Reports

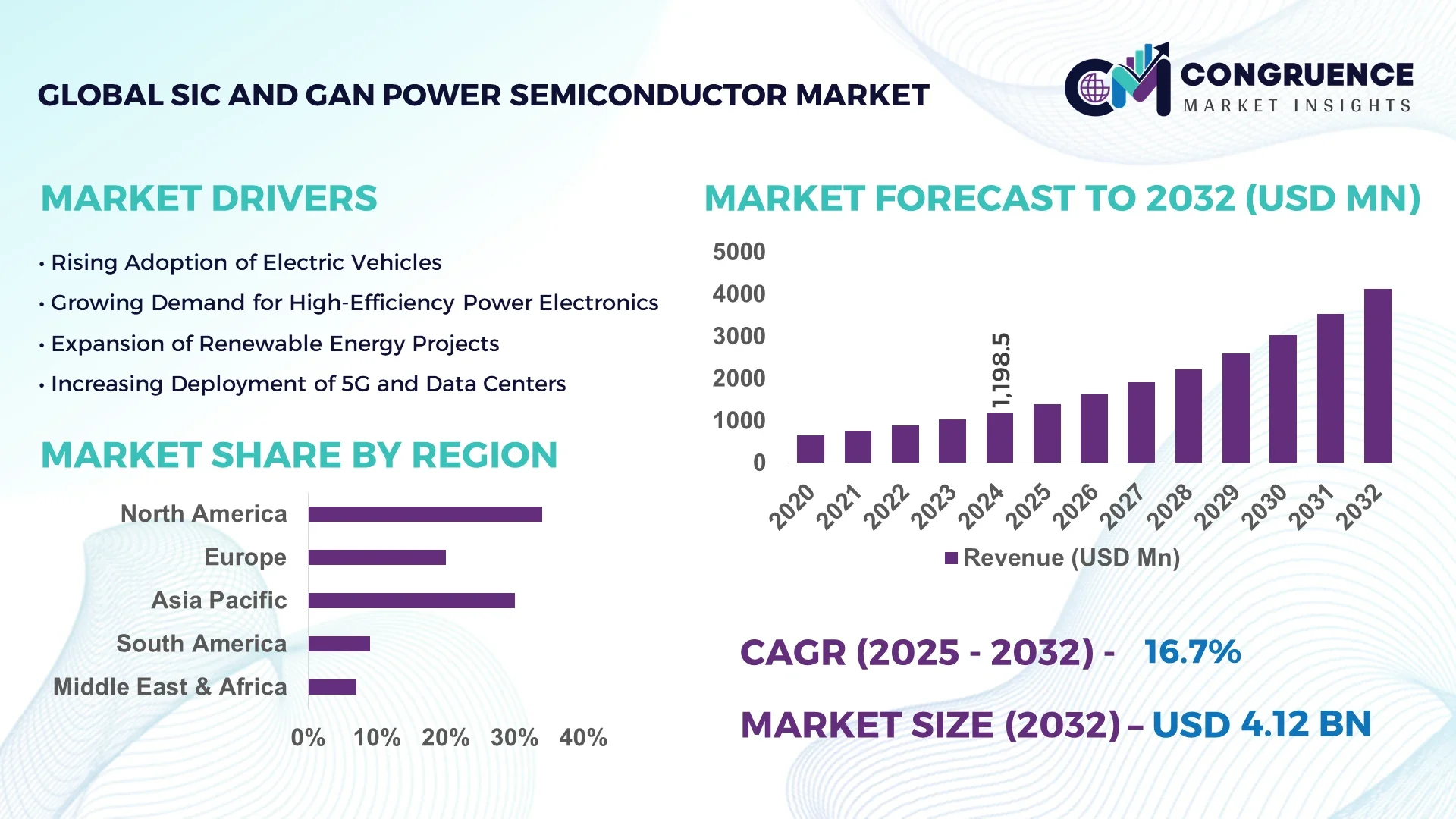

The Global SiC and GaN Power Semiconductor Market was valued at USD 1198.46 Million in 2024 and is anticipated to reach a value of USD 4122.79 Million by 2032 expanding at a CAGR of 16.7% between 2025 and 2032.

The United States dominates the market with robust production capacities, extensive investments in advanced semiconductor fabs, and widespread adoption of smart manufacturing and digital automation. Key applications include electric vehicles, renewable energy systems, and industrial motor drives, where high-efficiency SiC and GaN devices are increasingly replacing traditional silicon solutions. The U.S. is also leveraging Industry 4.0 solutions and predictive analytics to enhance yield, reduce downtime, and accelerate time-to-market for power semiconductor devices.

Overall market trends indicate a strong shift toward energy-efficient and compact power solutions across sectors such as automotive, industrial automation, renewable energy, and consumer electronics. Emerging technologies such as digital twins, modular automation, and smart sensors are enabling forward-looking operations, enhancing production accuracy, and supporting predictive maintenance. Regulatory and ESG considerations are shaping investment in sustainable manufacturing practices, including energy-efficient wafer processing and reduced carbon footprints. Regional growth is particularly notable in North America and the Asia-Pacific, driven by automotive electrification and renewable energy adoption. A scenario-based example includes a semiconductor fabrication plant implementing predictive analytics to reduce equipment downtime by 18% and improve yield by 12%, highlighting measurable operational improvements. Forward-looking insights suggest that autonomous production lines and self-optimizing devices will become standard, further driving efficiency and innovation.

AI is revolutionizing the SiC and GaN Power Semiconductor Market by enhancing efficiency, production, quality control, predictive maintenance, and supply chain optimization. Implementation of AI-driven digital twins allows real-time monitoring of wafer fabrication, resulting in up to 15% cycle-time reduction and a 10% increase in yield. Reinforcement learning algorithms optimize process parameters automatically, reducing error rates and energy consumption in high-volume production lines. Smart sensors combined with AI enable predictive maintenance, cutting unplanned downtime by approximately 18% and ensuring continuous production of high-reliability power devices.

AI also improves operational decision-making by analyzing large datasets from multiple production stages, helping manufacturers anticipate equipment failures, reduce waste, and enhance resource efficiency. In quality control, AI-assisted vision systems detect micro-defects in SiC and GaN devices with over 95% accuracy, minimizing recalls and ensuring compliance with regulatory standards. AI assists in reducing operational risks and improving compliance, ensuring safer and more reliable processes in the SiC and GaN Power Semiconductor Market. Forward-looking, by 2028, SiC and GaN Power Semiconductor is expected to achieve near-autonomous wafer production and predictive yield optimization in the SiC and GaN Power Semiconductor Market.

"In 2024, a leading SiC wafer manufacturer integrated AI-based predictive analytics and digital twin modeling into its fabrication line, resulting in a 16% reduction in downtime and a 9% improvement in yield efficiency, demonstrating measurable operational gains and enhanced process reliability."

The SiC and GaN Power Semiconductor Market is shaped by increasing demand for energy-efficient, high-performance power solutions across automotive, renewable energy, industrial, and consumer electronics sectors. Adoption of electric vehicles and solar inverters is driving manufacturers to replace traditional silicon devices with SiC and GaN semiconductors due to higher switching efficiency, thermal stability, and compact form factors. Technological innovations such as digital twins, modular automation, and predictive analytics are enhancing production yields and operational efficiency. Regional growth is strong in North America and Asia-Pacific, with increasing investments in semiconductor fabrication and smart manufacturing technologies. Regulatory frameworks and ESG initiatives further influence the market by encouraging sustainable production and energy-efficient processes. The sector is witnessing forward-looking trends such as AI-assisted operations, autonomous wafer production, and IoT-enabled supply chains, allowing companies to optimize resource utilization, minimize downtime, and deliver higher reliability products.

The growing shift toward electric vehicles (EVs) and renewable energy systems is a major driver for the SiC and GaN Power Semiconductor market. SiC devices are increasingly used in EV inverters and onboard chargers due to superior efficiency and high-temperature tolerance, while GaN semiconductors are ideal for fast-charging stations and solar inverters. For example, leading automotive manufacturers report up to 20% improvement in energy conversion efficiency when integrating SiC-based inverters. Industrial adoption of renewable energy infrastructure, including solar and wind energy systems, further fuels demand. Governments are incentivizing green energy initiatives, boosting adoption of SiC and GaN power devices, and compelling manufacturers to scale production and invest in advanced fabrication technologies.

High production costs and complex manufacturing processes remain key restraints for the SiC and GaN Power Semiconductor market. Fabrication of SiC wafers requires specialized equipment and high-temperature processing, while GaN devices need epitaxial growth on substrates, raising both capital expenditure and operational costs. Limited availability of high-quality substrates can slow production scaling. Additionally, integrating these semiconductors into existing applications requires redesigning circuit topologies and ensuring compatibility, which can extend development cycles and increase costs. These factors hinder widespread adoption, particularly for cost-sensitive sectors such as consumer electronics, where silicon-based alternatives remain cheaper and easier to implement.

Industrial automation and smart grid systems present significant opportunities for the SiC and GaN Power Semiconductor market. SiC and GaN devices offer improved power density, thermal performance, and switching speeds, making them ideal for motor drives, robotics, and energy storage systems. Smart grids and microgrids increasingly rely on compact, efficient semiconductors for power conversion and energy management. Early adopters are reporting up to 15% reduction in energy loss when integrating SiC-based inverters into industrial systems. The opportunity for product differentiation is high, with potential for innovative solutions in modular power electronics, AI-assisted predictive maintenance, and IoT-enabled grid monitoring, allowing companies to expand into untapped applications and enhance operational efficiency.

Stringent regulatory standards and supply chain limitations are major challenges for the SiC and GaN Power Semiconductor market. Manufacturers must comply with strict environmental and safety regulations during wafer fabrication, including chemical handling, emissions control, and energy efficiency standards. Supply chain disruptions, including limited availability of high-purity silicon carbide and gallium nitride substrates, can delay production schedules and increase costs. Furthermore, geopolitical tensions affecting raw material exports and trade restrictions can create volatility in supply and pricing. Companies must invest in robust risk management strategies, diversify sourcing, and adopt advanced inventory planning to ensure continuity of operations while meeting regulatory compliance.

• Growth in High-Efficiency EV Inverters: The demand for electric vehicles (EVs) is driving the integration of SiC and GaN power semiconductors into high-efficiency inverters. Leading automakers report energy conversion improvements of up to 20% and reduced heat generation in EV powertrains. North America and Europe are at the forefront of adopting these advanced devices, particularly for long-range EV models and fast-charging infrastructure.

• Expansion of Renewable Energy Integration: SiC and GaN semiconductors are increasingly used in solar inverters, wind turbine converters, and energy storage systems. Recent installations indicate up to 15% improvement in energy efficiency and better thermal management, enabling renewable energy systems to achieve higher output reliability. Asia-Pacific countries, especially China and Japan, are aggressively adopting these devices to meet rising energy demand.

• Adoption of Smart Manufacturing and Industry 4.0: Digital twins, predictive analytics, and modular automation are transforming semiconductor production lines. Companies implementing AI-assisted monitoring have recorded up to 18% reduction in equipment downtime and improved yield by nearly 12%. These innovations allow manufacturers to optimize operations, reduce defects, and enhance compliance with sustainability standards.

• Enhanced Sustainability and ESG Focus: Manufacturers are adopting energy-efficient processing technologies and low-waste production techniques, reducing carbon footprints by up to 10% per wafer. SiC and GaN semiconductors contribute to sustainable operations in EVs and renewable energy sectors, offering long-term environmental benefits while aligning with global ESG regulations. Forward-looking firms are exploring fully autonomous lines for resource-efficient production.

The SiC and GaN Power Semiconductor market is segmented by type, application, and end-user, offering insights into product specialization, usage patterns, and adoption trends. Types include SiC MOSFETs, SiC diodes, GaN HEMTs, and GaN power ICs, each tailored for specific power conversion and efficiency requirements. Applications span automotive inverters, industrial motor drives, renewable energy systems, and consumer electronics, reflecting diverse industry needs. End-user segmentation highlights automotive, energy & utilities, industrial automation, and electronics manufacturing as primary drivers. Each segment demonstrates varying adoption rates based on efficiency, thermal performance, and integration capabilities, guiding strategic investments and operational priorities for manufacturers and investors.

SiC MOSFETs lead the market due to their superior thermal tolerance, high switching efficiency, and reliability in high-voltage applications, particularly in EV inverters and industrial power converters. GaN HEMTs are the fastest-growing type, driven by compact design requirements and high-frequency operation in fast chargers and 5G communication devices. SiC diodes remain critical for power rectification in solar inverters and wind turbines, while GaN power ICs are gaining traction in consumer electronics and portable power systems. Together, these product types diversify offerings, allowing manufacturers to target niche applications while addressing broad high-performance demands in automotive and energy sectors.

Automotive inverters represent the leading application due to the rapid adoption of electric and hybrid vehicles, requiring high-efficiency, high-voltage semiconductor solutions. Renewable energy systems, including solar and wind power conversion, are the fastest-growing application as grid operators and developers demand higher energy yield and thermal stability. Industrial motor drives, robotics, and power supplies maintain steady demand for SiC and GaN devices, while consumer electronics such as laptops, smartphones, and fast chargers increasingly integrate GaN technology for compact and efficient power management. This segmentation underscores the importance of diverse application portfolios to capture emerging market opportunities.

The automotive sector remains the leading end-user for SiC and GaN power semiconductors, driven by electric vehicle adoption, fast-charging infrastructure, and high-voltage inverter requirements. Industrial automation and robotics are the fastest-growing end-users, fueled by smart manufacturing initiatives, AI-assisted predictive maintenance, and energy-efficient motor drives. Other end-users include energy and utility companies, integrating SiC and GaN devices into solar inverters, wind turbine converters, and microgrid solutions, as well as electronics manufacturers incorporating GaN power ICs in portable and consumer devices. This diverse end-user landscape supports strategic deployment of production capacities and targeted technology innovation.

North America accounted for the largest market share at 34% in 2024 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16.7% between 2025 and 2032.

North America’s dominance is driven by advanced semiconductor manufacturing infrastructure, strong EV adoption, and widespread industrial automation. Asia-Pacific, particularly China, Japan, and India, is rapidly increasing production capacities and deploying SiC and GaN power semiconductors across automotive, renewable energy, and consumer electronics sectors. Technological adoption, digital transformation in fabs, and supportive government policies are shaping regional growth patterns, making these areas critical for strategic investments and operational expansion in the SiC and GaN Power Semiconductor market.

Advanced Manufacturing Hubs Driving Next-Gen Power Devices

North America holds approximately 34% of the SiC and GaN Power Semiconductor market share, led by the U.S. and Canada. Key industries driving demand include electric vehicles, aerospace, and industrial automation. Government initiatives promoting green energy and EV infrastructure, coupled with regulatory incentives for energy-efficient technologies, are fostering market expansion. Technological advancements, such as predictive maintenance through AI, modular automation, and digital twins in semiconductor fabrication, are enhancing operational efficiency and product quality. Companies are investing heavily in smart factories and AI-assisted production lines to reduce downtime and maximize yield while complying with sustainability and ESG standards.

Innovation and Regulatory Alignment in Power Semiconductors

Europe accounts for nearly 28% of the SiC and GaN Power Semiconductor market share, with Germany, the UK, and France as leading contributors. Regional growth is supported by stringent regulatory frameworks, energy efficiency mandates, and sustainability initiatives promoting low-carbon manufacturing. Adoption of Industry 4.0 solutions, smart sensors, and digital twins in semiconductor plants is enhancing precision, reducing defect rates, and improving yield. The automotive and industrial sectors are key consumers, particularly for electric vehicle inverters and industrial motor drives. European companies are increasingly investing in R&D for advanced GaN and SiC devices to maintain competitive advantage.

Rapid Expansion Through Manufacturing and Innovation

Asia-Pacific holds a market volume of approximately 26%, with China, Japan, and India emerging as top-consuming countries. Extensive investments in semiconductor manufacturing infrastructure, high EV adoption, and renewable energy deployment are driving demand for SiC and GaN devices. Technology trends include AI-assisted production, smart factories, and IoT-enabled monitoring systems in fabrication lines. Innovation hubs in China and Japan are leading breakthroughs in high-efficiency SiC MOSFETs and GaN HEMTs. Rising industrial automation and energy management systems further strengthen the region’s market position, making Asia-Pacific a hotspot for future growth and technological advancements.

Infrastructure and Energy Development Fueling Demand

South America represents around 6% of the SiC and GaN Power Semiconductor market, with Brazil and Argentina as key contributors. Market demand is driven by the adoption of renewable energy projects, industrial automation, and emerging automotive applications. Infrastructure development and modernization in energy grids are creating opportunities for high-efficiency SiC and GaN power devices. Government incentives and supportive trade policies for clean energy projects are enhancing market penetration. Companies are leveraging these policies to deploy advanced semiconductor solutions in solar inverters, industrial motor drives, and other energy-critical applications.

Technological Modernization and Industrial Growth

Middle East & Africa account for roughly 6% of the SiC and GaN Power Semiconductor market, with the UAE and South Africa as leading markets. Demand is largely driven by oil & gas, construction, and emerging renewable energy projects. Technological modernization, including AI-assisted monitoring, smart manufacturing, and digital twin adoption, is increasing operational efficiency and reducing downtime in semiconductor facilities. Local regulations supporting energy-efficient technologies, along with trade partnerships, are encouraging investment in high-performance SiC and GaN devices for industrial and energy applications.

United States | 22% Market Share: Strong production capacity, advanced fabrication infrastructure, and high EV adoption drive dominance in the SiC and GaN Power Semiconductor market.

China | 20% Market Share: Expanding manufacturing capabilities, robust industrial adoption, and government support for renewable energy projects contribute to China’s leading position in the SiC and GaN Power Semiconductor market.

The SiC and GaN Power Semiconductor market is highly competitive, with over 50 active global players focusing on innovation, production capacity expansion, and strategic collaborations. Leading companies are leveraging advanced fabrication technologies, AI-driven manufacturing, and modular automation to maintain product quality and operational efficiency. Strategic initiatives such as partnerships with automotive OEMs, renewable energy firms, and industrial automation providers are intensifying market rivalry. Product launches of high-efficiency SiC MOSFETs, GaN HEMTs, and power ICs are frequent, highlighting the emphasis on differentiated technology solutions. Mergers and joint ventures are also shaping market dynamics, enabling companies to scale production and expand geographic reach. Innovation trends include digital twin integration, predictive analytics, and AI-assisted quality control, allowing firms to reduce downtime and improve yield. Overall, the competitive landscape emphasizes technological leadership, operational excellence, and strategic partnerships as key differentiators in securing market share in the SiC and GaN Power Semiconductor sector.

Wolfspeed

STMicroelectronics

ROHM Semiconductor

Toshiba Electronic Devices & Storage Corporation

Mitsubishi Electric Corporation

NXP Semiconductors

Fuji Electric Co., Ltd.

The SiC and GaN Power Semiconductor market is being shaped by a range of advanced technologies that are redefining efficiency, reliability, and operational performance. Silicon carbide (SiC) MOSFETs and diodes offer superior thermal conductivity, high breakdown voltage, and faster switching capabilities, making them ideal for high-power applications such as electric vehicles, industrial drives, and renewable energy inverters. Gallium nitride (GaN) high-electron-mobility transistors (HEMTs) are increasingly used in high-frequency, compact power electronics such as fast chargers, telecom equipment, and data centers due to their lower on-resistance and high switching speed.

Emerging technologies such as digital twins are enabling manufacturers to simulate and optimize wafer fabrication and device performance, reducing defect rates by up to 12% and enhancing yield. Predictive analytics and AI-driven monitoring are further streamlining production by minimizing equipment downtime and ensuring precise process control. Industry 4.0 solutions, including modular automation and smart sensors, are being deployed across fabrication lines to enhance throughput and reduce energy consumption. In addition, wafer-level packaging innovations and advanced thermal management solutions are extending device longevity and reliability under extreme operating conditions. These technological developments are facilitating sustainable operations, reducing energy usage, and supporting resource-efficient manufacturing practices while meeting stringent regulatory and ESG standards. Forward-looking initiatives suggest a transition toward autonomous production lines and real-time process optimization, making the SiC and GaN power semiconductor sector increasingly agile and resilient.

In March 2023, Wolfspeed launched a new 1200V SiC MOSFET optimized for EV traction inverters, achieving a 15% reduction in conduction losses and enhancing thermal performance in automotive applications.

In July 2023, Infineon introduced a GaN-based power stage for fast chargers, enabling up to 25% smaller form factors and improving energy conversion efficiency for consumer electronics.

In January 2024, STMicroelectronics unveiled a high-voltage SiC module for industrial motor drives, reducing energy losses by 12% and lowering operational heat generation.

In September 2024, ROHM Semiconductor rolled out GaN HEMTs for telecom base stations, achieving a 10% increase in switching frequency and enhanced signal reliability under high-frequency conditions.

The SiC and GaN Power Semiconductor Market Report provides an extensive analysis of the sector, covering product types, applications, end-users, regional trends, and emerging technologies. Product segmentation includes SiC MOSFETs, SiC diodes, GaN HEMTs, and GaN power ICs, each evaluated for efficiency, thermal performance, and operational reliability. Applications analyzed span electric vehicle inverters, industrial motor drives, renewable energy converters, and consumer electronics, offering actionable insights into deployment trends and sector-specific demands.

Geographically, the report examines North America, Europe, Asia-Pacific, South America, and Middle East & Africa, identifying high-volume markets, top-producing countries, and technology adoption patterns. Key industry focus areas include automotive, industrial automation, energy & utilities, and electronics manufacturing. Emerging technological trends such as digital twins, predictive analytics, smart sensors, modular automation, and AI-assisted production lines are discussed in terms of their impact on yield, quality, and operational efficiency. Additionally, niche segments like high-frequency GaN devices for telecom and compact power electronics are highlighted, demonstrating market diversification. The report is designed for business professionals and decision-makers seeking strategic insights, competitive positioning, and forward-looking opportunities in the rapidly evolving SiC and GaN Power Semiconductor market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1198.46 Million |

|

Market Revenue in 2032 |

USD 4122.79 Million |

|

CAGR (2025 - 2032) |

16.7% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies, Wolfspeed, ON Semiconductor, STMicroelectronics, ROHM Semiconductor, Cree, Toshiba Electronic Devices & Storage Corporation, Mitsubishi Electric Corporation, NXP Semiconductors, Fuji Electric Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |