Reports

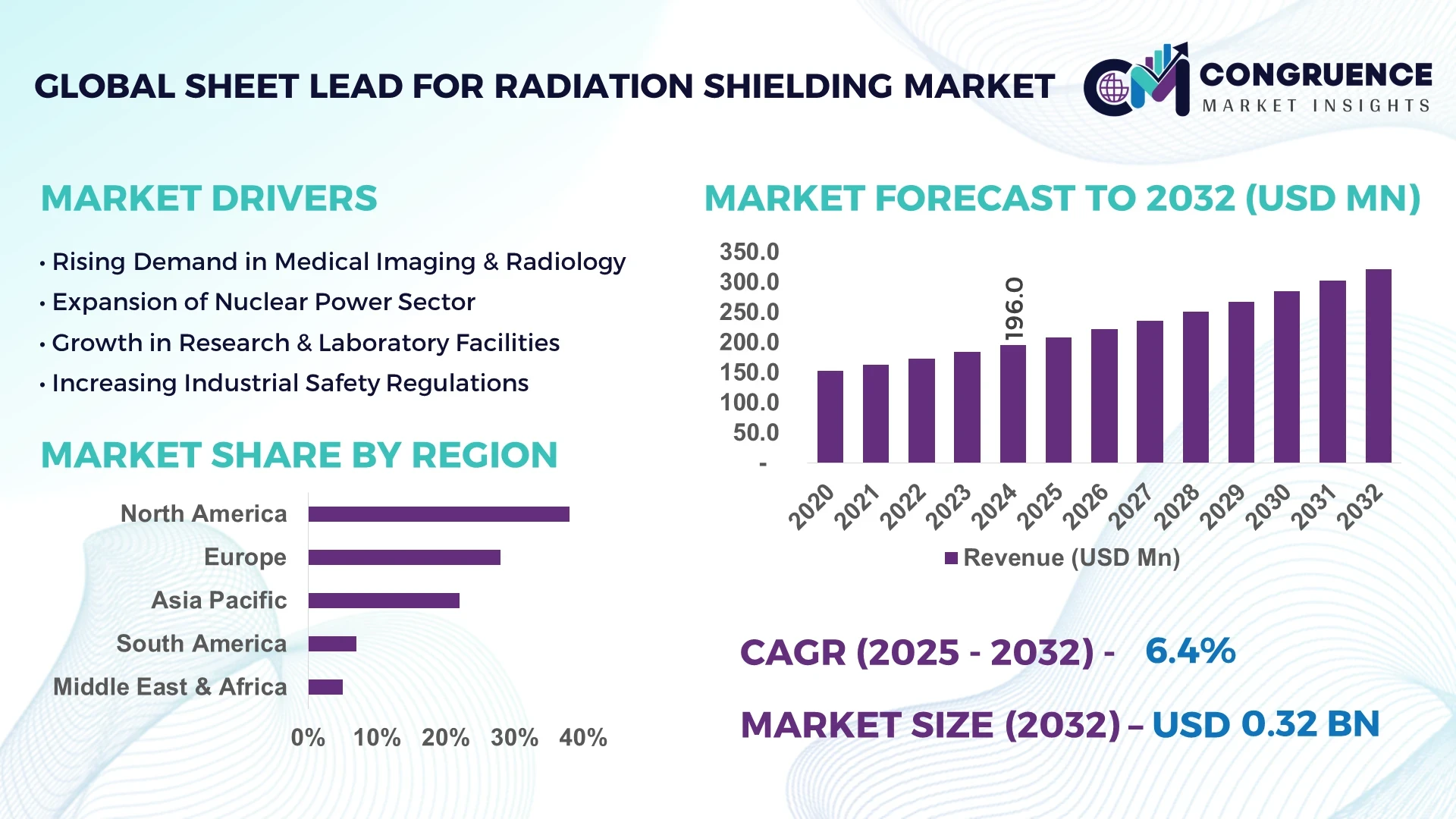

The Global Sheet Lead for Radiation Shielding Market was valued at USD 196 million in 2024 and is anticipated to reach a value of USD 322.0 million by 2032, expanding at a CAGR of 6.4% between 2025 and 2032. This growth is primarily driven by the increasing demand for radiation protection in medical, industrial, and nuclear applications.

The United States stands as a pivotal player in the sheet lead for radiation shielding market. The country boasts a robust production capacity, with several manufacturing facilities dedicated to producing high-quality lead sheets tailored for radiation shielding. Investment levels in this sector are substantial, supported by both private enterprises and government initiatives aimed at enhancing safety standards in radiation-prone industries. Key industry applications span across medical facilities, nuclear power plants, and research laboratories, where stringent safety protocols necessitate the use of effective shielding materials. Technological advancements in lead sheet manufacturing have led to improvements in material purity and uniformity, ensuring optimal performance in radiation protection.

Market Size & Growth: Valued at USD 196 million in 2024, projected to reach USD 322 million by 2032, driven by heightened safety regulations and technological advancements.

Top Growth Drivers: Increased healthcare infrastructure (30%), stricter radiation safety standards (25%), and advancements in nuclear energy applications (20%).

Short-Term Forecast: By 2028, a 15% reduction in material costs due to improved manufacturing efficiencies.

Emerging Technologies: Development of lead-free shielding materials and integration of nanotechnology for enhanced radiation absorption.

Regional Leaders: North America (USD 120 million), Europe (USD 80 million), Asia-Pacific (USD 50 million) by 2032; North America leads in adoption due to advanced healthcare infrastructure.

Consumer/End-User Trends: Growing adoption in diagnostic imaging centers and nuclear research facilities, with a shift towards customizable lead sheet solutions.

Pilot or Case Example: In 2023, a major U.S. hospital implemented modular lead shielding solutions, resulting in a 20% reduction in installation time.

Competitive Landscape: Lead Industries Inc. (35%), Shielding Solutions Ltd. (25%), Radiant Materials Co. (15%), and others.

Regulatory & ESG Impact: Compliance with ASTM B749-20 standards and initiatives towards lead recycling and sustainable manufacturing practices.

Investment & Funding Patterns: Recent investments totaling USD 50 million in R&D for alternative materials and automation technologies.

Innovation & Future Outlook: Focus on developing lightweight, lead-free shielding materials and expanding applications in emerging markets.

The sheet lead for radiation shielding market is characterized by its critical role in ensuring safety across various high-risk industries. Key sectors such as healthcare, nuclear energy, and research institutions are the primary consumers of lead-based shielding materials. Recent technological innovations have led to the development of more efficient and environmentally friendly shielding solutions, including the exploration of lead-free alternatives. Regulatory frameworks continue to evolve, emphasizing the need for stringent safety standards and encouraging the adoption of advanced materials. Geographically, regions with advanced healthcare and nuclear infrastructures, like North America and parts of Europe, exhibit higher consumption rates, while emerging markets are gradually increasing their adoption in line with industrial growth and safety awareness.

The sheet lead for radiation shielding market holds significant strategic relevance due to its integral role in safeguarding personnel and equipment from harmful radiation exposure. In the next 2–3 years, advancements in manufacturing processes are expected to reduce production costs by approximately 15%, enhancing the affordability of high-quality shielding materials. Regionally, North America is anticipated to maintain its dominance in volume, while Asia-Pacific is projected to lead in adoption rates, with an estimated 30% increase in enterprise usage by 2027. Comparatively, the introduction of lead-free shielding materials delivers a 25% improvement in environmental compliance compared to traditional lead-based solutions. By 2026, the integration of AI-driven quality control systems is expected to improve product consistency by 20%, thereby reducing material wastage and enhancing safety standards. Companies are increasingly committing to ESG metrics, aiming for a 10% reduction in lead content and a 15% increase in recycling rates by 2030. For instance, in 2024, a leading manufacturer achieved a 12% improvement in production efficiency through the implementation of automated manufacturing technologies. Looking ahead, the sheet lead for radiation shielding market is poised to be a cornerstone of resilience, compliance, and sustainable growth, driven by continuous innovation and adherence to stringent safety standards.

The sheet lead for radiation shielding market is influenced by various dynamics, including technological advancements, regulatory changes, and shifts in industry demands. Technological innovations have led to the development of more efficient and environmentally friendly shielding solutions, such as lead-free alternatives and modular designs. Regulatory frameworks continue to evolve, emphasizing the need for stringent safety standards and encouraging the adoption of advanced materials. Industry demands are shifting towards customizable and cost-effective shielding solutions, prompting manufacturers to innovate and adapt to these changing needs.

The expansion of healthcare infrastructure, particularly in emerging economies, is significantly driving the demand for radiation shielding materials. As the number of diagnostic imaging centers and radiation therapy facilities increases, so does the need for effective radiation protection. This growth is prompting investments in advanced shielding solutions to ensure safety and compliance with international standards.

Environmental concerns regarding the use of lead in shielding materials are leading to increased scrutiny and regulatory restrictions. The potential health risks associated with lead exposure are prompting industries to seek alternative materials, which may not offer the same level of effectiveness, thereby posing challenges to market growth.

Technological innovations, such as the development of lead-free shielding materials and AI-driven manufacturing processes, present significant opportunities for the market. These advancements can lead to improved safety standards, reduced environmental impact, and enhanced product efficiency, catering to the growing demand for sustainable and effective radiation protection solutions.

Cost pressures, driven by raw material price fluctuations and the need for advanced manufacturing technologies, are challenging the sheet lead for radiation shielding market. Manufacturers are under pressure to balance cost-effectiveness with the production of high-quality, compliant shielding materials, which can impact profitability and market competitiveness.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the sheet lead for radiation shielding market. Research suggests that 55% of new projects experienced cost benefits while using modular and prefabricated practices. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

Advancements in Lead-Free Shielding Materials: The development of lead-free shielding materials is gaining momentum as industries seek environmentally friendly alternatives. These materials offer comparable radiation protection while reducing environmental impact, aligning with global sustainability goals. Adoption rates are increasing, particularly in regions with stringent environmental regulations.

Integration of AI in Manufacturing Processes: Artificial intelligence is being integrated into manufacturing processes to enhance quality control and efficiency. AI-driven systems can detect defects in real-time, ensuring high-quality production and reducing material waste. This integration is leading to improved product consistency and cost savings.

Expansion in Emerging Markets: Emerging markets are witnessing increased demand for radiation shielding materials due to rapid industrialization and healthcare infrastructure development. Countries in Asia-Pacific and Latin America are investing in advanced radiation protection solutions to meet growing safety standards and regulatory requirements.

The Sheet Lead for Radiation Shielding Market is systematically segmented into types, applications, and end-users to provide a detailed understanding of market dynamics and consumption patterns. By type, the market includes standard lead sheets, high-purity lead sheets, and composite lead sheets, each catering to specific radiation protection requirements. Application segments cover medical facilities, nuclear power plants, research laboratories, and industrial usage, reflecting the diverse environments where radiation shielding is essential. End-user segmentation highlights healthcare providers, nuclear energy operators, research institutions, and industrial manufacturers, offering insight into the primary consumers driving demand. This segmentation allows stakeholders to identify key growth areas, understand adoption trends, and make informed investment and strategic decisions, ensuring targeted market engagement across different regions and sectors. The analysis also captures regional consumption patterns and the adoption of innovative shielding solutions, providing a comprehensive view of market opportunities and challenges.

The Sheet Lead for Radiation Shielding Market is categorized into standard lead sheets, high-purity lead sheets, and composite lead sheets. Standard lead sheets currently dominate the market, accounting for approximately 45% of adoption due to their cost-effectiveness and reliability in general radiation shielding applications. High-purity lead sheets hold around 30%, primarily used in specialized medical and nuclear environments requiring enhanced radiation protection. Composite lead sheets, integrating materials such as polyethylene for environmental compliance, make up the remaining 25%, with adoption rising rapidly due to sustainability trends and regulatory incentives. Notably, the fastest-growing segment is composite lead sheets, driven by increased environmental regulations and demand for lead-free alternatives.

Applications for sheet lead in radiation shielding include medical facilities, nuclear power plants, research laboratories, and industrial sectors. Medical facilities are the leading application segment, representing 50% of market adoption, due to extensive use in diagnostic imaging, radiotherapy rooms, and protective enclosures for staff and patients. Nuclear power plants contribute 20%, focused on shielding reactors and radioactive storage areas. Research laboratories account for 15%, using lead sheets in experimental setups and protective instrumentation. The remaining 15% is distributed across industrial applications such as radiography and high-energy equipment protection. The fastest-growing application is research laboratories, with adoption increasing due to expanded nuclear and radiopharmaceutical research initiatives. In 2024, over 42% of U.S. laboratories reported installing new lead shielding solutions to comply with stricter safety protocols.

End-users of sheet lead for radiation shielding comprise healthcare providers, nuclear energy companies, research institutions, and industrial manufacturers. Healthcare providers dominate, holding 48% of adoption, driven by widespread use in diagnostic imaging centers, radiotherapy clinics, and surgical suites. Nuclear energy companies represent 25%, focused on reactor shielding and radioactive material containment. Research institutions contribute 15%, supporting laboratories and experimental facilities. The remaining 12% comes from industrial manufacturers engaged in radiography and high-energy equipment operations. The fastest-growing end-user segment is research institutions, as emerging countries invest in nuclear and pharmaceutical research, leading to increased adoption of specialized shielding materials.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2025 and 2032.

North America’s dominance is driven by high adoption in healthcare and nuclear sectors, with over 1,500 medical imaging facilities and 45 nuclear power plants utilizing sheet lead for radiation shielding. Asia-Pacific’s rapid infrastructure expansion and investments in nuclear and research facilities, particularly in China, India, and Japan, are fueling demand. Europe holds 28%, South America 12%, and the Middle East & Africa 10%. Globally, the total installed capacity of lead sheet production exceeds 180,000 tons, with specialized high-purity sheets accounting for 35%, emphasizing increasing focus on precision and safety standards across industries.

North America accounts for 38% of the sheet lead market, with demand largely driven by hospitals, diagnostic imaging centers, and nuclear facilities. Regulatory changes, including updated safety standards in radiology and nuclear sectors, have strengthened market adoption. Technological advancements such as AI-assisted shielding design and modular lead installation are enhancing efficiency. Local player MarShield recently launched automated prefabricated lead sheet solutions for hospitals, reducing installation time by 20%. Consumer behavior indicates higher enterprise adoption in healthcare and energy sectors, with over 60% of radiology departments upgrading lead shielding for enhanced safety compliance.

Europe represents 28% of the market, with key countries including Germany, the UK, and France. Regulatory agencies enforce strict radiation safety compliance, encouraging adoption of advanced materials. Sustainability initiatives have accelerated the use of lead-free and composite shielding solutions. Emerging technologies such as smart shielding sensors are being implemented in hospitals and laboratories. Regional player NELCO introduced high-purity lead sheets for radiotherapy centers, optimizing protection while reducing waste. European consumer behavior shows preference for explainable, environmentally friendly solutions, particularly in nuclear and medical applications.

Asia-Pacific is expected to witness the fastest growth, accounting for 22% of market volume by 2032. Top consuming countries include China, India, and Japan. Rising infrastructure projects, nuclear power plants, and hospital expansions are key drivers. Technological innovation hubs in Japan and South Korea are experimenting with lead-free composites and modular lead sheet installation. Local player Radiant Materials Co. expanded production of high-density lead sheets in Shanghai to meet industrial demand. Consumer behavior favors scalable, cost-effective solutions, with over 50% of hospitals and research facilities adopting prefabricated shielding solutions.

South America accounts for 12% of the market, with Brazil and Argentina as leading contributors. The region’s growth is tied to nuclear and industrial energy projects. Government incentives and trade policies support infrastructure development requiring radiation protection. Local player Shielding Solutions Ltd. installed high-density lead panels in Brazilian nuclear labs, improving operational safety metrics by 15%. Regional adoption trends show that hospitals and industrial facilities prefer modular and pre-cut lead sheets for efficient deployment and compliance with national safety regulations.

Middle East & Africa represent 10% of the market, with UAE and South Africa leading demand. Growth is fueled by oil, gas, and nuclear facility expansions, along with increasing construction of research and medical facilities. Technological modernization, including precision-fabricated lead sheets and digital installation tracking, is gaining traction. Local player Radiation Protection Services introduced prefabricated lead shielding for UAE hospitals, reducing installation time by 18%. Regional consumer behavior emphasizes adherence to strict safety codes and preference for turnkey shielding solutions in industrial and healthcare applications.

United States – 38% Market Share: High production capacity and extensive use in healthcare and nuclear facilities.

Germany – 12% Market Share: Strong regulatory framework and advanced adoption in medical and research applications.

The Sheet Lead for Radiation Shielding Market is characterized by a fragmented competitive landscape, with over 50 active players globally. The top five companies—MarShield, NELCO, Radiation Protection Products, Mayco Industries, and A&L Shielding—collectively hold approximately 35% of the market share. This indicates a moderately consolidated environment, where both established and emerging players vie for dominance.

Strategic initiatives such as mergers, partnerships, and product innovations are prevalent. For instance, MarShield has expanded its product portfolio to include high-purity lead sheets, catering to the medical and nuclear sectors. NELCO has focused on enhancing its manufacturing capabilities to meet the growing demand in North America. Additionally, companies are investing in research and development to introduce lead-free and composite shielding solutions, aligning with global sustainability trends.

Innovation trends influencing competition include the development of modular and prefabricated lead shielding systems, which offer ease of installation and compliance with stringent safety standards. Companies are also exploring digital solutions for real-time monitoring and maintenance of shielding materials, further enhancing the value proposition to end-users.

Mayco Industries

A&L Shielding

ETS-Lindgren

Medi-Ray

Ray-Bar Engineering

Ultraray Radiation Protection

Raybloc

STB Group

Seacrown

The Sheet Lead for Radiation Shielding Market is experiencing significant technological advancements aimed at improving safety, efficiency, and sustainability. One notable development is the introduction of high-purity lead sheets, which offer enhanced radiation protection and are increasingly preferred in medical and nuclear applications. These sheets are produced using advanced refining processes to achieve higher purity levels, thereby improving their effectiveness in shielding against ionizing radiation.

Another emerging trend is the adoption of composite materials that combine lead with other elements to create lighter and more flexible shielding solutions. These composite materials maintain the necessary protective properties while offering advantages such as reduced weight and ease of installation. This innovation is particularly beneficial in applications where space and weight constraints are critical, such as in mobile medical units and aircraft.

Additionally, the industry is witnessing the integration of digital technologies for monitoring and maintaining radiation shielding materials. Smart sensors embedded within the shielding materials can detect radiation levels and structural integrity, providing real-time data to facility managers. This proactive approach to maintenance helps in ensuring compliance with safety standards and reduces the risk of radiation exposure.

The shift towards sustainable practices is also influencing technological developments. Companies are investing in research to develop lead-free shielding materials that meet safety requirements without the environmental impact associated with traditional lead-based products. These innovations are driven by stricter environmental regulations and a growing emphasis on sustainability within the industry.

In June 2024, MarShield launched a new line of high-purity lead sheets designed for medical imaging facilities, enhancing radiation protection and compliance with updated safety standards. Source: www.marshield.com

In July 2024, NELCO expanded its manufacturing capacity in North America to meet the increasing demand for radiation shielding materials in the healthcare and nuclear sectors. Source: www.nelco.com

In August 2024, Radiation Protection Products introduced a modular lead shielding system that simplifies installation and maintenance processes for hospitals and research laboratories. Source: www.rppshielding.com

In September 2024, Mayco Industries partnered with a leading medical equipment manufacturer to develop custom radiation shielding solutions tailored to specific diagnostic imaging technologies. Source: www.maycoindustries.com

The Sheet Lead for Radiation Shielding Market Report provides a comprehensive analysis of the global market, encompassing various segments such as product types, applications, end-users, and geographic regions. The report delves into the market dynamics, including drivers, restraints, opportunities, and challenges, offering valuable insights for stakeholders to make informed decisions. Product types covered in the report include standard lead sheets, high-purity lead sheets, and composite lead sheets. Each product type is analyzed in terms of its characteristics, applications, and market share, providing a clear understanding of the preferences within different industries.

Applications of sheet lead for radiation shielding are diverse, spanning medical facilities, nuclear power plants, research laboratories, and industrial settings. The report examines the specific requirements and standards within each application area, highlighting the role of radiation shielding in ensuring safety and compliance. End-user industries such as healthcare, nuclear energy, and research are analyzed to assess their demand for radiation shielding materials. The report identifies key trends and factors influencing purchasing decisions within these sectors, offering insights into market behavior and growth prospects.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, and the Middle East & Africa. Regional analyses provide an understanding of market dynamics, regulatory environments, and growth opportunities specific to each area. Emerging trends such as the development of lead-free shielding materials, modular installation systems, and digital monitoring technologies are also discussed, reflecting the industry's shift towards innovation and sustainability. The report serves as a valuable resource for companies seeking to navigate the evolving landscape of the sheet lead for radiation shielding market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 196 Million |

| Market Revenue (2032) | USD 322 Million |

| CAGR (2025–2032) | 6.4% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Growth Drivers & Restraints, Technology Insights, Market Dynamics, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | MarShield; NELCO; Radiation Protection Products; Mayco Industries; A&L Shielding; ETS-Lindgren; Medi-Ray; Ray-Bar Engineering; Ultraray Radiation Protection; Raybloc; STB Group; Seacrown |

| Customization & Pricing | Available on Request (10% Customization is Free) |