Reports

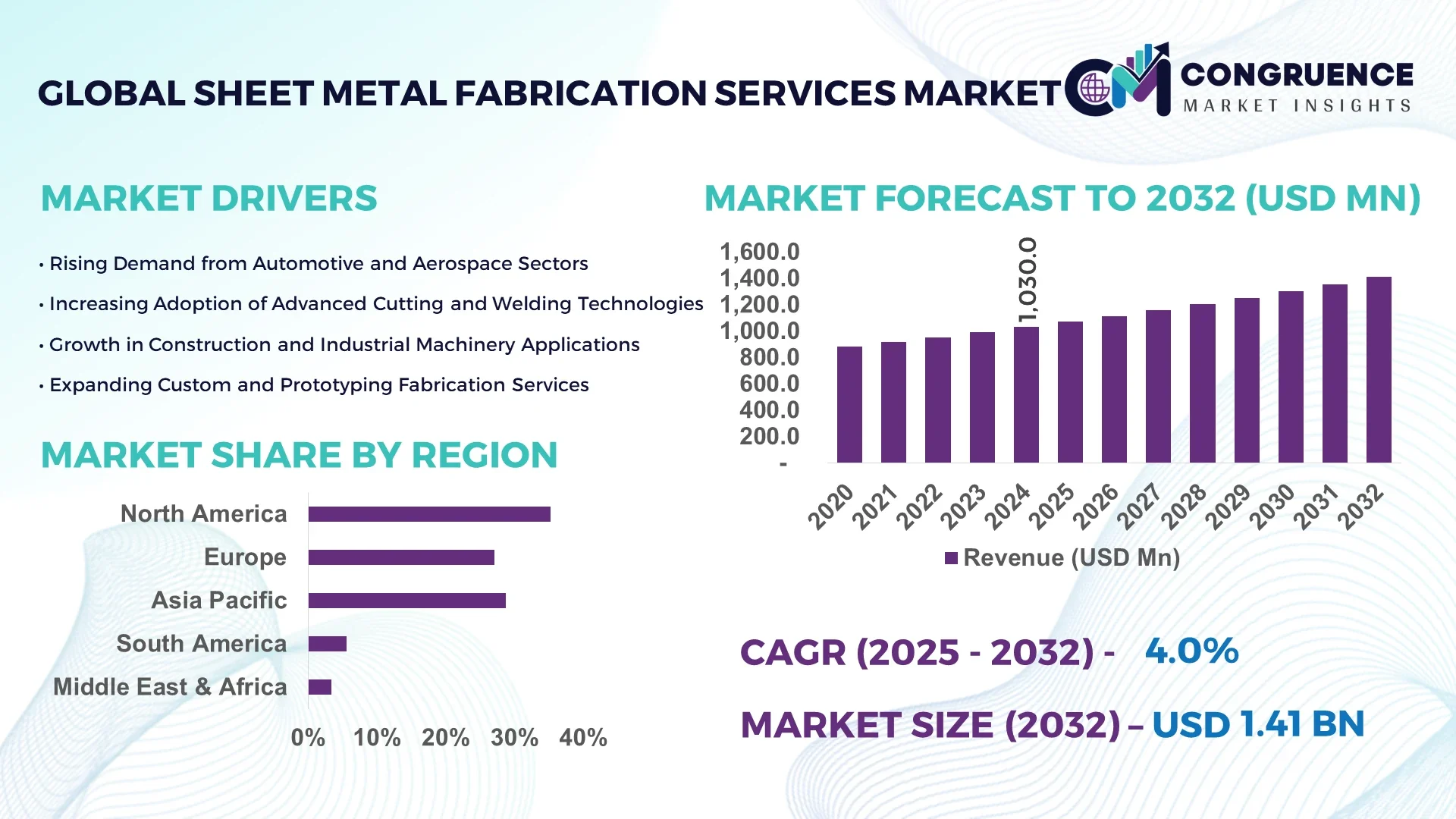

The Global Sheet Metal Fabrication Services Market was valued at USD 1,030.0 Million in 2024 and is anticipated to reach a value of USD 1,409.6 Million by 2032 expanding at a CAGR of 4.0% between 2025 and 2032.

The United States plays a pivotal role in the Sheet Metal Fabrication Services Market, supported by its extensive production capacity, advanced CNC machining facilities, and continuous investments in automation and robotics. The country’s aerospace, defense, and automotive sectors are major consumers, while Industry 4.0 integration drives innovation in precision manufacturing.

The Sheet Metal Fabrication Services Market spans multiple high-growth sectors such as automotive, aerospace, defense, construction, electronics, and energy. The automotive industry remains a dominant end-user, particularly for precision components and lightweight structures. Recent innovations in fiber laser cutting, robotic welding, and automated bending systems are improving speed, accuracy, and repeatability. Additionally, environmentally conscious regulations and green manufacturing practices are shaping production standards, especially across Europe and Asia-Pacific. Economically, shifting trade policies and nearshoring trends are altering global supply chain dynamics. Regional consumption patterns reveal growing demand in Asia-Pacific due to rapid industrialization, while North America and Europe benefit from the adoption of smart manufacturing technologies. Emerging trends such as additive manufacturing integration, hybrid fabrication models, and AI-driven quality control systems signal a future where customization, speed, and sustainability become competitive differentiators in this evolving market landscape.

Artificial Intelligence (AI) is revolutionizing the Sheet Metal Fabrication Services Market by enabling advanced automation, real-time process optimization, and predictive maintenance. AI-driven tools are increasingly integrated with CNC machinery, allowing manufacturers to reduce setup time and eliminate material waste through intelligent nesting algorithms. Machine learning applications are enhancing defect detection in real time, which minimizes rework and improves throughput. In high-volume production environments, AI-driven scheduling systems dynamically allocate resources and adjust workflows based on machine performance and material availability, improving overall operational efficiency by up to 25%.

In the Sheet Metal Fabrication Services Market, AI is also enabling more precise demand forecasting and inventory control, reducing downtime and improving just-in-time production models. The adoption of digital twins and AI-assisted simulation tools supports design validation and helps identify stress points in fabricated components before production begins. As fabrication requirements grow increasingly complex across sectors like aerospace and defense, AI ensures consistent quality and enhances traceability through data integration across the manufacturing lifecycle. These technologies not only increase accuracy and efficiency but also offer strategic advantages in lead time reduction and cost savings.

“In April 2025, a U.S.-based aerospace fabricator deployed an AI-integrated laser cutting system that improved sheet utilization by 18% and reduced material scrap rates by 22%, significantly lowering operational waste and production costs.”

The Sheet Metal Fabrication Services Market is undergoing significant transformation driven by evolving industrial demands, material advancements, and automation technologies. Sectors such as construction, automotive, and electronics are pushing for lightweight, high-strength components manufactured at scale and with minimal lead times. The expansion of smart factories and increased investment in automated fabrication lines are propelling demand for precision cutting, forming, and welding technologies. Moreover, evolving environmental regulations and consumer expectations are accelerating the shift towards more sustainable manufacturing methods, influencing market participants to adopt energy-efficient and low-waste fabrication processes. Regional growth disparities and changes in global trade dynamics also influence sourcing and production strategies, adding complexity to the competitive landscape.

The integration of advanced Computer Numerical Control (CNC) systems and fiber laser cutting technologies is a key driver accelerating growth in the Sheet Metal Fabrication Services Market. These systems offer higher precision, faster processing speeds, and reduced operational costs compared to traditional methods. Fiber laser machines, for instance, provide cutting speeds up to five times faster than CO₂ lasers for thin metals, significantly enhancing throughput. Automated CNC systems reduce human intervention and improve repeatability, essential in sectors such as automotive and electronics. With manufacturers demanding greater accuracy and efficiency, the use of programmable tools, multi-axis control, and real-time diagnostics has become standard practice in leading fabrication facilities worldwide. As capital investments in high-end equipment increase, particularly in Asia-Pacific and North America, the market is expected to witness a sharp improvement in productivity and innovation.

A major restraint in the Sheet Metal Fabrication Services Market is the growing shortage of skilled labor capable of operating advanced fabrication machinery. As the industry shifts toward digital and automated systems, the demand for technicians proficient in CNC programming, CAD/CAM software, and AI-integrated tools has surged. However, the supply of such talent remains limited. This gap impacts production capacity, quality control, and innovation timelines. Training cycles for new employees are often long and costly, and older workers with traditional fabrication expertise may lack the skills needed for smart factory environments. In regions like North America and parts of Europe, this shortage has led to project delays and increased dependency on contract labor. Companies are being forced to invest heavily in upskilling programs and partnerships with technical institutes, which, while beneficial in the long term, place immediate pressure on margins and timelines.

Emerging opportunities in the Sheet Metal Fabrication Services Market are largely tied to the expansion of aerospace and electric vehicle (EV) industries. These sectors require lightweight, durable, and precisely manufactured components. Aerospace, in particular, demands tight tolerances and high-performance alloys, encouraging fabricators to adopt advanced techniques like 5-axis machining and robotic welding. Similarly, EV manufacturers increasingly rely on complex enclosures and battery housing fabricated using aluminum and stainless steel. The push for higher energy efficiency and safety in EVs is stimulating innovation in heat shielding and structural reinforcements. Several companies are investing in dedicated fabrication lines for EV components, and global orders for aerospace parts are climbing, driven by increased aircraft production. These trends provide lucrative avenues for specialized service providers and those equipped with next-generation technologies.

The Sheet Metal Fabrication Services Market faces ongoing challenges from global supply chain instability and fluctuating raw material costs. Prices for key inputs like aluminum and stainless steel have seen sharp spikes due to geopolitical tensions, energy crises, and logistical bottlenecks. Fabricators often operate on tight margins and fixed delivery contracts, making it difficult to absorb unexpected price hikes. Additionally, sourcing delays for specialized alloys or imported machine parts can disrupt production schedules and delay client orders. Small and mid-sized enterprises are especially vulnerable, as they lack the procurement leverage or inventory capacity of larger players. These disruptions not only affect operational efficiency but also hinder strategic planning, forcing companies to adopt more conservative investment and production strategies.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Sheet Metal Fabrication Services Market. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Adoption of Digital Twin Technology: Fabricators are increasingly using digital twin models to simulate the behavior and integrity of sheet metal parts before production begins. This trend is gaining traction in aerospace and automotive sectors, improving design accuracy and reducing prototype costs. Implementation of digital twins has lowered design validation time by nearly 30% in some manufacturing setups.

Growing Use of Lightweight Alloys in EVs: With rising electric vehicle production, demand for lightweight alloys such as aluminum-magnesium blends is surging. These materials are essential for reducing vehicle weight and improving energy efficiency. Sheet metal fabricators are adapting by upgrading cutting tools and forming processes to handle new alloy compositions at scale.

Expansion of Smart Factory Initiatives: Smart factories leveraging IoT, AI, and automated tracking systems are expanding rapidly within the Sheet Metal Fabrication Services Market. Real-time monitoring of machinery, materials, and finished parts enhances productivity and reduces waste. In 2024, over 40% of medium-to-large fabrication plants in Asia implemented smart production systems, improving operational efficiency and safety compliance.

The Global Sheet Metal Fabrication Services Market is segmented based on type, application, and end-user, each reflecting distinct demand patterns and technological advancements. Segmentation by type includes services such as cutting, bending, and welding, where automation and CNC capabilities are playing a central role in modernizing production processes. Application-wise, the market caters to a range of industries including automotive, aerospace, construction, and electronics, each with specific structural and functional requirements for metal components. The end-user segmentation further highlights the dominant role of the manufacturing sector, while also underscoring the rising importance of the energy and consumer electronics sectors. These segmentation insights help clarify how industry-specific trends such as lightweighting in automotive or modular designs in construction are reshaping fabrication service requirements. Moreover, evolving materials and design complexities are driving specialization within segments, encouraging service providers to diversify capabilities and adopt advanced digital tools for customization and quality assurance.

The market for sheet metal fabrication services by type encompasses cutting, bending, welding, shearing, stamping, and others, each serving specific manufacturing functions. Among these, cutting services lead the segment due to their essential role in shaping and preparing metal sheets for subsequent processes. With the adoption of laser and plasma cutting technologies, manufacturers achieve faster throughput and higher precision, which is particularly critical in automotive and aerospace production lines. Bending services are the fastest-growing due to their increased utilization in complex assemblies across construction and industrial machinery, where precise angle formation and structural integrity are vital. The growth in custom fabrication and demand for lightweight components further fuels this segment. Welding services hold a significant share, especially in heavy industries and infrastructure, offering structural durability. Stamping and shearing, though more niche, are widely used in high-volume production environments such as appliance and electronics manufacturing, where efficiency and repeatability are prioritized.

The sheet metal fabrication services market spans multiple application areas, each characterized by unique fabrication requirements. The automotive sector represents the largest application segment, driven by high-volume production of lightweight body panels, brackets, and frames. Increased electric vehicle (EV) adoption and regulatory pressure for fuel efficiency further elevate the need for precision-fabricated parts. The aerospace sector is emerging as the fastest-growing application, owing to the increasing demand for lightweight, high-strength components made from aluminum and titanium alloys. The aerospace industry’s focus on structural accuracy, compliance, and material performance under extreme conditions necessitates advanced fabrication capabilities, such as 5-axis CNC machining and robotic welding. Construction remains a vital segment, particularly in the production of structural frameworks, cladding, and HVAC ducting, where prefabrication and modularity are increasingly common. Electronics and energy applications contribute through the demand for enclosures, mounting systems, and structural supports, often requiring precision and corrosion-resistant finishes.

End-user segmentation in the Sheet Metal Fabrication Services Market reveals a strong dominance by the manufacturing sector, which utilizes a wide range of fabricated components across machinery, tools, and industrial systems. The demand for customizable, durable, and mass-produced sheet metal parts makes manufacturing the cornerstone of the industry. The aerospace and defense sector stands out as the fastest-growing end-user segment, driven by escalating global investments in aircraft production, military modernization, and space technology. These applications necessitate stringent fabrication tolerances and material certifications, pushing providers to enhance technological capabilities. The automotive industry continues to play a pivotal role, particularly with the rise of electric vehicles, where battery enclosures, chassis components, and safety systems are fabricated at high precision. Construction and energy sectors also contribute significantly, requiring robust, weather-resistant parts for infrastructure and renewable installations. Together, these end-user dynamics underline the market’s diverse demand base and the critical role of advanced fabrication services across sectors.

North America accounted for the largest market share at 35.2% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2025 and 2032.

This regional performance is driven by varied macroeconomic, industrial, and infrastructural developments across geographies. North America's established manufacturing base and early adoption of automation technologies support its dominant position. Meanwhile, Asia-Pacific benefits from rapid urbanization, growing industrial output, and expanding investments in construction and automotive sectors, particularly in China and India. Europe remains a strong contributor with its advanced automotive and aerospace manufacturing capabilities, supported by stringent quality standards and sustainability mandates. South America and the Middle East & Africa present emerging opportunities, backed by infrastructure modernization and increasing demand for industrial fabrication solutions. Regional competitiveness is shaped by local labor costs, access to raw materials, and government support for domestic manufacturing.

North America held the largest share in the global sheet metal fabrication services market in 2024, accounting for 35.2% of the total market. The United States and Canada are at the forefront, driven by robust demand from the automotive, aerospace, and defense sectors. The U.S. government’s investments in domestic infrastructure and manufacturing revival initiatives have amplified fabrication needs. Key regulations such as the Inflation Reduction Act and Buy American Act further strengthen the preference for locally fabricated components. Additionally, the integration of automation technologies such as robotic welding, 3D laser cutting, and smart CNC systems enhances operational efficiency across fabrication facilities. Digital transformation trends, including cloud-based design software and predictive maintenance tools, are also increasingly adopted. The growing emphasis on lean manufacturing and sustainability practices drives innovation across fabrication workshops, positioning North America as a technologically advanced and demand-heavy region.

Europe accounted for 27.1% of the global sheet metal fabrication services market share in 2024, with leading contributions from Germany, the United Kingdom, and France. Germany’s stronghold in automotive manufacturing, coupled with the UK’s aerospace production and France’s industrial machinery output, sustains regional demand. European Union regulations focusing on energy efficiency, carbon neutrality, and circular manufacturing are prompting fabrication firms to adopt greener and more precise production methods. Programs under the EU Green Deal and directives from organizations such as REACH and RoHS are influencing material usage and waste reduction in fabrication processes. Furthermore, Europe is witnessing rapid adoption of emerging technologies like additive manufacturing, IoT-integrated CNC systems, and automated assembly lines. These developments support not only higher productivity but also compliance with stringent quality and environmental standards, reinforcing Europe's position as a technologically progressive market for sheet metal fabrication.

Asia-Pacific is poised as the fastest-growing region in the global sheet metal fabrication services market, expected to surpass 28.7% market share by the end of the forecast period. China, India, and Japan are the top-consuming countries, collectively contributing to a substantial portion of global fabrication output. This growth is driven by rapid urbanization, large-scale infrastructure projects, and expanding automotive and electronics manufacturing. China leads in production capacity with large-scale industrial zones and government-led initiatives supporting domestic manufacturing. India’s “Make in India” campaign and Japan’s technological edge in precision manufacturing are further boosting the regional landscape. The rise of smart factories, adoption of advanced robotics, and increasing investment in industrial automation across Asia-Pacific are significantly enhancing fabrication speed and consistency. Additionally, favorable labor costs and expanding exports make this region highly competitive, attracting multinational OEMs and tier-1 suppliers seeking cost-effective fabrication solutions.

South America is emerging as a strategic market for sheet metal fabrication services, with Brazil and Argentina leading regional demand. The region captured 5.6% of the global market in 2024. Infrastructure development programs, particularly in transportation and energy, are driving the demand for fabricated steel structures, brackets, and panels. Brazil’s ongoing expansion of renewable energy infrastructure and Argentina’s industrial modernization are increasing the need for metal components with high strength and durability. Trade policies supporting local manufacturing and reduced reliance on imports are encouraging regional production capabilities. Government-backed incentives, including tax breaks and equipment financing for small and medium enterprises, are fueling technological upgrades within fabrication workshops. Although the region still faces challenges such as fluctuating raw material prices and economic volatility, strategic investments in infrastructure and the gradual shift toward localized manufacturing are likely to create long-term growth opportunities.

The Middle East & Africa (MEA) region represented 3.4% of the global sheet metal fabrication services market in 2024, with notable growth observed in UAE and South Africa. Strong demand stems from ongoing construction booms in the Gulf countries and increased energy infrastructure projects across the region. The UAE’s focus on smart cities and renewable energy developments—such as solar parks and desalination plants—is creating strong fabrication demand for structural components and enclosures. South Africa is witnessing demand from mining equipment and power generation projects. Regional governments are also forming trade partnerships and updating regulatory frameworks to facilitate industrial growth. Technological modernization is underway, particularly through partnerships with international firms introducing advanced CNC and robotic welding technologies. The market is also being supported by investments in vocational training and technical education, which aim to build a skilled labor base for precision fabrication and assembly services.

United States – 28.4% Market Share

Strong demand from aerospace, defense, and automotive sectors, coupled with robust domestic manufacturing capacity and government support.

China – 24.6% Market Share

High-volume manufacturing, cost-effective labor, and expansive industrial infrastructure make China a global fabrication hub.

The global sheet metal fabrication services market is highly competitive, comprising over 350 active companies operating at local, regional, and international levels. The landscape is fragmented, with a mix of small-to-medium enterprises and a few large-scale players that dominate high-volume industrial contracts. Competitive positioning is increasingly influenced by capabilities in advanced manufacturing technologies such as automated laser cutting, robotic welding, and CNC machining. Companies with integrated design-to-fabrication solutions and strong supply chain networks tend to have a strategic edge. Strategic initiatives like mergers and acquisitions, long-term OEM partnerships, and geographic expansions have intensified in the past two years. For example, several fabricators have entered joint ventures with aerospace and automotive OEMs to deliver localized and customized solutions. Additionally, there is growing competition around digital transformation, with companies leveraging CAD/CAM integration, IoT-enabled monitoring systems, and real-time fabrication tracking to improve turnaround times and reduce operational inefficiencies. As sustainability becomes a differentiator, some players are also shifting to low-emission manufacturing and recyclable materials. Innovation in tooling, material processing, and lean operations continues to redefine the competitive dynamics of the market.

O’Neal Manufacturing Services

BTD Manufacturing, Inc.

Kapco Metal Stamping

Standard Iron & Wire Works, Inc.

Mayville Engineering Company, Inc.

Noble Industries, Inc.

Moreng Metal Products

Marlin Steel Wire Products LLC

Dynamic Aerospace and Defense Group

Metcam Inc.

Technological advancements are significantly reshaping the sheet metal fabrication services market, with manufacturers adopting both automation and digitalization to enhance productivity and precision. One of the most transformative trends is the widespread deployment of CNC (Computer Numerical Control) systems, which now control over 70% of fabrication equipment globally. CNC-enabled laser cutting, punching, and bending operations offer enhanced repeatability, speed, and material utilization.

Robotic welding systems are becoming standard in high-volume operations, particularly in the automotive and appliance manufacturing sectors. These systems improve welding precision, reduce labor dependence, and lower defect rates. The integration of CAD/CAM software is enabling real-time design modifications and seamless transitions from prototyping to production.

Another key development is the rise of fiber laser technology, which is gradually replacing CO₂ lasers due to its higher energy efficiency and cutting speed. Additionally, 3D printing is gaining traction for complex sheet metal prototypes and tooling components, particularly in aerospace and medical industries.

IoT (Internet of Things) and Industry 4.0 technologies are now incorporated into fabrication systems for remote monitoring, predictive maintenance, and data analytics, driving operational efficiency. Smart sensors, when embedded in equipment, provide insights into tool wear and machine performance, reducing downtime and improving quality assurance. The shift toward green fabrication is also fostering innovations in energy-efficient machinery and eco-friendly surface treatment processes, making technology a critical differentiator in the evolving market.

• In April 2024, Noble Industries installed a new high-speed fiber laser cutting machine capable of processing materials at rates up to 150 m/min, enhancing its capacity to serve the electronics and telecommunications sectors.

• In February 2024, Mayville Engineering Company expanded its contract manufacturing capabilities with a new 100,000 sq. ft. facility in Ohio, focused on serving growing demand from the off-highway and defense industries.

• In December 2023, Dynamic Aerospace and Defense Group launched a fully automated robotic cell for high-precision aerospace components, reducing cycle times by 40% and improving compliance with tight tolerance requirements.

• In July 2023, Metcam introduced an in-house powder coating line integrated with smart sensors for quality control, resulting in a 25% reduction in material waste and improved coating consistency across fabricated metal panels.

The Sheet Metal Fabrication Services Market Report provides a comprehensive analysis of the global industry, covering diverse market segments, geographic regions, technological trends, and end-user industries. The report segments the market based on process type (cutting, forming, welding, assembly, finishing), material type (aluminum, steel, copper, others), and end-use industries including automotive, aerospace, construction, electronics, and energy.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with in-depth assessments of leading and emerging markets such as the United States, China, Germany, India, and Brazil. The scope extends to analyzing market dynamics, demand shifts, and fabrication intensity across various sectors.

Emerging areas such as smart fabrication technologies, sustainable processing, and on-demand manufacturing models are explored to highlight growth opportunities. The report also considers innovations in equipment automation, integration of IoT systems, and advanced CAD/CAM capabilities that are reshaping production workflows. Additionally, the report evaluates industry trends related to reshoring, digital supply chains, and mass customization.

This business-oriented report is structured to support strategic decisions by providing insights into operational capabilities, regional competitiveness, technology adoption rates, and evolving client needs across the global sheet metal fabrication services landscape.

| Report Attribute / Metric | Report Details |

|---|---|

| Market Revenue (2024) | USD 1,030.0 Million |

| Market Revenue (2032) | USD 1,409.6 Million |

| CAGR (2025–2032) | 4.0% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | O’Neal Manufacturing Services, BTD Manufacturing, Inc., Kapco Metal Stamping, Standard Iron & Wire Works, Inc., Mayville Engineering Company, Inc., Noble Industries, Inc., Moreng Metal Products, Marlin Steel Wire Products LLC, Dynamic Aerospace and Defense Group, Metcam Inc. |

| Customization & Pricing | Available on Request (10% Customization is Free) |