Reports

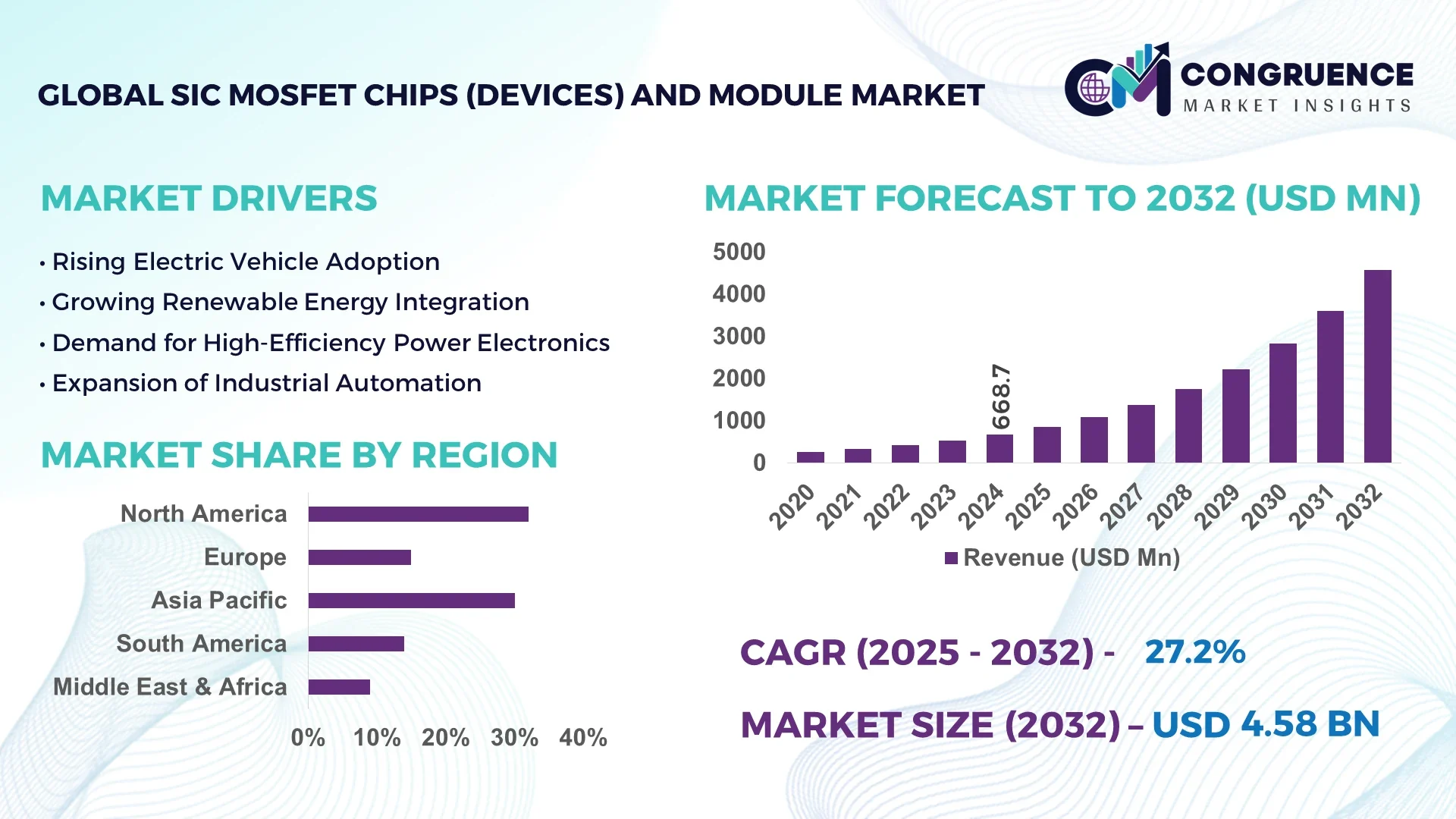

The Global SiC MOSFET Chips (Devices) and Module Market was valued at USD 668.69 Million in 2024 and is anticipated to reach a value of USD 4582.7 Million by 2032, expanding at a CAGR of 27.2% between 2025 and 2032. This robust growth is primarily driven by the increasing demand for energy-efficient power electronics and the rapid adoption of electric vehicles globally.

The United States stands as a prominent player in the SiC MOSFET Chips and Module Market, with significant investments bolstering its position. In 2024, the U.S. government allocated substantial funding through initiatives like the CHIPS and Science Act, aiming to enhance domestic semiconductor manufacturing capabilities. This strategic move is complemented by private sector investments, including a notable $5.4 billion investment by STMicroelectronics to establish a state-of-the-art SiC semiconductor plant in Catania, Italy, with approximately €2 billion in state support. Such investments underscore the nation's commitment to advancing SiC technology and meeting the escalating demand for high-performance power devices.

Market Size & Growth: The market was valued at USD 668.69 million in 2024 and is projected to reach USD 4.58 billion by 2032, growing at a CAGR of 27.2%. This growth is attributed to the increasing demand for energy-efficient power electronics and the rapid adoption of electric vehicles globally.

Top Growth Drivers: Adoption of electric vehicles (40%), demand for energy-efficient power electronics (35%), and advancements in renewable energy technologies (25%).

Short-Term Forecast: By 2028, the market is expected to witness a 15% reduction in power loss and a 20% increase in switching frequency, driven by technological advancements in SiC MOSFETs.

Emerging Technologies: Integration of wide-bandgap semiconductors, advancements in packaging technologies, and the development of high-temperature resistant materials.

Regional Leaders: North America (USD 1.5 billion by 2032), Europe (USD 1.2 billion by 2032), and Asia-Pacific (USD 1.8 billion by 2032). North America leads in adoption due to substantial public and private investments in domestic manufacturing.

Consumer/End-User Trends: Increased adoption in electric vehicles, renewable energy systems, and industrial automation sectors, with a growing preference for high-efficiency power modules.

Pilot or Case Example: In 2024, a leading automotive OEM implemented SiC MOSFET-based power modules in their electric vehicle platform, resulting in a 25% improvement in energy efficiency and a 30% reduction in system weight.

Competitive Landscape: Leading players include Wolfspeed (30% market share), Infineon Technologies, STMicroelectronics, ON Semiconductor, and ROHM Semiconductor.

Regulatory & ESG Impact: Stringent emission regulations and incentives for electric vehicle adoption are accelerating the demand for SiC-based power modules, aligning with environmental, social, and governance (ESG) objectives.

Investment & Funding Patterns: Recent investments exceed USD 10 billion, with a significant focus on establishing new manufacturing facilities and advancing research and development in SiC technologies.

Innovation & Future Outlook: Ongoing innovations in packaging, thermal management, and integration of SiC MOSFETs with other wide-bandgap materials are expected to drive the next wave of growth in the market.

The SiC MOSFET Chips (Devices) and Module Market is experiencing significant growth, driven by advancements in semiconductor technologies and increasing demand for energy-efficient solutions. Key industry sectors such as automotive, renewable energy, and industrial automation are contributing to this expansion. Technological innovations, including the development of high-temperature resistant materials and integration of wide-bandgap semiconductors, are enhancing the performance and efficiency of SiC-based power devices. Regulatory incentives and environmental considerations are further accelerating the adoption of SiC technologies, positioning the market for sustained growth in the coming years.

The SiC MOSFET Chips and Module Market has become strategically significant due to its pivotal role in enhancing energy efficiency across various sectors. SiC MOSFETs offer substantial improvements over traditional silicon-based devices, delivering up to 30% higher efficiency and 20% faster switching speeds. This performance enhancement is particularly beneficial in applications like electric vehicles (EVs), renewable energy systems, and industrial automation. By 2028, advancements in packaging technologies are expected to reduce thermal losses by 15%, further boosting system efficiency.

Regionally, North America leads in adoption, with approximately 60% of enterprises integrating SiC MOSFETs into their systems, driven by substantial investments and government incentives. In contrast, Asia-Pacific dominates in volume, with China accounting for over 40% of global SiC MOSFET production, supported by robust manufacturing capabilities and supply chain infrastructure.

In terms of compliance and sustainability, firms are committing to significant environmental goals, such as a 25% reduction in carbon emissions by 2030, aligning with global ESG standards. For instance, in 2023, a leading European automaker achieved a 20% improvement in energy efficiency through the integration of SiC MOSFETs in their EV platforms.

Looking ahead, the SiC MOSFET Chips and Module Market is positioned as a cornerstone for resilience, compliance, and sustainable growth, driven by continuous technological advancements and increasing global demand for energy-efficient solutions.

The SiC MOSFET Chips and Module Market is experiencing dynamic growth, influenced by technological advancements and increasing demand for energy-efficient solutions. Key trends include the adoption of wide-bandgap semiconductors, advancements in packaging technologies, and the integration of SiC MOSFETs in various applications such as electric vehicles, renewable energy systems, and industrial automation. These developments are driving the market towards higher efficiency, reduced system size, and improved thermal performance, positioning SiC MOSFETs as a critical component in modern power electronics.

The surge in electric vehicle adoption is a primary driver for the SiC MOSFET Chips and Module Market. SiC MOSFETs enable faster switching speeds and higher efficiency, which are crucial for enhancing EV performance. For instance, SiC-based inverters and onboard chargers contribute to longer driving ranges and reduced charging times. As governments implement stricter emissions regulations and offer incentives for electric mobility, the demand for SiC MOSFETs in EV applications is expected to continue its upward trajectory, fostering market growth.

High production costs pose a significant restraint to the SiC MOSFET Chips and Module Market. The manufacturing process for SiC MOSFETs involves complex techniques and high-purity materials, leading to increased production expenses compared to traditional silicon-based devices. These elevated costs can hinder the widespread adoption of SiC MOSFETs, particularly in price-sensitive applications. Additionally, the limited availability of high-quality SiC substrates further exacerbates the cost challenges, impacting the scalability of production and market penetration.

The expansion of renewable energy sources presents significant opportunities for the SiC MOSFET Chips and Module Market. SiC MOSFETs are well-suited for power conversion applications in solar inverters and wind turbines due to their high efficiency and thermal performance. As the global shift towards renewable energy intensifies, the demand for efficient power electronics to manage and convert energy is increasing. This trend opens avenues for SiC MOSFETs to play a pivotal role in enhancing the performance and reliability of renewable energy systems, driving market growth.

Supply chain limitations present a notable challenge to the SiC MOSFET Chips and Module Market. The production of SiC MOSFETs relies on specialized materials and advanced manufacturing processes, which are concentrated in specific regions. Disruptions in the supply chain, such as geopolitical tensions or raw material shortages, can lead to delays and increased costs. These supply chain vulnerabilities can impede the timely delivery of SiC MOSFETs to end-users, affecting the overall market growth and stability. Addressing these challenges requires diversification of supply sources and investment in resilient manufacturing capabilities.

Surge in Electric Vehicle Integration: The integration of SiC MOSFETs in electric vehicles (EVs) is accelerating, driven by their superior efficiency and thermal performance. In 2025, approximately 30% of new EV models incorporated SiC MOSFETs, reflecting a 15% increase from the previous year. This adoption enhances battery performance and reduces charging times, aligning with the automotive industry's shift towards electrification.

Advancements in Wide-Bandgap Semiconductor Technology: Technological innovations in wide-bandgap semiconductors are propelling the SiC MOSFET market forward. In 2025, the development of 8-inch SiC wafers became more prevalent, improving manufacturing efficiency and device performance. These advancements enable higher voltage and power density applications, expanding the scope of SiC MOSFET utilization across various industries.

Expansion in Renewable Energy Applications: The renewable energy sector is increasingly adopting SiC MOSFETs to enhance power conversion efficiency. In 2025, the use of SiC MOSFETs in solar inverters and wind turbine systems rose by 20%, driven by their ability to operate at higher temperatures and switch frequencies. This trend supports the global transition towards sustainable energy solutions.

Growth in Industrial Automation and Robotics: The industrial automation sector is experiencing significant growth, with SiC MOSFETs playing a crucial role in enhancing system efficiency. In 2025, the adoption of SiC MOSFETs in motor drives and variable frequency drives (VFDs) increased by 18%, attributed to their high switching speeds and reduced power losses. This trend underscores the importance of SiC MOSFETs in modernizing industrial processes.

The SiC MOSFET Chips (Devices) and Module Market is segmented based on type, application, and end-user industry. By type, the market is divided into SiC MOSFET chips and SiC MOSFET modules. SiC MOSFET chips are primarily utilized in applications requiring discrete devices, offering advantages in terms of size and integration. SiC MOSFET modules, on the other hand, are employed in power systems requiring higher power handling capabilities and thermal management. Applications span across automotive, industrial, renewable energy, and consumer electronics sectors, each leveraging the unique properties of SiC MOSFETs to enhance efficiency and performance. End-users include original equipment manufacturers (OEMs), system integrators, and aftermarket service providers, each contributing to the market's growth through adoption and integration of SiC MOSFET technologies.

SiC MOSFET chips dominate the market, accounting for approximately 58% of the total market share. This segment's leadership is attributed to the widespread adoption in automotive and industrial applications, where discrete devices are preferred for their compactness and efficiency. The fastest-growing segment is SiC MOSFET modules, driven by the increasing demand in power-intensive applications such as electric vehicles and industrial automation systems. These modules offer enhanced power handling and thermal management, making them suitable for high-performance applications. Other types, including Schottky diodes and power modules, collectively contribute to the remaining market share, catering to niche applications requiring specific functionalities.

The automotive sector leads in application share, driven by the integration of SiC MOSFETs in electric vehicle powertrains, enhancing efficiency and performance. The renewable energy sector is the fastest-growing application area, with increasing adoption in solar inverters and wind turbine systems, owing to the high efficiency and thermal stability of SiC MOSFETs. Industrial applications, including motor drives and variable frequency drives, also represent a significant portion of the market, benefiting from the high switching speeds and reduced power losses offered by SiC MOSFETs. Consumer electronics and aerospace & defense sectors contribute to the market, albeit to a lesser extent, focusing on specific applications requiring compact and efficient power solutions.

The automotive industry is the leading end-user segment, with a significant share attributed to the growing adoption of electric vehicles and the need for efficient power management solutions. Industrial applications follow closely, driven by the demand for automation and energy-efficient systems. The renewable energy sector is experiencing rapid growth, with increased investments in solar and wind energy projects requiring efficient power conversion systems. Consumer electronics and aerospace & defense sectors, while smaller in comparison, are emerging as important end-users, focusing on applications that demand high efficiency and compact power solutions. OEMs play a crucial role in driving market growth by integrating SiC MOSFET technologies into their products, while aftermarket service providers contribute by offering maintenance and upgrade solutions.

North America accounted for the largest market share at 32% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 29% between 2025 and 2032.

North America’s dominance is fueled by substantial investment in electric vehicles and renewable energy projects, with over 150,000 units of EV inverters utilizing SiC MOSFET modules in 2024. Asia-Pacific’s rapid growth is supported by China and Japan, where production volumes exceeded 120,000 units and 45,000 units respectively, coupled with increasing adoption in industrial automation and consumer electronics.

How is adoption in high-efficiency automotive and industrial applications shaping market dynamics?

North America holds approximately 32% of the market, driven by key industries such as automotive, industrial automation, and renewable energy. Regulatory incentives and government support, including tax credits for EV manufacturing and energy-efficient systems, are accelerating adoption. Technological advancements like high-voltage SiC MOSFET modules and digital monitoring platforms are enhancing system efficiency. Local players such as Wolfspeed are expanding their production of SiC wafers, with 20,000 units shipped to automotive manufacturers in 2024. North American enterprises show higher adoption rates in healthcare and finance automation sectors, emphasizing precision and reliability in power electronics.

How are sustainability regulations influencing industrial and automotive uptake?

Europe accounts for roughly 28% of the market, with Germany, France, and the UK leading adoption. Regulatory bodies enforcing strict emissions and energy-efficiency standards drive demand for SiC MOSFETs in EVs and industrial machinery. Emerging technologies such as integrated SiC modules and advanced packaging solutions support higher power density applications. Local players like Infineon Technologies implemented SiC MOSFET modules in over 10,000 EV platforms in 2024, enhancing energy efficiency by 18%. Regulatory pressure in Europe encourages enterprises to prioritize explainable and energy-efficient power devices.

What factors are driving rapid adoption in manufacturing and infrastructure projects?

Asia-Pacific represents approximately 36% of the market volume, with China, India, and Japan as top consumers. The region benefits from advanced semiconductor manufacturing facilities, large-scale EV deployment, and industrial automation initiatives. Technological hubs in China and Japan are developing next-generation SiC MOSFET modules for high-power applications. Local players such as STMicroelectronics expanded wafer production to 50,000 units in 2024 to meet rising demand. Consumer behavior in Asia-Pacific favors high-efficiency solutions for e-commerce and mobile AI applications, accelerating market adoption.

How are energy and infrastructure developments shaping power electronics demand?

South America accounts for 12% of the market, with Brazil and Argentina as key contributors. Growth is supported by renewable energy projects and government incentives promoting industrial modernization. Infrastructure development in Brazil led to deployment of 3,500 high-efficiency SiC MOSFET modules in 2024. Local players focus on customized solutions for energy and industrial sectors. Consumer adoption is influenced by media, localized industrial applications, and increasing demand for energy-efficient systems.

What trends are driving adoption in oil, gas, and construction sectors?

Middle East & Africa represents roughly 10% of the market, with UAE and South Africa leading demand. Technological modernization in construction and energy sectors drives adoption of high-efficiency SiC MOSFET modules. Regional regulations and trade partnerships support deployment in oil, gas, and renewable energy applications. Local companies supplied over 2,000 SiC MOSFET modules for industrial projects in 2024. Consumer behavior in this region reflects a preference for high-reliability and low-maintenance power solutions.

United States – 32% market share | Strong end-user demand and supportive regulatory environment for EV and renewable energy adoption.

China – 25% market share | High production capacity and rapid industrial adoption of SiC MOSFETs for automotive and infrastructure applications.

The SiC MOSFET Chips (Devices) and Module market is characterized by a highly competitive environment, with over 50 active global players operating across multiple regions. The top five companies—Wolfspeed, Infineon Technologies, STMicroelectronics, ROHM Semiconductor, and ON Semiconductor—collectively hold approximately 80% of the market share, indicating a moderately consolidated structure. Strategic initiatives such as mergers, acquisitions, joint ventures, and substantial R&D investments are prevalent, aiming to enhance technological capabilities and expand market presence. Innovation trends focus on higher power efficiency, improved thermal management, and integration of SiC MOSFETs in electric vehicle powertrains, industrial automation, and renewable energy systems. Regional consumer behavior varies, with North America showing higher enterprise adoption in healthcare and finance sectors, while Europe emphasizes regulatory-compliant and energy-efficient solutions. Additionally, companies are launching advanced packaging solutions and 8-inch wafer production to meet rising global demand, ensuring a forward-looking competitive edge in high-performance power electronics.

ROHM Semiconductor

ON Semiconductor

Mitsubishi Electric

Microchip Technology

GeneSiC Semiconductor

Littelfuse

Shenzhen BASiC Semiconductor

The SiC MOSFET market is undergoing rapid technological advancements that are enhancing device performance, reliability, and applicability across industries. Advanced packaging solutions, including high-density modules, are improving thermal management and reducing parasitic inductance, resulting in more efficient power conversion. Integration with other wide-bandgap materials is enabling SiC MOSFETs to operate at higher voltages and temperatures, expanding their use in electric vehicles, industrial automation, and renewable energy systems.

Enhanced reliability testing methodologies are being implemented to meet stringent requirements for critical applications, increasing adoption in automotive powertrains and industrial motor drives. Cost-reduction initiatives through efficient fabrication processes and economies of scale are making SiC MOSFETs more accessible for broader applications. Additionally, advancements in digital monitoring, predictive maintenance, and integration with smart power systems are improving device uptime and operational efficiency. These technological trends collectively support higher energy efficiency, reduced thermal losses, and improved power density, positioning SiC MOSFETs as a cornerstone for next-generation power electronics.

In August 2024, ROHM announced the adoption of its 4th-generation SiC MOSFET bare chips in power modules for the traction inverters of three ZEEKR electric vehicle models by Zhejiang Geely Holding Group. These modules have been mass-produced since 2023 and shipped from HAIMOSIC (SHANGHAI) Co., Ltd. to Viridi E-Mobility Technology (Ningbo) Co., Ltd., a Tier 1 manufacturer under Geely. Source: www.rohm.com

In November 2024, Mitsubishi Electric began shipping samples of its SiC MOSFET bare dies for use in drive-motor inverters of electric vehicles (EVs), plug-in hybrid vehicles (PHEVs), and other electric vehicles (xEVs). This move marks a significant step in advancing power electronics for the automotive industry. Source: www.mitsubishielectric.com

In April 2025, Navitas Semiconductor introduced its latest SiCPAK™ power modules, featuring advanced low-cost epoxy-resin potting technology. These modules are designed for high-temperature environments, offering enhanced reliability and efficient performance, setting a new standard in the industry. Source: www.navitassemi.com

In September 2025, Mitsubishi Electric unveiled its next-generation SiC MOSFET and Si RC-IGBT technologies, featuring compact high-reliability transfer mold packaging (T-PM) with Direct-Lead-Bonding (DLB) technology. These innovations aim to meet the growing demand for high power-density, scalable, and cost-effective solutions in e-mobility applications. Source: www.mitsubishielectric.com

The SiC MOSFET Chips (Devices) and Module Market Report provides a comprehensive overview of the global market, analyzing segments by product type, application, and end-user industries. Key geographic regions covered include North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional consumption patterns, adoption trends, and technological capabilities.

The report examines the use of SiC MOSFETs in electric vehicles, renewable energy systems, industrial automation, and power supplies, emphasizing innovations such as high-density modules, wide-bandgap integration, and enhanced thermal management. It also explores emerging niche segments, including aerospace, consumer electronics, and AI-powered industrial applications.

Competitive dynamics are addressed, profiling leading market players and their strategies, including product development, partnerships, and regional expansions. The report further evaluates technological trends, regulatory influences, and sustainability initiatives that shape market opportunities. It provides actionable insights for stakeholders seeking to understand market potential, identify investment opportunities, and align business strategies with evolving industry requirements.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 668.69 Million |

|

Market Revenue in 2032 |

USD 4582.7 Million |

|

CAGR (2025 - 2032) |

27.2% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Wolfspeed, Infineon Technologies, STMicroelectronics, ROHM Semiconductor, ON Semiconductor, Mitsubishi Electric, Microchip Technology, GeneSiC Semiconductor, Littelfuse, Shenzhen BASiC Semiconductor |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |