrain systems, renewable energy converters, aerospace components, advanced ceramics, and emerging sectors such as hydrogen energy and 5G infrastructure materials.

Technological focus highlights current synthesis and processing technologies, including carbothermal reduction, chemical vapor deposition refinements, and digital quality control systems enhancing particle consistency and reducing defect incidence. The report assesses innovation trends such as tailored morphologies for additive manufacturing, surface‑engineered SiC powders for enhanced sintering, and advanced classification systems improving application fit. End‑user analysis contextualizes adoption behaviors in semiconductor fabs, automotive OEMs, industrial equipment producers, and energy infrastructure developers, while reflecting regulatory and sustainability pressures impacting production methods and material selection. Strategic insights include competitive dynamics, capacity expansions, partnership ecosystems, and investment initiatives addressing supply chain resilience and performance optimization. This broad scoping ensures decision‑makers have actionable intelligence to evaluate market opportunities, technology drivers, and competitive positioning within the SiC powder value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 83.83 Million |

|

Market Revenue in 2032 |

USD 110.39 Million |

|

CAGR (2025 - 2032) |

3.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Saint-Gobain, Shin-Etsu Chemical Co., Ltd. , Wolfspeed, Inc. , Showa Denko Materials Co., Ltd., ESD-SIC, Ningxia Tianyuan Manganese Industry Group, Washington Mills , Tokai Carbon Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |